Global Connected Mining Market Size, Share, Growth Analysis By Offering (Solution (Asset Tracking & Optimization, Fleet Management, Industrial Safety & Security, Workforce Management, Analytics & Reporting, Process Control, Others), Services (Professional Services, Managed Services)), By Deployment Mode (On-Premises, Cloud-based), By Mining Type (Surface, Underground), By Application (Processing & Refining, Exploration, Transportation), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179415

- Number of Pages: 344

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

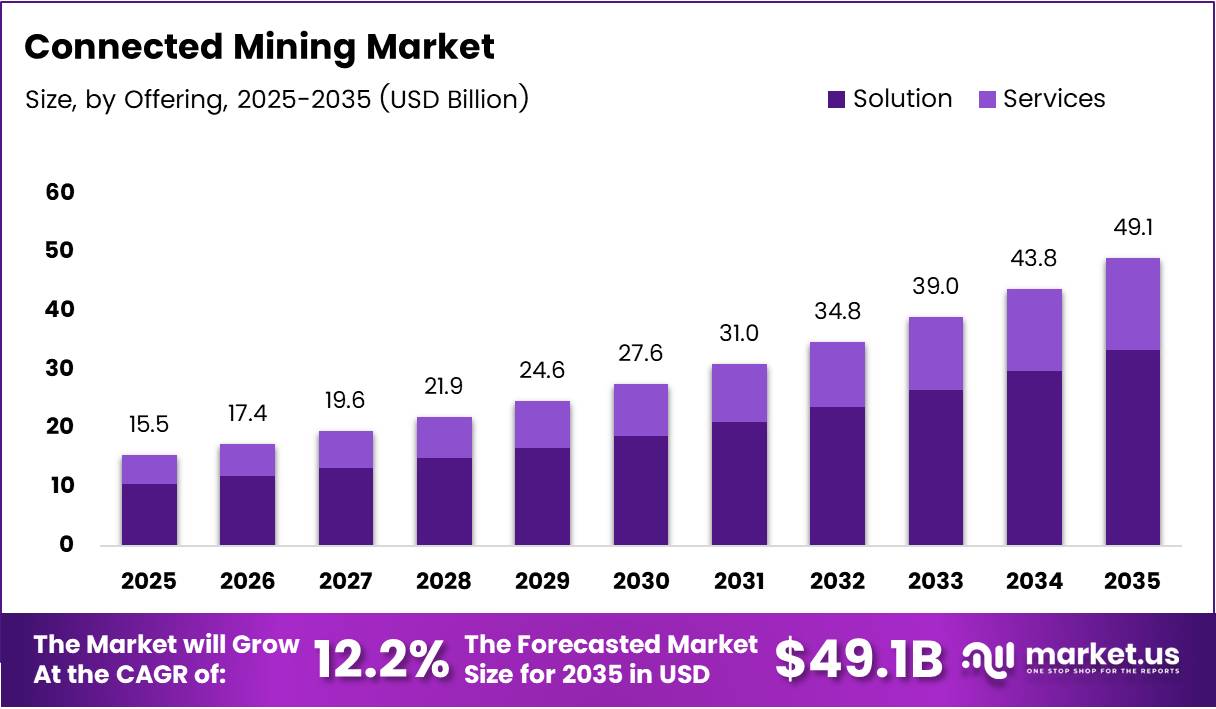

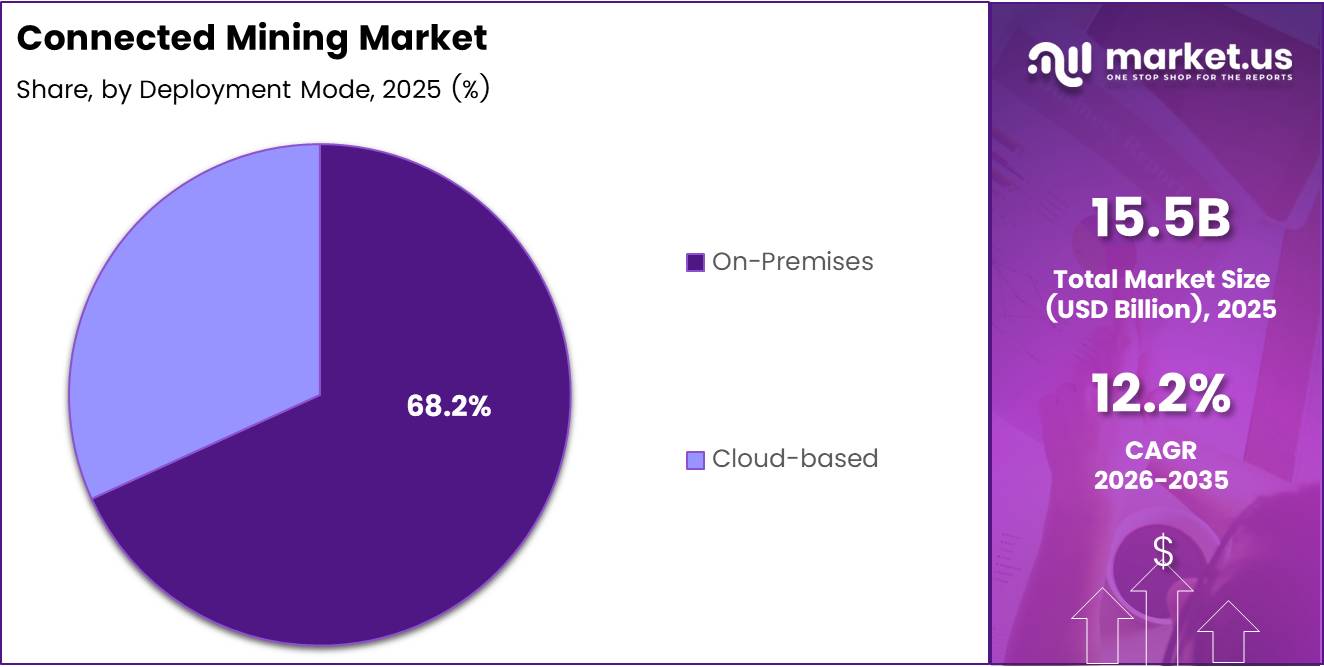

The Global Connected Mining Market size is expected to be worth around USD 49.1 Billion by 2035 from USD 15.53 Billion in 2025, growing at a CAGR of 12.20% during the forecast period 2026 to 2035.

Connected mining integrates industrial IoT sensors, autonomous systems, edge computing, and real-time data analytics into mine operations. This convergence enables operators to monitor equipment health, manage fleets, track workers, and optimize ore processing from centralized platforms — replacing reactive maintenance cycles with data-driven decision-making.

The structural shift in mining is not just technological — it is economic. Operators face mounting pressure to reduce downtime, control labor costs, and meet stricter environmental regulations. Connected platforms answer all three simultaneously, making digital infrastructure a capital priority rather than an optional upgrade for mine operators worldwide.

Government mandates on worker safety monitoring and emissions reporting are accelerating enterprise procurement timelines. In October 2025, Caterpillar entered into an agreement to acquire RPMGlobal Holdings Limited to expand its data-driven connected mine planning and fleet management portfolio — a signal that tier-one equipment vendors now treat software-defined connectivity as core to their competitive positioning.

Solution providers targeting on-premises deployment hold a structural advantage today, as mine operators in remote locations prioritize network reliability over cloud flexibility. However, the cost economics of cloud-based centralized command centers are narrowing this gap, particularly for multi-site operators managing assets across multiple geographies simultaneously.

According to the International Institute for Sustainable Development (IISD), advanced mining economies such as Australia and South Africa report a 75% adoption rate for connected technologies including IoT sensors, autonomous fleets, and AI software as of 2025. This concentration of adoption in mature markets means vendors currently derive most of their revenue from a narrow geographic base — and the next growth wave depends on replicating that infrastructure in emerging mineral-rich economies.

According to laccei.org, predictive monitoring enabled by machine learning and digital twin integration delivers up to a 50% reduction in maintenance costs for critical mining equipment. For a capital-intensive industry where unplanned equipment failures can halt production for days, this figure translates directly into enterprise-level ROI justification — and explains why asset optimization software commands premium pricing in procurement cycles.

Key Takeaways

- The Global Connected Mining Market was valued at USD 15.53 Billion in 2025 and is forecast to reach USD 49.1 Billion by 2035.

- The market is expanding at a CAGR of 12.20% during the forecast period 2026 to 2035.

- By Offering, Solution leads with a 78.43% share in 2025.

- By Deployment Mode, On-Premises holds the dominant share at 68.21% in 2025.

- By Mining Type, Surface mining accounts for 61.43% share in 2025.

- By Application, Processing and Refining holds the largest share at 36.80% in 2025.

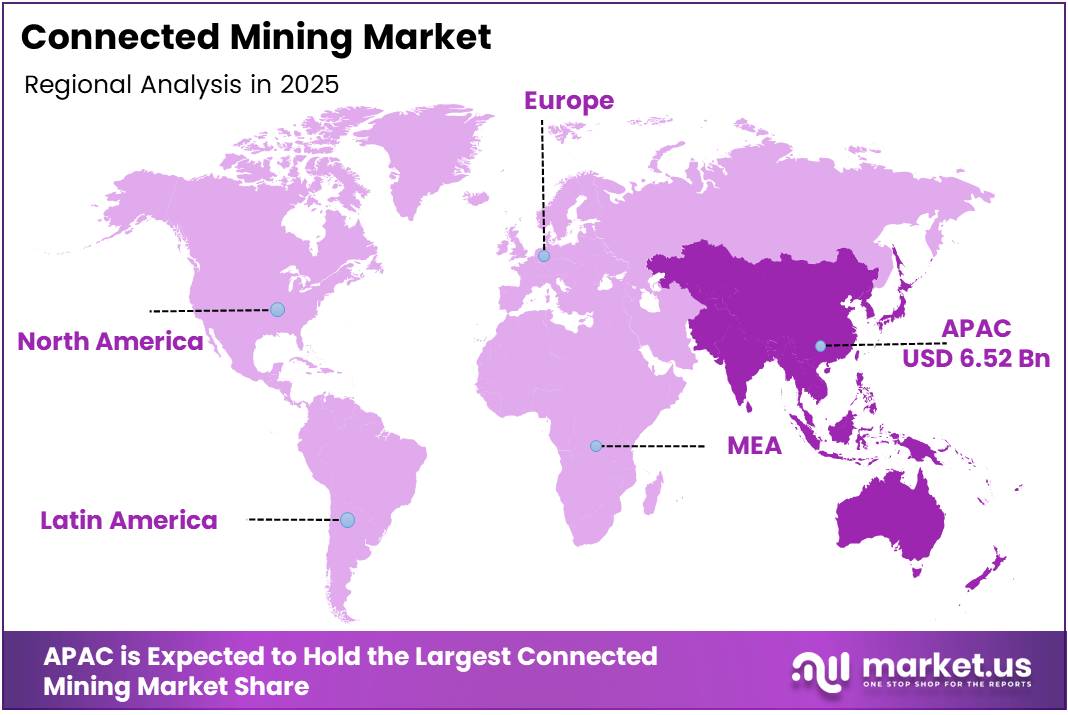

- Asia Pacific leads all regions with a 41.96% share, valued at USD 6.52 Billion in 2025.

Offering Analysis

Solution dominates with 78.43% due to integrated platform demand across mine operations.

In 2025, Solution held a dominant market position in the By Offering segment of the Connected Mining Market, with a 78.43% share. Mine operators prefer integrated software platforms over standalone services because they reduce vendor fragmentation, enable unified data flows, and deliver faster time-to-value across asset tracking, safety, and process control functions.

Asset Tracking and Optimization serves as the highest-priority entry point for connected mining deployments. Operators adopt asset tracking first because it delivers measurable ROI within months — reducing idle time and improving equipment utilization rates without requiring full mine-wide infrastructure overhaul. This makes it the most common starting point for digital transformation programs.

Fleet Management carries strong commercial weight because haulage accounts for the largest share of operational costs in surface mining. Connected fleet systems enable real-time route optimization, fuel consumption tracking, and shift coordination. For operators running large fleets, even marginal efficiency gains translate into tens of millions in annual cost savings.

Industrial Safety and Security differentiates through its direct alignment with regulatory compliance requirements. As governments mandate digital worker monitoring and incident reporting, safety solutions move from discretionary to required spend. This creates a procurement floor that insulates safety platform vendors from budget cuts during commodity price downturns.

Workforce Management addresses the labor productivity challenge that underground operations face most acutely. Real-time location tracking, task assignment, and fatigue monitoring tools reduce supervisory overhead and improve shift efficiency. Adoption accelerates in operations with high worker density and complex multi-level underground environments.

Analytics and Reporting functions as the intelligence layer that converts raw sensor data into operational decisions. Its value compounds over time as datasets grow, making early adopters increasingly difficult for competitors to displace — a lock-in dynamic that drives longer contract cycles and higher customer retention for analytics platform vendors.

Process Control targets the highest-value stage of the mining value chain — ore processing and refining. Connected process control systems optimize mill throughput, reagent dosing, and energy consumption in real time. In April 2025, Hitachi Construction Machinery launched LANDCROS Connect Insight, which collects near-real-time operational data to provide predictive analytics and fuel consumption dashboards, illustrating the commercial direction of this sub-segment.

Services — including Professional Services and Managed Services — represent the recurring revenue layer of connected mining ecosystems. While they account for a smaller share than solutions, their margin profile is typically higher and their churn rates lower, making them strategically valuable for vendors building long-term platform relationships with major mining operators.

Professional Services captures implementation, integration, and consulting revenue tied to initial deployment complexity. Large-scale mine network buildouts require significant professional services engagement, particularly where legacy systems and multi-vendor environments create integration challenges that off-the-shelf solutions cannot resolve alone.

Managed Services represents the transition toward subscription-based operational models in mining technology. Operators outsource network management, system monitoring, and software updates to reduce internal IT burden. This model works best for mid-tier miners that lack in-house digital expertise but still require enterprise-grade connectivity performance.

Deployment Mode Analysis

On-Premises dominates with 68.21% due to connectivity constraints in remote mine environments.

In 2025, On-Premises held a dominant market position in the By Deployment Mode segment of the Connected Mining Market, with a 68.21% share. Remote mine locations with limited and unreliable wide-area network coverage make local infrastructure the only viable option for real-time operations. Operators cannot risk production-critical systems depending on unstable external connectivity.

Cloud-based deployment gains traction among multi-site operators that need centralized visibility across geographically dispersed assets. While latency and connectivity constraints limit its penetration in underground operations today, the buildout of private 5G and LTE networks is systematically removing those barriers — making cloud-based command centers a credible option for surface and processing operations in well-connected jurisdictions.

Mining Type Analysis

Surface dominates with 61.43% due to easier infrastructure deployment and fleet scale.

In 2025, Surface held a dominant market position in the By Mining Type segment of the Connected Mining Market, with a 61.43% share. Open-pit and quarry environments support larger autonomous haulage fleets, broader sensor coverage, and simpler network infrastructure rollouts. The higher equipment density and larger operational footprint amplify the ROI of connected systems at scale.

Underground mining represents a technically demanding but commercially compelling segment for connected solutions. The confined, high-hazard environment creates stronger regulatory pressure for worker safety monitoring, gas detection, and emergency communication systems. As private LTE and mesh networking technologies mature, underground connectivity deployments become both feasible and financially justified.

Application Analysis

Processing and Refining dominates with 36.80% due to direct impact on ore recovery and energy cost.

In 2025, Processing and Refining held a dominant market position in the By Application segment of the Connected Mining Market, with a 36.80% share. Connected systems at the processing stage deliver measurable gains in mill throughput, reagent efficiency, and energy consumption — the three largest operating cost drivers in mineral processing. This direct cost linkage justifies premium software pricing and accelerates procurement decisions.

Exploration applications benefit from connected drone-based surveying, geospatial analytics, and real-time geological data integration. These tools compress survey timelines and improve resource estimation accuracy, reducing the capital risk of exploration programs. As drone mapping platforms advance, exploration becomes an increasingly data-dense function that demands connected infrastructure from the earliest project stages.

Transportation applications anchor the value proposition of autonomous haulage systems and connected fleet management. Haulage represents the highest share of operational cost in most surface mines, making transportation the application category with the clearest and most immediate ROI. The ongoing deployment of autonomous trucks across major mining regions confirms operator confidence in connected transportation solutions.

Key Market Segments

By Offering

- Solution

- Asset Tracking & Optimization

- Fleet Management

- Industrial Safety & Security

- Workforce Management

- Analytics & Reporting

- Process Control

- Others

- Services

- Professional Services

- Managed Services

By Deployment Mode

- On-Premises

- Cloud-based

By Mining Type

- Surface

- Underground

By Application

- Processing & Refining

- Exploration

- Transportation

Drivers

Industrial IoT Adoption and Autonomous Systems Drive Real-Time Operational Control Across Mining Environments

IoT sensor networks across surface and underground operations give mine managers continuous visibility into equipment health, environmental conditions, and worker location. This real-time data layer eliminates the operational blind spots that historically caused unplanned shutdowns. Operators that deploy connected sensor infrastructure reduce reactive maintenance cycles and shift to data-led operational decisions.

Fleet management and predictive maintenance represent the most commercially compelling use case for connected mining investment. According to laccei.org, ML-based predictive models achieve 95% accuracy in fault detection and real-time decision-making for mining plant equipment. This level of precision means operators can schedule maintenance before failures occur — directly cutting the downtime that erodes production targets and profitability.

Autonomous haulage systems and remote-controlled drilling add a second performance layer on top of connectivity. In July 2025, Nevada Gold Mines and Komatsu launched the first U.S. deployment of Komatsu’s FrontRunner Autonomous Haulage System, introducing connected autonomous trucks that enhance safety and real-time operational control. This deployment signals that autonomous connected systems have crossed from pilot programs into mainstream operational use.

Restraints

High Infrastructure Costs and Cybersecurity Exposure Constrain Mine-Wide Connected Deployment

Building a mine-wide connected network requires substantial upfront capital — fiber or wireless backbone infrastructure, ruggedized edge hardware, integration with legacy equipment, and specialized IT deployment teams. For mid-tier and junior miners operating in cost-constrained commodity cycles, this capital threshold delays or prevents full deployment, concentrating connected mining adoption among large-scale operators.

Cybersecurity risk compounds the capital challenge. Cloud-connected mining ecosystems expose operational technology to external threat vectors that were previously air-gapped from the internet. A successful cyberattack on a connected mine can halt production, corrupt process data, or compromise worker safety systems — consequences that carry regulatory, financial, and reputational consequences simultaneously.

ERG’s digital transformation, which delivered an economic impact exceeding USD 111 million in 2025, required multi-year investment in proprietary AI, computer vision, digital twins, and strengthened IT infrastructure. This scale of investment is feasible for tier-one producers but represents a structural barrier for smaller operators — widening the competitive gap between digitally mature miners and those still operating legacy systems.

Growth Factors

Private 5G Networks, AI-Driven Digital Twins, and Emerging Economy Investment Open New Revenue Horizons

Private 5G and LTE network deployments resolve the connectivity bottleneck that limits connected mining adoption in underground and remote surface operations. High-bandwidth, low-latency underground communication enables real-time autonomous vehicle coordination, continuous sensor streaming, and video-based safety monitoring — unlocking use cases that were technically impossible on legacy wireless infrastructure.

AI-driven digital twin platforms represent the most significant value multiplier in connected mining. According to laccei.org, machine learning and digital twin integration delivers a 7.62% reduction in SAG mill energy consumption and a 19.80% reduction in flotation process energy use. For energy-intensive processing operations, these figures translate into tens of millions in annual savings — making digital twin deployment one of the highest-ROI investments available to mine operators.

In September 2025, Komatsu announced a multi-year strategic partnership with Applied Intuition to accelerate next-generation intelligent and autonomous vehicles for connected mining haulage using AI and Vehicle OS technology. This partnership signals that connected mining platforms will increasingly depend on advanced AI software stacks — creating a new layer of the value chain where software-specialized vendors can build competitive positions independent of equipment manufacturing.

Emerging Trends

Geospatial Analytics, Cloud Command Centers, and Wearable Devices Redefine Connected Mine Management

Real-time geospatial analytics and drone-based surveying solutions compress data collection timelines and improve spatial accuracy across both exploration and active mine operations. Exyn’s autonomous drone mapping at Northern Star’s Pogo mine collected survey data in roughly half the time of traditional methods — illustrating how connected aerial platforms shift surveying from a periodic activity to a continuous operational data feed.

Cloud-based centralized command and control centers allow multi-site operators to unify operational visibility across geographically dispersed mine assets. As private 5G networks extend connectivity into previously unreachable areas, the economics of cloud command centers improve — enabling smaller operations to access enterprise-grade monitoring capabilities without building dedicated on-site control infrastructure for each mine.

According to laccei.org, ML and digital twin systems deliver a 13.10% increase in Overall Equipment Effectiveness for belt conveyors. This OEE improvement, combined with wearable smart devices for workforce health and location tracking, indicates that the next competitive frontier in connected mining is not just machine optimization — it is the integrated management of both equipment and human performance in real time.

Regional Analysis

Asia Pacific Dominates the Connected Mining Market with a Market Share of 41.96%, Valued at USD 6.52 Billion

Asia Pacific holds a 41.96% share of the connected mining market, valued at USD 6.52 Billion in 2025. The region’s dominance reflects the scale of mineral extraction activity in Australia, China, and Indonesia — combined with Australia’s mature digital mining ecosystem, where connected technology adoption rates among advanced economies reach 75% according to IISD. This concentration of mining output and digital readiness makes APAC the primary commercial battleground for connected mining vendors.

North America Connected Mining Market Trends

North America represents a high-value market driven by stringent worker safety regulations, autonomous vehicle commercialization, and strong capital availability among major producers. The July 2025 deployment of Komatsu’s FrontRunner Autonomous Haulage System at Nevada Gold Mines marks the first U.S. entry of connected autonomous haulage at scale — signaling that North American operators are moving from pilot evaluations to full operational commitments.

Europe Connected Mining Market Trends

Europe’s connected mining market advances on the back of sustainability mandates and renewable energy integration requirements tied to ESG compliance frameworks. European operators face dual pressure to reduce carbon intensity and improve traceability — both of which connected platforms address directly. Regulatory-driven procurement timelines compress vendor sales cycles and support premium solution pricing in this region.

Latin America Connected Mining Market Trends

Latin America hosts some of the world’s largest copper and lithium reserves, creating a strong structural demand for connected mining solutions tied to ore processing and transportation optimization. However, inconsistent grid infrastructure and limited high-bandwidth connectivity in remote Andean operations slow deployment timelines. Vendors that offer hybrid on-premises and edge computing architectures hold a competitive advantage in this region.

Middle East and Africa Connected Mining Market Trends

Africa’s mineral wealth — spanning copper in the DRC, gold in Ghana, and platinum in South Africa — creates a large addressable market for connected mining solutions. However, according to IISD, technology adoption rates in emerging African mining economies stand at 45%, compared to 75% in advanced economies. This gap signals that vendor strategies focused on lower-cost, modular deployment architectures will outperform those requiring full mine-wide infrastructure buildouts from day one.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ABB Group positions itself at the intersection of electrification and digital automation in mining — a combination that no single-focus competitor can easily replicate. Its integrated offering spans drive systems, process control, and connected energy management, giving ABB a structural advantage as operators seek to consolidate vendors and reduce integration complexity across processing and underground operations.

Cisco Systems Inc. approaches connected mining primarily as a network infrastructure play — building the communication backbone on which all other connected solutions depend. This positioning makes Cisco difficult to displace once deployed, as changing network vendors requires significant operational disruption. Its strength in private LTE and industrial wireless solutions directly addresses the underground connectivity challenge that constrains autonomous system adoption.

Rockwell Automation Inc. differentiates through deep integration between process control software and physical automation hardware. In a market where operational technology and information technology are converging, Rockwell’s ability to bridge both layers gives it an advantage in complex processing plant deployments. Its connected mine solutions target the processing and refining application segment — the largest by market share — which supports its commercial prioritization.

Schneider Electric leverages its energy management expertise to address a growing pain point in connected mining: the integration of renewable energy systems with operational technology platforms. As miners face pressure to decarbonize, Schneider’s ability to link power management with connected mine infrastructure positions it as a strategic partner for ESG-driven capital programs rather than a transactional equipment vendor.

Key Players

- ABB Group

- Cisco Systems Inc.

- Rockwell Automation Inc.

- Schneider Electric

- Hexagon AB

- Accenture

- Trimble Inc.

- Siemens AG

- SAP SE

- IBM Corporation

- Caterpillar

- Rio Tinto

- Komatsu

- Siemens

- Others

Recent Developments

- December 2024 — Sandvik completed the acquisition of Universal Field Robots (UFR), an Australia-based provider of autonomous interoperable solutions. This acquisition strengthens Sandvik’s connected automation portfolio for both surface and underground mining operations.

- September 2024 — Epiroc launched Groundbreaking Intelligence at MINExpo 2024, a flexible OEM-agnostic digital mine ecosystem. The platform integrates data-driven planning, collision avoidance, production monitoring, equipment health, automation, and connectivity solutions to accelerate connected digitalization across mixed fleets and legacy systems.

- September 2024 — Komatsu launched the Modular ecosystem at MINExpo 2024, an interoperable connected mine management platform. It builds on the DISPATCH fleet management system to unify operational data, introduce new optimization apps, and enable seamless mine-site data utilization and future-ready workflows.

- August 2025 — Komatsu North America and Pronto launched Komatsu Smart Quarry Autonomous, a connected autonomy solution integrating AI, rugged sensors, and real-time data for quarry-sized haul trucks. The system enables 24/7 operation, retrofitting, and integration with existing Smart Quarry platforms.

Report Scope

Report Features Description Market Value (2025) USD 15.53 Billion Forecast Revenue (2035) USD 49.1 Billion CAGR (2026-2035) 12.20% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Offering (Solution (Asset Tracking & Optimization, Fleet Management, Industrial Safety & Security, Workforce Management, Analytics & Reporting, Process Control, Others), Services (Professional Services, Managed Services)), By Deployment Mode (On-Premises, Cloud-based), By Mining Type (Surface, Underground), By Application (Processing & Refining, Exploration, Transportation) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ABB Group, Cisco Systems Inc., Rockwell Automation Inc., Schneider Electric, Hexagon AB, Accenture, Trimble Inc., Siemens AG, SAP SE, IBM Corporation, Caterpillar, Rio Tinto, Komatsu, Siemens, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ABB Group

- Cisco Systems Inc.

- Rockwell Automation Inc.

- Schneider Electric

- Hexagon AB

- Accenture

- Trimble Inc.

- Siemens AG

- SAP SE

- IBM Corporation

- Caterpillar

- Rio Tinto

- Komatsu

- Siemens

- Others

Our Clients

- 179415

- Feb 2026