Global Elastic Adhesives Market By Resin Type (Polyurethane, Silicone, SMP, and Others), By Application (Building And Construction, Industrial, Automotive And Transportation, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 179607

- Number of Pages: 289

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

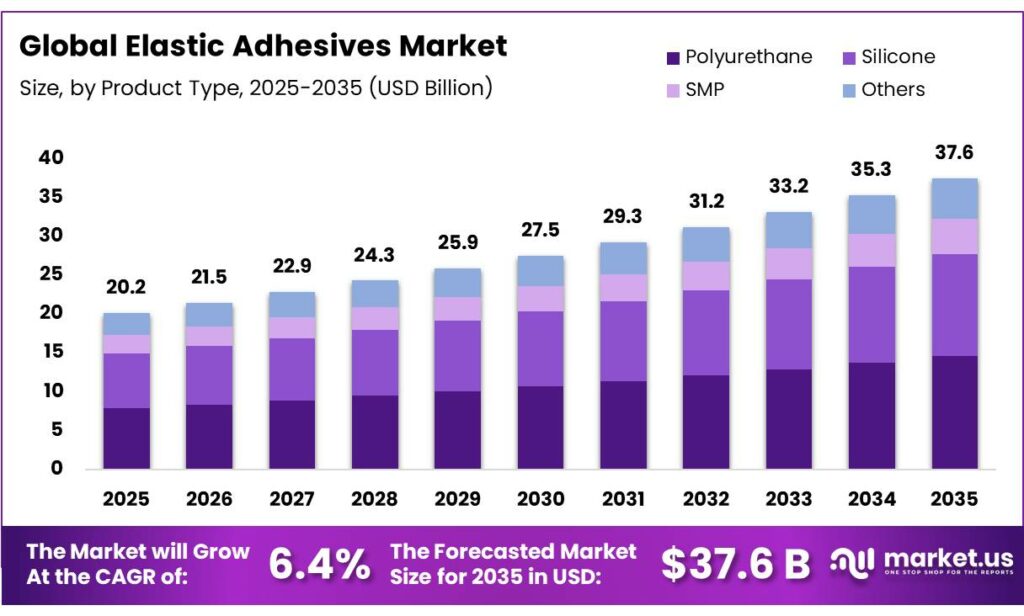

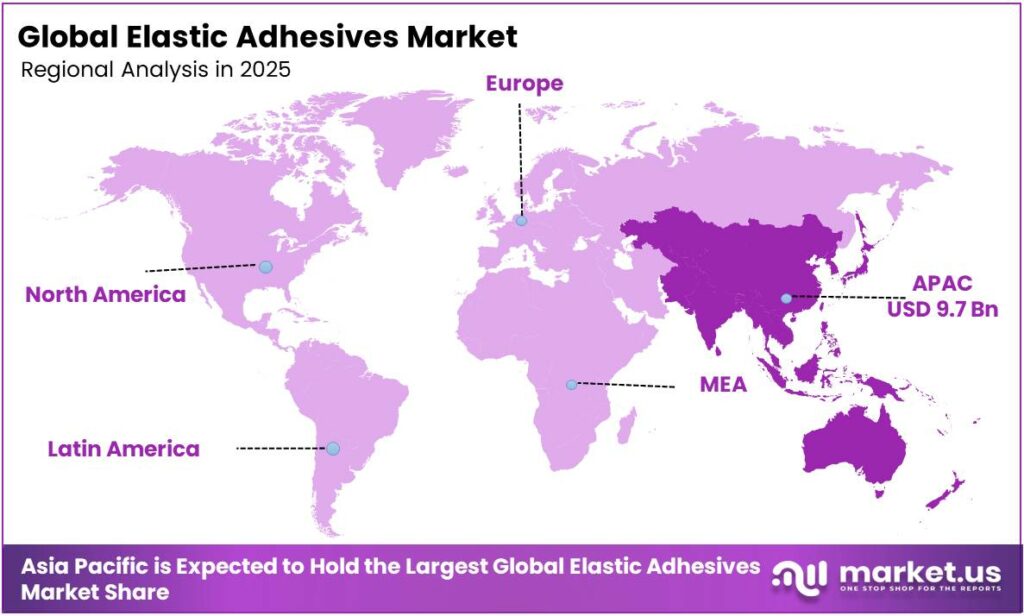

The Global Elastic Adhesives Market is expected to be worth around USD 37.6 Billion by 2035, up from USD 20.2 Billion in 2025, at a CAGR of 6.4% from 2026 to 2035. The Asia Pacific segment maintained 46.1%, supporting a Elastic Adhesives value of USD 2.5 Bn.

Elastic adhesives are specialized bonding agents formulated with elastic polymers that allow a bond to stretch, bend, and recover its shape without losing strength. Unlike rigid glues that may crack under stress, these adhesives act as shock absorbers, distributing mechanical stress and accommodating movement or thermal expansion between surfaces.

The elastic adhesives market is driven by its versatile applications across sectors such as construction, automotive, and infrastructure. In the construction industry, elastic adhesives are crucial for sealing, bonding, and weatherproofing, offering durability, flexibility, and resistance to environmental factors. Increasing demand for sustainable, eco-friendly solutions has led to the adoption of low-VOC and water-based formulations, aligning with stringent regulations such as REACH and LEED certification.

- According to the US Green Building Council, in 2024, New York alone added over 69 million square feet of LEED-certified space and 170 certified projects, or 3.44 square feet of LEED-certified building space per capita.

In the automotive sector, elastic adhesives are sought for their ability to bond lightweight materials, contributing to fuel efficiency and meeting stringent regulatory standards. Additionally, the shift toward electric vehicles has increased demand for high-performance adhesives in battery and structural component bonding.

- According to the International Energy Agency (IEA), the demand for EV batteries grew to over 950 GWh in 2024, 25% more than in 2023.

Key Takeaways:

- The global elastic adhesives market was valued at USD 20.2 billion in 2025.

- The global elastic adhesives market is projected to grow at a CAGR of 6.4% and is estimated to reach USD 37.6 billion by 2035.

- Based on the resin type, polyurethane elastic adhesives dominated the market, with a market share of around 38.9%.

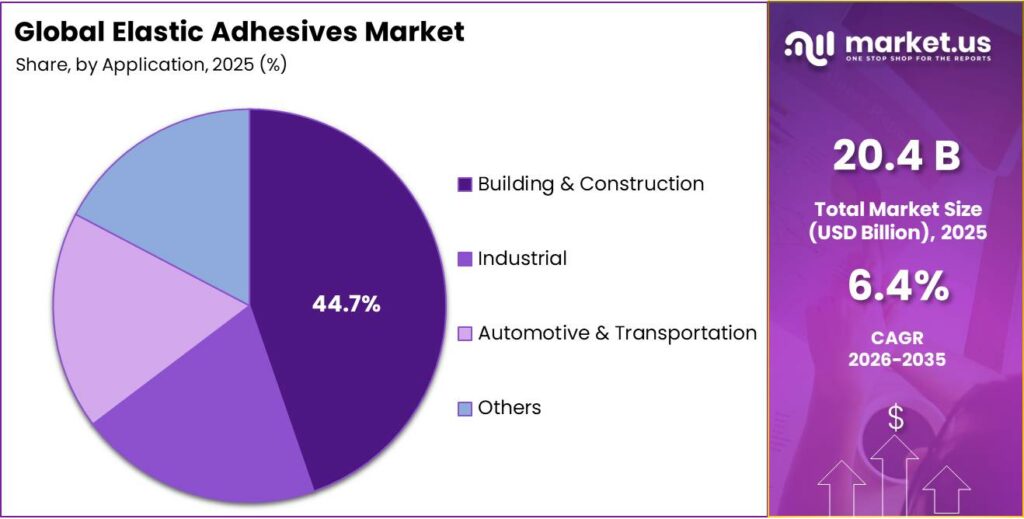

- Among the applications of elastic adhesives, the building & construction industry held a major share in the market, 44.7% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the elastic adhesives market, accounting for around 47.8% of the total global consumption.

Resin Type Analysis

Polyurethane Elastic Adhesives Held the Largest Share in the Market.

The elastic adhesives market is segmented based on product type into polyurethane, silicone, SMP (silane-modified polymers), and others. The polyurethane elastic adhesives dominated the market, comprising around 38.9% of the market share, due to their versatile combination of properties that meet a wide range of industrial requirements. They offer excellent adhesion to a variety of substrates, including metals, plastics, and wood, making them suitable for diverse applications.

Additionally, polyurethane adhesives provide superior mechanical strength and abrasion resistance, which is crucial for applications subject to heavy stress or wear. Their flexibility, combined with good weathering resistance and the ability to bond effectively in both dry and damp conditions, further enhances their appeal.

Moreover, they can be easily formulated to meet specific needs, offering an adaptable solution across multiple industries. Silicone and SMP adhesives, while specialized, often have limitations in adhesion, curing time, or performance under extreme conditions, making polyurethane a more broadly applicable choice.

Application Analysis

The Elastic Adhesives Are Mostly Utilized in Building & Construction Industry.

Based on the applications of elastic adhesives, the market is divided into building & construction, industrial, automotive & transportation, and others. The building & construction sector dominated the market, with a market share of 44.7%, due to the specific performance requirements and environmental conditions that align with their capabilities.

They are essential for sealing, bonding, and weatherproofing applications, where flexibility, durability, and resistance to moisture and temperature fluctuations are critical. The long curing times and easy application of elastic adhesives are suited for large-scale construction projects, including facades, roofing, and flooring.

Additionally, construction materials often require adhesives that can bond dissimilar substrates, such as glass, metal, and composites, which elastic adhesives excel at. While industrial and automotive sectors utilize elastic adhesives, the building sector’s larger and more diverse application scope makes it the dominant area for their use.

Key Market Segments:

By Resin Type

- Polyurethane

- Silicone

- SMP

- Others

By Application

- Building & Construction

- Industrial

- Automotive & Transportation

- Others

Drivers

Increased Applications in Infrastructure and Construction Drive the Elastic Adhesives Market.

The increased applications of elastic adhesives in infrastructure and construction have been driven by their superior bonding properties, flexibility, and durability. Elastic adhesives are increasingly used in applications such as facades, roofs, flooring, and structural joints, where resistance to environmental stresses such as temperature fluctuations and moisture is crucial.

For instance, the European Commission’s report noted that over 40% of the energy consumed in the EU is used in buildings, highlighting a growing demand for eco-efficient and high-performance materials, supporting the uptake of advanced adhesive solutions. The elastic adhesives are used in curtain wall facades, which require high adhesion strength and weather resistance.

Furthermore, regulatory initiatives such as the U.S. Green Building Council’s LEED certification incentivize the adoption of sustainable construction materials, driving further demand for high-performance adhesives. This regulatory landscape has fostered a steady expansion of the elastic adhesives market.

Restraints

Balancing of Technical Performance and Regulatory Compliance Might Hamper the Demand for Elastic Adhesives.

The balancing of technical performance and regulatory compliance constitutes a critical structural challenge for the elastic adhesives market, as manufacturers must reconcile escalating engineering requirements with tightening chemical restrictions. Manufacturers must meet stringent environmental regulations while ensuring the adhesives perform under demanding conditions.

For instance, the regulatory bodies such as the U.S. EPA and the European Union have established stringent thresholds, typically capping adhesive VOC content at 200 g/L, with some specific sealant applications restricted to 40-500 g/L. Similarly, the EU’s REACH regulation mandates the registration of substances exceeding one metric ton per year, forcing the phase-out of hazardous components such as PFOA and certain microplastics, influencing raw material selection.

This regulatory complexity can limit the range of acceptable materials, forcing manufacturers to innovate within tighter confines. In some cases, modifications to improve environmental compliance have led to trade-offs in adhesive performance, especially under extreme weather conditions.

Opportunity

Elastic Adhesives Demand in the Automotive and Transportation Industry Creates Opportunities in the Market.

The demand for elastic adhesives in automotive and transportation presents a significant opportunity driven by the need for lightweight, durable, and energy-efficient materials.

According to the U.S. Department of Energy, a 10% reduction in vehicle weight can improve fuel efficiency and lower carbon emissions by 6%-8%. This encourages the substitution of traditional mechanical fasteners with elastic adhesives, which distribute stress across entire bond lines and enable the joining of dissimilar materials such as aluminum, carbon fiber composites, and plastics. For instance, the adoption of electric vehicles (EVs) has spurred the demand for adhesives that can securely bond battery components and offer high-performance sealing.

According to IEA, the sales of electric cars surpassed 17 million globally in 2024, reaching a sales share of more than 20% of the total vehicles. Furthermore, government initiatives, such as the U.S. Bipartisan Infrastructure Law, have allocated over US$7 billion for EV battery components and materials, indirectly supporting adhesive demand in the supply chain in the US. Moreover, the need for noise and vibration damping in transportation systems, including rail and aerospace, further drives the adoption of elastic adhesives.

Trends

Rapid Shift Towards Eco-Friendly Elastic Adhesives.

The rapid shift towards eco-friendly elastic adhesives is characterized by the replacement of petroleum-derived components with bio-based alternatives and the reduction of Volatile Organic Compounds (VOCs). This trend is anchored by regulatory frameworks such as the EU Green Deal, which aims for climate neutrality by 2050, and EPA mandates that restrict VOC levels to enhance indoor air quality.

Similarly, the European Union’s REACH regulation, which mandates the reduction of hazardous substances, has pushed adhesive manufacturers to adopt water-based and solvent-free formulations. Furthermore, the green building standards set by the U.S. Green Building Council (USGBC) incentivize the use of environmentally friendly adhesives in LEED-certified buildings, supporting the adoption of low-VOC and non-toxic formulations.

The adoption of bio-based adhesives, such as those derived from plant-based materials, has been further accelerated by these regulatory frameworks, aligning with broader sustainability goals. According to a study published by NIH, bio-based polyurethane adhesives derived from vegetable oils can achieve a 22% lower life cycle impact compared to petrochemical counterparts.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the Elastic Adhesives Market Due to Disrupted Supply Chains.

The geopolitical tensions are significantly impacting the elastic adhesives market, particularly in terms of supply chain disruptions and raw material shortages. The ongoing trade restrictions and sanctions, especially between major economies such as the U.S. and China, have led to delays in the availability of key raw materials such as petrochemical derivatives used in adhesive production.

Furthermore, regional conflicts, such as those involving Eastern Europe, have caused fluctuations in energy prices. This volatility has increased the cost of production for manufacturers of elastic adhesives, especially those dependent on energy-intensive processes.

Moreover, the geopolitical instability has led to shifts in manufacturing bases. For instance, the European Union noted a trend towards reshoring and diversification of supply chains, as companies seek to mitigate risks from politically unstable regions. Such shifts may impact the cost structure and availability of adhesives in global markets, further complicating industry planning and procurement strategies.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Elastic Adhesives Market.

In 2025, the Asia Pacific dominated the global elastic adhesives market, holding about 47.8% of the total global consumption, driven by robust industrial growth, particularly in automotive, construction, and electronics sectors. The rapid infrastructure development in emerging economies of the region, which accelerates demand for construction materials, including high-performance adhesives. For instance, China’s major investments in sustainable infrastructure have increased the use of adhesives in green building projects.

- A report by the International Energy Agency (IEA) noted that EV battery demand grew by over 30% in China in 2024.

In the automotive sector, the increasing vehicle production and the shift toward electric vehicles (EVs) in the region drive the demand for lightweight bonding solutions, where elastic adhesives play a critical role. The India Brand Equity Foundation (IBEF) further highlighted the expansion of India’s automotive sector, with EV sales rising 20%, contributing to higher adhesive consumption.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis:

Manufacturers of elastic adhesives focus on product innovation, where companies invest in developing high-performance adhesives with improved properties such as enhanced flexibility, durability, and environmental resistance.

Additionally, manufacturers emphasize regional expansion by setting up production facilities closer to growing demand centers, particularly in the Asia Pacific and emerging economies. Furthermore, supply chain optimization is crucial, with companies focusing on securing reliable raw material sources to mitigate disruptions. Similarly, collaboration with end-users in industries such as automotive, construction, and electronics allows for tailored solutions that meet specific application needs. These activities collectively enable manufacturers to maintain and expand their market share.

The Major Players in The Industry

- BASF SE

- Henkel AG & Co. KGaA

- B. Fuller Company

- 3M

- Dow

- DuPont, Inc.

- Arkema

- The Sherwin-Williams Company

- Huntsman International LLC

- PPG Industries

- Sika AG

- Wacker Chemie AG

- Other Key Players

Key Development:

- In May 2025, BASF introduced its adhesive solutions designed specifically for next-generation batteries, incorporating the innovative Debonding on Demand concept, which supports the repair, reuse, and recycling of batteries.

- In December 2025, Henkel unveiled Loctite MS 9650, a next-generation adhesive and sealant designed to surpass the stringent demands of automotive customers for flexibility and sustainability. Formulated with a silane-modified polymer, it cures through moisture reaction, resulting in a soft, elastic product that is sufficiently robust for elastic bonding applications.

Report Scope:

Report Features Description Market Value (2025) US$20.2 Bn Forecast Revenue (2035) US$37.6 Bn CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Resin Type (Polyurethane, Silicone, SMP, and Others), By Application (Building & Construction, Industrial, Automotive & Transportation, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape BASF SE, Henkel AG & Co. KGaA, H.B. Fuller Company, 3M, Dow, DuPont, Inc., Arkema, The Sherwin-Williams Company, Huntsman International LLC, PPG Industries, Sika AG, Wacker Chemie AG, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- BASF SE

- Henkel AG & Co. KGaA

- B. Fuller Company

- 3M

- Dow

- DuPont, Inc.

- Arkema

- The Sherwin-Williams Company

- Huntsman International LLC

- PPG Industries

- Sika AG

- Wacker Chemie AG

- Other Key Players

Our Clients

- 179607

- Feb 2026