Global Biocontrol Agents Market Size, Share Analysis Report By Active Substance (Microbials, Macro-organisms, Bio-chemicals), By Crop (Fruits and Vegetables, Cereals And Grains, Pulses, Others), By Application (Seed treatment, On-Field, Post-harvest) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183676

- Number of Pages: 198

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

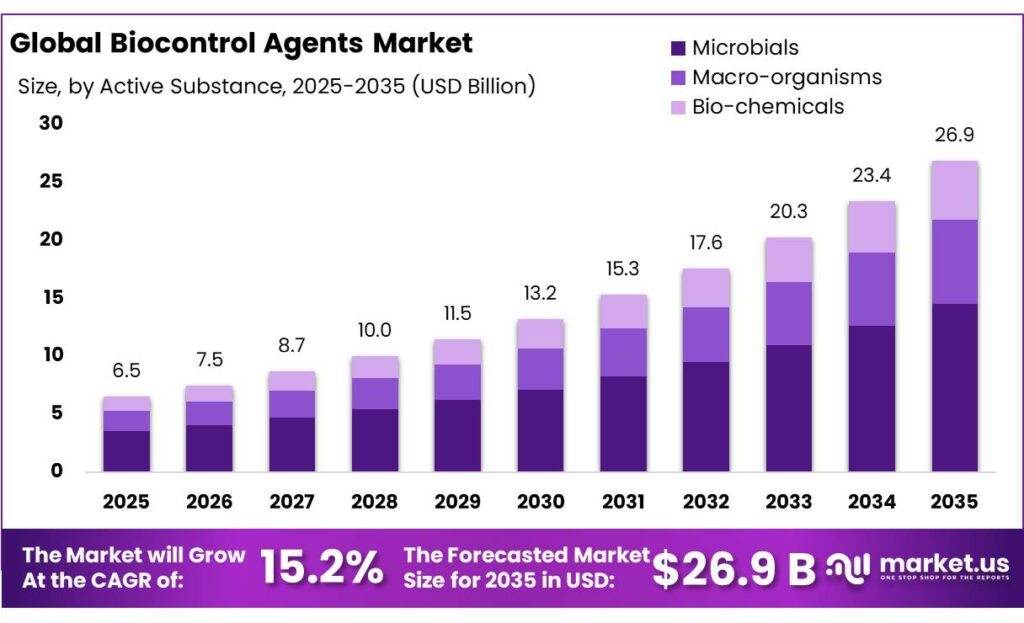

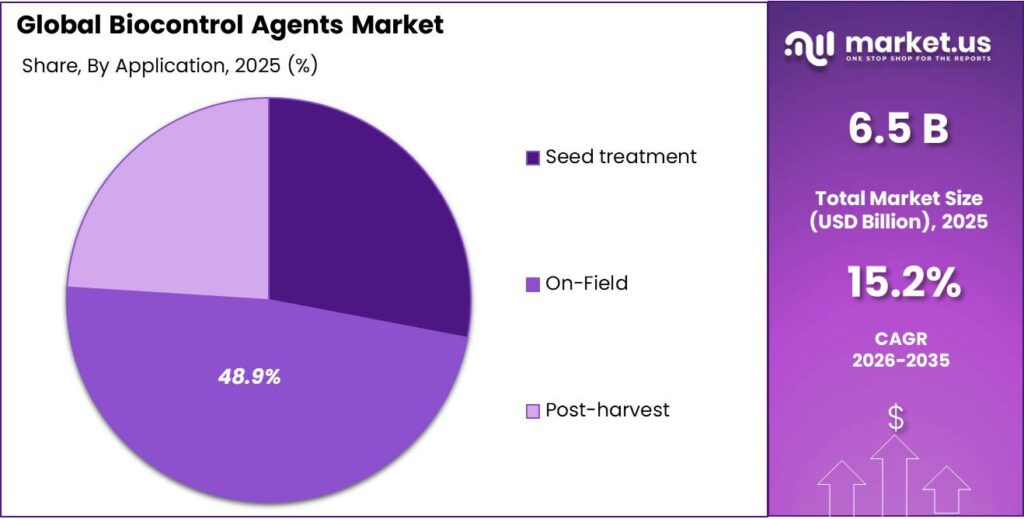

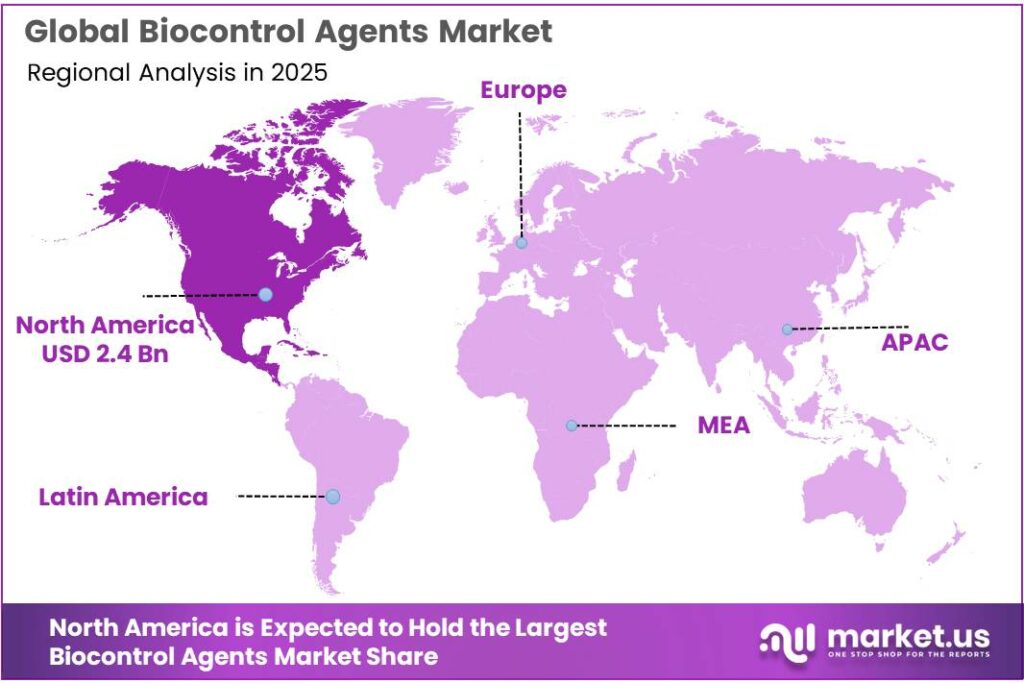

The Global Biocontrol Agents Market size is expected to be worth around USD 26.9 Billion by 2035, from USD 6.5 Billion in 2025, growing at a CAGR of 15.2% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 37.5% share, holding USD 2.4 Billion revenue.

Biocontrol agents are moving from a niche crop-protection tool to a mainstream input within integrated pest management programs. The commercial rationale is strong because plant pests and diseases still reduce global crop yields by 20% to 40% every year, while FAO also notes that trade losses from plant pests exceed USD 220 billion annually and invasive insects alone cause at least USD 70 billion in economic losses.

From an industrial scenario perspective, the category is moving from a niche specialty input toward a more structured agri-input segment supported by regulation, retailer residue expectations, and organic acreage expansion. In the United States, EPA notes that there were 390 registered biopesticide active ingredients as of August 31, 2020, and the agency also reported that it had registered 15 new biopesticide active ingredients since January 2025, indicating continuing regulatory throughput.

In Europe, policy direction is equally supportive: the European Commission’s pesticide framework is tied to a 50% reduction in the use and risk of chemical pesticides by 2030, while the European Environment Agency reported that organic farmland in the EU rose from 5.9% in 2012 to 10.8% in 2023, against a 25% target by 2030. These figures signal a clear opening for biological alternatives and complementary pest-management technologies.

The main growth drivers are therefore practical as much as regulatory. Biocontrol agents generally fit residue-sensitive fruit, vegetable, greenhouse, and export-oriented crops; they are also increasingly relevant where resistance management and worker-safety considerations matter. The annual biocontrol industry meeting ABIM 2025 drew more than 2,000 participants from over 60 countries and featured more than 150 exhibiting companies, illustrating the depth of commercial participation and innovation momentum now surrounding the segment.

BASF stated that its Agricultural Solutions division invested €919 million in R&D in 2024 and generated €9.8 billion in sales, while BASF Group sales reached €65.3 billion. In November 2025, BASF announced that Integral® Pro was registered in France for sunflower, with EU field trials from 2022 to 2024 showing an average yield increase of +3.5 dt/hectare versus untreated seeds. This indicates that large crop-input suppliers are commercializing biological seed-treatment platforms with measurable field economics.

Key Takeaways

- Biocontrol Agents Market size is expected to be worth around USD 26.9 Billion by 2035, from USD 6.5 Billion in 2025, growing at a CAGR of 15.2%.

- Microbials held a dominant market position, capturing more than a 54.2% share.

- Fruits and Vegetables held a dominant market position, capturing more than a 42.7% share.

- On-Field held a dominant market position, capturing more than a 48.9% share in the biocontrol agents market.

- North America held the dominant position in the biocontrol agents market, accounting for 37.5% of the global share and reaching nearly USD 2.4 billion.

By Active Substance Analysis

Microbials leads the Biocontrol Agents market with a 54.2% share in 2025, supported by broad use across sustainable crop protection

In 2025, Microbials held a dominant market position, capturing more than a 54.2% share in the biocontrol agents market by active substance. This leadership reflects the strong preference for microbial-based solutions in modern agriculture, where growers are increasingly choosing naturally derived crop protection tools that are effective, residue-friendly, and suitable for integrated pest management practices. Products based on beneficial bacteria, fungi, viruses, and other microorganisms continue to see strong acceptance because they offer targeted pest and disease control while aligning with the rising focus on soil health and sustainable farming.

By Crop Analysis

Fruits and Vegetables dominate with a 42.7% share in 2025, driven by higher crop sensitivity and residue concerns

In 2025, Fruits and Vegetables held a dominant market position, capturing more than a 42.7% share in the biocontrol agents market by crop. This leading position mainly comes from the high-value nature of these crops and their greater sensitivity to pest and disease attacks throughout the growing cycle. Growers in this segment rely heavily on crop protection methods that can maintain quality, appearance, and shelf life, making biocontrol agents a preferred choice for managing insects, fungal diseases, and post-harvest risks without affecting marketability.

By Application Analysis

On-field use leads with a 48.9% share in 2025, supported by broad adoption across large-scale farming operations

In 2025, On-Field held a dominant market position, capturing more than a 48.9% share in the biocontrol agents market by application. This leading share is mainly driven by the widespread use of biological crop protection solutions across open-field farming, where large cultivation areas require effective and scalable pest and disease management. Farmers growing cereals, pulses, oilseeds, fruits, vegetables, and plantation crops are increasingly using biocontrol agents directly in field conditions to improve crop protection while reducing dependence on conventional chemical pesticides.

Key Market Segments

By Active Substance

- Microbials

- Bacteria

- Fungi

- Virus

- Protozoa

- Yeast

- Others

- Macro-organisms

- Insects

- Mites

- Nematodes

- Others

- Bio-chemicals

- Semio-chemicals

- Plant extracts

- Plant growth regulators

- Organic acids

- Minerals

By Crop

- Fruits and Vegetables

- Cereals & Grains

- Pulses

- Others

By Application

- Seed treatment

- On-Field

- Post-harvest

Emerging Trends

AI-based pest monitoring is becoming the latest trend in biocontrol agents

One of the latest trends in the biocontrol agents industry is the integration of AI-based pest monitoring with biological crop protection programs. Farmers are no longer depending only on manual scouting or scheduled sprays. In 2025, the trend is clearly moving toward smart detection systems, digital alert platforms, and precision release of beneficial organisms. FAO’s latest 2025 integrated pest management guidance for eight priority global pests and diseases specifically highlights the use of digital alert systems, robotics, and biopesticides as modern solutions for sustainable crop protection.

Government-led biodiversity programs are pushing nature-based pest control into the mainstream

Another major 2025 trend is the strong push toward biodiversity-friendly pest control through government and FAO-backed initiatives. In May 2025, FAO emphasized scaling safer alternatives to highly hazardous pesticides through biological control and integrated pest management at the Basel, Rotterdam and Stockholm Conventions. The organization also highlighted that pests and diseases now cause around USD 220 billion in losses annually to the global agri-food sector, which is accelerating interest in preventive biological solutions and ecosystem-based farming.

Drivers

Rising pesticide-related crop losses is a major driver for biocontrol adoption

One of the biggest driving factors for biocontrol agents is the growing pressure to reduce crop losses caused by pests while cutting the use of synthetic pesticides. Recent scientific evidence shows that nearly 40% of global agri-food production is lost to pests, which directly affects farm income, food supply stability, and export quality.

This level of loss is forcing growers to adopt more reliable biological crop protection systems that can work in both open-field and protected farming. Biocontrol agents are becoming important because they help manage insects, mites, and diseases in a targeted way without creating the same residue and resistance issues often linked with repeated chemical pesticide use.

Government support and food security initiatives are accelerating growth

Another major growth driver is the increasing support from governments and global food institutions for sustainable pest management. In February 2025, India’s Ministry of Agriculture-backed international biocontrol conference brought together more than 400 delegates, including policymakers, scientists, and industry experts, specifically to strengthen sustainable pest management and One Health practices.

These initiatives matter because policy support directly improves product approvals, farmer awareness, and field-level adoption. In simple terms, when governments actively promote eco-friendly farming and safer food systems, growers gain more confidence in switching to biocontrol products. This support is expected to remain a strong long-term market driver through 2026 as countries focus more on food security, residue-free produce, and climate-resilient agriculture.

Restraints

Limited shelf life and inconsistent field performance remain a key restraint

One of the biggest restraining factors for biocontrol agents is their limited shelf life and unstable performance under real farm conditions. Unlike synthetic crop protection products, many microbial biocontrol formulations are highly sensitive to storage temperature, moisture, UV exposure, and carrier quality. A 2025 agricultural study showed that even after formulation improvements, researchers had to specifically extend product stability up to 150 days of storage to make field use practical.

This clearly shows that product stability is still a challenge for manufacturers and distributors, especially in regions where cold-chain infrastructure and warehouse conditions are weak. For farmers, short shelf life creates hesitation because product effectiveness may drop before application, directly affecting crop protection results. In simple terms, growers need confidence that the product will perform the same way in storage, transport, and final field use.

Regulatory delays and uneven approval systems slow wider adoption

Another major restraint comes from slow and inconsistent regulatory approval systems across countries and regions. FAO-backed regional biopesticide guidelines have openly recognized that the registration system for biocontrol agents is still a challenge because many countries continue to use the same approval pathway as chemical pesticides. This increases time, compliance costs, and data requirements for biological products that naturally behave very differently from synthetic molecules.

This delays farmer access to safer alternatives and limits product availability in many agricultural regions. Because biocontrol agents often need crop-specific and climate-specific validation, any regulatory delay further adds to development costs. Until governments continue simplifying biological registration frameworks and harmonizing standards, this will remain one of the most important barriers holding back faster industry expansion through 2026.

Opportunity

Expansion of protected cultivation is creating the biggest growth opportunity

One of the strongest growth opportunities for biocontrol agents is the rapid expansion of protected cultivation and greenhouse farming, where biological pest control works more efficiently than in many open-field conditions. Greenhouses provide controlled temperature, humidity, and crop monitoring, making them highly suitable for beneficial insects, microbial solutions, and natural predators.

A strong recent example came from FAO’s 2025 greenhouse initiative, where cucumber cultivation under protected structures in Uzbekistan delivered a 232% increase in yield, while farmer incomes reportedly quadrupled through better pest control and reduced chemical use.

Government-backed sustainable farming programs are opening new scale opportunities

Another major growth opportunity comes from government and global food-agency support for biodiversity-friendly agriculture. FAO’s global workshop on biological control agents, held in September 2024, specifically focused on scaling up adoption through better regulations, cross-country cooperation, and awareness among regulators from Europe, Africa, the USA, and Latin America.

This matters because faster approvals and better policy support directly improve product reach into mainstream agriculture. In parallel, FAO data also shows that global organic agricultural land reached nearly 73 million hectares, reflecting the widening cultivation base where biocontrol products fit naturally.

Regional Insights

North America dominated the Biocontrol Agents market with a 37.5% share, reaching USD 2.4 billion in 2025

In 2025, North America held the dominant position in the biocontrol agents market, accounting for 37.5% of the global share and reaching nearly USD 2.4 billion in value. The region’s leadership is strongly supported by the United States and Canada, where growers have rapidly adopted sustainable pest management tools across fruits, vegetables, row crops, greenhouse produce, and organic farming systems. The region benefits from a highly developed agricultural input ecosystem, advanced microbial formulation capabilities, and strong awareness among commercial growers regarding residue-free crop protection.

A major regional strength comes from the well-established regulatory framework led by the U.S. Environmental Protection Agency (EPA) and USDA APHIS, which continue to support faster approvals and field use of biological solutions. EPA reported 390 registered biopesticide active ingredients, highlighting the maturity of the biological crop protection landscape in the region.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Andermatt Biocontrol remains one of the most specialized players in the biological crop protection space, with a strong focus on microbial and baculovirus-based pest control. In 2025, the company demonstrated its global scale by sending 58 delegates from across its worldwide businesses to ABIM, reflecting deep technical engagement in the biologicals ecosystem.

BASF continues to be a global leader in biological and integrated crop protection through its Agricultural Solutions division. In the 2025 business year, the segment generated €9,587 million in sales, underlining its strong scale in crop science and biological innovation. BASF is also strengthening its biological manufacturing base, including a new fermentation plant for biological crop protection products.

Biobest holds a strong position in beneficial insects, pollination, and biological crop protection solutions, particularly in greenhouse and horticulture systems. The company reports 3,000+ employees worldwide, presence in 70+ countries, and annual turnover above €500 million, showing strong commercial scale in biological farming inputs.

Top Key Players Outlook

- Andermatt Biocontrol

- Basf

- Biobest

- Bioworks

- Cbc

- Certis

- Cropscience Bayer

- Isagro

- Koppert Biological Systems

- Marrone Bio Innovations

- Novozymes

- Nufarm

- Syngenta

- Valent Bioscience

Recent Industry Developments

In 2025, BASF’s Agricultural Solutions segment reported sales of €9,587 million, EBITDA before special items of €2,081 million, segment cash flow of €1,505 million, and R&D spending of €990 million; within that segment, reported sales were €2,838 million in fungicides, €1,089 million in insecticides, and €575 million in seed treatment, which shows the company has the financial scale to keep expanding biological.

2026, Biobest’s own company profile shows 3,000+ employees, presence in 70+ countries with distributors, and EUR 500+ million turnover, which gives it solid commercial scale in biological crop protection, and in April 2026 the company further strengthened its market reach by expanding its exclusive distribution partnership with Plant Products across the U.S., giving growers wider access to its biological portfolio.

Report Scope

Report Features Description Market Value (2025) USD 6.5 Bn Forecast Revenue (2035) USD 26.9 Bn CAGR (2026-2035) 15.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Active Substance (Microbials, Macro-organisms, Bio-chemicals), By Crop (Fruits and Vegetables, Cereals And Grains, Pulses, Others), By Application (Seed treatment, On-Field, Post-harvest) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Andermatt Biocontrol, Basf, Biobest, Bioworks, Cbc, Certis, Cropscience Bayer, Isagro, Koppert Biological Systems, Marrone Bio Innovations, Novozymes, Nufarm, Syngenta, Valent Bioscience Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Andermatt Biocontrol

- Basf

- Biobest

- Bioworks

- Cbc

- Certis

- Cropscience Bayer

- Isagro

- Koppert Biological Systems

- Marrone Bio Innovations

- Novozymes

- Nufarm

- Syngenta

- Valent Bioscience

Our Clients

- 183676

- April 2026