Global Bio-Butadiene Market Size, Share and Report Analysis By Grade (Industrial Grade, Laboratory Grade), By Application (Styrene Butadiene Rubber (SBR), Styrene Butadiene Latex (SBL), Polybutadiene (PB), Acrylonitrile-Butadiene-Styrene (ABS), Styrene-Butadiene Block Copolymers (SBS And SEBS), Nitrile Butadiene Rubber (NBR), Others), By End Use (Automotive And Transportation, Consumer Goods, Chemical Processing, Building And Construction, Healthcare, Textile, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Mar 2026

- Report ID: 179836

- Number of Pages: 362

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

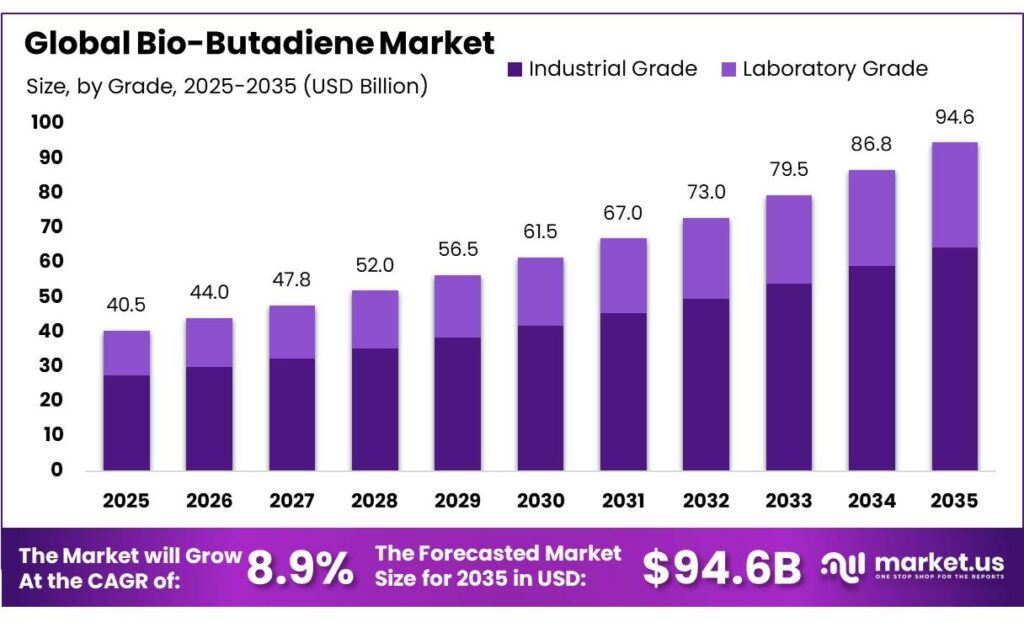

The Global Bio-Butadiene Market is expected to be worth around USD 94.6 Million by 2035, up from USD 40.5 Million in 2025, at a CAGR of 8.9% from 2026 to 2035. The North America segment maintained 41.6%, supporting a Bio-Butadiene value of USD 7.8 Bn.

Bio-butadiene is an emerging renewable alternative to fossil-derived 1,3-butadiene, a key monomer for synthetic rubber, ABS plastics and latexes. It is typically produced by catalytically converting bioethanol from sugar, starch or lignocellulosic feedstocks. Recent techno-economic work on ethanol-to-butadiene routes shows that, under current cost structures, bio-butadiene is still less competitive than naphtha-derived butadiene, with a probability of positive net present value of only about 11–17% for one-step processes and around 5% for two-step configurations. However, the same studies report life-cycle CO₂ emissions reductions of 7.6–52.4% versus conventional butadiene, underlining the environmental case for this pathway.

The current industrial scenario is pre-commercial but moving quickly. Globally, technology readiness levels for biobased butadiene are reported around TRL 6–8, meaning pilot to demonstration scale, while in India catalytic and hybrid routes are in the TRL 4–6 range, still mainly at lab and early pilot scale. One of the most visible industrial milestones is the BioButterfly™ project led by Michelin, IFPEN and Axens, which commissioned an industrial-scale demonstrator at Bassens, France, in July 2023.

Several structural drivers support long-term demand for bio-butadiene. First, the rapid expansion of bioenergy and biofuels is increasing the availability of sustainable ethanol feedstock. FAO’s latest bioenergy statistics show that world bioenergy final consumption rose from 24.4 exajoules (EJ) in 1990 to 39.5 EJ in 2023, with 4.4 EJ (about 11%) already coming from liquid biofuels. The International Energy Agency (IEA) projects that global biofuel demand will grow by 38 billion litres between 2023 and 2028, reaching roughly 200 billion litres and representing a 23% increase over the period, with ethanol and renewable diesel providing about two-thirds of the growth.

- In the European Union, the biomass-producing and converting sectors of the bioeconomy generated up to €863 billion of value added in 2023, equal to about 5% of EU GDP, and supported more than 17 million jobs, with the bioeconomy highlighted as one of the highest-growth industrial domains. For chemicals specifically, the bio-based share of the EU chemical industry increased from 6% in 2008 to 7% in 2015, signalling a gradual structural shift toward renewable feedstocks.

Regulation is another important driver. The U.S. Environmental Protection Agency’s 2026 final risk evaluation for fossil-based 1,3-butadiene concluded that the substance presents an “unreasonable risk” to human health under 11 of 30 assessed conditions of use, signalling tighter controls on emissions around conventional butadiene production and processing.

Key Takeaways

- Bio-Butadiene Market is expected to be worth around USD 94.6 Million by 2035, up from USD 40.5 Million in 2025, at a CAGR of 8.9%.

- Industrial Grade held a dominant market position, capturing more than a 68.3% share.

- Styrene Butadiene Rubber (SBR) held a dominant market position, capturing more than a 48.2% share.

- Automotive & Transportation held a dominant market position, capturing more than a 49.7% share.

- North America held a dominant position in the bio-butadiene market, capturing around 43.8% of global share with an estimated value of roughly 17.7 Mn.

By Grade Analysis

Industrial Grade Bio-Butadiene leads the market with a strong 68.3% share

In 2024, Industrial Grade held a dominant market position, capturing more than a 68.3% share, mainly because manufacturers relied on this grade for producing synthetic rubber, latex binders, and high-volume polymer applications where consistent purity and process stability are essential. The segment benefited from rising demand for bio-based tires, adhesives, and performance elastomers, as industries continued shifting away from fossil-derived monomers.

During 2024, industrial buyers preferred this grade due to its compatibility with existing downstream facilities, allowing companies to adopt bio-based feedstocks without modifying large-scale reactors or compounding systems. This compatibility drove higher procurement volumes, especially as global rubber manufacturers tested bio-butadiene for styrene-butadiene rubber (SBR) and polybutadiene rubber (PBR), both of which consume large quantities of the monomer.

By Application Analysis

Styrene Butadiene Rubber (SBR) leads the market with a 48.2% share

In 2024, Styrene Butadiene Rubber (SBR) held a dominant market position, capturing more than a 48.2% share, largely because SBR remains the backbone of tire manufacturing and automotive rubber goods. As industries increasingly looked for low-carbon raw materials, bio-butadiene became a preferred alternative to its fossil counterpart, allowing SBR producers to lower their overall emissions without redesigning existing polymerization lines.

Throughout 2024, major tire and rubber manufacturers expanded their testing and procurement of bio-based monomers to meet internal sustainability targets, leading to a noticeable rise in demand for bio-butadiene specifically for SBR formulations. The strong compatibility between bio-butadiene and traditional SBR production routes helped keep transition risks low, which played a major role in the segment’s dominance.

By End Use Analysis

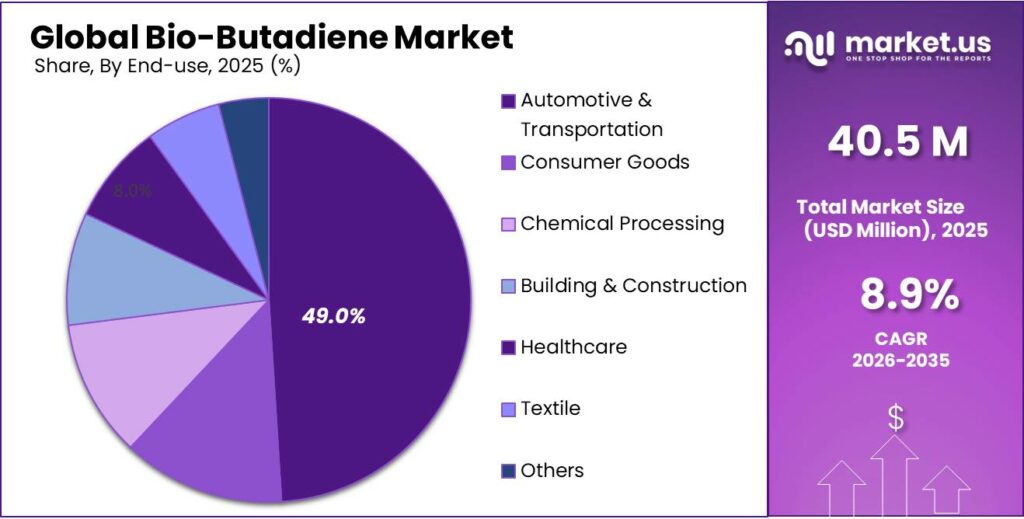

Automotive & Transportation leads the market with a 49.7% share

In 2024, Automotive & Transportation held a dominant market position, capturing more than a 49.7% share, driven by the sector’s heavy reliance on rubber components produced from bio-butadiene. Tires, seals, belts, mounts, and vibration-damping parts remained the largest consumers, and manufacturers increasingly turned to renewable monomers to align with stricter sustainability targets.

Automakers and tier-1 suppliers also intensified their shift toward greener material sourcing in 2024, adopting bio-based feedstocks to reduce lifecycle emissions across vehicle platforms. This transition allowed companies to maintain performance standards while gradually replacing fossil-based butadiene, making the automotive and transportation segment the strongest demand center for bio-butadiene during the year.

Key Market Segments

By Grade

- Industrial Grade

- Laboratory Grade

By Application

- Styrene Butadiene Rubber (SBR)

- Styrene Butadiene Latex (SBL)

- Polybutadiene (PB)

- Acrylonitrile-Butadiene-Styrene (ABS)

- Styrene-Butadiene Block Copolymers (SBS & SEBS)

- Nitrile Butadiene Rubber (NBR)

- Others

By End Use

- Automotive & Transportation

- Consumer Goods

- Chemical Processing

- Building & Construction

- Healthcare

- Textile

- Others

Emerging Trends

Stronger push for low-carbon tires is pulling bio-butadiene into mainstream bioeconomy plans

One clear latest trend around bio-butadiene is how quickly it is getting woven into broader sustainable tire and bioeconomy strategies. Big rubber and tire manufacturers are under pressure to cut the carbon footprint of their products, and bio-butadiene sits at the heart of that transition because it is a drop-in alternative to fossil butadiene in synthetic rubber. At the same time, governments and global food-linked bodies are pushing for better use of biomass and residues, which indirectly supports bio-based monomers.

Behind this trend is a strong growth in sustainable biomass and biofuels, which supply the ethanol used to make bio-butadiene. FAO’s latest bioenergy statistics show that world bioenergy final consumption rose from 24.4 exajoules (EJ) in 1990 to 39.5 EJ in 2023, an increase of nearly two-thirds. In 2023, fuelwood accounted for about 22 EJ, and “other vegetal materials and residues” another 7 EJ, while biogasoline (which includes bioethanol) reached around 2.3 EJ. Liquid and gaseous biofuels grew at average annual rates of roughly 9% and 8% from 1990 to 2023, much faster than traditional solid biofuels.

Energy statistics from the International Energy Agency add more momentum to this trend. In its Renewables 2023 work, the IEA estimates that global biofuel demand will expand by about 38 billion litres between 2023 and 2028. That is a 23% increase, bringing total demand up to roughly 200 billion litres by 2028. Ethanol and renewable diesel are expected to account for about two-thirds of this growth. In a newer outlook, the IEA notes that the share of biofuels in total liquid transport fuel demand is set to rise from 5.6% in 2023 to 6.4% in 2030, reaching around 215 billion litres a year, or about 5.7 EJ of energy.

Perhaps the most visible signal of this trend comes from major tire makers. Michelin has publicly committed to producing tires made entirely from renewable, recycled or otherwise sustainable materials by 2050, with an interim target of 40% sustainable materials by 2030. In 2023, the company even won an award for a passenger car tire containing 45% sustainable materials and has demonstrated concepts with up to 58% sustainable content.

Drivers

Growing bio-based feedstock supply is pushing the Bio-Butadiene market forward

One major driving factor for the bio-butadiene market is the rapid growth in sustainable bio-based feedstocks, especially biofuels and biomass coming from the wider food and agriculture system. Bio-butadiene is typically produced from bioethanol, so the health of global bioenergy directly shapes its future.

- According to FAO’s Bioenergy statistics 1990–2023, world bioenergy final consumption reached about 40 exajoules (EJ) in 2023, with 35.0 EJ from solid biofuels, 4.4 EJ from liquid biofuels (about 11%) and 0.1 EJ from gaseous biofuels (0.3%). Over 1990–2023, liquid biofuels such as ethanol grew at roughly 9% per year, while gaseous biofuels grew about 8% per year on average, showing how quickly modern bioenergy has scaled from agricultural and forestry resources.

This expansion continues in the transport sector, which is crucial for bio-butadiene because it underpins large bioethanol streams that can be upgraded into the monomer. The International Energy Agency (IEA) expects global biofuel demand to increase by about 38 billion litres between 2023 and 2028, lifting total demand by around 23% to nearly 200 billion litres by 2028. Ethanol and renewable diesel together account for roughly two-thirds of this additional volume, reinforcing ethanol’s role as a central renewable platform molecule.

Beyond fuels, modern bioenergy as a whole is being asked to carry more of the global energy transition. In the IEA’s Net Zero pathways, modern bioenergy rises from around 21 EJ in 2023, or 4.5% of total final energy consumption, to about 39 EJ in 2030, roughly 9.5% of final consumption. In longer-term scenarios, IEA Bioenergy estimates that modern bioenergy may need to reach around 100 EJ by 2050 and meet close to 20% of total energy supply. For bio-butadiene producers, this means that feedstock availability is not a niche story; global policy expectations are actively pushing biomass, residues and biofuels into the centre of the energy and materials system, creating a broader and more reliable base for renewable C4 chemicals.

Government strategies around the bioeconomy add another layer of support to this same driver. The European Commission’s Bioeconomy and Bio-based Products initiatives explicitly aim to build lead markets for bio-based materials, biochemicals and agri-food value chains, linking agricultural biomass and side-streams to new chemical and materials applications, including elastomers and plastics that can use bio-butadiene as a building block. These programmes sit under the broader EU Green Deal objective of climate neutrality by 2050, with dedicated funding frameworks such as the Circular Bio-based Europe Joint Undertaking to accelerate industrial projects.

Restraints

Feedstock Competition with Food and Land Use

One of the most significant restraining factors in the growth of the bio-butadiene market is the competition for bioethanol feedstock with food and agriculture sectors, which creates pressure on land use, crop pricing, and food security. Because bio-butadiene production relies heavily on bioethanol as a precursor, anything that limits the availability or increases the cost of ethanol directly affects the viability and cost-competitiveness of bio-butadiene. Globally, this tension between fuel/chemical feedstock and food production is well documented in biofuel economies — especially where arable land is limited and food security remains a central policy priority.

Moreover, ethanol production from certain feedstocks like molasses, cassava or palm oil faces constraints due to technical and infrastructure challenges, which further limit how quickly feedstock volumes can be increased without affecting food supply chains. For instance, FAO technical analyses note that significant technological improvements are still needed to make ethanol from lignocellulosic biomass commercially competitive and scalable — feedstock types that would otherwise relieve pressure on food crops. Because these advanced ethanol routes are not yet mainstream, reliance on traditional food-related biomass persists.

Government policies attempt to balance these competing interests, but this balance is delicate. Policies that mandate high blending rates of ethanol into fuels increase ethanol production, but these mandates can unintentionally push food crop prices higher if supply does not keep pace with both food and industrial demand. For example, historic bioethanol blend mandates in some countries have required higher ethanol supply without commensurate growth in cellulosic capacity, creating market distortions that ripple into agrichemical supply chains and food pricing dynamics.

Opportunity

Turning agricultural residues into a new growth engine for bio-butadiene

A major growth opportunity for the bio-butadiene market lies in using agricultural residues and food-system side streams as feedstock for bioethanol, and then converting that ethanol into bio-butadiene. Instead of relying on sugar or starch crops that also feed people, the industry can tap crop residues, straw, husks and other by-products that are currently under-used. Global energy and food agencies see these residues as a key pillar of the future bioeconomy, which creates a strong long-term opportunity for bio-based chemicals such as bio-butadiene.

Recent work by the International Renewable Energy Agency (IRENA) shows just how large this resource pool could become. In its World Energy Transitions Outlook 1.5 °C scenario, IRENA projects that bioenergy will need to supply about 22% of total primary energy by 2050, requiring up to 135 exajoules (EJ) of sustainable biomass, compared with around 56 EJ in 2020. Agricultural residues are expected to play a major role in meeting this gap.

FAO’s latest bioenergy statistics confirm that residues are already important, even before full-scale deployment of advanced technologies. In 2023, global bioenergy final consumption reached about 40 EJ, up from roughly 24 EJ in 1990. Of this, solid biofuels dominated with 35.0 EJ (89%), while liquid biofuels accounted for 4.4 EJ (11%) and gaseous biofuels for 0.1 EJ (0.3%). Within solid biofuels, FAO notes that “other vegetal materials and residues” contributed around 7 EJ, alongside 22 EJ from fuelwood, meaning that residues and traditional biomass together made up nearly 80% of global bioenergy use.

- The International Energy Agency adds another piece to the picture through its biofuel outlook. In its Renewables 2023 analysis, the IEA expects total biofuel demand to rise by about 38 billion litres between 2023 and 2028, a 23% increase that takes consumption to roughly 200 billion litres. Ethanol and renewable diesel are projected to provide about two-thirds of this growth.

Regional Insights

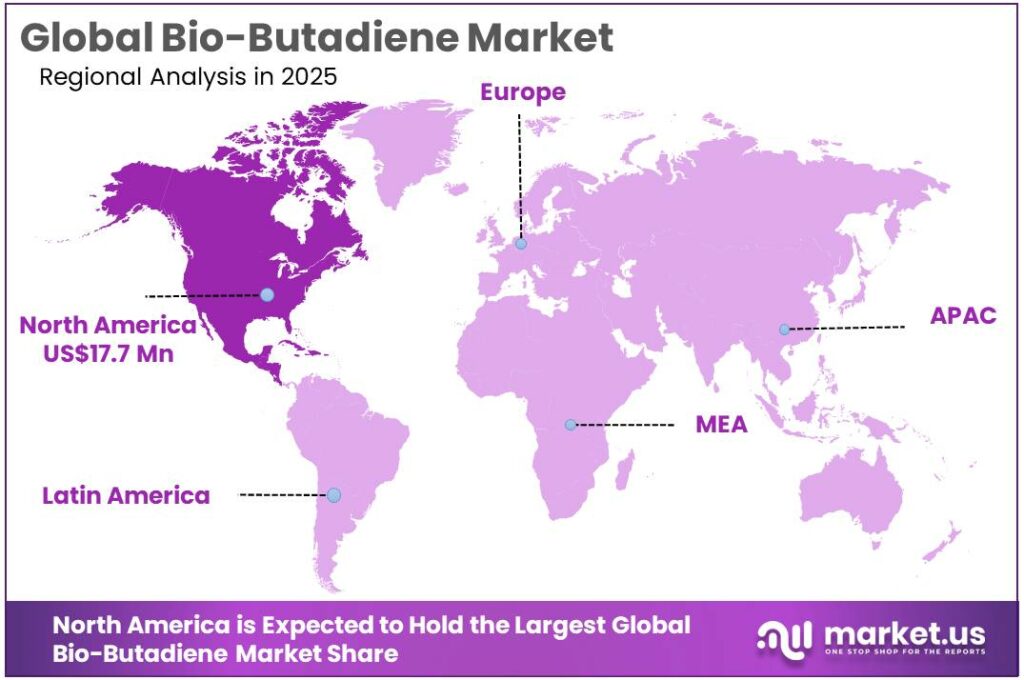

North America leads the bio-butadiene landscape with 43.8% share and 17.7 Mn value

In 2024, North America held a dominant position in the bio-butadiene market, capturing around 43.8% of global share with an estimated value of roughly 17.7 Mn. This leadership is underpinned by the region’s strong automotive and tire manufacturing base, combined with one of the world’s most mature bioethanol and biomass infrastructures.

The United States alone produced about 15.4 billion gallons of fuel ethanol in 2023, according to the U.S. Energy Information Administration (EIA), providing a deep feedstock pool for potential ethanol-to-butadiene routes. This scale is reinforced by federal policy: under the Renewable Fuel Standard (RFS), renewable fuel volume obligations are set to rise from 20.94 billion ethanol-equivalent gallons in 2023 to 22.33 billion gallons in 2025, signalling continued policy support for bio-based feedstocks that bio-butadiene producers can leverage.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Michelin is one of the most visible industrial users driving bio-butadiene development. Through the BioButterfly™ project with IFPEN and Axens, it inaugurated in January 2024 the first industrial-scale demonstrator producing bio-based butadiene from bioethanol at Bassens, with a capacity of 20–30 tonnes per year. The company sells around 200 million tires annually and targets 40% renewable or recycled materials in its tires by 2030, rising to 100% by 2050, creating strong downstream pull for bio-butadiene.

Trinseo positions bio-butadiene as a cornerstone of its sustainable solutions strategy. In 2021, it signed a letter of intent with ETB to develop purified bio-based 1,3-butadiene, combining catalyst and process know-how to create renewable feedstock for performance tires and specialty polymers. As of 2023, Trinseo reported net sales of about US$3.7 billion and employs roughly 3,100 people worldwide, giving it the scale to commercialize bio-based intermediates once the technology is proven.

SABIC is emerging as a key enabler of renewable butadiene through its TRUCIRCLE™ portfolio. In 2022 it started supplying certified renewable butadiene to Kraton for bio-based styrenic block copolymers, marking one of the first commercial uses of renewable C4 streams. In 2023, SABIC reported total chemical production of about 53.5 million metric tons and set a target of 1 million metric tons per year of TRUCIRCLE sales by 2030, giving scale to future bio-butadiene offerings.

Top Key Players Outlook

- SABIC

- Michelin

- Zeon Corporation

- Trinseo

- Braskem

- Versalis

- Lummus Technology

- Invista

- Evonik Industries

- Synthos

Recent Industry Developments

In February 2025, SABIC announced that net income for 2024 had recovered to SAR 1.5 billion, from a net loss of SAR 2.8 billion in 2023, giving it more financial room to back low-carbon platforms.

In 2024, Braskem reported a strong financial performance with Recurring EBITDA of US$1.1 billion, up 46% from 2023, and maintained a healthy cash position of approximately US$2.4 billion, giving it financial resilience to invest in sustainable chemical pathways.

Report Scope

Report Features Description Market Value (2025) USD 40.5 Mn Forecast Revenue (2035) USD 94.6 Mn CAGR (2026-2035) 8.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Grade (Industrial Grade, Laboratory Grade), By Application (Styrene Butadiene Rubber (SBR), Styrene Butadiene Latex (SBL), Polybutadiene (PB), Acrylonitrile-Butadiene-Styrene (ABS), Styrene-Butadiene Block Copolymers (SBS And SEBS), Nitrile Butadiene Rubber (NBR), Others), By End Use (Automotive And Transportation, Consumer Goods, Chemical Processing, Building And Construction, Healthcare, Textile, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape SABIC, Michelin, Zeon Corporation, Trinseo, Braskem, Versalis, Lummus Technology, Invista, Evonik Industries, Synthos Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- SABIC

- Michelin

- Zeon Corporation

- Trinseo

- Braskem

- Versalis

- Lummus Technology

- Invista

- Evonik Industries

- Synthos

Our Clients

- 179836

- Mar 2026