Global Diaphragm Pump Market Size, Share, Growth Analysis By Operation (Double Acting, Single Acting), By Mechanism (Air Operated, Electrically Operated), By Discharge Pressures (Up to 80 Bar, 80 to 200 Bar, Above 200 Bar), By End-Use Industry (Water Treatment, Oil and Gas, Chemical, Pharmaceutical, Food and Beverage, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180920

- Number of Pages: 294

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

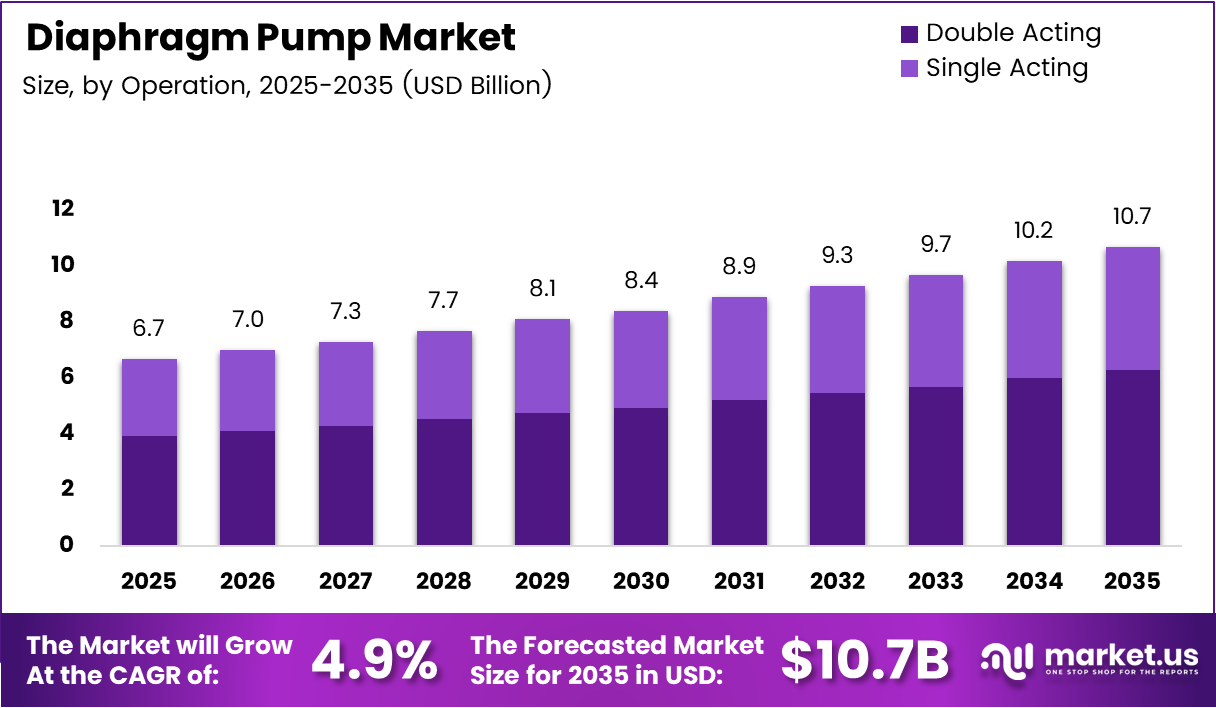

Global Diaphragm Pump Market size is expected to be worth around USD 10.7 Billion by 2035 from USD 6.7 Billion in 2025, growing at a CAGR of 4.9% during the forecast period 2026 to 2035.

Diaphragm pumps transfer fluids using a flexible membrane driven by air pressure or an electric motor. Industries choose them for their leak-free design and ability to handle abrasive, viscous, and chemically aggressive fluids. This structural advantage makes them irreplaceable in applications where seal failure carries regulatory or safety consequences.

Chemical processing, pharmaceutical manufacturing, wastewater treatment, and food production all rely on diaphragm pumps for safe fluid handling. The breadth of end-use coverage means demand tracks global industrial output, not a single sector cycle. Consequently, the market holds resilience that single-application pump categories cannot match.

Air-operated double diaphragm pumps dominate current installations, but electrically operated variants are gaining traction as energy costs pressure plant operators to cut compressed-air consumption. This technology shift creates a replacement cycle within the installed base, generating upgrade revenue on top of new-installation growth.

Government environmental mandates in water treatment and chemical handling are tightening discharge standards worldwide. Operators upgrading legacy systems to meet these standards must replace older pump technologies with contained, zero-leak solutions — a structural demand signal that will sustain procurement activity through the forecast period.

In September 2025, ARO (Ingersoll Rand) launched the EVO 210 electric diaphragm pump, eliminating compressed air requirements while adding built-in safety features. This launch signals that leading manufacturers are accelerating the shift toward electric platforms, compressing the timeline for AODD-to-electric transitions across industrial facilities.

According to Graco, the QUANTM electric double diaphragm pump achieves up to 80% greater energy efficiency than traditional pumps. That performance gap translates directly into operating cost reduction, making the upgrade economics compelling for high-utilization facilities and accelerating replacement cycles across process industries.

According to Cognito Pump, EODD pumps reduce energy consumption by up to 75% compared to pneumatic technologies. When plant operators calculate total cost of ownership over a five-year period, this saving reverses the higher upfront cost argument, removing one of the primary adoption barriers for electric diaphragm systems.

Key Takeaways

- The Global Diaphragm Pump Market was valued at USD 6.7 Billion in 2025.

- The market is forecast to reach USD 10.7 Billion by 2035, at a CAGR of 4.9%.

- By Operation, Double Acting held the dominant share at 58.7% in 2025.

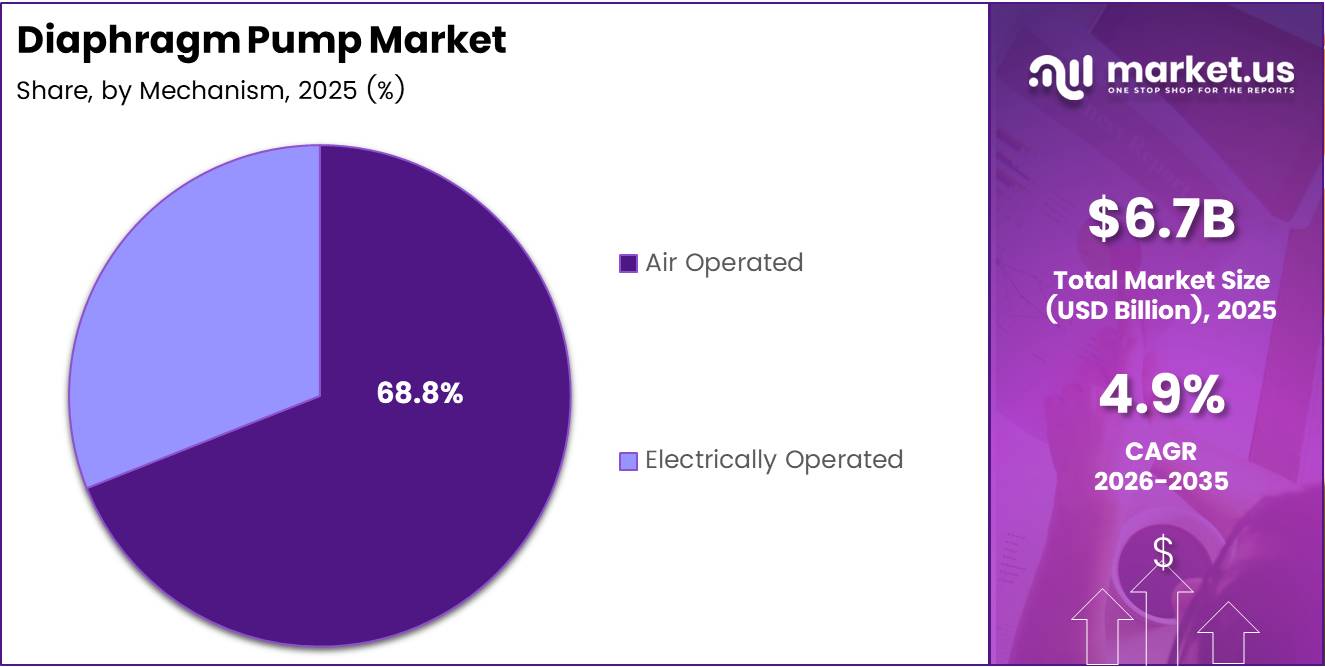

- By Mechanism, Air Operated led with a 68.8% share in 2025.

- By Discharge Pressures, the Up to 80 Bar segment accounted for 46.7% share in 2025.

- By End-Use Industry, Water Treatment led with a 24.5% share in 2025.

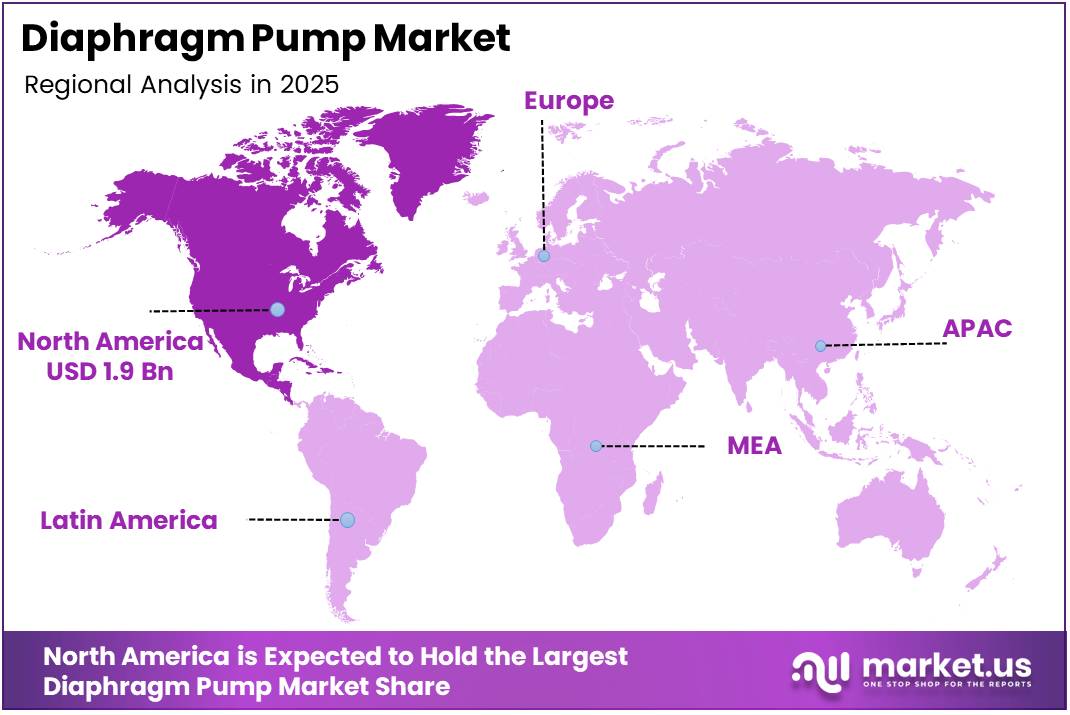

- North America dominated regionally with a 28.9% share, valued at USD 1.9 Billion in 2025.

Operation Analysis

Double Acting dominates with 58.7% due to continuous flow and higher output efficiency.

In 2025, Double Acting held a dominant market position in the By Operation segment of the Diaphragm Pump Market, with a 58.7% share. Double acting pumps deliver fluid on both strokes, producing continuous flow that single acting units cannot match. This output consistency makes them the default specification for high-volume industrial and process applications.

Single Acting pumps serve as the preferred choice where simplicity and lower initial cost outweigh throughput requirements. Their simpler construction reduces maintenance touchpoints, making them suitable for intermittent-duty cycles in smaller facilities. However, their share reflects a niche positioning rather than broad industrial preference, as process plants consistently prioritize continuous-flow capability.

Mechanism Analysis

Air Operated dominates with 68.8% due to established infrastructure and intrinsic safety compliance.

In 2025, Air Operated held a dominant market position in the By Mechanism segment of the Diaphragm Pump Market, with a 68.8% share. Compressed air infrastructure already exists across most manufacturing and processing facilities, reducing installation costs for AODD pumps. Additionally, their spark-free operation satisfies ATEX and hazardous-area regulations without additional engineering — a compliance advantage that sustains their dominance in chemical and oil and gas plants.

Electrically Operated pumps carry the strongest growth momentum within the mechanism segment. Plant operators facing rising compressed air costs and tightening carbon reporting requirements are actively evaluating electric alternatives. The gap between air operated and electrically operated share will narrow as energy cost pressures intensify and new electric models achieve feature parity with established AODD platforms.

Discharge Pressures Analysis

Up to 80 Bar dominates with 46.7% due to broad compatibility across general industrial applications.

In 2025, Up to 80 Bar held a dominant market position in the By Discharge Pressures segment of the Diaphragm Pump Market, with a 46.7% share. Most water treatment, food processing, and general chemical transfer applications operate comfortably within this pressure range. The wide applicability across multiple end-use industries consolidates volume in this tier, giving vendors serving standard-pressure requirements access to the broadest addressable base.

80 to 200 Bar pumps address more demanding process environments including high-pressure chemical injection and oil and gas applications. This segment commands premium pricing because fewer manufacturers offer validated designs at these pressures, creating defensible margin positions for specialized producers. Growth in upstream energy and chemical processing will pull this segment upward over the forecast period.

Above 200 Bar represents the narrowest but most technically differentiated segment within the pressure range classification. These units serve ultra-high-pressure applications including certain hydrocarbon processing and specialty chemical injection tasks. The small number of qualified manufacturers and the stringent material and certification requirements create high barriers, but also limit volume scale for suppliers competing here.

End-Use Industry Analysis

Water Treatment dominates with 24.5% due to mandatory pump replacement driven by environmental compliance.

In 2025, Water Treatment held a dominant market position in the By End-Use Industry segment of the Diaphragm Pump Market, with a 24.5% share. Regulatory mandates governing chemical dosing, sludge handling, and effluent discharge require leak-proof pumping solutions. Diaphragm pumps meet these containment requirements natively, making them the specified technology for municipal and industrial water treatment infrastructure worldwide.

Oil and Gas operations use diaphragm pumps for chemical injection, produced water transfer, and metering applications where containment and chemical compatibility are non-negotiable. Offshore and onshore installations both require ATEX-rated equipment, and AODD pumps satisfy this requirement without supplementary electrical systems. Capital spending cycles in upstream energy directly influence this segment’s procurement volumes.

Chemical processing facilities represent a technically demanding end-use where fluid aggressiveness and containment requirements rule out most alternative pump technologies. Diaphragm pumps handle corrosive acids, solvents, and slurries that would destroy seal-dependent alternatives. This application criticality translates into higher unit values and longer approved vendor lists, giving established pump suppliers pricing leverage in this segment.

Pharmaceutical manufacturing demands hygienic fluid transfer with full traceability and cleanability. Diaphragm pumps meet FDA and GMP standards without contamination risk because the fluid path never contacts mechanical seals or lubricants. Regulatory scrutiny in drug manufacturing therefore functions as a procurement driver rather than a barrier, directing buyers toward diaphragm technology by default.

Food and Beverage production requires pumps that handle viscous products — from sauces and pastes to beverages — without shear damage or contamination. Diaphragm pumps deliver gentle, low-shear transfer that preserves product integrity, satisfying both quality and food safety audit requirements. Expansion of packaged food production in emerging markets extends the addressable buyer base for this segment.

Others encompasses mining, pulp and paper, and construction dewatering applications. These uses prioritize slurry-handling capability and portability over precision dosing. Compact and portable diaphragm pump formats serve field and mobile operations in this group, creating a product category distinct from fixed industrial installations in the primary end-use segments above.

Key Market Segments

By Operation

- Double Acting

- Single Acting

By Mechanism

- Air Operated

- Electrically Operated

By Discharge Pressures

- Up to 80 Bar

- 80 to 200 Bar

- Above 200 Bar

By End-Use Industry

- Water Treatment

- Oil and Gas

- Chemical

- Pharmaceutical

- Food and Beverage

- Others

Drivers

Stringent Containment and Hygiene Requirements Force Diaphragm Pump Adoption Across Process Industries

Chemical processing plants, pharmaceutical facilities, and food manufacturers all operate under regulations that prohibit fluid leakage and contamination. Diaphragm pumps satisfy these requirements by design — the flexible membrane isolates process fluid from mechanical components entirely. This structural compliance advantage removes specification risk for procurement engineers, making diaphragm pumps the lowest-risk purchase decision in regulated applications.

Wastewater treatment operators face tightening discharge standards that require precise chemical dosing for pH control and disinfection. Diaphragm pumps deliver the accurate, repeatable metering these processes demand. In April 2025, Graco unveiled major enhancements to its QUANTM electric double diaphragm pump line, including a new 480V input range and XTREME TORQUE™ motor technology — evidence that leading vendors are investing to deepen performance in exactly these high-precision treatment applications.

According to PSG Dover, Wilden Chem-Fuse diaphragms last 2 to 3 times longer than traditional diaphragms. Extended service life directly reduces unplanned downtime and maintenance labor costs — two factors that dominate total cost of ownership calculations for plant engineers. Longer diaphragm life strengthens the business case for diaphragm technology over competing pump designs in continuous-duty process environments.

Restraints

Pressure and Flow Ceilings Restrict Diaphragm Pump Use in Heavy Industrial Pumping Tasks

Diaphragm pumps lose competitiveness in applications requiring sustained high-pressure output above 200 bar or very high volumetric flow rates. Centrifugal and positive displacement alternatives outperform them on both metrics at scale. This ceiling limits diaphragm pump penetration in segments like large-scale oil transfer, high-volume cooling water circulation, and certain power generation applications where throughput requirements exceed membrane-driven design limits.

Continuous-duty operations accelerate diaphragm fatigue and valve wear, raising maintenance frequency and spare parts consumption compared to less complex pump types. Facilities running pumps around the clock face higher lifecycle costs than intermittent-use installations. In December 2024, GODO PUMPS launched its new Electric Diaphragm Pump with Pressure Relief Controller at CHINACOAT 2024, signaling that manufacturers recognize pressure management as an active engineering challenge requiring dedicated product development.

According to Ingersoll Rand/ARO, electric diaphragm pumps use 40% less electricity than the best pneumatic equivalents at equivalent flow and pressure. This figure confirms that energy inefficiency remains a documented cost burden for facilities still running pneumatic units. The performance gap gives operators a measurable reason to replace existing AODD installations, but the capital replacement cost slows adoption — particularly among mid-sized industrial buyers with constrained maintenance budgets.

Growth Factors

IoT Integration and Emerging Market Industrialization Open New Revenue Streams for Diaphragm Pump Suppliers

Industrial facilities increasingly embed sensors and connectivity into pump systems to enable real-time condition monitoring and predictive maintenance scheduling. Diaphragm pump suppliers who integrate IoT capability into their platforms can offer service contracts and data subscriptions alongside hardware, shifting revenue from one-time equipment sales to recurring streams. This business model transition benefits suppliers with established installed bases and direct customer relationships.

Renewable energy facilities and biofuel production plants require precise chemical handling for processes including feedstock transfer, acid washing, and catalyst dosing. These applications match the diaphragm pump’s core capability profile. In August 2025, Circor International acquired two Indian pump manufacturers — Swelore Engineering and Hiro Nisha Systems — adding diaphragm metering and dosing packages specifically to serve industrializing markets where energy infrastructure investment is accelerating.

According to Graco, the QUANTM electric double diaphragm pump delivers return on investment within 12 months in typical industrial applications. A sub-twelve-month payback period removes the financial objection that delays capital equipment purchases. When buyers can demonstrate this ROI internally, procurement approval timelines shorten — which directly converts market opportunity into confirmed orders faster than longer-payback alternatives.

Emerging Trends

Advanced Diaphragm Materials and Electric Platforms Redefine Performance Standards in Fluid Transfer

Manufacturers now develop elastomer and PTFE diaphragm compounds engineered for specific chemical environments rather than general-purpose resistance. This materials specialization allows pumps to handle aggressive fluids — including titanium dioxide slurries and concentrated solvents — without accelerated degradation. Buyers in chemical and pharmaceutical applications increasingly specify material certification as a procurement requirement, raising the technical bar for new market entrants.

Compact and portable diaphragm pump formats address field operations in mining, construction, and environmental remediation where fixed infrastructure does not exist. This form-factor trend creates a product category that competes on mobility rather than throughput, opening buyer segments that stationary industrial pumps cannot serve. Suppliers offering both fixed and portable platforms extend their addressable market without cannibalizing core industrial sales.

According to Ovell Pump, switching to aluminum diaphragm pumps in ink manufacturing delivers a 20% increase in production efficiency through stable fluid flow. That efficiency gain reflects a broader shift — buyers now evaluate diaphragm pump performance against production output metrics, not just pump specifications. Suppliers who document application-specific performance outcomes gain a competitive advantage in technical sales cycles where procurement decisions require measurable business justification.

Regional Analysis

North America Dominates the Diaphragm Pump Market with a Market Share of 28.9%, Valued at USD 1.9 Billion

North America holds a 28.9% share of the global diaphragm pump market, valued at USD 1.9 Billion in 2025. The region’s mature water treatment infrastructure, active chemical processing sector, and stringent EPA and OSHA containment regulations collectively drive procurement volumes. Early adoption of electric diaphragm pump platforms by US industrial facilities also positions the region as the primary testbed for next-generation product launches.

Europe Diaphragm Pump Market Trends

Europe’s diaphragm pump demand reflects the region’s strong pharmaceutical manufacturing base and increasingly strict REACH chemical handling regulations. German and Swiss process industries anchor procurement volumes, while EU environmental directives push water utilities to upgrade dosing and chemical feed systems. The regulatory environment here replicates conditions that drove North American adoption, suggesting Europe follows a similar technology adoption path with a two-to-three-year lag.

Asia Pacific Diaphragm Pump Market Trends

Asia Pacific represents the fastest-expanding geography for diaphragm pump installations, driven by large-scale water treatment projects in China and India and rapid growth in pharmaceutical and chemical manufacturing capacity across the region. Government infrastructure spending on wastewater management and industrial zone development sustains multi-year procurement pipelines. Regional manufacturers are also entering the market, intensifying price competition in standard-specification product tiers.

Middle East and Africa Diaphragm Pump Market Trends

Middle East and Africa pump demand concentrates in oil and gas chemical injection applications and municipal water treatment projects funded by government infrastructure programs. GCC nations investing in desalination and water reuse infrastructure require reliable chemical dosing equipment, while African industrial development projects create new installation opportunities. Project-based procurement cycles make revenue timing variable but support sustained long-term volume growth.

Latin America Diaphragm Pump Market Trends

Latin America’s diaphragm pump market centers on mining, food processing, and water treatment applications across Brazil and Mexico. Mining operations in Chile and Peru drive demand for slurry-handling pump designs, while Brazil’s large agri-food processing sector purchases hygienic transfer units. Infrastructure investment in municipal water systems across the region creates a public-sector procurement channel that supplements private industrial buying.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Dover Corporation positions itself as the dominant force in diaphragm pump technology through its PSG brand portfolio, which includes Wilden AODD pumps and advanced diaphragm materials. Dover’s multi-brand strategy allows it to serve distinct end-use segments — from pharmaceutical hygienic transfer to chemical slurry handling — without forcing customers into a single product architecture. This breadth creates cross-sell opportunities that single-product competitors cannot replicate.

Flowserve Corporation leverages its global service network as a strategic differentiator in the diaphragm pump market. Large process industry customers — particularly in oil and gas and chemical plants — prioritize vendor service capability over unit price when specifying critical-duty pumps. Flowserve’s established aftermarket and parts distribution infrastructure locks in long-term service revenue from an installed base that competitors struggle to displace through price alone.

Graco Inc. has built a clear differentiation strategy around electric diaphragm pump technology, positioning its QUANTM platform as the industry benchmark for energy efficiency. The QUANTM pump’s documented sub-twelve-month ROI and up to 80% efficiency advantage give Graco a quantifiable sales argument at a time when industrial buyers face pressure to reduce energy costs and carbon footprint. This data-backed positioning accelerates Graco’s conversion of the existing AODD installed base.

Grundfos Holding A/S approaches the diaphragm pump market through its water treatment and industrial fluid management expertise, integrating pump products into broader system solutions. Grundfos’s investment in digital monitoring and connected pump platforms aligns its hardware offering with buyer preference for predictive maintenance capability. This systems-level positioning shifts the competitive discussion from pump unit cost to operational outcome — a more defensible value proposition against lower-cost regional manufacturers.

Key Players

- Dover Corporation

- Flowserve Corporation

- Graco Inc. (Newell Brands)

- Grundfos Holding A/S

- IDEX Corporation

- LEWA GmbH (Atlas Copco Group)

- Serfilco, Ltd.

- SPX Corporation

- Tapflo Group

- Verder Group

- Wenzhou Kaixin Pump Co., Ltd.

- Xylem Inc.

- Yamada Corporation

- Other Key Players

Recent Developments

- August 2024 — Tapflo UK acquired TS Pumps, a UK-based diaphragm pump manufacturer, to strengthen its product portfolio and expand application coverage across industries. This acquisition extended Tapflo’s manufacturing capability within the UK market and broadened its access to established industrial customer relationships.

- December 2024 — GODO PUMPS launched its new Electric Diaphragm Pump with Pressure Relief Controller alongside High-pressure Diaphragm Pumps at the CHINACOAT 2024 exhibition. The launch targeted coating and paint industry applications, addressing demand for precise pressure management in high-viscosity fluid transfer tasks.

- April 2025 — Graco unveiled major enhancements to its QUANTM electric double diaphragm pump line, including a new 480V input power range and XTREME TORQUE™ motor technology. These upgrades improved energy efficiency and simplified integration into existing industrial power infrastructure for large facility operators.

- August 2025 — Circor International acquired Swelore Engineering Pvt. Ltd. and Hiro Nisha Systems Pvt. Ltd., two Indian pump manufacturers, expanding its diaphragm metering pump and dosing package portfolio. The acquisition added direct manufacturing presence in India, positioning Circor to serve the region’s growing industrial and water treatment sectors.

- September 2025 — ARO (Ingersoll Rand) launched the EVO 210 electric diaphragm pump, a compact model for general transfer and batching that eliminates the need for compressed air. The pump features simplified maintenance design and built-in safety features, targeting facilities seeking to reduce compressed air operating costs without compromising transfer reliability.

Report Scope

Report Features Description Market Value (2025) USD 6.7 Billion Forecast Revenue (2035) USD 10.7 Billion CAGR (2026-2035) 4.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Operation (Double Acting, Single Acting), By Mechanism (Air Operated, Electrically Operated), By Discharge Pressures (Up to 80 Bar, 80 to 200 Bar, Above 200 Bar), By End-Use Industry (Water Treatment, Oil and Gas, Chemical, Pharmaceutical, Food and Beverage, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Dover Corporation, Flowserve Corporation, Graco Inc. (Newell Brands), Grundfos Holding A/S, IDEX Corporation, LEWA GmbH (Atlas Copco Group), Serfilco Ltd., SPX Corporation, Tapflo Group, Verder Group, Wenzhou Kaixin Pump Co. Ltd., Xylem Inc., Yamada Corporation, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Dover Corporation

- Flowserve Corporation

- Graco Inc. (Newell Brands)

- Grundfos Holding A/S

- IDEX Corporation

- LEWA GmbH (Atlas Copco Group)

- Serfilco, Ltd.

- SPX Corporation

- Tapflo Group

- Verder Group

- Wenzhou Kaixin Pump Co., Ltd.

- Xylem Inc.

- Yamada Corporation

- Other Key Players

Our Clients

- 180920

- Mar 2026