Global Aerospace Lubricants Market Size, Share, And Enhanced Productivity By Product (Gas Turbine Oil, Piston Engine Oil, Hydraulic Fluid, Others), By Application (Engine, Hydraulic Systems, Landing Gear, Airframe, Others), By End-Use (Civil, Defense, Space), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179730

- Number of Pages: 386

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

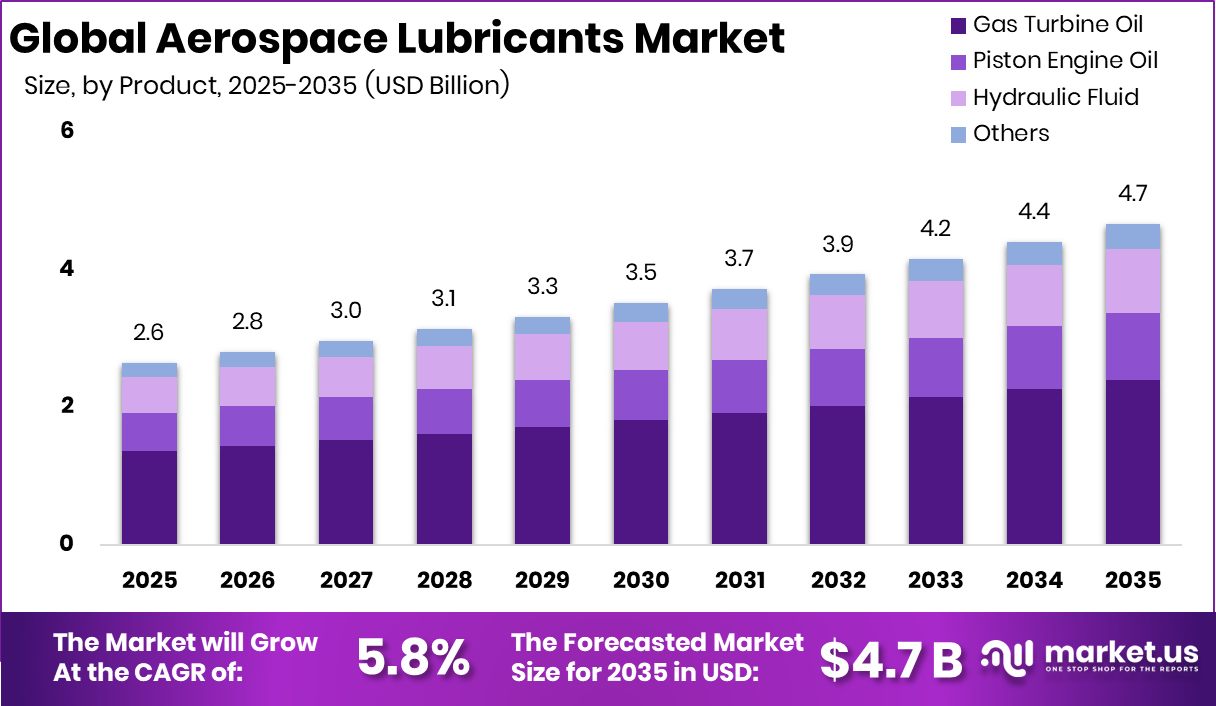

The Global Aerospace Lubricants Market is expected to be worth around USD 4.7 billion by 2035, up from USD 2.6 billion in 2025, and is projected to grow at a CAGR of 5.8% from 2026 to 2035. Aerospace Lubricants Market in North America totaled USD 1.0 Bn, capturing 39.4%.

The global Aerospace Lubricants Market covers essential products such as gas turbine oil, piston engine oil, hydraulic fluid, and other specialized blends used across engines, hydraulic systems, landing gear, airframes, and multiple civil, defense, and space applications. These lubricants reduce friction, protect components under extreme temperature ranges, and ensure safe, efficient aircraft performance. The market spans broad end-use sectors, each requiring precise formulations that support long operational cycles and strict aviation standards.

Aerospace lubricants are high-performance fluids designed to keep aircraft systems stable, clean, and reliable. They safeguard engines, moving parts, and hydraulic mechanisms, ensuring smooth operation during takeoff, flight, and landing. Meanwhile, the Aerospace Lubricants Market represents the commercial ecosystem that produces, distributes, and innovates these fluids to meet evolving aviation requirements, regulatory expectations, and fleet modernization trends.

Market growth is influenced by rising aircraft operations, expansion in civil aviation, and increasing focus on efficient propulsion systems. Developments such as NanoMech securing $12 million in Series B funding, and large-scale energy investments like Texas’ $7.2 billion loan program, highlight broader industrial momentum supporting demand for advanced materials and high-temperature lubrication.

Demand rises as new platforms emerge and infrastructure strengthens. Strategic energy and power financing—including Boom Supersonic’s $300 million funding, the €325 million Greek CCGT plant financing, and the DOE’s $165 million geothermal grant—supports industrial ecosystems that indirectly boost aerospace lubricant needs. Opportunities grow further with global export-oriented initiatives such as SACE’s $6 billion support for manufacturing growth, creating a stronger foundation for innovation in specialized lubricant technologies.

Key Takeaways

- The Global Aerospace Lubricants Market is expected to be worth around USD 4.7 billion by 2035, up from USD 2.6 billion in 2025, and is projected to grow at a CAGR of 5.8% from 2026 to 2035.

- Aerospace Lubricants Market sees strong demand as gas turbine oil dominates with 51.5% share globally.

- Engine applications continue leading the Aerospace Lubricants Market, contributing a significant 51.3% portion of overall usage.

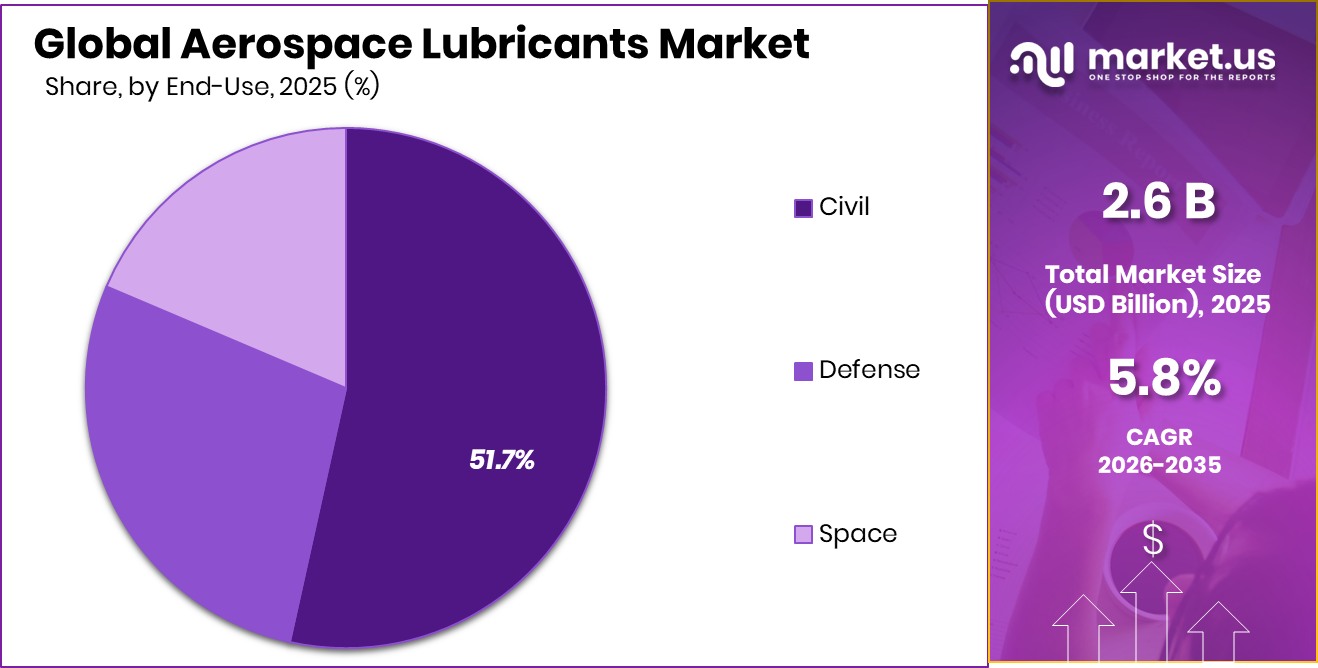

- Civil aviation remains the primary driver in the Aerospace Lubricants Market, holding 51.7% end-use share.

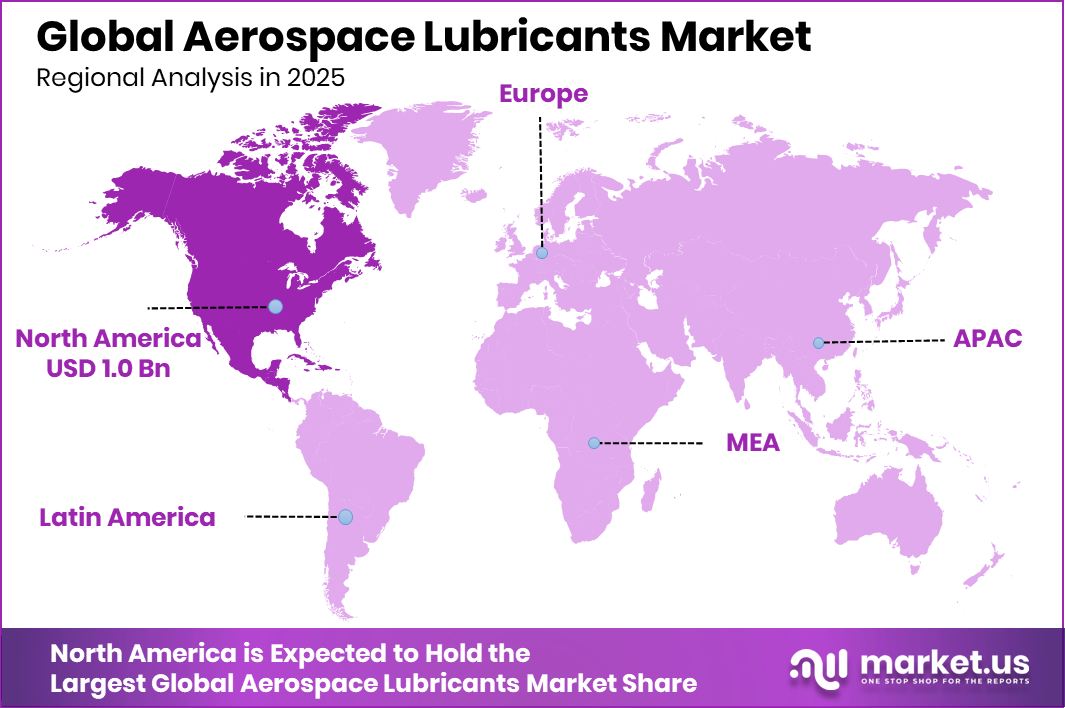

- In North America, the Aerospace Lubricants Market achieved USD 1.0 Bn with a 39.4% share.

By Product Analysis

Aerospace Lubricants Market was dominated by Gas Turbine Oil holding a 51.5% share.

In 2025, the Aerospace Lubricants Market continued to rely heavily on gas turbine oil, which secured a dominant 51.5% share due to its essential role in modern aircraft propulsion systems. Airlines across commercial, defense, and private aviation sectors expanded their fleets, driving steady consumption of high-performance turbine oils that can withstand extreme temperature ranges and long operational hours.

The shift toward more efficient engines and rising global flight activity further supported demand. Manufacturers focused on cleaner formulations that improve engine stability, reduce carbon deposits, and extend maintenance cycles. With fleets becoming more technologically advanced, gas turbine oil remained the backbone of aircraft lubrication, maintaining its leadership position across global aviation networks.

By Application Analysis

Aerospace Lubricants Market engine application dominated overall performance with its strong 51.3% share.

In 2025, the engine segment held a commanding 51.3% share of the Aerospace Lubricants Market, reflecting its critical role in ensuring reliable aircraft performance. Engine lubrication remained a top maintenance priority, as airlines emphasized safety, efficiency, and longer component life amid rising operational pressures. Increased aircraft utilization on domestic and international routes pushed demand for premium lubricants that enhance fuel efficiency and protect against wear.

The rise of next-generation engines with tighter tolerances also strengthened the need for advanced synthetic formulations. As global air travel moved toward recovery and modernization, lubricant suppliers aligned with OEM standards to support cleaner combustion, reduced emissions, and efficient thermal management, keeping the engine segment firmly in the dominant position.

By End-Use Analysis

Aerospace Lubricants Market civil end-use segment dominated the sector demand with a 51.7% share.

In 2025, the civil aviation segment accounted for a leading 51.7% share in the Aerospace Lubricants Market, driven by growing passenger traffic, fleet modernization programs, and expanding airline networks. Commercial operators increasingly prioritize high-quality lubricants that improve operational reliability, reduce downtime, and support longer flight cycles. The push for more fuel-efficient aircraft, coupled with rising deliveries from major OEMs, boosted demand across engine oils, hydraulic fluids, and system lubricants.

Civil carriers adopting sustainable aviation strategies also encouraged the shift toward low-emission, long-life lubrication solutions. With regional and international air travel strengthening in major markets, the civil segment maintained its dominance, supported by continuous technical upgrades and the need for dependable lubrication across diverse fleets.

Key Market Segments

By Product

- Gas Turbine Oil

- Piston Engine Oil

- Hydraulic Fluid

- Others

By Application

- Engine

- Hydraulic Systems

- Landing Gear

- Airframe

- Others

By End-Use

- Civil

- Defense

- Space

Driving Factors

Growing aircraft operations increase lubricant consumption

Growing aircraft operations continue to increase lubricant consumption, supported by higher flight hours, expanding civil fleets, and more frequent engine cycles that demand dependable lubrication. As aviation activity grows, so does the need for thermal-stable turbine oils, hydraulic fluids, and advanced greases capable of handling extreme operating conditions. Broader industrial and automotive developments also influence this environment.

The General Motors $150M Engine Defect Class Action Settlement underscores the importance of reliable lubrication in high-stress systems, reinforcing awareness across industries about performance fluids. Additionally, the Green Finance: $200 million Chinese loan for Morocco’s climate resilience reflects global investment momentum that ultimately strengthens infrastructure, manufacturing capacity, and energy-linked supply chains—factors that indirectly support aerospace lubricant demand worldwide.

Restraining Factors

Stringent aviation standards limit product flexibility

Stringent aviation standards continue to limit product flexibility, requiring every lubricant to meet demanding certification, safety, and performance criteria before adoption. These regulatory expectations slow down formulation changes, extend development cycles, and restrict rapid market entry. Added to this are broader industry pressures affecting aviation operations and fuel systems.

A key development involves the FAA’s ongoing work to include the availability of 100LL avgas at general aviation airports as part of Airport Improvement Program grant assurances. Such policy directions influence fuel and lubricant usage patterns, creating additional compliance layers for manufacturers. As aviation transitions toward cleaner fuels and tighter environmental policies, lubricant producers must invest more resources into testing and validation, creating challenges that restrain faster market expansion.

Growth Opportunity

Rising space missions boost lubricant demand

Rising space missions offer new opportunities for highly specialized lubricants capable of operating in vacuum, radiation exposure, and extreme thermal ranges. As launch systems, satellites, and orbital platforms expand, demand grows for advanced fluids that maintain stability under these conditions. Beyond aerospace, broader industrial and consumer developments also reinforce the need for high-performance lubrication technologies.

The $42M GM Chevy Equinox Oil Guzzling Class Action Settlement highlights increasing scrutiny on lubrication efficiency and long-term reliability. Meanwhile, the UK’s £4.5 billion funding for pro-EV measures signals strong investment in next-generation mobility systems, encouraging cross-industry innovation in synthetic oils and engineered fluids. These external advancements collectively open doors for lubricant innovators to refine aerospace-grade solutions.

Latest Trends

Shift toward cleaner synthetic lubricant formulations

A major trend is the shift toward cleaner synthetic lubricant formulations, driven by environmental goals, longer service intervals, and the need for better thermal management in modern aircraft systems. Aviation stakeholders increasingly prefer low-volatility, oxidation-resistant fluids that support lower emissions and improved operational efficiency. Broader renewable-energy and storage investments also shape the innovation landscape.

The IDAE’s €202.5 million funding for innovative renewables and energy storage reinforces global momentum toward cleaner technologies, encouraging aerospace lubricant manufacturers to align with sustainability-focused chemical strategies. As advanced materials and environmentally balanced additives become more prominent, the market continues moving toward formulations that reduce environmental impact while delivering durable performance across engines, hydraulics, landing gear, and critical onboard systems.

Regional Analysis

North America held 39.4% share in the Aerospace Lubricants Market, reaching USD 1.0 Bn.

In the Aerospace Lubricants Market, North America remained the leading region, holding a dominant 39.4% share and reaching USD 1.0 Bn, supported by strong aircraft operations and steady maintenance demand across commercial and defense fleets. Europe followed with stable consumption driven by mature aviation infrastructure and ongoing fleet modernization programs, particularly in Western European economies.

Asia-Pacific continued to expand rapidly as rising passenger traffic, new airline establishments, and increasing aircraft deliveries strengthened lubricant usage across major markets, including China, India, and Southeast Asia. The Middle East and Africa showed consistent growth, supported by expanding long-haul networks and maintenance activities among regional carriers.

Meanwhile, Latin America experienced gradual improvement with growing commercial aviation movements and improving maintenance operations in key economies. Overall, North America remained the clear dominant region at 39.4%, backed by high operational intensity, advanced aviation infrastructure, and a large in-service fleet that ensures continuous demand for high-performance aerospace lubricants.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, Aerospace Lubricants Inc. continued to strengthen its position as a specialized supplier in the global Aerospace Lubricants Market. The company’s focus on high-performance synthetic oils and greases supported growing demand for advanced aviation maintenance solutions. Its emphasis on reliability, temperature stability, and compatibility with modern aircraft systems enabled it to align closely with evolving OEM and airline requirements. The company benefited from rising aircraft utilization and increased maintenance intervals, positioning its product portfolio as a dependable choice among civil and defense operators seeking consistent operational performance.

Astronics Corporation contributed to the market through its engineering capabilities across aviation systems, indirectly supporting lubricant demand via enhanced aircraft operations and technical performance needs. Its involvement in power systems, lighting, and operational safety technologies helped shape the conditions that require precision lubrication across various aircraft components. As fleets adopt more sophisticated onboard technologies, Astronics’ role in improving system efficiency reinforces the broader ecosystem where high-grade aerospace lubricants remain essential for reliability and long-term component protection.

Crane Aerospace Inc. maintained its influence through its extensive portfolio of critical aircraft systems, including fluid management and landing systems. These components rely on stable lubrication environments to ensure consistent operation under high-stress conditions. The company’s engineering advancements help create performance expectations that drive the adoption of premium lubricants across hydraulic, mechanical, and actuator systems. In 2025, Crane’s strong integration with global aircraft platforms continued to support lubricant demand by reinforcing the importance of precision, durability, and compatibility within the aviation maintenance landscape.

Top Key Players in the Market

- Aerospace Lubricants Inc.

- Astronics Corporation

- Crane Aerospace Inc.

- Eastman Chemical Company

- Exxon Mobil Corporation

- LUBRICANT CONSULT GMBH

- Nye Lubricants Inc.

- NYCO Solution ahead

- Royal Dutch Shell plc

- Shell Global

- TotalEnergies Company

- The Chemours Company

- Zodiac Aerospace

Recent Developments

- In July 2024, AMSOIL INC., a well-known synthetic lubricant company, acquired Aerospace Lubricants Inc. Aerospace Lubricants makes high-performance greases used in aviation, military, industrial, and other applications. After the acquisition, Aerospace Lubricants continues to operate as an independent subsidiary, expanding its access to technical expertise and support from AMSOIL, while still serving its existing customers.

- In March 2024, Astronics Corporation launched the next-generation Typhon T-400 Ku SATCOM system, a new satellite communication product designed to improve aircraft connectivity while lowering cost and installation complexity. The system uses fewer parts and offers flexible installation options, making it easier for airlines and airborne platforms to stay connected. Astronics is a global aerospace technology company that provides power, connectivity, lighting, and test systems for aircraft and defense customers.

Report Scope

Report Features Description Market Value (2025) USD 2.6 Billion Forecast Revenue (2035) USD 4.7 Billion CAGR (2026-2035) 5.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Gas Turbine Oil, Piston Engine Oil, Hydraulic Fluid, Others), By Application (Engine, Hydraulic Systems, Landing Gear, Airframe, Others), By End-Use (Civil, Defense, Space) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Aerospace Lubricants Inc., Astronics Corporation, Crane Aerospace Inc., Eastman Chemical Company, Exxon Mobil Corporation, LUBRICANT CONSULT GMBH, Nye Lubricants Inc., NYCO Solution ahead, Royal Dutch Shell plc, Shell Global, TotalEnergies Company, The Chemours Company, Zodiac Aerospace Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Aerospace Lubricants MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Aerospace Lubricants MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Aerospace Lubricants Inc.

- Astronics Corporation

- Crane Aerospace Inc.

- Eastman Chemical Company

- Exxon Mobil Corporation

- LUBRICANT CONSULT GMBH

- Nye Lubricants Inc.

- NYCO Solution ahead

- Royal Dutch Shell plc

- Shell Global

- TotalEnergies Company

- The Chemours Company

- Zodiac Aerospace

Our Clients

- 179730

- February 2026