Global Agricultural Inoculants Market Size, Share and Report Analysis By Type (Bacterial Inoculants, Fungal Inoculants, Others), By Microorganism (Bacteria, Fungi, Others), By Crop Type (Cereals And Grains, Oilseeds And Pulses, Fruits And Vegetables, Others), By Application (Seed Inoculation, Soil Inoculation), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 178691

- Number of Pages: 277

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

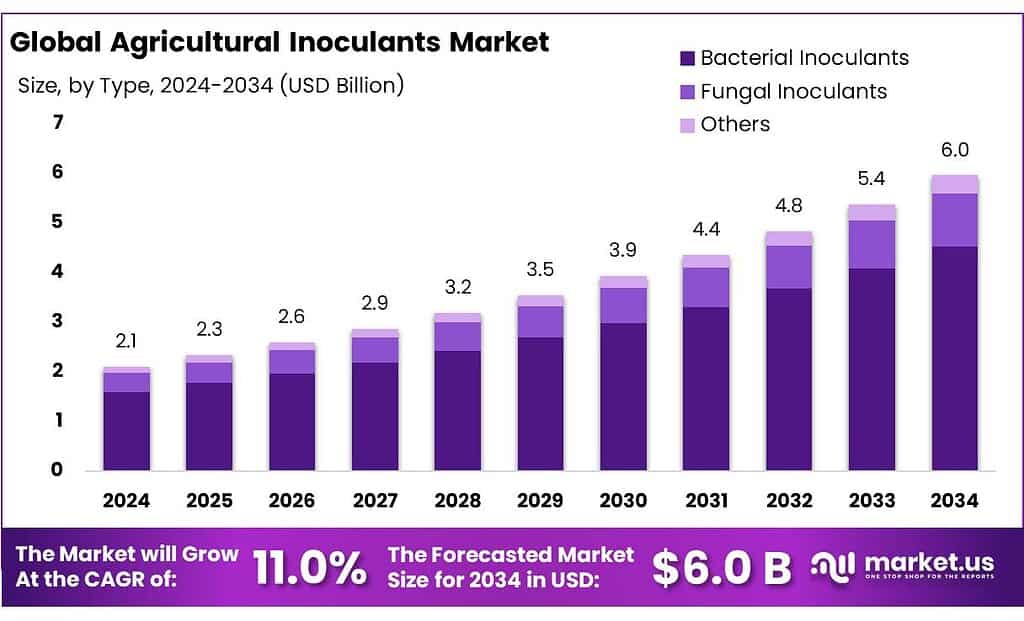

Global Agricultural Inoculants Market size is expected to be worth around USD 6.0 Billion by 2034, from USD 2.1 Billion in 2024, growing at a CAGR of 11.0% during the forecast period from 2025 to 2034. In 2024 North America held a dominant market position, capturing more than a 46.1% share, holding USD 16.9 Billion in revenue.

Agricultural inoculants sit at the intersection of microbiology and sustainable farming, providing live microorganisms that help crops fix nitrogen, solubilize phosphorus, or resist stress. They are increasingly viewed as a practical way to maintain yields while cutting synthetic inputs. The backdrop is a global soil and nutrient crisis: the Food and Agriculture Organization (FAO) estimates global use of inorganic fertilizers in 2022 at about 185 million tonnes of N, P and K nutrients, even after a 7% drop from 2021, underlining how dependent farming remains on mineral fertilizers.

- The Food and Agriculture Organization (FAO) reports that world production of inorganic fertilizers reached about 208 million tonnes in 2023, roughly 40 percent higher than in 2002, with nitrogen alone accounting for around 120 million tonnes, or 58 percent of output. At the same time, FAO and related UN assessments indicate that approximately 33 percent of the world’s arable land is already degraded, and around 100 million hectares of productive land have been lost each year between 2015 and 2019 due to land degradation.

Several structural drivers support this trajectory. First, the heavy use of synthetic fertilizers is under scrutiny: FAO data show global fertilizer consumption reaching tens of millions of tonnes annually, with individual countries such as China peaking at 55.61 million tonnes in 2014 before stabilising. Policymakers increasingly encourage biological alternatives or complements. In India, for example, the government promotes biofertilizers alongside soil-test–based nutrient management; official estimates place potential biofertilizer requirements at around 235,000 tonnes if 50% of cultivated area adopts them, highlighting the scale of latent demand.

Policy and regulatory signals also underpin the industrial outlook. Under the Farm to Fork strategy, the European Commission has set targets to reduce chemical pesticide use and overall fertilizer use by around 50% and at least 20% respectively by 2030, and to make 25% of EU farmland organic. Achieving such cuts without sacrificing yields effectively requires biological inputs, including microbial seed treatments and soil inoculants.

In the United States, projects funded by USDA National Institute of Food and Agriculture (NIFA) are testing phosphorus biofertilizers with the explicit goal of cutting synthetic or organic phosphorus fertilizer use by about 50% without lowering yields, providing a concrete public-sector benchmark for what inoculants are expected to deliver.

Government initiatives further underpin demand. In India, biofertilizers and related inoculant technologies are actively promoted under schemes such as Paramparagat Krishi Vikas Yojana (PKVY) and the Mission Organic Value Chain Development for North Eastern Region (MOVCDNER).

- Under PKVY, farmers receive INR 15,000 per hectare over three years via direct benefit transfer for organic inputs including biofertilizers, while MOVCDNER provides INR 32,500 per hectare over three years for similar inputs. Capacity-building initiatives complement these subsidies: in 2025, the ICAR-National Institute of Biotic Stress Management in India reached over 4,100 farmers in 49 villages across 10 districts, explicitly training them in biofertilizers and biocontrol agents during a government-led campaign.

Key Takeaways

- Agricultural Inoculants Market size is expected to be worth around USD 6.0 Billion by 2034, from USD 2.1 Billion in 2024, growing at a CAGR of 11.0%.

- Bacterial Inoculants held a dominant market position, capturing more than a 76.4% share.

- Bacteria held a dominant market position, capturing more than a 69.2% share.

- Cereals & Grains Component held a dominant market position, capturing more than a 47.3% share.

- North America stands as the clear demand centre, with the region holding a dominant 46.10% share, valued at around USD 16.9 billion.

By Type Analysis

Bacterial inoculants lead the field with a solid 76.4% share in 2024

In 2024, Bacterial Inoculants held a dominant market position, capturing more than a 76.4% share, reflecting how strongly farmers now rely on microbial solutions to improve soil health and nutrient use. This segment benefits from everyday pressures on growers to get higher yields from the same land while reducing chemical fertilizer use, so bacterial products naturally become the first choice in many cropping systems. Moving into 2025, the same drivers—tight fertilizer economics, stricter residue norms, and rising interest in regenerative farming—are expected to keep bacterial inoculants at the centre of purchasing decisions.

By Microorganism Analysis

Bacteria lead the inoculants space with a strong 69.2% share

In 2024, Bacteria held a dominant market position, capturing more than a 69.2% share, showing that growers increasingly trust bacterial strains for improving nutrient uptake and crop performance. Their wide compatibility with major crops like cereals, pulses, and oilseeds has made bacterial inoculants the most accessible and dependable category for farmers. By 2025, this segment continues to strengthen as producers focus on soil recovery, reduced chemical dependence, and more resilient cropping systems. Extension programs and on-farm demonstrations are steadily boosting confidence in microbial inputs, helping bacteria-based inoculants expand beyond traditional legume markets.

By Crop Type Analysis

Cereals & grains take the lead with a strong 47.3% share

In 2024, Cereals & Grains Component held a dominant market position, capturing more than a 47.3% share, reflecting how essential inoculants have become for high-volume staple crops like wheat, corn, rice, and barley. Farmers in major producing regions leaned heavily on microbial inputs to boost nutrient efficiency, especially nitrogen use, as fertilizer costs and soil fatigue remained constant challenges. This strong reliance helped cereals and grains remain the largest user group for inoculants throughout the year.

By Application Analysis

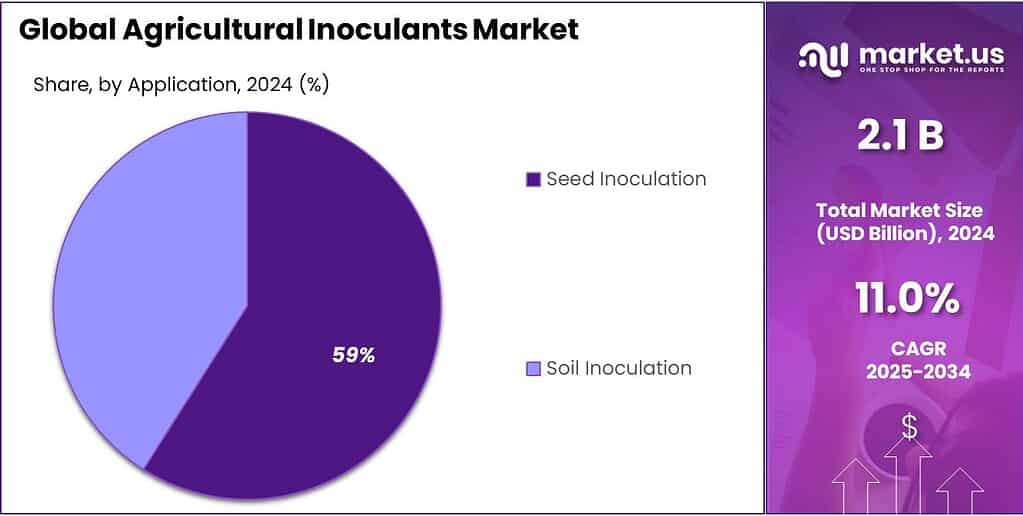

Seed inoculation leads the market with a firm 59.1% share

In 2024, Seed Inoculation held a dominant market position, capturing more than a 59.1% share, showing how strongly farmers prefer applying microbial inputs directly to seeds for better early-stage crop performance. This method became the most widely adopted because it is simple, low-cost, and ensures microbes reach the root zone at the exact moment seedlings need support. Growers across cereals, pulses, and oilseeds increasingly chose seed inoculation in 2024 to improve germination, strengthen root development, and boost nutrient uptake, especially nitrogen.

Key Market Segments

By Type

- Bacterial Inoculants

- Fungal Inoculants

- Others

By Microorganism

- Bacteria

- Rhizobacteria

- Azotobacter

- Phosphobacteria

- Others

- Fungi

- Trichoderma

- Mycorrhiza

- Others

- Others

By Crop Type

- Cereals & Grains

- Oilseeds & Pulses

- Fruits & Vegetables

- Others

By Application

- Seed Inoculation

- Soil Inoculation

Emerging Trends

Moving from single microbes to smart microbial consortia

One of the most important new trends in agricultural inoculants is the shift from single-strain products to carefully designed “microbial consortia” – mixes of bacteria and fungi that work together to support the plant and the soil. For years, many farmers knew inoculants mainly as rhizobium on legume seed. Now researchers and companies are experimenting with blends that fix nitrogen, solubilise phosphorus, release growth hormones, and help crops cope with drought or salinity, all in one treatment. The FAO estimates that 33% of the world’s soils are already degraded, and warns that, if nothing changes, up to 90% of soils could be degraded by 2050, even though about 95% of our food still comes from soil. When land is tired and weather is less predictable, farmers look for solutions that can multitask rather than relying on a single function or input.

Multi-strain inoculants fit well with the broader agenda of “soil health.” A recent FAO-backed report on soil biodiversity notes that soil organisms drive over 90% of all ecosystem services provided by soils, from nutrient cycling to carbon storage and disease suppression. The same report highlights that increased biological activity in soils can help lock away carbon and improve resilience to droughts and floods. This scientific understanding is pushing researchers to move away from one “hero” microbe and instead mimic the diversity that exists in healthy soils, building consortia where several species cooperate rather than compete.

Governments are quietly encouraging this direction through programmes that reward soil-friendly practices. In the European Union, the Common Agricultural Policy now links a significant share of payments to “eco-schemes” and conditionalities that include improved soil management and reduced input use. Member states together spend roughly €48–50 billion per year in CAP support, with at least 25% of direct payments ring-fenced for eco-schemes under the current period. This money does not pay for inoculants directly, but it rewards farmers who build soil organic matter, diversify rotations, or reduce synthetic fertilisers – conditions where complex microbial products can play a practical supporting role.

Drivers

Pressure to grow more food with fewer chemical fertilizers

One major force pushing the agricultural inoculants market forward is the simple but intense pressure to grow more food while using fewer synthetic fertilizers and cutting emissions. Global agencies are very clear about the scale of this challenge. The FAO warns that by 2050 the world population could reach about 9.7 billion people, and agriculture will need to produce 50% more food, feed and fibre than in 2012, even though land and water are under stress. In 2024, around 673 million people were still facing hunger, showing that today’s system is already struggling.

The world is still heavily dependent on mineral fertilizers. FAO data show that world production of inorganic fertilizers reached 208 million tonnes in 2023, an increase of 40% compared with 2002; nitrogen alone made up 120 million tonnes or 58% of that total. This input boom has helped raise yields, but it comes with side-effects. Scientific work published in Scientific Reports finds that synthetic nitrogen fertilizer production accounts for 38.8% of total fertilizer-related emissions, while field emissions add another 58.6%. Agriculture, forestry and other land uses together already generate about 11.9 gigatonnes of CO₂-equivalent per year, roughly 21% of global net anthropogenic greenhouse gas emissions.

Policy signals are becoming more concrete. In India, the government channels support for organic and biological inputs through schemes such as Paramparagat Krishi Vikas Yojana (PKVY) and MOVCDNER. Under current provisions, farmers receive INR 31,500 per hectare over three years under PKVY and INR 46,500 per hectare over three years under MOVCDNER, with a substantial share earmarked specifically for organic and bio-inputs like biofertilizers and inoculants. These are not pilot projects; they operate across multiple states and encourage clusters of small and marginal farmers to move away from purely chemical regimes.

Brazil offers another clear signal. The country created a National Program for Biobased Agricultural Inputs in 2020 under Decree No. 10.375, aiming to respond to “growing demand” for sustainable biobased inputs in crops, livestock and aquaculture. A 2025 technical note further explains how this Bioinputs Program recognises four product groups—biological pesticides, biofertilizers, inoculants and biostimulants—and positions them as tools to improve long-term sustainability of Brazilian agriculture.

Restraints

Low farmer awareness and weak technical support for inoculants

One of the biggest brakes on the growth of agricultural inoculants is not the science, but the gap between lab knowledge and what actually reaches the farmer’s field. Around the world, smallholders play a huge role in food production: the World Bank estimates there are about 510 million farms under two hectares, and together these small farms contribute roughly 35% of global food output.

Field studies on biofertilizers and microbial inputs show this clearly. In one study on biofertilizers in India, 58% of farmers reported that a simple lack of knowledge about biofertilizers was their main constraint, followed by issues like poor guidance from extension staff. Research from Africa paints a similar picture: a review on biofertilizer production notes that the industry remains underdeveloped in many countries because of inadequate research, weak technology development and ineffective regulatory frameworks, meaning that the full benefits of biofertilizers are “yet to be realized” compared with developed regions.

Behavioural research in Europe, where information and infrastructure are relatively stronger, still finds similar hurdles. A survey of nearly 200 arable farmers in the Netherlands and Germany on microbial products found that lack of knowledge and lack of professional support were among the key barriers to adoption, while trust in the technology was a main driver.

Another layer is that many smallholders operate on thin margins and cannot afford to gamble on inputs they are unsure about. A 2023 analysis on fertilizer alternatives for low-income countries notes that biological products can increase yields by 20–30% in a single season, yet actual use among smallholder farmers in Sub-Saharan Africa and South Asia remains low because of limited product awareness, cost, variable availability and the need for proper handling and storage.

Opportunity

Rising organic and regenerative farming that depends on microbial solutions

One of the biggest long-term openings for agricultural inoculants comes from the quiet but steady shift toward organic and regenerative farming. Global organic agriculture is no longer a niche. The latest figures from FiBL and IFOAM show that organic farmland grew by more than 20 million hectares in 2022 alone, reaching about 96 million hectares worldwide, with more than 4.5 million organic producers active that year. Organic food sales were close to €135 billion in 2022, climbed to around €136 billion in 2023, and reached about €145 billion in 2024, showing that consumer demand is still rising even in a period of inflation and uncertainty.

Behind this market story is a deeper soil story. The FAO estimates that roughly 33% of the world’s soils are already degraded, and warns that, if current trends continue, up to 90% of soils could be degraded by 2050. At the same time, about 95% of global food still comes from soil-based agriculture. Another FAO analysis puts global degraded land at around 1.66 billion hectares, with more than 60% of that degradation occurring on agricultural land, including cropland and pasture. Every year, an estimated 100 million hectares of land are further degraded by unsustainable farming, urban growth and more frequent droughts.

Policy commitments are moving in the same direction and create concrete demand for microbial inputs. In Europe, the Farm to Fork Strategy under the Green Deal sets a target to cut nutrient losses from fertilizers by at least 50% by 2030, which is expected to reduce overall fertiliser use by about 20% while maintaining soil fertility. The same framework aims to make 25% of EU farmland organic by 2030 and to halve the use and risk of chemical pesticides.

Brazil offers a clear preview of what this opportunity looks like in practice. In 2020, the Ministry of Agriculture launched the National Bioinputs Program to speed up the adoption of biological products—many of them microbial—in crop and livestock systems. Even before that, the area under biological control of pests and diseases in Brazilian agriculture was estimated at more than 33 million hectares in 2017, and recent scientific work reports that the country’s bioinputs market has been expanding at around 21% per year, about four times the global average for this sector.

Regional Insights

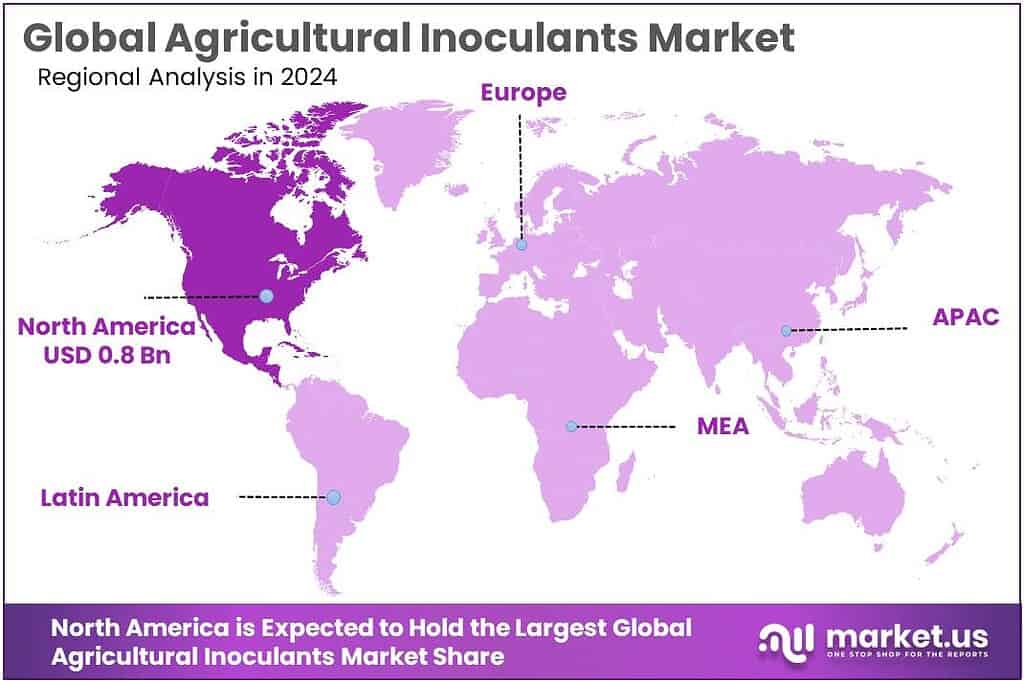

North America leads the inoculants landscape with a 46.10% share worth USD 16.9 billion

In the global agricultural inoculants market, North America stands as the clear demand centre, with the region holding a dominant 46.10% share, valued at around USD 16.9 billion. This leadership is rooted in its large, highly mechanised row-crop base and rapid uptake of biological inputs across the United States, Canada, and Mexico. The region’s push toward more sustainable farming is visible in the organic and low-input segment: by 2023, North America had about 3.3 million hectares of organic agricultural land, while retail sales of organic food in the region reached roughly €63.9 billion, underpinned by the United States as the world’s single largest organic market.

Farmers in major grain and oilseed belts are using inoculants to improve nitrogen use, support soil biology, and manage yield risks as fertiliser prices and regulatory pressure on agrochemicals rise. Together, these structural features—large commercial farms, expanding organic retail markets, and strong policy attention to sustainable practices—help North America not only retain its leading 46.10% share in 2024, but also position the region as a key reference point for new product launches, field validation, and technology partnerships in agricultural inoculants.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer AG, founded in 1863 and headquartered in Leverkusen, Germany, is a diversified life-science company with 3 divisions, including Crop Science, which develops seed treatments and inoculant solutions. In 2024 the group reported €46.6 billion in sales and employed about 94,081 people in 80+ countries, investing €6.2 billion in R&D with 15,900 employees in research roles. These resources support bacterial and fungal inoculants targeting major field crops worldwide.

BASF SE, established in 1865 and headquartered in Ludwigshafen, Germany, is the world’s largest chemical producer, supplying chemical and biological inputs for agriculture. In 2023 it generated €68.9 billion in revenue, held €77.4 billion in assets and €36.6 billion in equity, and employed 111,991 people. BASF operates 6 integrated “Verbund” sites and about 390 other production sites in 80+ countries, providing seed treatments and microbial inoculant technologies within its agricultural solutions portfolio.

DowDuPont split, is a pure agriculture company headquartered in Indianapolis, USA. It reported about US$16.9 billion in annual sales, with roughly 57% from seed and 43% from crop protection, and a market value close to US$46 billion. The company employs 20,000+ people and sells into about 110 countries. Corteva’s Pioneer® brand offers silage and forage inoculants that improve fermentation quality and feed value for dairy and livestock producers.

Top Key Players Outlook

- Bayer AG

- BASF SE

- Corteva

- Isagro S.p.a.

- Lallemand Inc.

- Rizobacter

- Verdesian Life Sciences

- KALO

- Advanced Biological Marketing Inc.

Recent Industry Developments

In 2025, Corteva expects modest growth with net sales projected around $17.3 billion to $17.7 billion, reflecting continued demand for seed technologies, crop protection and biological products.

Lallemand is a privately held company headquartered in Montreal, Canada, with about 4,500 employees worldwide and annual revenue around 1.4 billion CAD, reflecting its size in microbial products that span many industries including agriculture.

Report Scope

Report Features Description Market Value (2024) USD 2.1 Bn Forecast Revenue (2034) USD 6.0 Bn CAGR (2025-2034) 11.0% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Bacterial Inoculants, Fungal Inoculants, Others), By Microorganism (Bacteria, Fungi, Others), By Crop Type (Cereals And Grains, Oilseeds And Pulses, Fruits And Vegetables, Others), By Application (Seed Inoculation, Soil Inoculation) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Bayer AG, BASF SE, Corteva, Isagro S.p.a., Lallemand Inc., Rizobacter, Verdesian Life Sciences, KALO, Advanced Biological Marketing Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Agricultural Inoculants MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Agricultural Inoculants MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Bayer AG

- BASF SE

- Corteva

- Isagro S.p.a.

- Lallemand Inc.

- Rizobacter

- Verdesian Life Sciences

- KALO

- Advanced Biological Marketing Inc.

Our Clients

- 178691

- Feb 2026