Global Automotive Vents Market Size, Share, Growth Analysis By Material (Polytetrafluoroethylene (PTFE), Polypropylene (PP), Polyethylene (PE)), By Functionality (Climate Control Vents, Air Intake Vents, Exhaust Vents, Cabin Ventilation Vents), By Mechanism (Manual, Electronic), By Propulsion (Gasoline, Diesel, BEV, PHEV, HEV, Others), By Vehicle (Passenger Vehicle, Commercial Vehicle), By Vent (Filter Vents, Cap Vents, Adhesive Vents), By Application (Powertrain Components, Electronics, Lighting, Interior and Exterior Components, Others), By Distribution Channel (OEM, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179345

- Number of Pages: 326

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Material Analysis

- Functionality Analysis

- Mechanism Analysis

- Propulsion Analysis

- Vehicle Analysis

- Vent Analysis

- Application Analysis

- Distribution Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

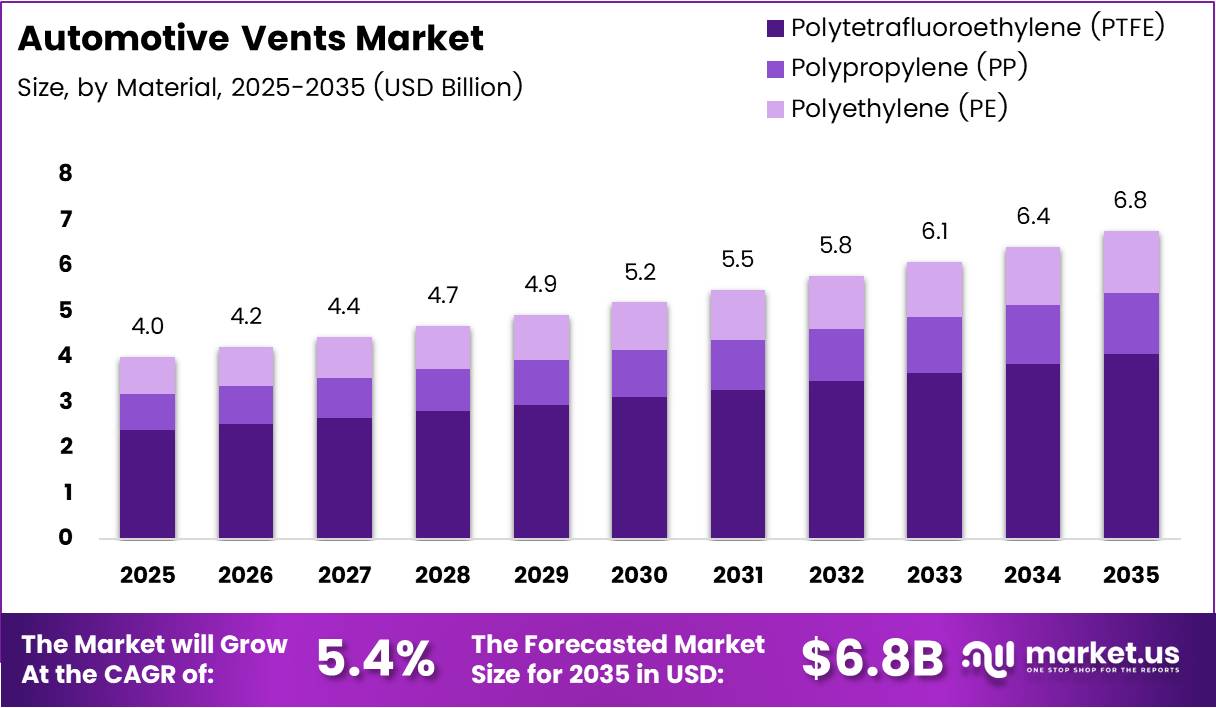

Global Automotive Vents Market size is expected to be worth around USD 6.8 Billion by 2035 from USD 4.0 Billion in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

The automotive vents market covers a broad set of pressure-management, moisture-control, and airflow-regulation components embedded across vehicle systems. These include cabin ventilation vents, filter vents, exhaust vents, and powertrain-integrated vent systems. Together, they protect electronics, battery packs, lighting modules, and interior components from pressure imbalance and environmental contamination.

Passenger vehicles account for the structural backbone of this market, with OEM procurement channels controlling 82.5% of distribution. This concentration signals that the market’s growth trajectory is closely tied to OEM platform decisions — meaning suppliers who secure design-in positions early in vehicle development cycles gain durable, long-cycle revenue streams that are difficult for aftermarket competitors to displace.

Electric and hybrid vehicle adoption fundamentally reshapes demand for automotive ventilation systems. Battery packs require precise pressure equalization and thermal venting to prevent thermal runaway — a safety-critical function that standard legacy vents cannot fulfill. This structural shift forces OEMs to qualify entirely new vent architectures, creating a product replacement cycle that benefits specialized vent manufacturers over generalist component suppliers.

Polytetrafluoroethylene (PTFE) and advanced membrane materials now define the technical frontier of this space. These materials allow selective gas permeation while blocking liquids and particulates — a performance combination that conventional polymers cannot match. As vehicle platforms become more electronically dense, the need for membrane-grade venting solutions across lighting, sensors, and cabin systems compounds the addressable market for high-specification vent components.

According to a study published on PubMed, application of 70% air recirculation reduced PM₂.₅ concentrations in vehicle cabins by approximately 55% with a new filter and 39% with an aged filter. This quantifies the direct performance dependency between vent quality and in-cabin air safety — a metric that OEM procurement teams and regulators increasingly reference when specifying ventilation component standards.

Further reinforcing this, research published via MDPI shows that overall in-vehicle PM₂.₅ mass concentration reached as low as ~0.69 µg/m³ in recirculation mode, compared to ~7.68 µg/m³ in outside-air mode — an 11x difference. For suppliers, this performance gap positions advanced recirculation-compatible vent systems as a regulatory compliance tool, not merely a comfort feature, opening a higher-value procurement category within cabin air quality management.

Key Takeaways

- The global Automotive Vents Market was valued at USD 4.0 Billion in 2025 and is forecast to reach USD 6.8 Billion by 2035.

- The market grows at a CAGR of 5.4% during the forecast period 2026 to 2035.

- By Material, Polytetrafluoroethylene (PTFE) leads with a 45.2% market share.

- By Functionality, Climate Control Vents hold the dominant position with 34.7% share.

- By Mechanism, Manual vents dominate with 67.8% share.

- By Propulsion, Gasoline vehicles lead with 44.9% share.

- By Vehicle, Passenger Vehicles account for 78.1% of the market.

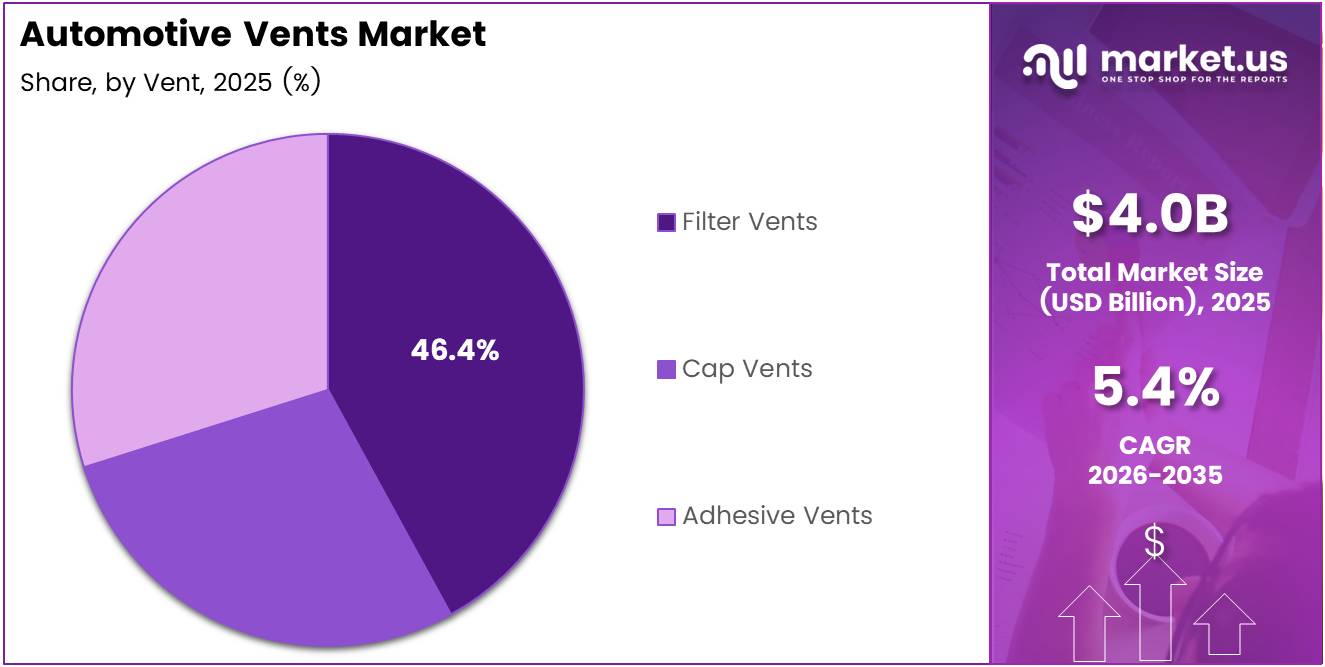

- By Vent type, Filter Vents hold the largest share at 46.4%.

- By Application, Powertrain Components represent the top segment at 34.6%.

- By Distribution Channel, OEM channels dominate with 82.5% share.

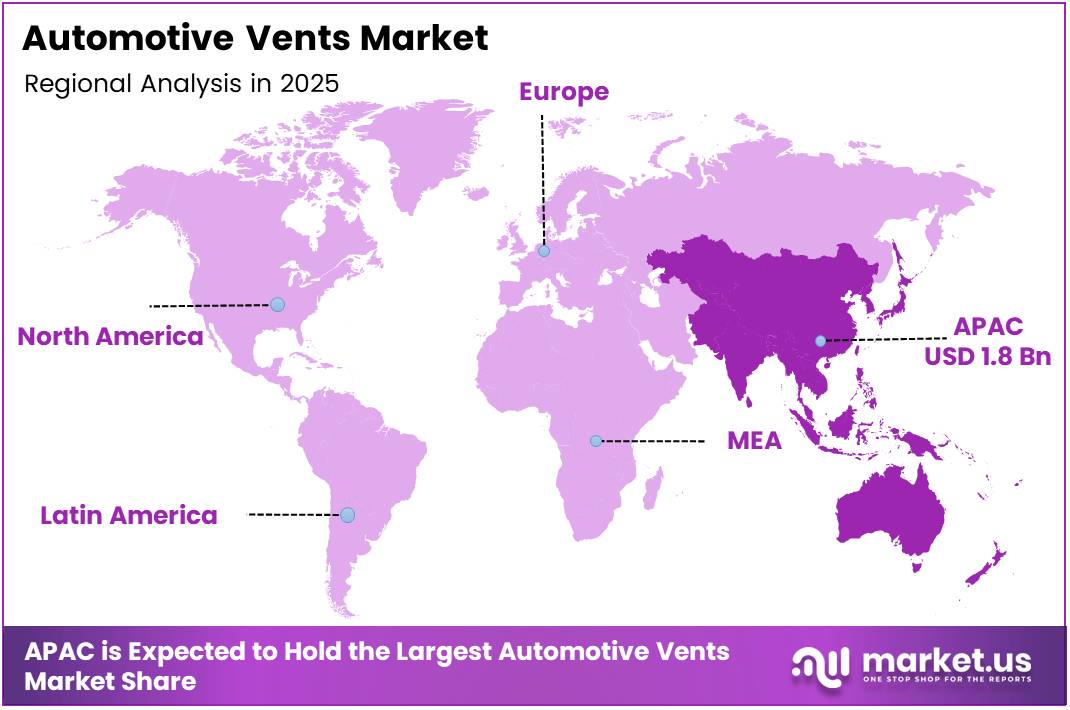

- Asia Pacific leads all regions with a 46.30% share, valued at USD 1.8 Billion.

Material Analysis

Polytetrafluoroethylene (PTFE) dominates with 45.2% due to superior chemical resistance and membrane-grade filtration.

In 2025, Polytetrafluoroethylene (PTFE) held a dominant market position in the By Material segment of the Automotive Vents Market, with a 45.2% share. PTFE’s ability to allow selective gas passage while blocking liquids and particulates makes it the default material for high-performance vent applications. This structural advantage means PTFE-based vents command premium pricing and face lower substitution risk than commodity polymer alternatives.

Polypropylene (PP) serves as the cost-efficient alternative for applications where membrane-grade performance is not required. PP vents find wide use in cabin and interior component ventilation where moderate chemical exposure and pressure differentials are the norm. However, PP’s lower thermal ceiling limits its use in powertrain and battery-adjacent applications, concentrating PP demand in lower-specification vehicle segments.

Polyethylene (PE) differentiates through flexibility and processability, making it suitable for shaped or contoured vent components in interior assemblies. PE’s lower rigidity compared to PP and PTFE restricts its share in high-load mechanical vent positions. Consequently, PE remains a secondary material choice, with its market position tied largely to cost-competitive applications rather than performance-driven procurement decisions.

Functionality Analysis

Climate Control Vents dominate with 34.7% due to direct linkage to occupant comfort mandates across all vehicle classes.

In 2025, Climate Control Vents held a dominant market position in the By Functionality segment of the Automotive Vents Market, with a 34.7% share. Their dominance reflects the fact that thermal comfort systems are standard across every vehicle segment — from entry-level hatchbacks to premium SUVs. This universal fitment ensures stable, volume-driven demand regardless of powertrain type or vehicle platform generation.

Air Intake Vents carry critical airflow management functions for both combustion engine performance and battery thermal regulation in electrified platforms. As BEV and PHEV architectures scale, air intake vent specifications are being reengineered to handle higher thermal loads. Suppliers capable of qualifying intake vent designs for electrified platforms position themselves to capture a dual-market opportunity across both legacy and next-generation vehicle programs.

Exhaust Vents manage pressure equalization and heat dispersal in enclosed component housings, including battery enclosures and lighting modules. Their role becomes more technically demanding as vehicle electronics density increases. Therefore, exhaust vent specifications are rising — from simple pressure-relief designs toward membrane-integrated solutions that combine outgassing control with ingress protection.

Cabin Ventilation Vents directly determine in-cabin air quality outcomes, a function that occupant health data increasingly supports as a core vehicle specification — not a secondary feature. Regulatory focus on particulate matter and CO₂ management inside vehicle cabins elevates the procurement priority of high-performance cabin vents. This shifts buyer conversation from unit cost toward performance certification.

Mechanism Analysis

Manual vents dominate with 67.8% due to lower cost and universal fitment across mass-market vehicle platforms.

In 2025, Manual vents held a dominant market position in the By Mechanism segment of the Automotive Vents Market, with a 67.8% share. Their dominance reflects the volume reality of global vehicle production — the majority of vehicles manufactured globally are cost-optimized platforms where electronic actuation adds complexity without proportional consumer value. Manual vent dominance is therefore a volume story, not a technology preference.

Electronic vents represent the higher-margin, lower-volume segment where growth is structurally tied to electrification and autonomous vehicle adoption. Electronic actuation enables precision airflow control, integration with HVAC software systems, and remote cabin conditioning — capabilities increasingly demanded in premium BEV and PHEV platforms. As electrified vehicle share expands, electronic vent penetration will follow, compressing the manual-to-electronic ratio over the forecast period.

Propulsion Analysis

Gasoline vehicles dominate with 44.9% due to their current global production volume leadership.

In 2025, Gasoline vehicles held a dominant market position in the By Propulsion segment of the Automotive Vents Market, with a 44.9% share. This reflects the current installed base and production volume of internal combustion engine vehicles globally. However, this dominance is structurally time-limited as electrification mandates in major markets accelerate platform transitions away from pure gasoline powertrains.

Diesel vehicles contribute a declining share, with their market position under pressure from emissions regulations in Europe and Asia. However, diesel commercial vehicles retain relevance in heavy-load applications where alternatives remain technically and economically unviable. Vent suppliers serving diesel commercial platforms face a mature but stable demand profile rather than outright volume contraction in the near term.

Battery Electric Vehicles (BEV) represent the fastest-shifting demand segment for automotive vent manufacturers. BEV battery packs require dedicated pressure equalization, thermal venting, and moisture management systems — all of which differ fundamentally from combustion engine vent applications. This creates a new vent specification category with higher technical barriers and correspondingly higher margin potential for qualifying suppliers.

Plug-in Hybrid Electric Vehicles (PHEV) combine combustion and battery vent requirements within a single platform, creating compound complexity for vent system design. PHEV vent systems must manage both engine-bay thermal loads and battery enclosure pressure — a dual-function demand that pushes procurement toward integrated vent solutions rather than single-application components.

Hybrid Electric Vehicles (HEV) occupy a transitional position in the market, retaining significant combustion vent demand while introducing initial battery-adjacent ventilation requirements. HEV platforms serve as the engineering bridge across which many OEMs are qualifying next-generation vent designs before full BEV program rollout.

Others — including fuel cell electric vehicles and alternative fuel platforms — remain a minor but technically distinct vent demand segment. Hydrogen fuel cell systems introduce unique venting requirements around hydrogen safety management and stack cooling. Though volumetrically small today, these platforms represent a long-cycle development opportunity for specialized vent manufacturers with membrane expertise.

Vehicle Analysis

Passenger Vehicles dominate with 78.1% due to global production volume and universal vent fitment requirements.

In 2025, Passenger Vehicles held a dominant market position in the By Vehicle segment of the Automotive Vents Market, with a 78.1% share. The sheer scale of global passenger vehicle production sustains this dominance across all vent types — cabin, filter, exhaust, and powertrain. Moreover, rising consumer expectations for cabin air quality and comfort in passenger vehicles continue to drive vent specification upgrades at the OEM design level.

Hatchback platforms serve as the entry-level volume anchor for automotive vent demand, particularly in cost-competitive Asian and European markets. Hatchback vent specifications typically favor PP and PE materials over PTFE, reflecting the cost optimization priorities of this segment. Nevertheless, volume scale means hatchbacks remain a significant base for standardized vent component programs.

Sedan platforms occupy the mid-tier of passenger vehicle vent demand, where OEMs balance comfort performance with cost efficiency. Sedans increasingly specify climate control and cabin ventilation upgrades as market differentiation tools. This elevates vent component specifications beyond commodity-level, creating supplier opportunities in feature-grade vent assemblies for this segment.

SUV platforms carry the highest per-unit vent content value within the passenger vehicle segment, driven by larger cabin volumes, higher electronic content, and premium HVAC system fitment. SUV programs increasingly specify membrane-grade filter vents and electronic cabin ventilation — a combination that directly benefits suppliers positioned in high-performance vent categories.

Commercial Vehicles represent a structurally distinct demand profile, where vent durability and resistance to harsh operating environments take precedence over weight or cost optimization. Commercial vehicle vent specifications are set by fleet operators and logistics companies with high replacement cost sensitivity, making long-life vent designs a critical purchasing criterion in this segment.

Light Commercial Vehicles (LCV) form the highest-volume commercial vent demand tier, driven by e-commerce logistics growth and last-mile delivery fleet expansion globally. LCV vent requirements combine cabin comfort with powertrain durability — a specification range that aligns well with mid-grade PTFE and PP vent products.

Medium Commercial Vehicles (MCV) serve regional freight and distribution applications where route length and load cycles place sustained thermal stress on powertrain vent systems. MCV vent procurement is typically fleet-driven and replacement-oriented, with aftermarket channels playing a larger role compared to passenger vehicle procurement patterns.

Heavy Commercial Vehicles (HCV) represent the highest per-unit vent specification demand within the commercial segment. HCV powertrain vent systems must withstand extreme temperature cycling, vibration, and chemical exposure over high-mileage service lives. This performance requirement positions PTFE-based vent systems as the material of choice for HCV powertrain applications.

Vent Analysis

Filter Vents dominate with 46.4% due to dual function combining pressure equalization and contamination protection.

In 2025, Filter Vents held a dominant market position in the By Vent segment of the Automotive Vents Market, with a 46.4% share. Filter vents combine pressure equalization with particulate and liquid ingress protection — a dual function that makes them the default specification across powertrain, electronics, and lighting enclosures. Their multi-application utility directly drives per-vehicle fitment volume, compounding demand beyond single-use vent categories.

Cap Vents serve simpler pressure-relief applications where filtration is secondary and mechanical reliability under thermal cycling is the primary performance criterion. Cap vents find use in fluid reservoirs, transmission housings, and lower-sensitivity electronics enclosures. Their lower technical barrier creates more supplier competition and tighter pricing dynamics relative to filter and adhesive vent categories.

Adhesive Vents differentiate through their mounting flexibility — bonding directly to enclosure surfaces without requiring a molded port or threaded housing. This installation simplicity makes adhesive vents increasingly attractive for compact electronics and sensor enclosures where design space constraints preclude traditional vent fittings. Additionally, adhesive vent adoption rises with vehicle electronics density, linking their demand directly to electrification platform growth.

Application Analysis

Powertrain Components dominate with 34.6% due to thermal and pressure management criticality in engine and battery systems.

In 2025, Powertrain Components held a dominant market position in the By Application segment of the Automotive Vents Market, with a 34.6% share. Powertrain vent systems manage pressure differentials and thermal venting in engine housings, transmission systems, and increasingly in battery enclosures. The criticality of failure prevention in powertrain applications drives OEM specification of premium vent materials, supporting higher average selling prices in this segment.

Electronics applications represent the fastest-shifting demand area, as vehicle electronic content per unit continues to rise across all platform types. Sensors, control modules, and power electronics require reliable ingress protection through precisely specified vent systems. As ADAS and software-defined vehicle architectures expand, electronics vent fitment per vehicle increases — directly expanding addressable volume for filter and adhesive vent suppliers.

Lighting applications require vents that manage thermal expansion-driven pressure cycles without allowing moisture ingress — a performance combination that favors PTFE membrane vents. LED and matrix lighting systems run at higher temperatures than halogen predecessors, raising vent specification requirements. Suppliers who have established PTFE vent qualifications for lighting OEM programs benefit from the ongoing LED conversion across global vehicle fleets.

Interior and Exterior Components cover a diffuse set of vent applications including door panels, exterior trim, mirror housings, and acoustic management systems. These applications typically specify lower-grade vent materials, but their combined volume across a vehicle contributes meaningfully to total vent content per unit. Design simplification trends in this category increasingly favor adhesive vent formats for fitment efficiency.

Others include niche and emerging vent application categories such as fuel systems, safety sensors, and HVAC component housings. While individually small, these applications often carry disproportionate technical requirements — and consequently higher margin potential — for suppliers capable of meeting specialized performance certifications in safety-critical environments.

Distribution Channel Analysis

OEM channels dominate with 82.5% due to design-in requirements and long-cycle supply agreements.

In 2025, OEM channels held a dominant market position in the By Distribution Channel segment of the Automotive Vents Market, with an 82.5% share. OEM dominance reflects the design-in nature of automotive vent procurement — vents are specified at the platform engineering stage, locking in suppliers for the production life of the vehicle program. This creates high switching costs and durable revenue streams for qualified OEM vent suppliers.

Aftermarket channels serve replacement and retrofit demand across the installed vehicle base, with commercial vehicles and older passenger vehicles driving the majority of aftermarket vent volume. While the aftermarket’s 17.5% share appears modest, it offers distinct strategic value — shorter sales cycles, direct-to-fleet relationships, and exposure to vehicle segments underserved by OEM specification upgrades. Aftermarket growth is structurally supported by the expanding global vehicle parc and rising replacement demand for long-life vent systems.

Key Market Segments

By Material

- Polytetrafluoroethylene (PTFE)

- Polypropylene (PP)

- Polyethylene (PE)

By Functionality

- Climate Control Vents

- Air Intake Vents

- Exhaust Vents

- Cabin Ventilation Vents

By Mechanism

- Manual

- Electronic

By Propulsion

- Gasoline

- Diesel

- BEV

- PHEV

- HEV

- Others

By Vehicle

- Passenger Vehicle

- Hatchback

- Sedan

- SUV

- Commercial Vehicle

- Light Commercial Vehicle (LCV)

- Medium Commercial Vehicle (MCV)

- Heavy Commercial Vehicle (HCV)

By Vent

- Filter Vents

- Cap Vents

- Adhesive Vents

By Application

- Powertrain Components

- Electronics

- Lighting

- Interior and Exterior Components

- Others

By Distribution Channel

- OEM

- Aftermarket

Drivers

Electrification and Safety Regulations Redefine Vent Specifications Across Vehicle Platforms

Rising global vehicle production across passenger and commercial segments compounds total vent demand per production cycle. Platform diversification — particularly the parallel growth of BEV, PHEV, and HEV architectures alongside conventional gasoline and diesel platforms — forces vent manufacturers to maintain multiple qualified product families simultaneously. Suppliers unable to span both legacy and electrified platform requirements face structural revenue concentration risk.

Thermal management in electric and hybrid vehicles creates a qualitatively different vent requirement from combustion-era specifications. Battery enclosures demand pressure equalization systems capable of handling rapid outgassing events without allowing moisture ingress — a combination that directly disqualifies standard cap vent and low-grade polymer solutions. According to research published via MDPI, in-cabin CO₂ dropped from approximately ~1,150 ppm to ~850 ppm as vehicle speed increased from 40 km/h to 120 km/h in recirculation mode, illustrating how airflow dynamics directly determine cabin air quality outcomes and reinforcing the performance standard now expected of integrated vent systems.

Stringent automotive safety and component durability regulations push OEMs to specify high-performance vent materials — particularly PTFE membranes — across battery, lighting, and electronics enclosures. Regulatory certification requirements create qualification barriers that favor established vent suppliers with existing OEM approvals. Consequently, new entrants face a structurally longer path to capture OEM design-in positions, concentrating near-term revenue growth among qualified incumbent suppliers.

Restraints

Raw Material Price Volatility and Platform Complexity Compress Vent Supplier Margins

Automotive raw material price volatility — particularly for polymer resins including PTFE, PP, and PE — directly squeezes vent manufacturing cost structures. Since material costs represent a significant input in vent production, price spikes reduce gross margins for suppliers operating under fixed OEM supply agreements. This dynamic particularly disadvantages smaller vent manufacturers who lack the procurement scale to hedge raw material exposure.

Vehicle design complexity continues to rise as platforms integrate higher electronics density, multi-material assemblies, and electrified powertrain architectures. Each new platform iteration requires custom vent qualification — a process that consumes engineering resources and extends time-to-revenue for vent suppliers. According to MDPI research, estimated natural ventilation leakage airflow ranged from approximately ~0.01025 m³/s at 60 km/h to ~0.0141 m³/s at 120 km/h, demonstrating that vehicle airflow dynamics vary significantly by operating condition — a variance that complicates standardized vent design and limits interchangeability across platform variants.

The combination of material cost pressure and platform standardization barriers creates a structural margin squeeze for vent suppliers dependent on OEM program revenues. Suppliers without proprietary material formulations or differentiated membrane technologies face increasing pricing pressure from OEM procurement teams seeking cost-out on maturing platform designs. Therefore, investment in material innovation is not optional — it is the mechanism through which suppliers protect their margin position over the program lifecycle.

Growth Factors

EV Battery Venting, Lightweight Design, and Aftermarket Demand Open New Revenue Tiers for Vent Manufacturers

Electric vehicle battery venting solutions represent the highest-value new product category in the automotive vents market. Battery thermal runaway events require dedicated pressure-relief and outgassing management systems — specifications that standard vent platforms cannot fulfill. In March 2025, Eaton unveiled its 3-in-1 battery vent valve for electrified vehicles, a single solution combining passive and active venting, leak-check capability, and resealing technology designed to meet the SAE J3277 standard — a product launch that directly validates the commercial scale of EV-specific vent demand.

Lightweight and compact vent designs for next-generation mobility platforms create a material and engineering differentiation opportunity. As vehicle platforms target mass reduction targets, bulky legacy vent housings become design liabilities. Suppliers who develop thin-profile, adhesive-mounted, or membrane-integrated vent solutions position themselves for specification wins on weight-sensitive EV and autonomous vehicle platforms where packaging constraints are acute.

According to research published via TRID, real-drive sensor studies showed average PM₂.₅ removal efficiencies of approximately ~17–50% under fresh-air mode with existing cabin filters, rising to ~80–86% removal with brand-new filters and up to ~97% with optimized ionization-enhanced filters. This performance range directly frames the aftermarket replacement opportunity — aging filter vents represent a measurable in-cabin air quality degradation that fleet operators and health-conscious consumers increasingly act to correct, sustaining aftermarket vent replacement demand across the expanding global vehicle parc.

Emerging Trends

Smart Membrane Technologies and Sustainable Materials Reshape Vent Product Roadmaps

Smart membrane-based vent technologies move the product category from passive pressure relief toward active environmental management. ePTFE membranes and next-generation composite materials enable vents to selectively manage gas permeation, moisture exclusion, and acoustic dampening within a single component. This multi-function capability shifts OEM procurement decisions from unit-cost comparison toward integrated performance value — a structural change that benefits suppliers with proprietary membrane platforms.

Noise-reduction and pressure-stabilization venting solutions respond to the heightened acoustic sensitivity of electric vehicle cabins. Without combustion engine noise masking, even minor pressure differentials through vent pathways become perceptible to occupants. According to a study published via MDPI, fresh-air mode maintained in-cabin CO₂ below approximately ~520 ppm at driving speeds above ~40 km/h, establishing a measurable performance benchmark that vent system designers now reference when specifying airflow and pressure management targets for next-generation cabin ventilation architectures.

OEM focus on sustainable and recyclable vent component materials reflects the broader vehicle lifecycle emissions commitments now embedded in OEM supplier codes of conduct. Recyclability requirements are beginning to influence material selection at the vent design stage — particularly for PP and PE-based components where end-of-life material recovery pathways exist. Suppliers who develop documented recyclability credentials for their vent product lines gain a qualification advantage as OEM sustainability sourcing criteria tighten across major automotive markets.

Regional Analysis

Asia Pacific Dominates the Automotive Vents Market with a Market Share of 46.30%, Valued at USD 1.8 Billion

Asia Pacific commands 46.30% of the global automotive vents market, valued at USD 1.8 Billion in 2025. China, Japan, South Korea, and India anchor this dominance through their combined passenger and commercial vehicle production scale. China’s accelerating BEV platform rollout further compounds vent demand by introducing battery-specific venting requirements across a high-volume production base that no other region matches in absolute unit output.

North America Automotive Vents Market Trends

North America holds a structurally important position in the automotive vents market, supported by a mature OEM procurement infrastructure and tightening federal emissions and safety standards. The U.S. market’s rapid EV adoption — driven by federal incentive programs and OEM electrification commitments — accelerates demand for battery-specific vent systems. Established Tier 1 supplier networks in the region provide vent manufacturers with direct OEM qualification access.

Europe Automotive Vents Market Trends

Europe’s automotive vents market benefits from the continent’s stringent Euro 7 emissions framework and aggressive CO₂ fleet average targets, both of which push OEMs toward electrified platforms requiring advanced vent solutions. Germany, France, and the UK concentrate the majority of European OEM program activity. Additionally, European OEMs lead on sustainability sourcing requirements, creating a first-mover advantage for vent suppliers with certified recyclable material portfolios.

Latin America Automotive Vents Market Trends

Latin America represents a volume-growth market for automotive vents, driven primarily by expanding vehicle production in Brazil and Mexico. Mexico’s deep integration into North American OEM supply chains positions it as a vent manufacturing hub serving both regional and export demand. However, lower average vehicle specification levels in Latin America favor cost-optimized PP and PE vent solutions over premium PTFE membrane products in the near term.

Middle East and Africa Automotive Vents Market Trends

The Middle East and Africa market for automotive vents centers on vehicle import activity and a growing aftermarket replacement segment, rather than domestic vehicle production at scale. Extreme operating temperatures across the region stress vent component performance — particularly thermal cycling durability — creating specification demand for high-grade vent materials in extreme-environment applications. GCC fleet operators increasingly prioritize long-life vent systems to reduce total ownership cost in high-temperature commercial vehicle operations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Berghof positions itself as a specialist in high-performance membrane and filtration solutions, a background that directly translates into competitive advantage in PTFE-based automotive vent applications. By leveraging deep materials science expertise, Berghof targets technically demanding vent specifications in electronics and powertrain enclosures — segments where material qualification barriers reduce direct price competition and support margin sustainability.

CREHERIT focuses on precision-engineered vent components for automotive electronics and battery applications, aligning its product portfolio with the fastest-shifting demand segments in the market. Its concentration on compact, high-performance vent formats positions it to benefit from the per-unit vent content increases driven by rising vehicle electronics density and electrified platform growth across Asian OEM programs.

Donaldson applies its filtration platform — built across industrial and aerospace markets — to automotive vent applications, providing OEM customers with validated performance data across multiple operating environments. In June 2024, Donaldson launched the Dual-Stage Jet battery vent, a high-performance venting system capable of rapidly degassing EV battery packs while significantly reducing the number of vents required per pack. This product launch directly addresses the OEM need to simplify EV battery architecture without sacrificing safety performance.

Nifco brings a strong OEM supply chain footprint in fastening and functional components, which it leverages to cross-sell automotive vent solutions within established procurement relationships. Nifco’s advantage lies in its embedded position across global OEM Tier 1 supply chains — a structural distribution advantage that independent vent specialists cannot replicate without equivalent investment in OEM qualification programs and regional manufacturing presence.

Key Players

- Berghof

- CREHERIT

- Donaldson

- Nifco

- Nitto Denko

- Parker Hannifin

- Porex

- W. L. Gore & Associates

- Weber

Recent Developments

- June 2024 – Donaldson Company, Inc. launched the Dual-Stage Jet battery vent, a high-performance venting system capable of rapidly degassing EV battery packs. The solution significantly reduces the number of vents required per battery pack, lowering system complexity and cost for OEM customers while meeting stringent EV safety standards.

Report Scope

Report Features Description Market Value (2025) USD 4.0 Billion Forecast Revenue (2035) USD 6.8 Billion CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Polytetrafluoroethylene (PTFE), Polypropylene (PP), Polyethylene (PE)), By Functionality (Climate Control Vents, Air Intake Vents, Exhaust Vents, Cabin Ventilation Vents), By Mechanism (Manual, Electronic), By Propulsion (Gasoline, Diesel, BEV, PHEV, HEV, Others), By Vehicle (Passenger Vehicle, Commercial Vehicle), By Vent (Filter Vents, Cap Vents, Adhesive Vents), By Application (Powertrain Components, Electronics, Lighting, Interior and Exterior Components, Others), By Distribution Channel (OEM, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Berghof, CREHERIT, Donaldson, Nifco, Nitto Denko, Parker Hannifin, Porex, W. L. Gore & Associates, Weber Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Berghof

- CREHERIT

- Donaldson

- Nifco

- Nitto Denko

- Parker Hannifin

- Porex

- W. L. Gore & Associates

- Weber

Our Clients

- 179345

- Feb 2026