Global Carbon Black Feedstock Market Size, Share, And Enhanced Productivity By Source (Clarified Slurry Oil, Coal Tar Oils), By Product (High BMCI Type, General Type), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179789

- Number of Pages: 335

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

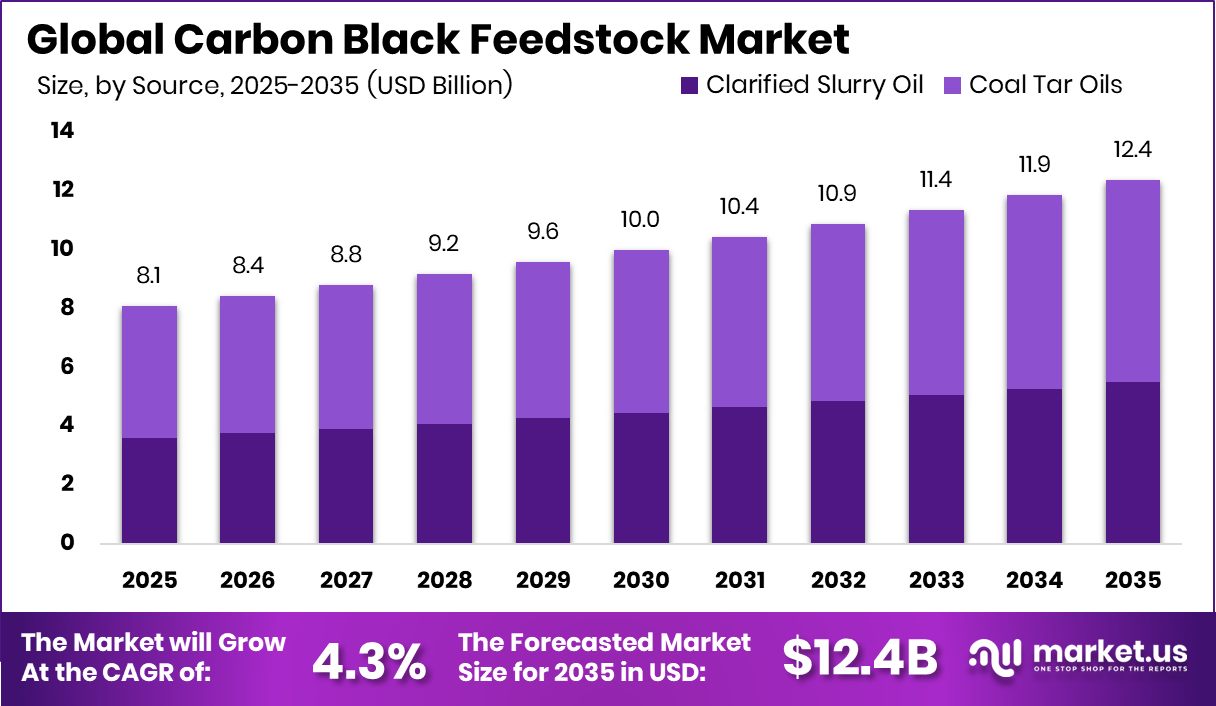

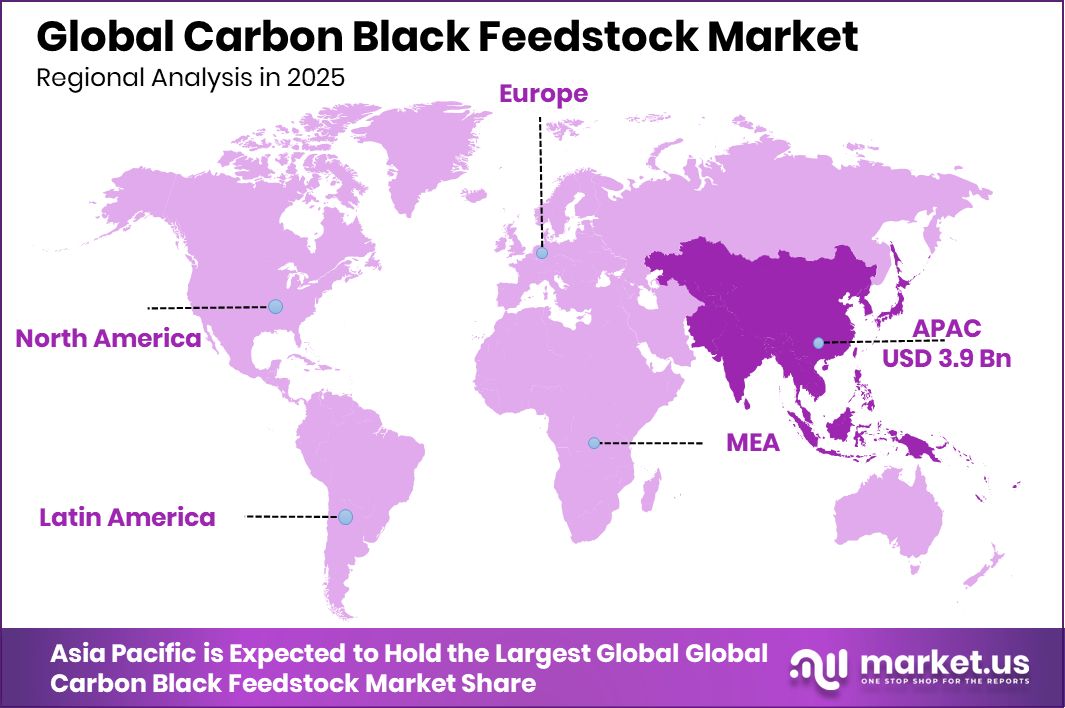

The Global Carbon Black Feedstock Market is expected to be worth around USD 12.4 billion by 2035, up from USD 8.1 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035. Asia Pacific maintains 49.1% market dominance as Carbon Black Feedstock value hits USD 3.9 Bn.

The Global Carbon Black Feedstock Market is shaped by two major source categories—clarified slurry oil and coal tar oils. These feedstocks act as the base material from which carbon black is produced through high-temperature cracking. In simple terms, carbon black feedstock is the heavy aromatic oil derived from refinery or coal-based streams, chosen for its ability to generate strong yields of carbon black used across rubber, industrial, and specialty applications. As demand for reinforced materials and performance additives grows, choosing the right feedstock type becomes central to production efficiency.

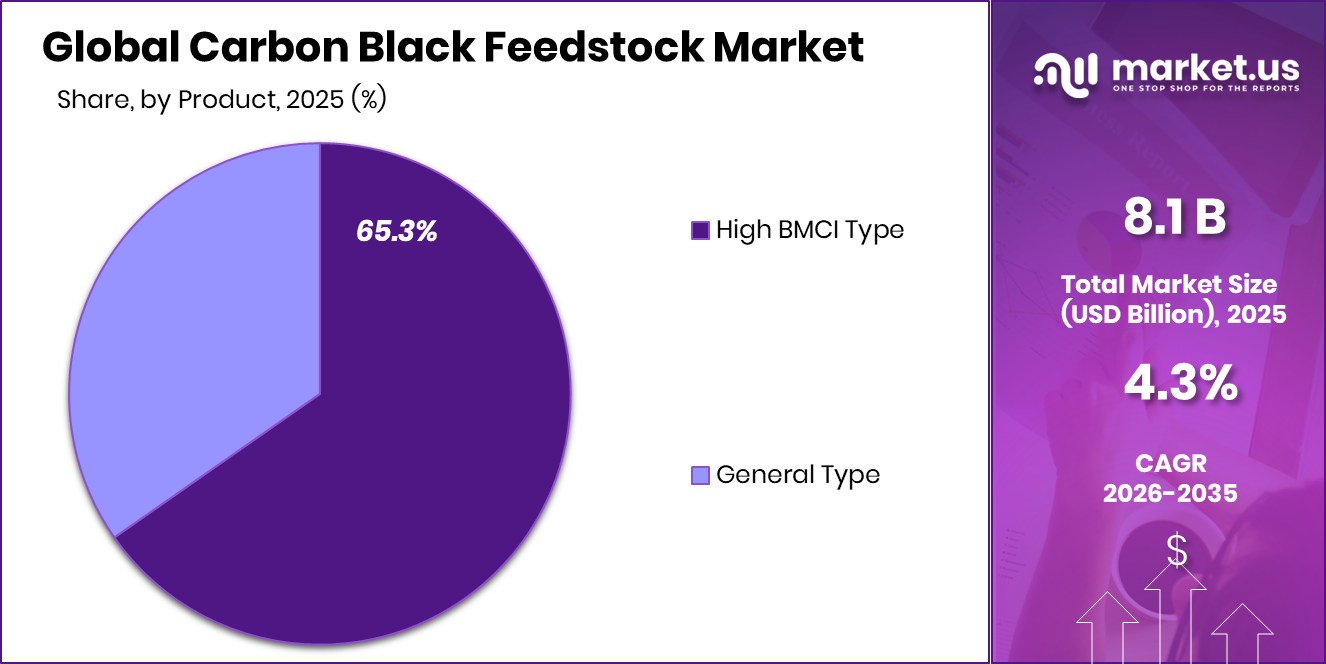

The Carbon Black Feedstock Market revolves around the availability, quality, and pricing of clarified slurry oil and coal tar oils. These materials influence product consistency, furnace efficiency, and the ability to serve a wide range of industrial applications. The product taxonomy is led by High BMCI Type, known for its stronger aromatic content, followed by General Type, which supports broader, cost-centered uses.

Growth is supported by increasing attention toward cleaner and more efficient feedstock utilization. Public and private initiatives are also shaping the landscape, including DOE Invests $17 Million to Advance Carbon Utilization Projects, which encourages better use of heavy residues.

Demand prospects broaden with cleaner energy and carbon-focused technologies, highlighted by Monolith Secures $1 Billion DOE Loan for Clean Hydrogen, Carbon Black, pushing innovation in feedstock processing and downstream applications.

Opportunities continue to expand as countries adopt greener industrial practices, supported further by financing programs such as the EBRD and Partners Provide €65 Million Green Financing to BMCI, helping industries upgrade units and refine feedstock pathways for future-ready carbon black production.

Key Takeaways

- The Global Carbon Black Feedstock Market is expected to be worth around USD 12.4 billion by 2035, up from USD 8.1 billion in 2025, and is projected to grow at a CAGR of 4.3% from 2026 to 2035.

- In the Carbon Black Feedstock Market, clarified slurry oil holds a strong 44.6% share globally.

- The Carbon Black Feedstock Market is dominated by high-BMCI-type products, capturing a 65.3% share.

- In the Asia Pacific, strong industrial expansion drives Carbon Black Feedstock demand reaching USD 3.9 Bn and 49.1%.

By Source Analysis

Carbon Black Feedstock Market shows clarified slurry oil dominating with a 44.6% share.

In 2025, the Carbon Black Feedstock Market is expected to maintain a strong reliance on clarified slurry oil, which continues to hold around 44.6% share due to its consistent availability and suitability for high-temperature cracking processes. Refineries across Asia, Europe, and the Middle East are increasing their output of slurry oil as part of ongoing modernization programs, helping producers stabilize feedstock supply even as global fuel dynamics shift.

The segment benefits from refiners’ focus on efficiency upgrades, enabling better recovery of aromatic-rich residue streams that enhance carbon black yield. With tire manufacturing and industrial rubber goods expanding steadily, clarified slurry oil remains the preferred feedstock option, offering cost advantages and performance reliability for large-scale furnace carbon black production.

By Product Analysis

High BMCI type leads the Carbon Black Feedstock Market with 65.3% dominance.

In 2025, the High BMCI (Bureau of Mines Correlation Index) Type continues to dominate the Carbon Black Feedstock Market with a 65.3% share, driven by its high aromatic content and superior carbon-forming characteristics. Manufacturers increasingly choose high-BMCI feedstock to achieve deeper black pigmentation, improved reinforcement properties, and higher furnace process efficiency. Tire producers, mechanical rubber goods manufacturers, and specialty black producers rely heavily on this segment as demand for durable, high-performance rubber components grows worldwide.

The segment’s strong position is also supported by refineries optimizing residue conversion units, enabling a consistent supply of feedstock grades with elevated BMCI values. As performance specifications tighten across automotive and industrial sectors, high-BMCI types remain essential for meeting quality and productivity benchmarks.

Key Market Segments

By Source

- Clarified Slurry Oil

- Coal Tar Oils

By Product

- High BMCI Type

- General Type

Driving Factors

Rising demand for high-aromatic feedstock materials

The Carbon Black Feedstock Market is being pushed forward by the rising demand for high-aromatic feedstock materials, especially as industries look for stronger, more stable furnace-grade inputs. This demand creates a steady pull across refining networks and residue-based supply chains. A major financial backdrop influencing this trend comes from global fossil-fuel financing, where banks have poured $6.9 trillion into fossil operations since the Paris Agreement.

In 2023 alone, $705 billion was supplied, with JPMorgan Chase, Mizuho, and Bank of America standing among the top funders. These financial flows help sustain refinery expansions, residue recovery systems, and aromatic-rich output capacity, indirectly supporting feedstock availability for carbon black production, much like steady equipment demand drives growth in the Chainsaw Market.

Restraining Factors

Volatile residue prices affect feedstock stability

The market continues to face pressure from volatile residue prices, which directly affect feedstock stability and production planning. Shifts in global crude balances or refinery operating patterns can disrupt supply, creating uncertainty for producers dependent on consistent aromatic residues.

A significant restrictive layer comes from the reality that 60 major banks collectively finance nearly $7 trillion in coal, oil, and gas projects, as highlighted in global reviews of fossil-fuel banking. This level of funding encourages continued reliance on conventional fuels, often delaying transitions toward cost-stable or cleaner residue streams.

As observed in the Chainsaw Market, where cost fluctuations in raw materials slow purchasing cycles, similar financial dependencies can restrict technological updates and flexible feedstock reformulation.

Growth Opportunity

Cleaner feedstock technologies unlock new potential

Growth potential is strengthening as cleaner feedstock technologies gain traction, opening new pathways for efficient, low-emission production. Innovations aimed at improving residue utilization, enhancing aromatic quality, and reducing furnace impurities present meaningful opportunities for manufacturers.

A notable push comes from emerging carbon-removal technologies receiving investment support, such as Frontier’s $58.3 million funding for Vaulted Deep, which showcases confidence in new carbon-focused solutions. These investments create an ecosystem where sustainable feedstock processing becomes more achievable.

Similar to how the Chainsaw Market sees growth from battery-powered and low-emission models, the Carbon Black Feedstock Market benefits from technologies that reduce environmental load while improving performance reliability, giving producers room to adopt modern, differentiated feedstock strategies.

Latest Trends

Shift toward high-BMCI aromatic feedstocks

A major trend shaping the market is the shift toward high-BMCI aromatic feedstocks, which offer improved furnace performance and stronger yield consistency. Manufacturers are prioritizing feedstocks with richer aromatic structures to meet rising expectations in rubber, industrial goods, and specialty applications.

Another notable market-shaping event is the U.S. purchase of over 2 million barrels of jet fuel from Dangote Refinery, marking a historic shift in global refinery trade flows. This development signals broader changes in residue availability, refinery economics, and international supply dependencies.

As with the Chainsaw Market’s shift toward quieter and more efficient models, the feedstock sector reflects a transition toward higher-performance inputs aligned with evolving industry and energy-trade dynamics.

Regional Analysis

Asia Pacific leads the Carbon Black Feedstock Market with a dominant 49.1% share worth USD 3.9 Bn.

The Asia Pacific region continues to anchor the Carbon Black Feedstock Market, holding a dominant 46.5% share valued at USD 1.8 Bn, supported by its expanding tire production base and strong petrochemical output. In North America, demand remains steady as refinery operations and rubber goods manufacturing sustain the need for consistent feedstock availability across industrial clusters.

Europe shows balanced growth driven by specialty carbon black applications and improving utilization rates within integrated refineries. Meanwhile, the Middle East and Africa benefit from large-scale refining capacity and increasing export-oriented feedstock supply, supporting downstream industries.

Latin America experiences stable consumption aligned with regional tire replacements and developing industrial activities. Across all regions, Asia Pacific remains the leading contributor due to its strong manufacturing ecosystem, large automotive output, and expanding processing capacity, allowing it to retain the highest market share and value positioning in the global Carbon Black Feedstock landscape.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, Indian Oil Corporation Ltd maintains a strong strategic position in the global Carbon Black Feedstock Market due to its extensive refining network and steady production of key aromatic-rich residue streams. The company’s ability to supply clarified slurry oil and related feedstock consistently gives it a competitive advantage, especially as downstream tire producers seek stable, quality-controlled inputs. Its integrated operations allow better cost management, and this reliability continues to increase its presence among carbon black manufacturers that depend on uninterrupted feedstock flows.

For Dow, 2025 reflects an emphasis on optimizing feedstock suitability for performance-driven carbon black applications. Leveraging its broad chemical portfolio and long-standing expertise in residue processing, Dow strengthens its market relevance by supporting producers that require cleaner, more uniform feedstock qualities. The company’s scale and technical capabilities enable it to stay aligned with evolving product specifications across rubber, plastics, and industrial sectors that increasingly demand consistency in carbon black reinforcement properties.

Arham Petrochem Private Limited continues to strengthen its footprint in 2025 by catering to regional and mid-sized carbon black manufacturers needing flexible supply solutions. Its specialization in processing aromatic by-products and offering customized feedstock grades positions the company as a responsive supplier. With a focus on reliability and tailored product offerings, Arham Petrochem supports customers aiming to balance performance requirements with cost efficiency, helping it solidify its role in the broader feedstock ecosystem.

Top Key Players in the Market

- Indian Oil Corporation Ltd

- Dow

- Arham Petrochem Private Limited

- Haldia Petrochemicals Ltd (HPL)

- Jalan Carbons & Chemicals (P) Ltd.

- Shell

- BASF

- Aramco

- Sherwin-Williams Company

- Epsilon Carbon Private Limited

Recent Developments

- In July 2025, Indian Oil announced plans to upgrade a key unit at its Panipat refinery so it can produce sustainable aviation fuel (SAF) by using used cooking oil as input. This new capability supports cleaner fuel goals and expands the company’s refining operations beyond traditional products. This development shows Indian Oil’s focus on greener feedstock options and more efficient use of refinery streams. The SAF production unit will contribute to future energy diversification.

- In December 2024, Dow agreed to sell its 50% ownership in the DowAksa Advanced Composites joint venture to its partner, Aksa Akrilik Kimya. This business made flexible packaging laminating adhesives, and the sale helps Dow focus on its core chemicals and materials science efforts. The deal supports reallocating capital toward areas where Dow sees stronger long-term growth, including feedstock and performance chemicals.

Report Scope

Report Features Description Market Value (2025) USD 8.1 Billion Forecast Revenue (2035) USD 12.4 Billion CAGR (2026-2035) 4.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Clarified Slurry Oil, Coal Tar Oils), By Product (High BMCI Type, General Type) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Indian Oil Corporation Ltd, Dow, Arham Petrochem Private Limited, Haldia Petrochemicals Ltd (HPL), Jalan Carbons & Chemicals (P) Ltd., Shell, BASF, Aramco, Sherwin-Williams Company, Epsilon Carbon Private Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Carbon Black Feedstock MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Carbon Black Feedstock MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Indian Oil Corporation Ltd

- Dow

- Arham Petrochem Private Limited

- Haldia Petrochemicals Ltd (HPL)

- Jalan Carbons & Chemicals (P) Ltd.

- Shell

- BASF

- Aramco

- Sherwin-Williams Company

- Epsilon Carbon Private Limited

Our Clients

- 179789

- February 2026