Global Dicamba Market By Form (Liquid, Dry), By Time of Application (Post-Emergence, Pre-Emergence), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Pastures And Forage Crops, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 177627

- Number of Pages: 315

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

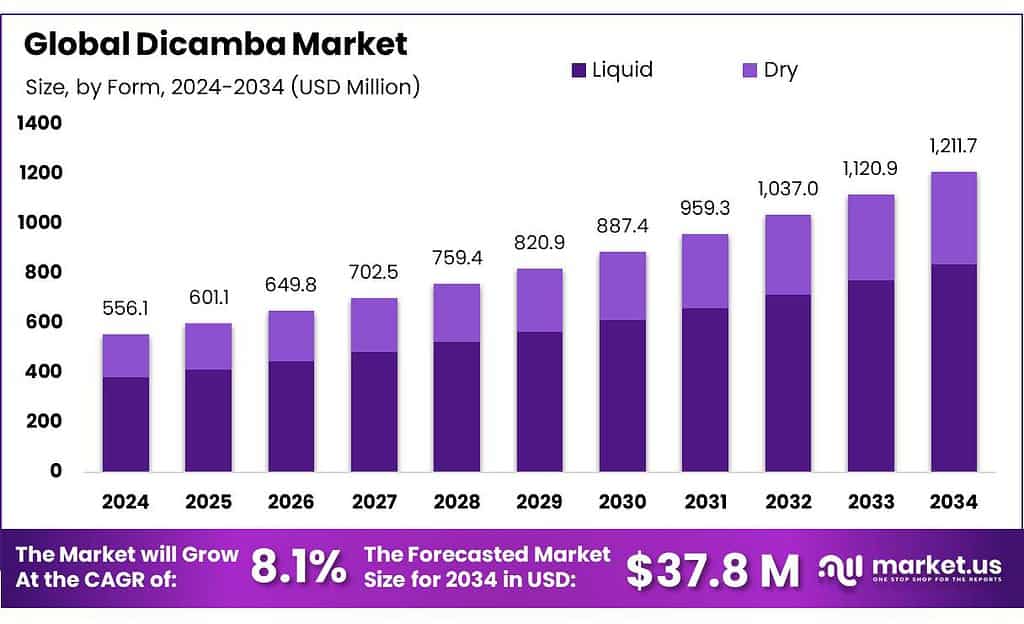

The Global Dicamba Market is expected to be worth around USD 1211.7 Million by 2034, up from USD 556.1 Million in 2024, and is projected to grow at a CAGR of 8.1% from 2025 to 2034. The North America segment maintained 52.7%, supporting a Psychedelic Mushrooms value of USD 293.0 Mn.

Dicamba is a selective, auxin-type herbicide mainly used to control broadleaf weeds. In modern row-crop farming, it is closely tied to herbicide-tolerant production systems—especially soybeans and cotton—because it helps growers manage tough weeds that reduce yield and slow harvest operations. The industrial relevance is also “food-system adjacent”: soybeans are a major source of edible oil and animal feed, so weed control decisions in soybean belts directly influence downstream supply chains and price stability.

In the United States, soybean planted area was 87.1 million acres in 2024, and soybean production totaled 4.37 billion bushels. In 2025, USDA estimated 83.4 million acres of soybeans planted, and reported that 96% of soybean acreage used herbicide-resistant seed varieties—an important indicator of how strongly the crop system depends on chemical weed control platforms. At the farm-practice level, USDA’s chemical-use highlights show herbicides applied on 96% of soybean planted acres, underlining how central herbicide programs remain in commercial soybean production.

Key driving factors include weed resistance pressure, operational efficiency, and the economics of protecting yield across very large acreages. As the soybean complex scales, the “pull” on weed-control tools grows with it: USDA’s global supply data indicates world soybean production rising from 396.35 million metric tons (2023/24) to 427.15 million metric tons (2024/25).

Regulation is not a side issue—it is a core market variable. EPA documents that a court ruling on February 6, 2024 vacated certain over-the-top dicamba registrations, followed by an EPA Existing Stocks Order issued February 14, 2024 to manage limited sale/distribution and time-bound use for the 2024 season.

Key Takeaways

- Dicamba Market is expected to be worth around USD 1211.7 Million by 2034, up from USD 556.1 Million in 2024, and is projected to grow at a CAGR of 8.1%.

- Liquid held a dominant market position, capturing more than a 69.3% share.

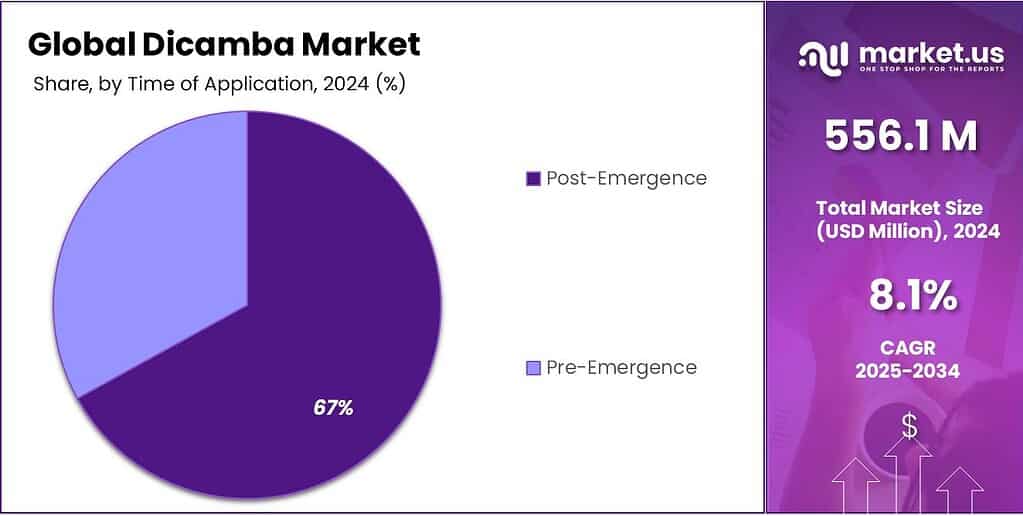

- Post-Emergence held a dominant market position, capturing more than a 67.2% share.

- Cereals and Grains held a dominant market position, capturing more than a 45.8% share.

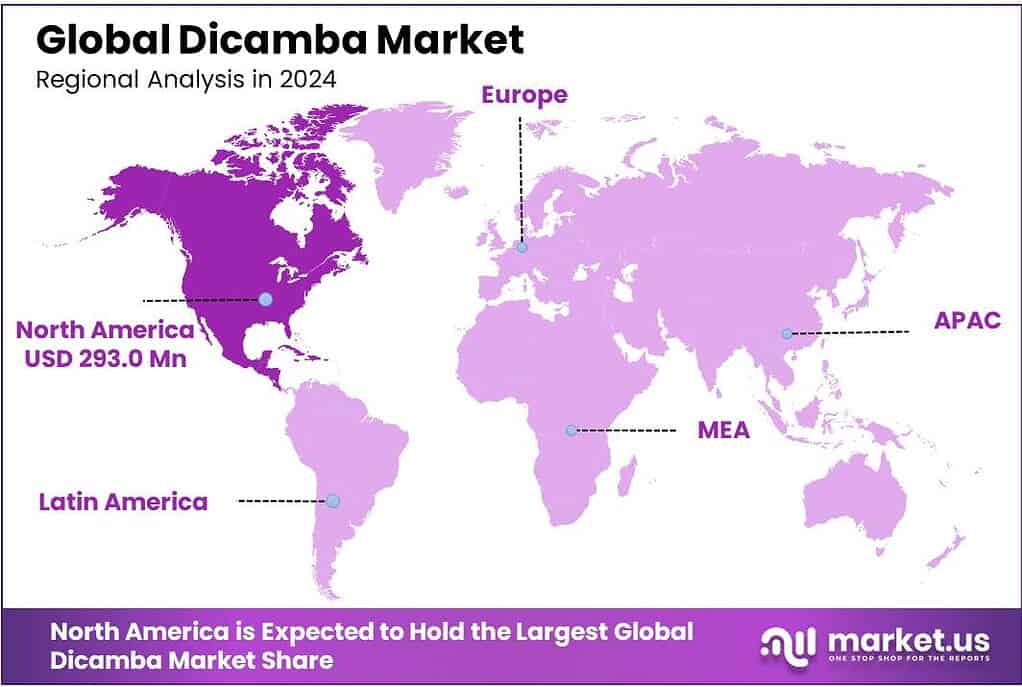

- North America is the dominating region in the dicamba market, holding 52.7% share and reaching USD 293.0 Mn.

By Form Analysis

Liquid Dicamba leads strongly with 69.3% share in 2024, driven by field-level practicality and ease of large-scale spraying

In 2024, Liquid held a dominant market position, capturing more than a 69.3% share. This strong position reflects how farmers prefer liquid formulations for large-acre crop protection programs, especially in soybean and cotton fields where spray uniformity and compatibility with modern equipment matter a lot. Liquid dicamba blends smoothly with water and other tank-mix partners, making it easier for applicators to manage spraying schedules during narrow weather windows. Growers increasingly rely on precision sprayers and calibrated boom systems, and liquid formulations fit naturally into this setup without extra handling steps.

By Time of Application Analysis

Post-Emergence application leads firmly with 67.2% share in 2024, supported by flexible in-season weed control

In 2024, Post-Emergence held a dominant market position, capturing more than a 67.2% share. This leadership reflects how farmers prefer to respond to weed pressure after crops and weeds have already emerged, rather than relying only on early preventive treatments. Post-emergence dicamba applications allow growers to visually assess weed intensity and target specific broadleaf species at the right growth stage. In large soybean and cotton farms, this flexibility makes a practical difference, especially when weather conditions delay planting or early spraying windows.

By Crop Type Analysis

Cereals and Grains take the lead with 45.8% share in 2024, backed by broad acreage and steady weed pressure

In 2024, Cereals and Grains held a dominant market position, capturing more than a 45.8% share. This strong position reflects the vast acreage under crops such as wheat, corn, barley, and sorghum, where consistent weed management is essential for maintaining yield and grain quality. Farmers growing cereals typically operate on large fields, and even moderate weed infestation can directly impact productivity and harvest efficiency. Dicamba continues to be valued in these cropping systems for its effectiveness against tough broadleaf weeds that compete aggressively during early and mid-growth stages.

Key Market Segments

By Form

- Liquid

- Dry

By Time of Application

- Post-Emergence

- Pre-Emergence

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Pastures & Forage Crops

- Others

Emerging Trends

A clear shift toward “stewardship-first” dicamba use, driven by tighter rules and drift prevention

One of the latest trends shaping dicamba is the industry’s move away from “just spray it” thinking and toward stewardship-led, tightly controlled use. The direction is simple: dicamba remains a valuable broadleaf weed tool, but it is increasingly treated like a high-responsibility product where training, documentation, and drift prevention decide whether it stays in a farm program. This trend is not coming from marketing—it is being pushed by regulators, by neighboring crop risk, and by the real-world cost of complaints and investigations.

The strongest evidence behind this trend is the public record on off-target incidents. The U.S. Environmental Protection Agency (EPA) reported receiving about 3,500 dicamba-related incident reports from the 2021 growing season, and those reports indicated more than one million acres of non-dicamba-tolerant soybean crops were allegedly damaged by off-target movement. This type of scale changes behavior across the supply chain: applicators become cautious, retailers tighten how products are sold and supported, and growers pay more attention to what happens beyond their own fence line.

Regulatory actions in 2024 accelerated the “stewardship-first” trend even more. A federal court order on February 6, 2024 vacated registrations for certain over-the-top dicamba products, and EPA followed with an Existing Stocks Order dated February 14, 2024 that allowed limited disposition and time-bound use under specific conditions. When rules shift midstream like this, farms and input dealers respond by simplifying decisions—often favoring programs that have clearer compliance pathways. That pushes dicamba suppliers and users to emphasize best-practice application details as a core “product feature,” not a footnote.

The market context makes this even more important because dicamba lives inside very large-acre crop systems. In the U.S., soybean planted area was estimated at 83.4 million acres in 2025, and producers planted 96% of soybean acreage using herbicide-resistant seed varieties (the same level as 2024). With that level of trait adoption, weed control decisions happen at industrial scale. The trend is that large farms increasingly rely on standardized spray playbooks: fewer “judgment calls” in the field, more pre-checks around weather, droplet size, and field-edge risk. In practice, this is where dicamba’s direction is headed—more controlled use, fewer surprises, and stronger proof that the application followed the label.

Drivers

Weed resistance pressure across huge food-crop acreage is pushing dicamba demand

One major driving factor for dicamba is the rising need to control hard-to-kill broadleaf weeds in very large food and feed crop systems, where even small yield losses become expensive. Dicamba is often chosen when growers need a fast, reliable “in-season reset” against broadleaf weeds that compete aggressively with crops like soybeans and corn. This matters because soybean is not a niche crop—it sits in the center of edible oil, protein meal, and livestock feed supply chains. In the United States alone, soybean planted area was 87.1 million acres in 2024, showing how big the weed-control battleground is each season.

The scale becomes clearer when output is considered. USDA reports soybean production of 4.37 billion bushels in 2024. When production volumes are this high, growers focus heavily on protecting harvestable yield and keeping fields clean for efficient combining. In practical farm terms, that means weed programs are not optional—they are built into the crop budget. Dicamba benefits from this reality because it is positioned as a broadleaf herbicide that can be used as part of planned spray passes when weeds are visible and actively growing.

Another reason this driver is strong is that modern seed systems are built around herbicide tolerance. USDA noted that producers planted 96% of U.S. soybean acreage using herbicide-resistant seed varieties. This level of adoption shows how tightly weed control is linked to farm productivity and time management: when most acres are planted with herbicide-resistant traits, growers expect chemical weed control tools to stay dependable and workable within label rules. Dicamba demand grows in years when weeds break through early programs, because post-emergence decisions are often made quickly and at scale.

Field practice data supports the same story. USDA’s 2023 soybean chemical use highlights show herbicides were applied to 96% of planted soybean acres. That single number explains why dicamba keeps industrial relevance: herbicide use is already near-universal in commercial soybean production, and farmers continually adjust the active ingredients they rely on as weed pressure and resistance patterns evolve. In other words, dicamba’s demand is pulled forward by the same forces that keep herbicide programs essential—large acreage, tight spray windows, and the need to protect yield potential under real-world conditions.

Restraints

Regulatory and Drift Concerns Hurt Dicamba Adoption Despite Its Benefits

One of the major restraining factors limiting dicamba’s wider acceptance is the ongoing regulatory uncertainty and environmental concerns tied to its off-target movement and crop damage. Although dicamba is valued for controlling stubborn broadleaf weeds, real-world data show that its ability to drift beyond the intended application site has led to significant complaints, costly investigations, and tighter government oversight.

A stark example of this restraint is seen in the volume of incident reports submitted to the U.S. Environmental Protection Agency (EPA). In the 2021 growing season alone, the EPA received nearly 3,500 dicamba-related incident reports from across the United States that indicated damage to non-target vegetation due to off-target movement and spray drift. These reports included cases where dicamba harmed plants and crops it was never intended to treat, raising alarms among regulators and neighboring growers.

The scale of the problem did not go unnoticed. In those reports, it was estimated that more than one million acres of non-dicamba-tolerant soybean crops suffered damage because of dicamba drift. Damage was also documented to other agricultural crops, non-agricultural vegetation, and even wildlife refuge land. These large figures underscore why regulatory agencies have had to rethink how dicamba products can be used safely without jeopardizing adjacent farms or fragile ecosystems.

Regulators in several states have reacted to these concerns with local measures that further constrain use. For example, Minnesota’s Department of Agriculture received 249 complaints and conducted 56 official investigations related to dicamba damage in 2017, spread across 49 counties in the state. These numbers have shaped how state regulators think about label restrictions, cutoff dates, and allowable conditions for application.

Opportunity

Export-driven growth in soybeans is opening room for “safer-use” dicamba programs

One major growth opportunity for dicamba sits in the simple math of global soybean demand. As soybean trade expands, farmers are pushed to protect yields on bigger, more valuable acreage—and broadleaf weed control becomes a must-have line item, not a “nice to have.” In 2024/2025, Brazil produced 171.5 million metric tons of soybeans, while the United States produced 119.05 million metric tons. That scale matters because soybeans feed both edible oil and protein meal markets, so any yield loss from weed pressure shows up quickly in supply chains.

The pull from importing countries is just as important. In 2025, China imported a record 111.83 million metric tons of soybeans, up 6.5% from the prior year, largely driven by South American buying patterns and supply security planning. When import volumes move at this size, growers and exporters feel pressure to deliver consistent quality and volume, which increases the value of dependable in-season weed control in soybean fields.

This opportunity is reinforced by how industrialized weed management already is in major producing regions. In the U.S., farmers planted 83.4 million acres of soybeans in 2025, and 96% of soybean acreage used herbicide-resistant seed varieties. This indicates that herbicide-enabled crop systems remain the default on most farms, and growers tend to adopt products that fit into modern sprayer operations, trait packages, and documented stewardship practices.

Government-backed investment in on-farm practices also supports this shift toward more controlled, precision-led application. USDA announced up to $7.7 billion in assistance for fiscal year 2025 to help producers adopt conservation practices on working lands, including up to $5.7 billion for climate-smart practices. While this funding is not “for dicamba,” it accelerates the exact on-farm upgrades dicamba programs benefit from—better equipment calibration, training, recordkeeping, and field-edge protections that reduce off-target movement and neighbor-to-neighbor conflict.

Regional Insights

North America dominates with 52.7% share, valued at USD 293.0 Mn, backed by large-scale row-crop farming and herbicide-tolerant systems

North America is the dominating region in the dicamba market, holding 52.7% share and reaching USD 293.0 Mn. The region’s lead is strongly linked to the scale of commercial farming and the continued reliance on herbicide-based weed control in major food and feed crops. In the U.S., soybeans alone covered 87.1 million planted acres in 2024, and production reached 4.37 billion bushels, which keeps weed management budgets high and consistent across seasons.

In 2025, soybean planted area was estimated at 83.4 million acres, showing that even with year-to-year shifts, the planted base remains massive. What matters more is the technology mix: USDA reported that producers planted 96% of U.S. soybean acreage using herbicide-resistant seed varieties (the same level as 2024). This high adoption supports ongoing demand for compatible herbicide programs where dicamba has historically been used as a broadleaf option in certain systems.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF supports weed-control programs through a broad crop-protection portfolio and global manufacturing footprint. In 2024, BASF reported €65.3 billion in sales and 111,822 employees (headcount). Its size helps fund formulation improvements and application guidance, which matters as drift-risk and label compliance become stricter in modern herbicide use.

Bayer is a major dicamba-linked player through its Crop Science herbicide portfolio and row-crop stewardship focus. In 2024, Bayer reported €46.6 billion in group sales and 99,538 employees (FTEs). These scale advantages support R&D, regulatory work, and dealer training needed for high-compliance herbicide programs.

Corteva is a key crop-inputs company serving farmers with seed and crop protection solutions used across major food-crop acres. The company reports $16.9B in 2024 net sales, operations in 110 countries, and about ~22K employees—scale that supports product rollouts, agronomy support, and stewardship programs tied to in-season weed control needs.

Top Key Players Outlook

- Bayer AG

- BASF SE

- Corteva Agriosciences

- Nufarm Ltd

- Albaugh LLC

- Alligare, LLC

- ADAMA Ltd

- Syngenta

Recent Industry Developments

In 2024, Bayer reported Group sales of €46.6 billion and Crop Science sales of €22.3 billion, showing how large its agriculture business is inside the wider company. In workforce terms, Bayer reported 94,081 employees worldwide.

In 2025, BASF continued to operate under a tougher dicamba environment in the U.S.; after EPA’s February 14, 2024 Existing Stocks Order that covered Engenia® Herbicide, BASF stated it would continue to not sell or distribute Engenia herbicide in the United States, highlighting how policy and litigation-driven decisions can directly shape dicamba availability and regional demand.

Report Scope

Report Features Description Market Value (2024) USD 556.1 Mn Forecast Revenue (2034) USD 1211.7 Mn CAGR (2025-2034) 8.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Liquid, Dry), By Time of Application (Post-Emergence, Pre-Emergence), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Pastures And Forage Crops, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Bayer AG, BASF SE, Corteva Agriosciences, Nufarm Ltd, Albaugh LLC, Alligare, LLC, ADAMA Ltd, Syngenta Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Bayer AG

- BASF SE

- Corteva Agriosciences

- Nufarm Ltd

- Albaugh LLC

- Alligare, LLC

- ADAMA Ltd

- Syngenta

Our Clients

- 177627

- Feb 2026