Global Biological Organic Fertilizer Market Size, Share and Report Analysis By Type (Microorganisms And Organic Residues, Organic Residue-Based Fertilizers, Biofertilizers), By Form (Dry, Liquid), By Crop Type ( Pulses And Oilseeds, Grains And Cereals, Fruits And Vegetables, Turf And Ornamentals, Commercial Crops, Others), By Application (Soil Treatment, Seed Treatment, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 178883

- Number of Pages: 319

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

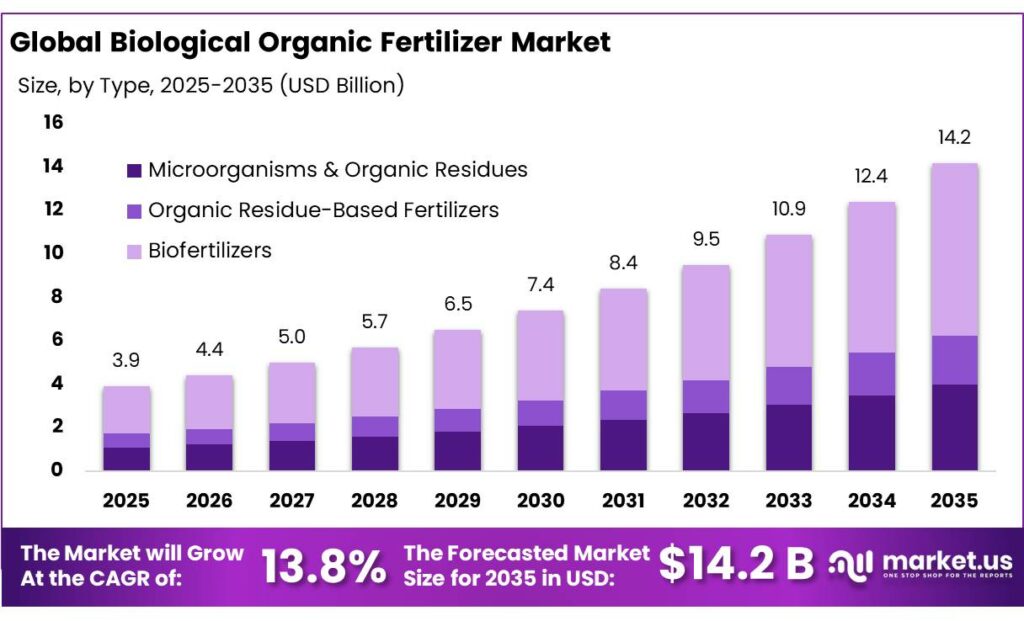

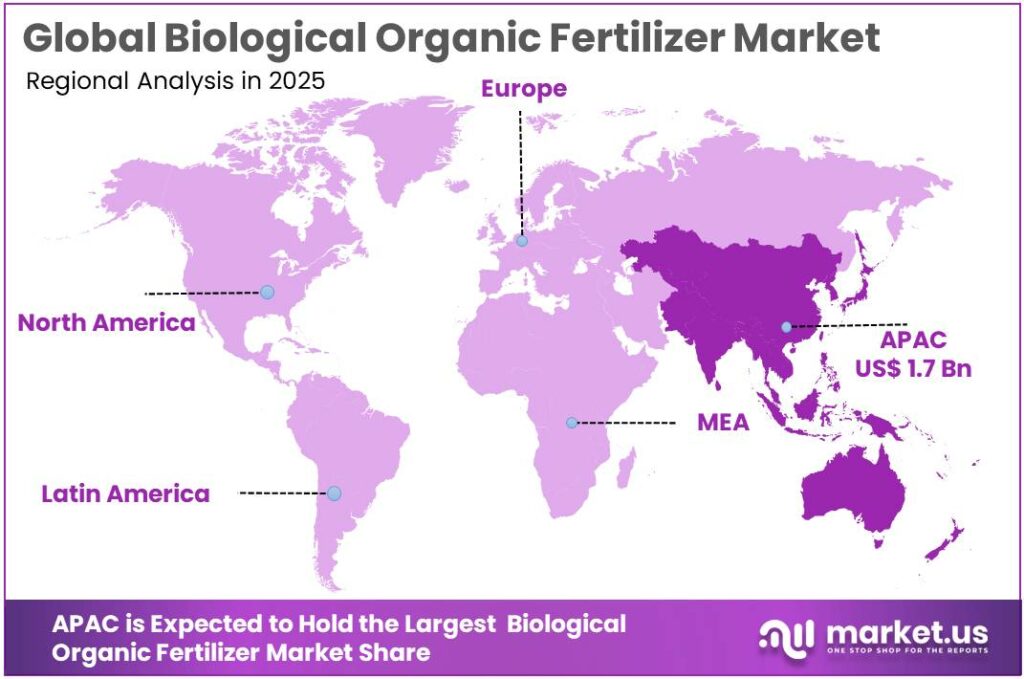

The Global Biological Organic Fertilizer Market is expected to be worth around USD 14.2 Billion by 2034, up from USD 3.9 Billion in 2024, and is projected to grow at a CAGR of 13.8% from 2025 to 2034. The Asia Pacific segment maintained 45.8%, supporting a Biological Organic Fertilizer value of USD 1.7 Bn.

Biological organic fertilizers are typically defined as inputs based on living or once-living materials—such as microbial inoculants, composts, manures and plant-based extracts—that improve soil fertility through biological processes rather than synthetic chemistry. They sit at the intersection of the fast-growing organic food sector and the broader shift toward regenerative agriculture. Globally, the area under organic farming reached about 96 million hectares in 2022, with more than 4.5 million producers and organic food sales close to €135 billion in the same year, underlining a solid demand base for organic nutrient solutions.

From an industrial perspective, demand is underpinned by the rapid expansion of organic and sustainably managed farmland. According to joint statistics from FAO and partners, organic agriculture is now practiced in 188 countries, with more than 96 million hectares under organic management and over 4.5 million organic producers worldwide; global sales of organic food and drink reached almost EUR 135 billion in 2022.

Policy commitments in major food-producing regions are reinforcing this trajectory. Under the EU Green Deal’s Farm to Fork strategy, the European Commission has set a binding objective for at least 25 percent of EU agricultural land to be farmed organically by 2030. Eurostat reports that organic farming already covered about 16.9 million hectares of EU agricultural land in 2022, and meeting the 25 percent target will require converting more than 3 million hectares per year, significantly above historic growth rates.

The same parliamentary response notes that 25.61 crore Soil Health Cards have been issued and supported by 8,302 soil testing labs and 1,020 school mini-labs, backed by INR 1,970 crore in central funding, encouraging balanced nutrient use and organic amendments. Under schemes such as Paramparagat Krishi Vikas Yojana, farmers can receive up to INR 50,000 per hectare over three years to adopt organic practices, including purchase of biofertilizers and vermicompost, while the Mission Organic Value Chain Development for the North East further supports organic input adoption.

Key Takeaways

- Biological Organic Fertilizer Market is expected to be worth around USD 14.2 Billion by 2034, up from USD 3.9 Billion in 2024, and is projected to grow at a CAGR of 13.8%.

- Biofertilizers held a dominant market position, capturing more than a 56.3% share in the Biological Organic Fertilizer Market.

- Dry held a dominant market position, capturing more than a 61.2% share in the Biological Organic Fertilizer Market.

- Grains & Cereals held a dominant market position, capturing more than a 37.9% share in the Biological Organic Fertilizer Market.

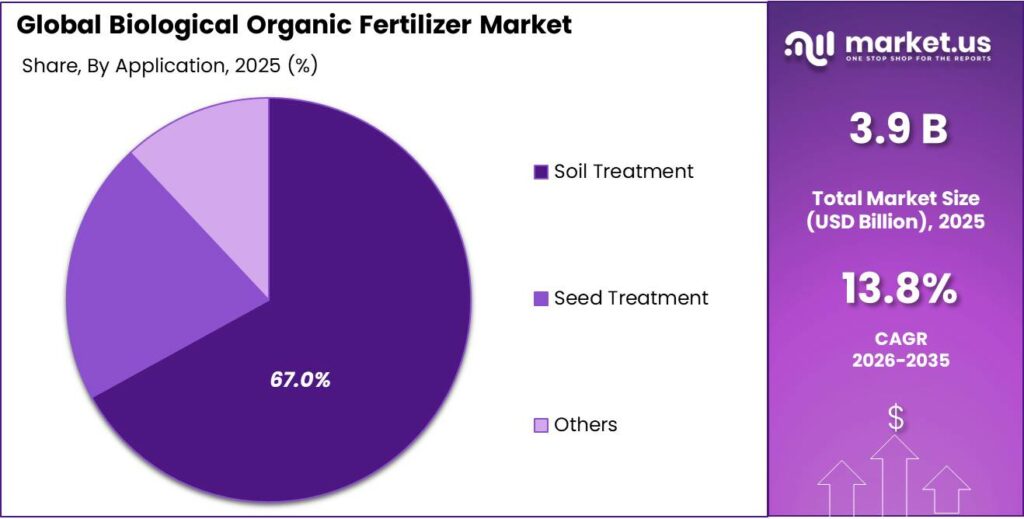

- Soil Treatment held a dominant market position, capturing more than a 67.1% share in the Biological Organic Fertilizer Market.

- Asia Pacific is the clear growth hub in the Biological Organic Fertilizer Market, dominating with 45.8% of global revenue, equivalent to around USD 1.7 billion.

By Type Analysis

Biofertilizers lead the market with a strong 56.3% share

In 2024, Biofertilizers held a dominant market position, capturing more than a 56.3% share in the Biological Organic Fertilizer Market. Their rising adoption is strongly driven by farmers’ preference for natural soil enhancers that improve nutrient availability without harming long-term soil health. During 2024, the segment continued to benefit from growing awareness about residue-free farming and the global push toward reducing chemical fertilizer dependence.

By 2025, the demand for biofertilizers is expected to rise further as more countries strengthen sustainability programs and encourage the use of microbe-based solutions that boost crop yield. The segment also gains momentum from expanding organic cultivation areas, where these products are essential for improving soil structure and biological activity.

By Form Analysis

Dry Form dominates with 61.2% because of its long shelf life and easy handling

In 2024, Dry held a dominant market position, capturing more than a 61.2% share in the Biological Organic Fertilizer Market. Farmers preferred dry formulations mainly because they store well, are simple to apply, and remain stable during transportation. Throughout 2024, this form saw increased use across large farming regions where bulk application and cost-efficient distribution mattered the most.

By 2025, the dry segment is expected to stay strong as more growers shift toward fertilizers that offer longer shelf life and consistent performance in different climate conditions. Its convenience, lower moisture sensitivity, and suitability for both small and large farms continue to make dry biological fertilizers the most trusted option in the market.

By Crop Type Analysis

Grains & Cereals lead the market with a strong 37.9% share

In 2024, Grains & Cereals held a dominant market position, capturing more than a 37.9% share in the Biological Organic Fertilizer Market. This segment grew steadily as farmers focused on improving soil fertility and boosting yield for staple crops like wheat, rice, and corn. During 2024, the rising demand for residue-free food and sustainable cultivation practices encouraged wider use of biological fertilizers across major grain-producing regions.

Looking into 2025, the adoption rate is expected to increase as more countries promote eco-friendly farming methods and support products that enhance nutrient uptake in high-volume cereal crops. The consistent global demand for grains and cereals ensures that this crop segment remains the key driver for biological organic fertilizer consumption.

By Application Analysis

Soil Treatment leads the market with a strong 67.1% share

In 2024, Soil Treatment held a dominant market position, capturing more than a 67.1% share in the Biological Organic Fertilizer Market. The segment maintained its lead as farmers increasingly focused on restoring soil structure, improving organic matter, and enhancing microbial activity. Throughout 2024, soil treatment products were widely adopted in regions facing soil degradation and nutrient depletion, making them essential for long-term crop productivity. By 2025, the demand for biological fertilizers used in soil treatment is expected to rise further as sustainable farming practices become more common and governments promote natural soil-reviving inputs. This strong need for healthier, more fertile soil ensures soil treatment continues as the most influential application segment in the market.

Key Market Segments

By Type

- Microorganisms & Organic Residues

- Organic Residue-Based Fertilizers

- Biofertilizers

By Form

- Dry

- Liquid

By Crop Type

- Pulses & Oilseeds

- Grains & Cereals

- Fruits & Vegetables

- Turf & Ornamentals

- Commercial Crops

- Others

By Application

- Soil Treatment

- Seed Treatment

- Others

Emerging Trends

Surge in regulated, bio-based and microbial fertilisers is reshaping the market

One of the strongest recent trends in biological organic fertilisers is that they are moving from the margins into the “official” fertiliser toolbox. Governments and international bodies are no longer seeing them as niche products; they are writing them directly into laws, standards and circular-bioeconomy plans. That shift is opening the door for faster adoption on normal commercial farms, not just on small organic plots.

In the European Union, this change is very visible. The EU Fertilising Products Regulation (EU) 2019/1009, which became fully applicable in July 2022, created a single framework for all fertilising products marketed in the EU. For the first time, it explicitly includes organic and organo-mineral fertilisers, soil improvers and biostimulants alongside traditional mineral fertilisers.

This means microbial products, compost-based fertilisers and other bio-based inputs can now carry the same CE mark as conventional fertilisers if they meet strict quality and safety rules. For producers of biological organic fertilisers, this is a big step: once a product is CE-marked, it can circulate freely across the EU’s internal market instead of being blocked at national borders by different rules.

At the same time, global policy is pushing agriculture toward more circular and bio-based systems. The FAO has highlighted microbial fertilisers (biofertilisers) as a key tool for reducing dependence on synthetic fertilisers and improving nutrient-use efficiency. In a 2025 note on sustainable and circular bioeconomy for agrifood systems, FAO cites expert estimates that the biofertiliser market could grow from about USD 1 billion in 2016 to around USD 3–4 billion by 2027.

Scientific work is reinforcing this trend. FAO and soil scientists describe biofertilisers and biostimulants as part of a broader effort to manage the soil microbiome more intelligently, rather than just adding more mineral nutrients. A 2022 FAO publication calls the soil microbiome “a game changer” and notes that the use of biostimulants, biofertilisers and biopesticides is emerging as a major approach to sustainable production. Behind these technical and regulatory shifts lies a strong demand story.

- According to the latest global organic agriculture statistics from FiBL and IFOAM, organic farming already covers about 98.9 million hectares worldwide and generated nearly €136 billion in organic food sales in 2023.

Drivers

Growing shift toward organic, climate-smart farming is pushing demand

One major driving factor for the Biological Organic Fertilizer market is the rapid global shift toward organic and climate-smart agriculture. Farmers, policymakers, and consumers are all asking the same question: how do we grow enough food without exhausting soils and heating the planet further? Biological organic fertilizers fit neatly into this transition because they feed the soil with living microbes and natural nutrients instead of relying on heavy doses of synthetic chemicals.

Over the last few years, organic farming has moved from a niche to a serious part of global agriculture. According to FiBL and IFOAM, around 96 million hectares of land were farmed organically in 2022, after increasing by more than 20 million hectares in a single year, while sales of organic food reached almost €135 billion in 2022. By the end of 2023, the organic area had grown further to 98.9 million hectares, with 2.5 million additional hectares converted in just one year.

Climate pressure is another strong push factor. The FAO estimates that global agrifood systems emitted about 16.2 billion tonnes of CO₂-equivalent in 2022, accounting for just under 30% of total human-made emissions. A large share of these emissions comes from fertilizer production and use, soil degradation, and land-use change. When farmers switch part of their nutrient program to bio-based inputs—such as microbial inoculants, composted manures, and plant-based fertilizers—they can reduce nitrous oxide emissions from soils, cut energy-intensive synthetic fertilizer use, and gradually build more carbon into the ground.

Governments are picking up on this and turning it into concrete targets. In Europe, the EU Farm to Fork Strategy aims to make 25% of agricultural land organic by 2030, while also targeting a 50% reduction in overall pesticide and fertilizer use to protect soil, water, and biodiversity. These goals are impossible to reach without a big shift toward biological and organic nutrient sources.

Restraints

Yield Gap and Lower Output Compared to Conventional Methods

One of the biggest restraining forces holding back the Biological Organic Fertilizer market is the yield gap between organic and conventional farming, especially in regions where farmers prioritize immediate production results. While biological and organic fertilizers clearly improve soil health and long-term sustainability, they often struggle to match the short-term nutrient delivery and output levels that synthetic fertilizers provide. This phenomenon is commonly referred to as the yield gap, and it plays out in real numbers that farmers, policymakers, and food systems cannot ignore.

A comprehensive review of organic farming practices found that, on average, organic crop yields can be between 5% and 34% lower than yields under conventional practices that use synthetic fertilizer inputs. In practical terms, this means that for every 100 kilograms of crop a conventional system might produce, an organic system using biological fertilizers could produce only 66 to 95 kilograms under similar conditions.

The reason for this lower output lies in the nature of how biological fertilizers work. Unlike synthetic fertilizers, which deliver nutrients in instantly available forms, biological organic fertilizers rely on microbial activity, organic matter decomposition, and soil biological processes to release nutrients over time. That slow-release process is better for soil structure and ecology, but it doesn’t always keep pace with crop nutrient demand during critical growth phases, especially in high-yield crops like cereals and legumes. Farmers in developing regions facing food security challenges often cannot afford this trade-off between sustainability and production speed, especially when population pressures are high.

Opportunity

Expanding organic and sustainable farming is opening a huge window for biofertilizers

One of the clearest growth opportunities for biological organic fertilizers is the rapid, policy-backed expansion of organic and sustainable farming worldwide. Farmers are under pressure to protect soil, reduce emissions, and still feed a growing population. That shift is creating a long-term demand base for inputs that work with nature, and biofertilizers sit right at the center of that story.

In just a few years, organic farming has become a serious global force. By the end of 2023, about 98.9 million hectares of agricultural land were managed organically, an increase of 2.5 million hectares in a single year. Organic agriculture is now practised in 188 countries, with more than 4.5 million farmers involved, and global retail sales of organic food and drink reached almost €135 billion in 2022. New data released in 2026 show that organic food and drink sales climbed further to €145.0 billion in 2024, confirming that consumer demand is not a fad but a strong, ongoing trend.

This is not only a market trend; it is also a policy trend. Under the European Green Deal, the EU’s Farm to Fork Strategy has set a target to bring at least 25% of the EU’s agricultural land under organic farming by 2030. Studies show that achieving this target would also cut fertilizer use in the EU by almost 20% compared with 2020 levels, simply as a co-benefit of more organic land. If a quarter of Europe’s fields move toward systems that avoid or sharply reduce synthetic inputs, then biological organic fertilizers will become an essential tool, not just a niche choice.

Regional Insights

Asia Pacific dominates with 45.8% share, valued around USD 1.7 billion

Asia Pacific is the clear growth hub in the Biological Organic Fertilizer Market, dominating with 45.8% of global revenue, equivalent to around USD 1.7 billion in 2024. The region’s leadership is anchored in its vast agricultural base and the rapid shift toward sustainable and organic practices across major economies such as India, China, and key Southeast Asian countries. Globally, organic agriculture now covers nearly 99 million hectares, managed by about 4.3 million farmers, with India ranked among the top countries by organic area at around 4.5 million hectares, underlining the scale of opportunity within Asia.

Governments in the region are actively pushing bio-based inputs to cut chemical dependence and rebuild soil health. India, for example, has rolled out national organic and soil-health programmes, while state-level schemes such as Mission Organic initiatives in the North-East have brought tens of thousands of hectares, including about 22,000 hectares in Tripura, under certified organic cultivation.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Batian – Batian, headquartered in Shenzhen, China, was founded in 1998 and operates in the agricultural chemicals sector, including fertilizers and crop-enhancement products. As of 2024, the company reported annual revenue of about USD 445.2 million, net profit of USD 56.1 million and EBITDA of roughly USD 104.5 million, highlighting strong financial capacity to scale biological and organic nutrient solutions. Batian competes with several global biological and ag-tech players, using its sizeable revenue base to invest in improved, more sustainable fertilizer formulations.

Novozymes (Novonesis A/S) – Novozymes’ BioAg business (now under Novonesis A/S) is one of the largest global suppliers of microbial solutions for broad-acre and specialty crops. In 2024, Novozymes reported sales of about EUR 3.83 billion and a workforce of roughly 10,582 employees, with 36.5% of net sales coming from agriculture, bioenergy and animal feed markets. Earlier disclosures highlight 700+ enzyme and microbial products serving 30+ industries, giving its biofertility and biofertilizer lines a powerful R&D and distribution backbone.

Top Key Players Outlook

- Biomax

- Agri Life

- Batian

- RIZOBACTER

- Novozymes

- National Fertilizers Limited

Recent Industry Developments

In 2024, Agri Life’s portfolio included multiple biofertilizer lines – nitrogen-fixing, phosphorus-solubilizing, potash-mobilizing and zinc/iron-solubilizing bacteria, along with mycorrhiza (VAM) and composting cultures – sold under brands such as Nitrofix, P Sol B, K Sol B, Zn Sol B, Fe Sol B and Agri VAM, with single-product purity often specified at around 99% and recommended soil application doses of 3–5 kg per acre.

In 2024, Novonesis reported EUR 3,833.5 million in sales with 305.8 million EUR net income, reflecting strong overall growth and broad global reach.

Report Scope

Report Features Description Market Value (2025) USD 3.9 Bn Forecast Revenue (2035) USD 14.2 Bn CAGR (2026-2035) 13.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Microorganisms And Organic Residues, Organic Residue-Based Fertilizers, Biofertilizers), By Form (Dry, Liquid), By Crop Type ( Pulses And Oilseeds, Grains And Cereals, Fruits And Vegetables, Turf And Ornamentals, Commercial Crops, Others), By Application (Soil Treatment, Seed Treatment, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Biomax, Agri Life, Batian, RIZOBACTER, Novozymes, National Fertilizers Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Biological Organic Fertilizer MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Biological Organic Fertilizer MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Biomax

- Agri Life

- Batian

- RIZOBACTER

- Novozymes

- National Fertilizers Limited

Our Clients

- 178883

- Feb 2026