Global Eyelash Serum Market Size, Share, Growth Analysis By Ingredient (Conventional, Organic), By Type (Peptides, Prostaglandins, Lash Primer), By Distribution Channel (Online, Hypermarkets and Supermarkets, Specialty Store, Drugstore and Pharmacy, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182145

- Number of Pages: 240

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

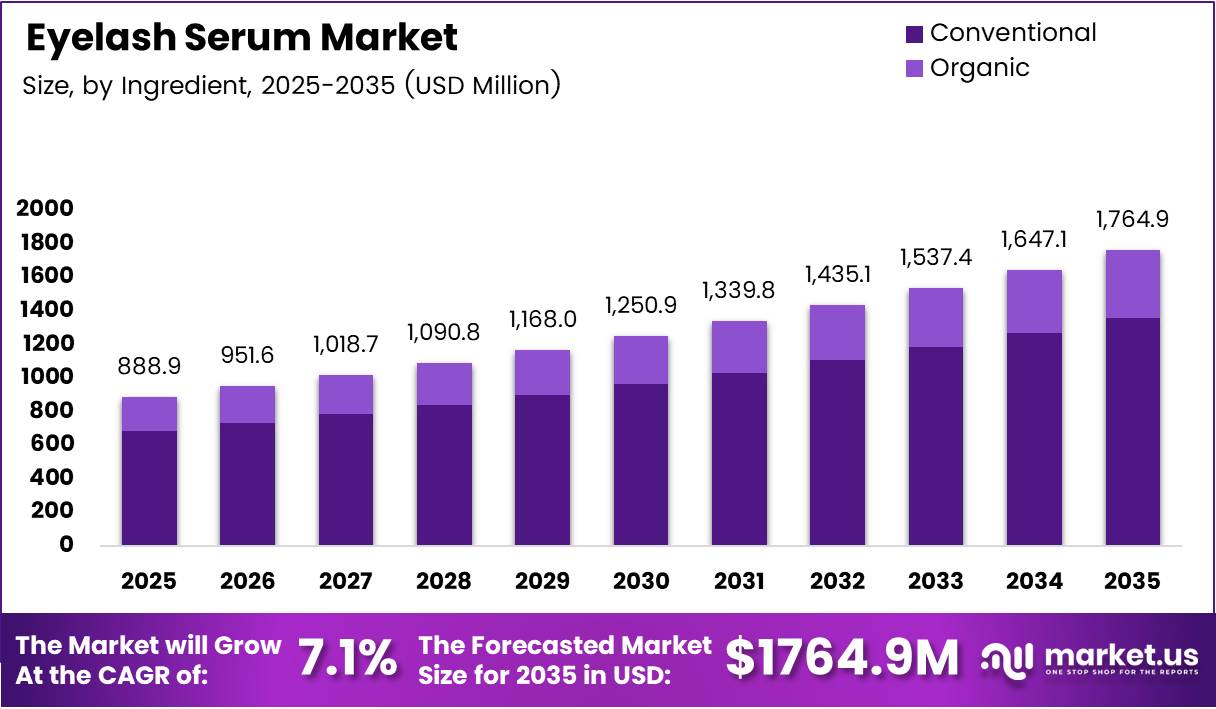

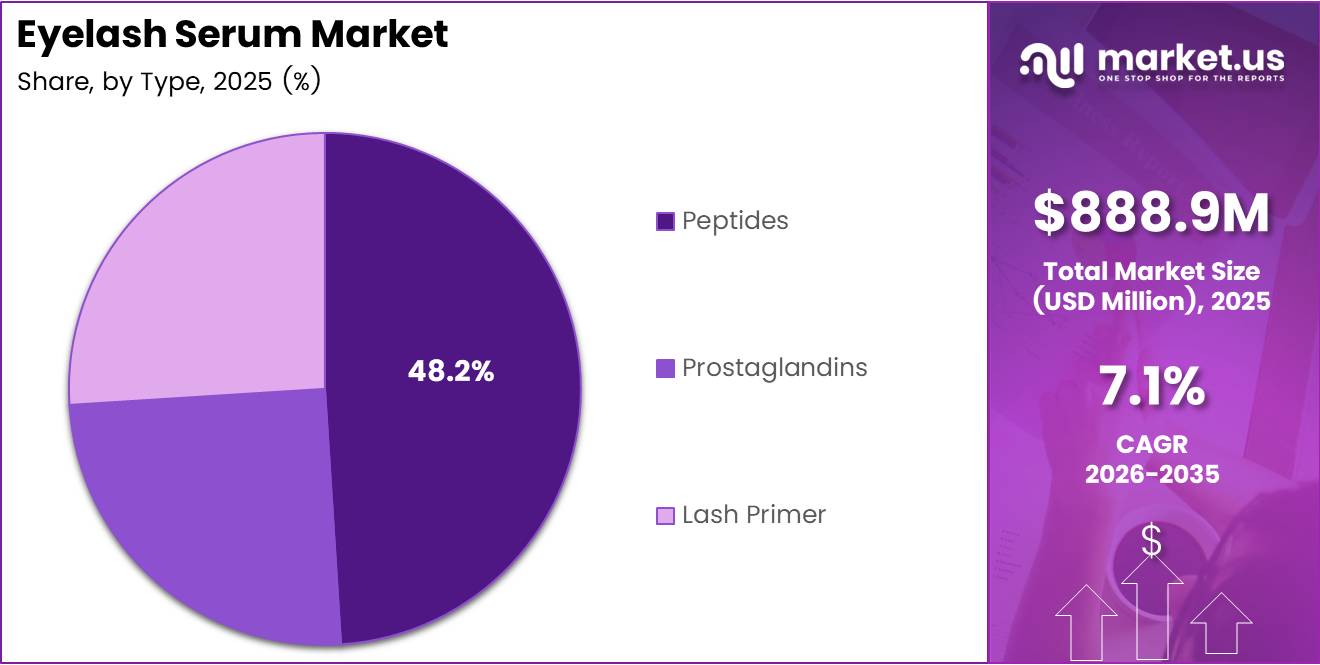

Global Eyelash Serum Market size is expected to be worth around USD 1,764.9 Million by 2035 from USD 888.9 Million in 2025, growing at a CAGR of 7.1% during the forecast period 2026 to 2035.

The eyelash serum market covers topical cosmetic and cosmeceutical products formulated to enhance lash length, density, and health. These lash growth serums sit at the crossroads of personal care and active beauty science, moving beyond decorative cosmetics into treatments consumers use daily at home.

Consumer preference has shifted decisively toward non-invasive lash enhancement over extensions and false lashes. This shift reflects a broader behavioral change — buyers now favor products with measurable results and clean ingredient profiles over temporary aesthetic fixes. That behavior pattern creates durable, repeat-purchase demand across all price tiers.

Social media and influencer culture have compressed the traditional adoption curve for beauty innovations. Lash serum formats that once required dermatologist or salon channels now reach mass consumers within weeks of launch. This distribution speed advantages brands with strong digital-first strategies and direct-to-consumer channels.

Premium and cosmeceutical positioning has elevated average selling prices and margin structures within this category. Brands that combine clinical language, dermatologist validation, and clean formulation claims command a measurable price premium — a dynamic that raises entry barriers for undifferentiated competitors and rewards formulation investment.

Government and regulatory scrutiny of active lash ingredients, particularly prostaglandin analogues, is reshaping formulation strategy across key markets. Brands are redirecting R&D investment toward peptide-based and botanical alternatives that satisfy both consumer safety expectations and evolving compliance requirements in the EU and North America.

According to a 2025 Danish Environmental Protection Agency study, 82% of surveyed eyelash and eyebrow serum products contain peptides as active ingredients. This near-universal adoption signals that peptide technology has become the baseline formulation standard — not a differentiator — pushing brands to compete on peptide concentration, bioavailability, and clinical evidence instead.

According to the same source, 77% of surveyed eyelash and eyebrow serum products contain vitamins, most commonly B5 and B7. This tells us that buyers now expect multi-benefit formulas combining growth stimulation with conditioning and strengthening — a product design requirement that raises R&D cost floors and separates serious cosmeceutical brands from low-investment competitors.

Key Takeaways

- The global eyelash serum market was valued at USD 888.9 Million in 2025 and is forecast to reach USD 1,764.9 Million by 2035.

- The market grows at a CAGR of 7.1% over the forecast period 2026 to 2035.

- By Ingredient, Conventional formulations lead with a 76.3% market share in 2025.

- By Type, Peptides hold the dominant position with a 48.2% share in 2025.

- By Distribution Channel, Online leads with a 48.1% share in 2025.

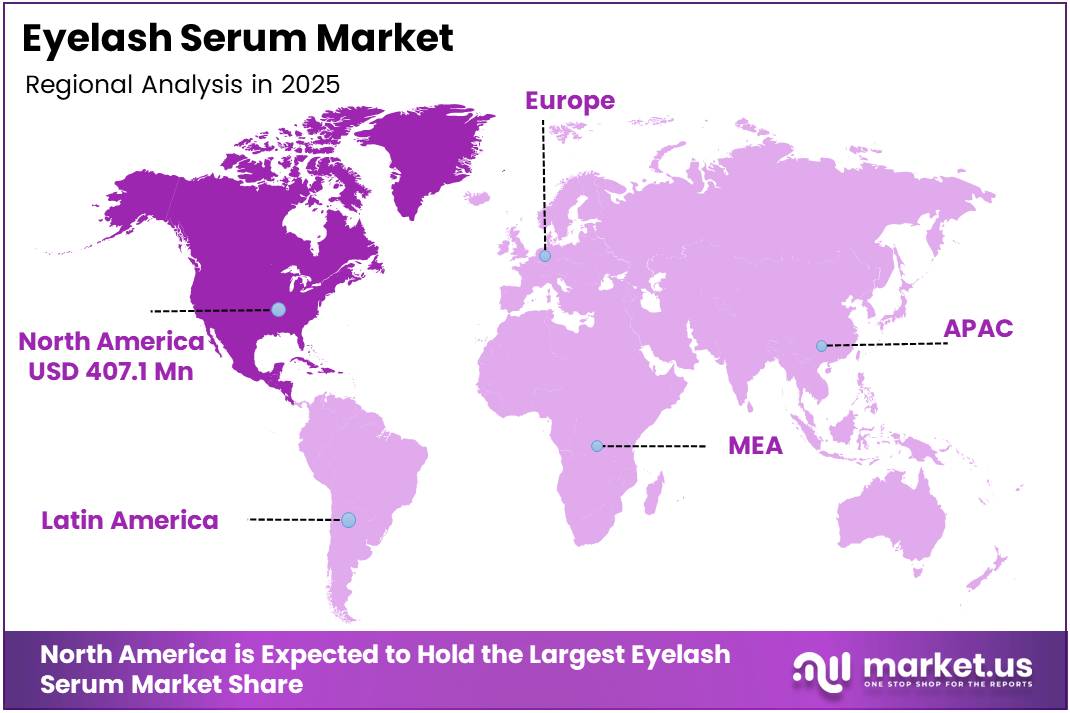

- North America dominates regionally with a 45.80% share, valued at USD 407.1 Million in 2025.

Ingredient Analysis

Conventional dominates with 76.3% due to broader consumer familiarity and retail availability.

In 2025, Conventional held a dominant market position in the By Ingredient segment of the Eyelash Serum Market, with a 76.3% share. Conventional formulations benefit from established supply chains, lower production costs, and existing consumer trust built through years of mass-market retail exposure. Moreover, their compatibility with a wider ingredient palette — including synthetic peptides and proven preservative systems — gives formulators more flexibility to deliver clinically validated results.

Organic formulations serve the fastest-shifting consumer preference segment within this market. Buyers prioritizing clean beauty, allergen avoidance, and sustainability increasingly select organic-certified lash serums despite a higher price point. Consequently, organic SKUs command stronger margins and drive brand differentiation in DTC and specialty retail channels where ingredient transparency is a primary purchase trigger.

Type Analysis

Peptides dominate with 48.2% due to proven efficacy, safety profile, and regulatory acceptance.

In 2025, Peptides held a dominant market position in the By Type segment of the Eyelash Serum Market, with a 48.2% share. Peptide-based serums have displaced prostaglandin-dominant formulations in many markets, primarily because they carry a lower side-effect profile and face fewer regulatory restrictions. According to the Danish Environmental Protection Agency (2025 study), Myristoyl Pentapeptide-17 appears in approximately 45% of surveyed non-prostaglandin serum products, making it the most widely adopted individual peptide — a signal that this ingredient has achieved formulation-standard status across competing brands.

Prostaglandins carry the highest efficacy reputation within the category but face a narrowing regulatory window. According to the same source, 24% of surveyed eyelash and eyebrow serum products contain prostaglandins or prostaglandin analogues. However, mounting EU regulatory pressure on this ingredient class is accelerating brand reformulation timelines. Brands that have already built peptide-led alternatives hold a structural advantage as compliance deadlines tighten.

Lash Primer differentiates through its role as a complementary pre-treatment rather than a standalone growth solution. Primers extend the addressable usage occasion for lash care — positioning the category within broader daily makeup routines and creating attachment-sale opportunities at point of purchase. This hybrid functionality makes lash primers increasingly relevant for mass-market and drugstore distribution formats.

Distribution Channel Analysis

Online dominates with 48.1% due to direct-to-consumer reach and subscription model scalability.

In 2025, Online held a dominant market position in the By Distribution Channel segment of the Eyelash Serum Market, with a 48.1% share. E-commerce channels give lash serum brands direct access to consumer data, enabling personalized repurchase triggers and subscription bundling. Additionally, the online channel removes geographic distribution barriers, allowing DTC brands to build national and international scale without proportional retail infrastructure investment.

Hypermarkets and Supermarkets serve as the primary access point for first-time, price-sensitive buyers entering the lash serum category. Shelf placement within mass-market retail converts browsing beauty consumers into trial purchasers at a scale that digital-only brands cannot replicate. However, margin compression from retail markups limits profitability for brands relying solely on this channel.

Specialty Stores carry the highest-value customer in this channel mix. Beauty specialty retailers attract informed, brand-loyal consumers willing to pay a premium for curated product selection and expert staff guidance. For cosmeceutical and premium lash serum brands, specialty store placement functions as credibility signaling that supports DTC price integrity.

Drugstores and Pharmacies bridge the gap between cosmetic and clinical positioning for lash serums. Placement alongside skincare actives and pharmaceutical-adjacent products reinforces dermatologist-tested and ophthalmologist-approved messaging — a positioning advantage that mass-market grocery channels cannot provide. This channel is especially relevant in markets with established OTC beauty-pharmaceutical crossover purchasing behavior.

Others include salons, spas, and professional beauty outlets that serve a niche but high-engagement customer base. Professional channel sales support premium pricing, build brand reputation through practitioner endorsement, and generate direct referral traffic to online DTC platforms. For newer brands, this channel functions as a trial and advocacy engine rather than a primary volume driver.

Key Market Segments

By Ingredient

- Conventional

- Organic

By Type

- Peptides

- Prostaglandins

- Lash Primer

By Distribution Channel

- Online

- Hypermarkets and Supermarkets

- Specialty Store

- Drugstore and Pharmacy

- Others

Drivers

Social Media Influence and the Non-Invasive Beauty Shift Are Accelerating Lash Serum Adoption

Consumer preference for longer, fuller eyelashes without salon appointments or extensions has created a structurally durable demand base for at-home lash serums. This is not trend-driven volatility — it reflects a fundamental reallocation of beauty spend toward daily-use cosmeceuticals that deliver visible, measurable results without professional intervention.

Social media platforms have compressed the awareness-to-purchase cycle for lash enhancement products to a degree unmatched in most beauty subcategories. Celebrity-endorsed lash serums move from launch to mainstream adoption within weeks rather than years. This speed benefits brands with established influencer networks and penalizes those reliant on traditional retail sell-in timelines.

According to the Danish Environmental Protection Agency (2025), 24% of surveyed lash serum products contain prostaglandins or prostaglandin analogues — ingredients clinically associated with accelerated lash growth. This adoption level reflects the subset of consumers willing to accept higher-efficacy, higher-risk formulations, while the broader market migrates toward peptide alternatives. In April 2024, Neora launched LashLush, a lash and brow serum delivering visible results in four weeks without hormones or irritants — illustrating how efficacy claims are converging with clean-label demands to drive purchase decisions.

Restraints

Safety Concerns and Regulatory Compliance Costs Create Formulation and Market Entry Barriers

Active lash serum ingredients — particularly prostaglandin analogues — carry documented side effect risks including periorbital fat atrophy, iris pigmentation changes, and skin irritation. These safety concerns are not marginal; they generate negative consumer reviews, product withdrawals, and regulatory investigations that elevate the reputational risk for the entire category.

Stringent cosmetic regulations across the EU and North America require extensive safety documentation, clinical testing, and ingredient transparency disclosures before market authorization. For smaller brands, this compliance infrastructure represents a material cost barrier. For larger players, it demands ongoing reformulation investment — particularly as regulators in the EU intensify scrutiny of prostaglandin-class ingredients.

The convergence of consumer safety anxiety and tightening regulatory frameworks creates a two-sided constraint. Brands face consumer demand for high efficacy while regulators restrict the very ingredients that deliver it most reliably. Companies that resolve this tension through clinically validated, compliance-ready peptide formulations will structurally outperform those still dependent on legacy active ingredients.

Growth Factors

Clean-Label Innovation, E-Commerce Expansion, and Multifunctional Formulas Open New Revenue Channels

Consumer demand for organic, vegan, and cruelty-free beauty products is reshaping the lash serum formulation pipeline. Brands that achieve clean-label certification unlock premium price positioning and access specialty retail channels that require these credentials for shelf placement. According to the Danish Environmental Protection Agency (2025), 82% of surveyed non-prostaglandin eyelash serum products contain one or more plant extracts — confirming that botanical ingredient integration has become a baseline formulation expectation, not a premium differentiator.

E-commerce penetration gives DTC lash serum brands a scalable path into emerging markets without proportional physical retail investment. Platforms in Southeast Asia, Latin America, and the Middle East are delivering beauty consumers to digital storefronts faster than traditional retail infrastructure can be established. In August 2025, UKLASH launched groa — a peptide-powered, prostaglandin-free lash serum sub-brand priced at $20 and targeting Gen Z and Gen Alpha specifically through digital channels, demonstrating how price-tiered DTC launches can penetrate new consumer cohorts at scale.

Multifunctional serums combining lash growth, conditioning, and strengthening in a single formula address the consumer preference for streamlined beauty routines. This format commands a higher average selling price by replacing multiple single-function products, while also reducing consumer decision fatigue at the point of purchase. Brands that successfully position multifunctional lash serums as daily skincare essentials — not just cosmetic treatments — capture a more loyal, higher-frequency buyer.

Emerging Trends

Peptide Science Advances and Ethical Beauty Standards Are Redefining the Lash Serum Category

Peptide-based and biotin-enriched formulations are replacing prostaglandin-dominant products as the preferred technical platform for lash enhancement. This shift reflects both regulatory pressure and consumer demand for safer, evidence-backed alternatives. According to the Danish Environmental Protection Agency (2025), hyaluronic acid appears in just over 50% of surveyed non-prostaglandin lash serum products — indicating that hydration and barrier support have become expected co-benefits embedded alongside growth-stimulating actives.

Dermatologist-tested and ophthalmologist-approved claims are transitioning from marketing language into purchase prerequisites for a growing segment of informed beauty buyers. Brands that invest in third-party clinical validation and publish verifiable efficacy data are building trust equity that generic beauty brands cannot replicate quickly. In May 2025, Re/do Beauty launched India’s first clinically effective peptide-based lash growth serum using Resulook and the WKPep Pro-Lash Peptide Complex — signaling that clinical formulation standards are now reaching emerging markets.

Consumer preference for cruelty-free and sustainable packaging is compressing the product development cycle for brands that have not yet completed ethical certification processes. Buyers in premium channels increasingly use cruelty-free status as a purchase filter rather than a bonus attribute. Additionally, the integration of advanced cosmetic science with active botanical ingredients signals convergence between the cosmeceutical and natural beauty segments — a merging that will reward brands capable of credibly occupying both positions simultaneously.

Regional Analysis

North America Dominates the Eyelash Serum Market with a Market Share of 45.80%, Valued at USD 407.1 Million

North America holds a 45.80% share of the global eyelash serum market, valued at USD 407.1 Million in 2025. This leadership reflects the region’s mature DTC beauty infrastructure, high per-capita beauty spend, and early consumer adoption of cosmeceutical lash products. Additionally, North America’s regulatory environment has shaped a market that rewards clinically validated formulations — creating a quality floor that sustains premium pricing.

Europe Eyelash Serum Market Trends

Europe represents the most regulatory-complex region in this category. EU scrutiny of prostaglandin analogues has accelerated reformulation activity among European-market brands, effectively pushing the region toward peptide and botanical formulations ahead of global peers. This regulatory leadership position means European market trends frequently set formulation standards that other regions adopt within two to three product cycles.

Asia Pacific Eyelash Serum Market Trends

Asia Pacific combines the world’s largest beauty consumer base with rapidly expanding e-commerce infrastructure, making it the highest-potential expansion region for lash serum brands. South Korea and Japan anchor the premium segment with sophisticated cosmeceutical buyers, while China, India, and Southeast Asia represent volume-growth markets where digital-first distribution strategies are proving more effective than traditional retail rollouts.

Middle East and Africa Eyelash Serum Market Trends

The Middle East presents a structurally favorable environment for premium lash serums, driven by high beauty spend among urban female consumers and strong preference for eye-focused cosmetic products — a category elevated by regional dress and makeup traditions. GCC countries in particular sustain premium price points that support margin-positive entry for international lash serum brands.

Latin America Eyelash Serum Market Trends

Latin America’s lash serum market is developing through two parallel channels: mass-market penetration via e-commerce platforms and premium expansion through specialty beauty retail in Brazil and Mexico. Brazil’s established beauty industry provides a launch-pad infrastructure for international brands, while Mexico’s proximity to North American supply chains reduces distribution cost complexity for mid-tier entrants.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

E.l.f. Cosmetics Inc. positions itself as the value-access leader in the lash serum category, combining mass-market price points with clean beauty credentials. This dual positioning — affordable and consciously formulated — captures the largest buyer segment: consumers who want efficacy-forward lash products without a premium price barrier. Their distribution breadth across mass retail and digital channels amplifies reach in ways specialty-only brands cannot match.

Grande Cosmetics LLC built its market position on clinical efficacy claims and measurable visible results, making it a benchmark brand in the cosmeceutical lash serum segment. Its strategy of leading with before-and-after evidence and dermatologist endorsements has established a trust foundation that sustains premium pricing and drives repeat purchase loyalty — the two most valuable metrics in this high-repurchase category.

JB Cosmetics Group leverages professional beauty channel expertise to build brand credibility that transfers into consumer retail. By establishing validation through salon and professional practitioner networks first, the company creates a practitioner-endorsed positioning that is difficult for purely DTC competitors to replicate quickly. This channel strategy supports premium retail pricing by anchoring product efficacy in professional use cases.

L’Oréal S.A. applies global R&D investment and multi-brand portfolio management to the lash serum category at a scale unavailable to independent brands. Its ability to develop proprietary ingredient technologies, conduct large-scale clinical trials, and distribute across every global channel simultaneously gives it structural advantages in both formulation leadership and market reach. L’Oréal’s positioning across mass and luxury tiers allows it to capture share across the full consumer income spectrum.

Key Players

- E.l.f. Cosmetics Inc.

- Grande Cosmetics LLC

- JB Cosmetics Group

- L’Oréal S.A.

- LVMH Group

- Pacifica Beauty

- Uklash

- Neora

- Shiseido Company, Limited

- Skin Research Laboratories

Recent Developments

- May 2024 — NEXGEL acquired the international beauty brand Silly George, which specializes in eye and eyelash products including lash serums and accessories. This acquisition extended NEXGEL’s lash care portfolio and gave it an established international consumer base in the eye beauty segment.

- September 2025 — Amaani raised $3 Million in seed funding for its AÏZA Arab beauty brand, which includes the Date Setter brow and lash serum formulated with date seed and castor oil. This funding round signals investor confidence in culturally positioned, ingredient-authentic beauty brands targeting underserved regional consumer identities.

- November 2025 — BeautyLab launched its advanced Lash and Brow Power Serum featuring an innovative peptide complex, lipo-oligopeptide, and botanical hair-growth complex for visibly enhanced thickness, length, and density. This launch demonstrates continued market momentum toward multi-ingredient, clinically positioned lash formulations combining synthetic and botanical actives.

Report Scope

Report Features Description Market Value (2025) USD 888.9 Million Forecast Revenue (2035) USD 1,764.9 Million CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Ingredient (Conventional, Organic), By Type (Peptides, Prostaglandins, Lash Primer), By Distribution Channel (Online, Hypermarkets and Supermarkets, Specialty Store, Drugstore and Pharmacy, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape E.l.f. Cosmetics Inc., Grande Cosmetics LLC, JB Cosmetics Group, L’Oréal S.A., LVMH Group, Pacifica Beauty, Uklash, Neora, Shiseido Company Limited, Skin Research Laboratories Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- E.l.f. Cosmetics Inc.

- Grande Cosmetics LLC

- JB Cosmetics Group

- L'Oréal S.A.

- LVMH Group

- Pacifica Beauty

- Uklash

- Neora

- Shiseido Company, Limited

- Skin Research Laboratories

Our Clients

- 182145

- Mar 2026