Global Defense Communication Intelligence Market Size, Share, Growth Analysis By Component (Hardware, Software, Services), By Installation (HandHeld, Vehicle Mounted, Fixed), By Platform (Land, Airborne, Naval, Space-based Platforms), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 183681

- Number of Pages: 224

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

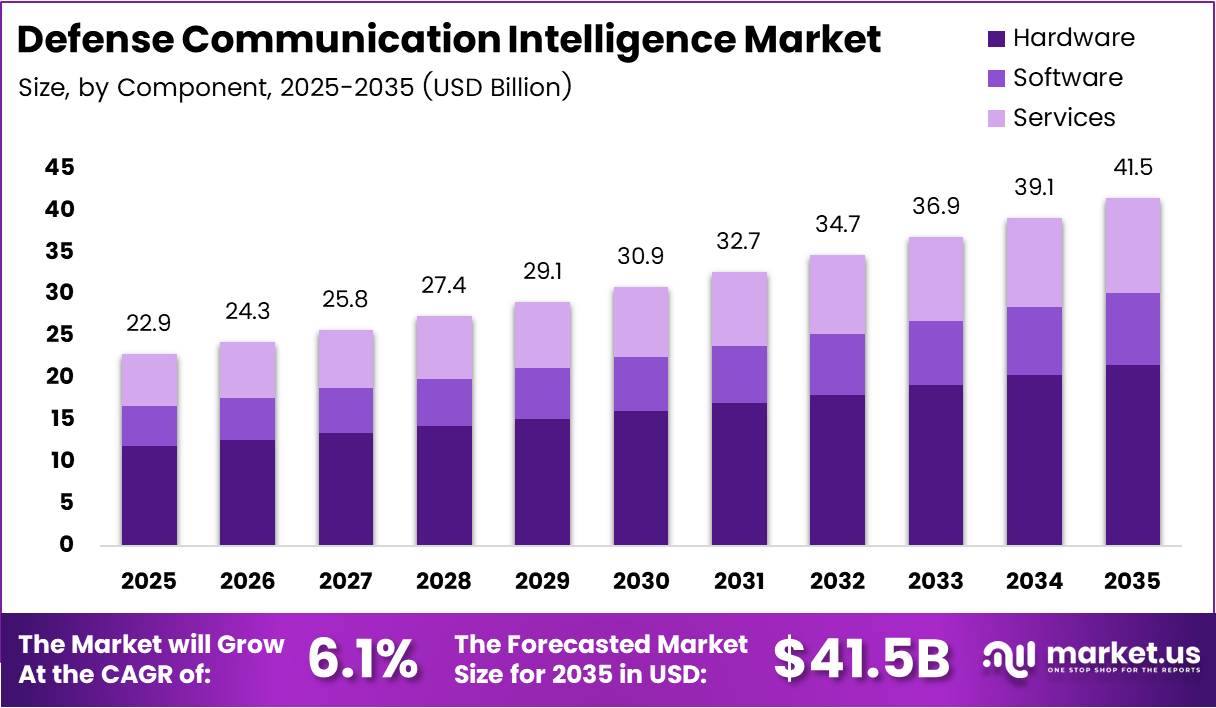

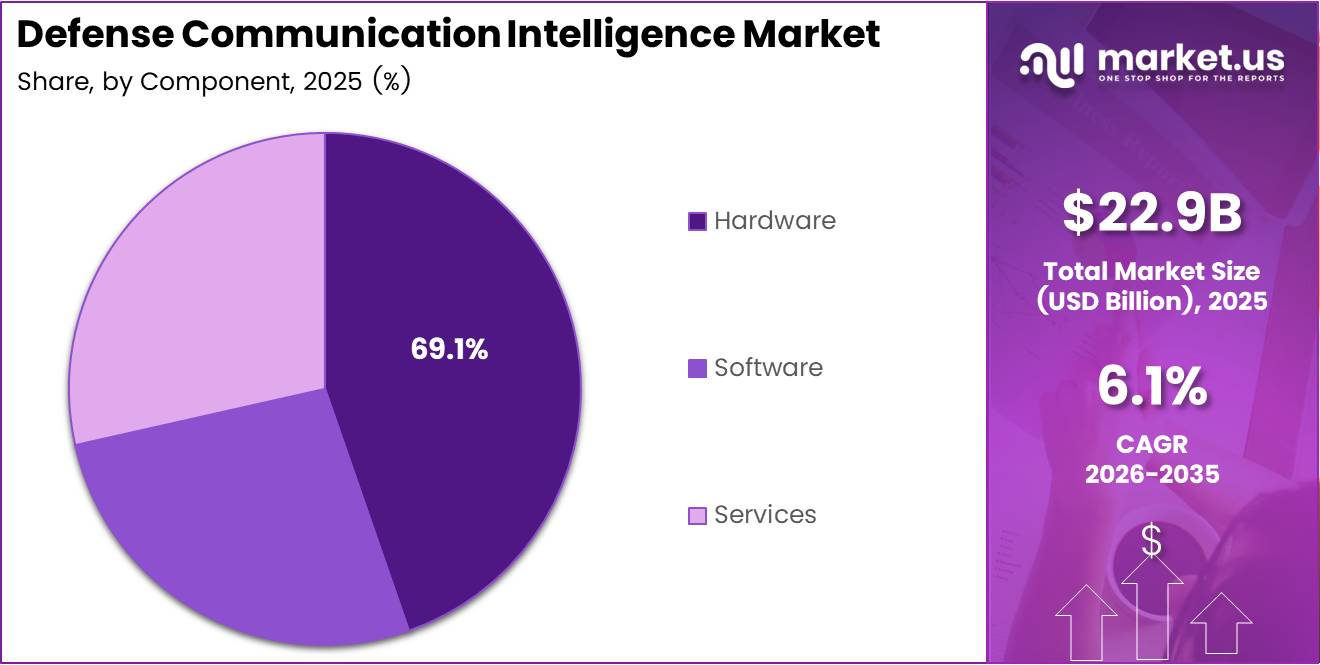

Global Defense Communication Intelligence Market size is expected to be worth around USD 41.5 Billion by 2035 from USD 22.9 Billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

The defense communication intelligence market covers hardware, software, and service solutions that enable military forces to collect, process, and act on signals intelligence across land, air, naval, and space domains. These systems form the operational backbone of modern defense, connecting battlefield units to command-and-control infrastructure in real time.

What separates this market from conventional defense electronics is its convergence of communications and intelligence. Platforms must not only transmit data securely but also intercept, analyze, and jam adversary signals — often simultaneously. This dual function drives procurement complexity and raises the technical bar for every vendor competing for defense contracts.

Military forces worldwide are accelerating investment in network-centric warfare capabilities, requiring secure, interoperable communication intelligence systems across all domains. The shift from platform-centric to network-centric operations means that every soldier, vehicle, and aircraft becomes a node — and each node demands communication intelligence solutions that are both hardened and adaptable.

Government defense budgets reflect this priority directly. NATO members are increasing defense spending toward the 2% GDP target, while Indo-Pacific nations are expanding their tactical communication and SIGINT procurement programs. These allocation decisions create durable, multi-year demand across all segments of this market.

In March 2025, Ultra Electronics Advanced Tactical Systems unveiled its unified ADSI platform integrating AI to enhance data translation, collaboration, and communications intelligence capabilities across military platforms. This product launch signals that vendors are no longer selling standalone systems — they are selling integrated intelligence ecosystems, a shift that will reshape procurement evaluations going forward.

According to a 2025 analysis from the Centre for Advanced Strategic Studies (CAPSS India), AI-based predictive maintenance and decision-support tools reduce unplanned equipment downtime by around 20–30% and shorten operational planning cycles by roughly 30–40% in early-fielded systems. For defense buyers, this is not an incremental improvement — it directly translates to higher mission readiness rates and reduced lifecycle operating costs.

These efficiency gains are reshaping procurement criteria. Defense ministries now evaluate communication intelligence systems not just on raw capability but on AI integration depth and platform interoperability. Vendors who cannot demonstrate measurable operational impact through embedded AI face an accelerating disadvantage in competitive bids.

Key Takeaways

- The Global Defense Communication Intelligence Market was valued at USD 22.9 Billion in 2025 and is forecast to reach USD 41.5 Billion by 2035, at a CAGR of 6.1%.

- By Component, Hardware leads the market with a 51.7% share in 2025, reflecting strong demand for ruggedized communication and signal intelligence equipment.

- By Installation, Vehicle Mounted systems dominate with a 56.2% share, driven by mobile operational requirements across ground forces.

- By Platform, Land platforms hold the largest share at 51.9%, supported by the scale of ground-based defense operations globally.

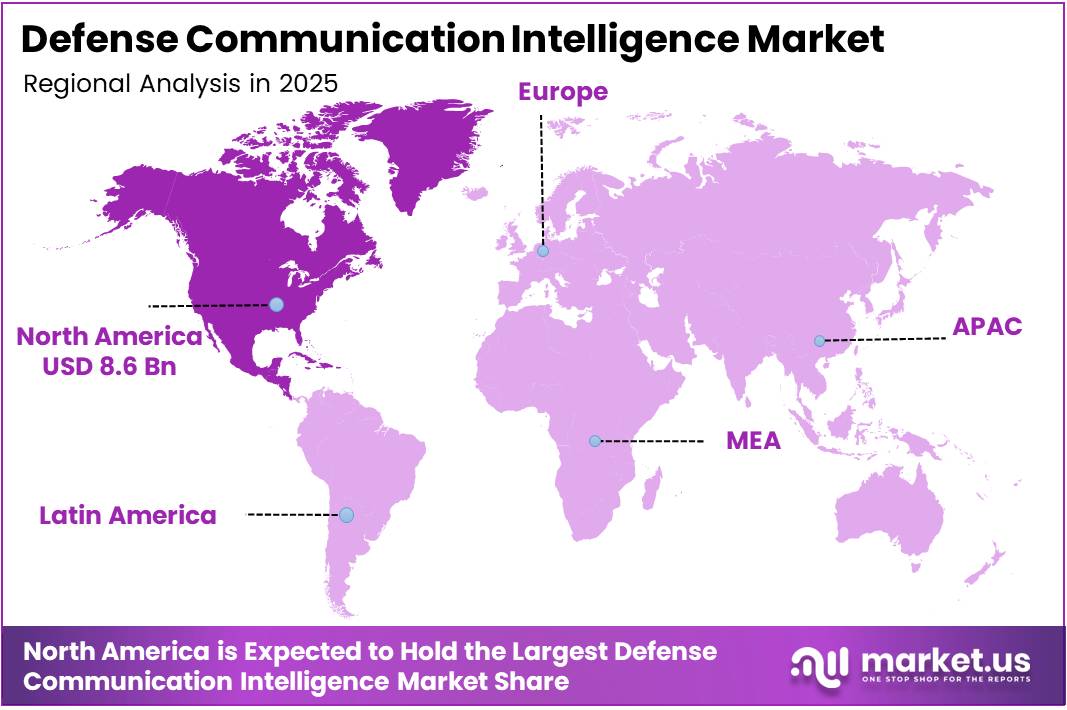

- North America leads all regions with a 37.90% share, valued at USD 14.8 Billion, underpinned by the highest defense R&D expenditure globally.

Product Analysis

Hardware dominates with 51.7% due to essential ruggedized physical communication systems.

In 2025, Hardware held a dominant market position in the By Component segment of the Defense Communication Intelligence Market, with a 51.7% share. Military operations require physical radio transceivers, antennas, signal processors, and electronic warfare equipment that must function in extreme environments. No software layer operates without this hardware foundation, making it the non-negotiable first-spend category for every defense procurement program. In September 2025, TCI unveiled two new rackmount RF COMINT and geolocation systems for continuous real-time signal collection, underscoring ongoing hardware investment across defense agencies.

Software carries the highest margin within the defense communication intelligence value chain. As platforms mature, defense agencies shift spending toward software-defined upgrades rather than full hardware replacement cycles. This upgrade-driven demand model gives software vendors a recurring revenue advantage and positions them as long-term partners rather than one-time suppliers.

Services serve as the operational continuity layer for defense communication intelligence systems. Integration, training, maintenance, and managed intelligence services ensure that complex multi-domain platforms remain mission-ready throughout their lifecycle. As systems grow more interconnected and technically demanding, services revenue scales in parallel with installed base growth.

Installation Analysis

Vehicle Mounted dominates with 56.2% due to mobile ground force operational requirements.

In 2025, Vehicle Mounted systems held a dominant market position in the By Installation segment of the Defense Communication Intelligence Market, with a 56.2% share. Ground vehicles form the operational core of most defense forces, and mounting communication intelligence systems on armored platforms provides protected mobility that neither handheld nor fixed installations can replicate. The scale of vehicle-mounted deployments across NATO and Indo-Pacific forces makes this the structurally largest installation category by procurement volume.

HandHeld systems differentiate through individual-soldier deployment and rapid tactical flexibility. Handheld communication intelligence devices allow special operations forces and forward observers to operate independently from vehicle or fixed infrastructure. Their portability creates demand in scenarios where larger platforms cannot operate, sustaining a niche but high-value procurement category.

Fixed installations serve as the intelligence backbone at command centers, forward operating bases, and strategic facilities. Fixed systems offer the highest processing throughput and can support continuous, long-duration SIGINT collection that mobile platforms cannot maintain. Consequently, fixed installations anchor the high-end of the intelligence processing architecture for most national defense programs.

Platform Analysis

Land dominates with 51.9% due to the scale of ground-based military operations globally.

In 2025, Land platforms held a dominant market position in the By Platform segment of the Defense Communication Intelligence Market, with a 51.9% share. Ground forces represent the largest uniformed segment of every major military, and the communication intelligence requirements across armored brigades, infantry units, and special forces create sustained procurement demand that no other platform category matches in volume.

Airborne platforms carry the highest intelligence collection value per asset due to their speed, altitude, and sensor reach. Airborne SIGINT and COMINT systems cover wide geographic areas in a single mission, making them critical to strategic intelligence operations. The premium unit cost of airborne systems means that this segment delivers disproportionate revenue per platform despite lower unit volume than land-based deployments.

Naval platforms serve a dual role in defense communication intelligence — both as intelligence collection platforms and as protected communication relay nodes for maritime forces. Naval systems must operate in contested electromagnetic environments while maintaining reliable connectivity with shore-based command infrastructure, making their technical requirements among the most demanding in the market.

Space-based platforms represent the fastest-expanding segment within defense communication intelligence. Satellite-based SIGINT and secure communication constellations provide persistent global coverage that no terrestrial or airborne platform can replicate. The integration of space-based intelligence with tactical land and airborne systems is redefining the operational concept of multi-domain awareness for modern defense forces.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Installation

- HandHeld

- Vehicle Mounted

- Fixed

By Platform

- Land

- Airborne

- Naval

- Space-based Platforms

Drivers

Military Investments in Secure Communication and Network-Centric Intelligence Systems Accelerate Global Procurement

Defense ministries across NATO, Indo-Pacific, and Middle Eastern alliances are directing larger budget shares toward secure communication and battlefield intelligence infrastructure. This spending shift reflects a doctrinal transition — modern warfare demands that every unit, from special forces to armored brigades, operates within an integrated intelligence network rather than relying on isolated communication links.

Real-time battlefield data sharing has become an operational requirement rather than a capability upgrade. Forces operating without continuous SIGINT feeds and encrypted communication links face asymmetric disadvantages against adversaries who have already fielded these systems. This creates non-negotiable procurement demand across all platform categories — land, airborne, naval, and space.

According to a 2025 analysis from CAPSS India, AI-enabled data-fusion and situational-awareness systems cut analyst processing time for multi-sensor information by about 40–50%, allowing defense intelligence units to handle higher ISR data volumes with the same staffing. Additionally, in August 2025, Elbit Systems secured a USD 1.635 billion contract to deliver advanced SIGINT, COMINT, and electronic warfare systems to a European country — a single award that demonstrates the scale of national investment entering this market.

Restraints

High Procurement Costs and Cybersecurity Vulnerabilities Constrain Adoption Among Smaller Defense Forces

Advanced defense communication intelligence platforms demand significant upfront capital for development, integration, and procurement. Hardware-intensive systems with embedded signal processing, electronic warfare, and encryption capabilities carry costs that mid-tier and smaller defense budgets cannot absorb without international co-financing or phased procurement programs. This cost barrier concentrates procurement power among a small number of well-funded defense establishments.

Cybersecurity risks compound the procurement challenge. Military communication networks present high-value targets for state-sponsored actors, and a single vulnerability in a tactical communication system can compromise entire operational networks. The engineering investment required to harden systems against both electronic warfare and cyber intrusion adds material cost to every platform generation, further stretching procurement timelines.

These combined constraints slow the democratization of advanced communication intelligence capabilities across allied nations. Smaller NATO members and developing-world defense forces often operate legacy communication systems longer than strategically advisable, creating interoperability gaps within alliances. For vendors, this means the addressable market for high-end systems remains concentrated among fewer than 20 nations with sufficient defense budgets to procure at scale.

Growth Factors

AI-Powered Intelligence Platforms, Quantum-Secure Communications, and Space Integration Open New Defense Market Segments

AI-powered intelligence analysis platforms are unlocking a new procurement category within defense communication intelligence. Defense agencies that have invested in ISR hardware now require software layers capable of automating signal classification, threat identification, and intelligence dissemination. Reporting on India’s 2025 AI military modernization program shows AI-enabled ISR and decision-support tools integrating into command-and-control workflows — a trajectory that mirrors procurement planning across multiple Asia-Pacific defense establishments.

Quantum-resistant secure communication technologies address an emerging strategic threat — the risk that current encryption standards become vulnerable to future quantum computing capabilities. Defense procurement offices in the US, UK, and EU are beginning to mandate quantum-resistant protocols in new communication intelligence platform specifications. This creates an upgrade cycle across the installed base that will generate sustained replacement demand through the forecast period.

In September 2025, Voyager Technologies acquired BridgeComm Technologies to accelerate optical communication solutions for secure, high-throughput defense connectivity. This acquisition reflects the broader integration of space-based communication intelligence systems into tactical operations — a convergence that creates new revenue opportunities for vendors able to deliver end-to-end multi-domain communication intelligence architectures.

Emerging Trends

AI Automation, Secure Cloud Platforms, and Multi-Domain Integration Redefine Defense Communication Intelligence Architecture

Artificial intelligence is shifting from a supplementary feature to the core processing layer in defense communication intelligence systems. Automated signal intelligence processing reduces the time between intercept and actionable intelligence from hours to minutes. Defense forces that embed AI into SIGINT workflows gain a structural decision-cycle advantage over adversaries relying on manual analyst pipelines — a gap that compounds in high-tempo operational environments.

Secure cloud-based military communication platforms are enabling forward-deployed forces to access centralized intelligence databases without compromising operational security. Cloud architecture allows defense agencies to scale intelligence processing capacity rapidly in response to emerging threats, without pre-positioning hardware in every theater. This model also reduces the physical logistics burden that traditional hardware-heavy communication intelligence deployments impose on mobile operations.

Multi-domain integration across air, land, sea, and space communication systems represents the most structurally demanding trend for vendors. According to the same CAPSS India 2025 analysis, AI-based decision-support tools can shorten operational planning cycles by roughly 30–40% when deployed in multi-sensor environments. Vendors capable of delivering unified cross-domain communication intelligence architectures will hold a decisive competitive position as defense forces consolidate procurement toward integrated platform providers.

Regional Analysis

North America Dominates the Defense Communication Intelligence Market with a Market Share of 37.90%, Valued at USD 14.8 Billion

North America holds 37.90% of the global defense communication intelligence market, valued at USD 14.8 Billion in 2025. The United States drives this dominance through the world’s largest defense R&D budget, deep institutional relationships between the Pentagon and prime defense contractors, and a procurement infrastructure that enables rapid transition from development to fielded systems. This structural advantage sustains North America’s lead through the forecast period.

Europe Defense Communication Intelligence Market Trends

Europe accelerates defense communication intelligence investment following NATO’s renewed emphasis on collective security and the 2% GDP defense spending target. Germany, France, and the UK are expanding tactical communication and SIGINT procurement programs, while Eastern European NATO members are modernizing legacy Soviet-era communication systems. The December 2025 Saab EUR 130 million Sirius COMINT/ELINT order from a European NATO country illustrates the scale of active procurement across the region.

Asia Pacific Defense Communication Intelligence Market Trends

Asia Pacific defense communication intelligence spending reflects the region’s intensifying strategic competition and maritime territorial disputes. India, Japan, Australia, and South Korea are expanding secure communication and ISR capabilities as part of broader defense modernization programs. India’s active deployment of AI-enabled command-and-control tools in 2025 demonstrates that adoption in this region has moved beyond pilot programs into operational integration.

Middle East and Africa Defense Communication Intelligence Market Trends

The Middle East drives defense communication intelligence procurement through well-funded Gulf Cooperation Council defense establishments seeking to modernize force structures. GCC nations are investing in tactical communication networks, electronic warfare capabilities, and SIGINT systems as part of comprehensive defense transformation programs. Africa remains at an earlier stage of adoption, with procurement concentrated among nations with active security operations requiring upgraded battlefield communication infrastructure.

Latin America Defense Communication Intelligence Market Trends

Latin America presents a constrained but developing market for defense communication intelligence systems. Brazil and Mexico represent the primary procurement centers, with spending focused on border security, counter-narcotics operations, and force modernization rather than large-scale conventional defense programs. Budget limitations and competing domestic priorities limit the pace at which Latin American defense forces can transition to advanced communication intelligence platforms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Thales occupies a structurally advantaged position in defense communication intelligence through its integration of secure radio, SIGINT, and electronic warfare capabilities within a single vendor architecture. This breadth reduces the integration risk that defense procurement offices face when assembling multi-vendor communication intelligence systems, making Thales a preferred prime contractor across NATO procurement programs where interoperability is a mandatory specification requirement.

IAI (Israel Aerospace Industries) builds its defense communication intelligence positioning around a combat-proven SIGINT and electronic warfare portfolio developed through decades of operational deployment. IAI’s systems carry credibility that laboratory-certified alternatives cannot replicate — defense buyers in high-threat environments actively seek this operational track record. This positions IAI favorably in competitive tenders across Middle Eastern and Asian defense establishments modernizing their intelligence collection capabilities.

General Dynamics Corporation leverages its deep integration into US Department of Defense communication infrastructure to sustain a durable competitive moat. Its classified communication systems, encryption platforms, and C4ISR architectures are embedded into long-cycle DoD programs that create multi-decade revenue visibility. This installed-base lock-in limits competitive displacement and positions General Dynamics as the baseline architecture against which all challengers are evaluated in US defense procurement.

L3Harris Technologies, Inc. differentiates through its tactical radio and multi-domain communication systems, which cover the full spectrum from handheld soldier radios to airborne SIGINT platforms. This vertical coverage allows L3Harris to pursue integrated communication intelligence contracts rather than competing on individual components — a strategic positioning that commands higher contract values and reduces exposure to single-segment price pressure across defense procurement cycles.

Key Players

- Thales

- IAI (Israel Aerospace Industries)

- General Dynamics Corporation

- L3Harris Technologies, Inc.

- AIRBUS

- BAE Systems

- Rohde & Schwarz

- Leonardo S.p.A.

- HENSOLDT

- Ultra

Recent Developments

- March 2025 — Ultra Electronics Advanced Tactical Systems unveiled its unified ADSI platform integrating AI to enhance data translation, collaboration, and communications intelligence capabilities across military platforms. This launch marks a shift toward AI-integrated communication intelligence ecosystems, raising the interoperability standard for defense procurement evaluations.

- September 2025 — TCI unveiled two new rackmount RF COMINT and geolocation systems (models 955 and 957) designed for continuous real-time signal collection and electronic warfare operations. These systems expand TCI’s hardware portfolio for fixed and vehicle-mounted intelligence collection applications across defense agencies.

- December 2025 — Saab received an order worth approximately EUR 130 million from a European NATO country for the Sirius passive sensor system, combining COMINT and ELINT capabilities for SIGINT surveillance and multi-domain situational awareness, with deliveries scheduled through 2030. The contract scale reflects the sustained European demand for integrated passive SIGINT platforms as NATO members accelerate defense modernization programs.

Report Scope

Report Features Description Market Value (2025) USD 22.9 Billion Forecast Revenue (2035) USD 41.5 Billion CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Hardware, Software, Services), By Installation (HandHeld, Vehicle Mounted, Fixed), By Platform (Land, Airborne, Naval, Space-based Platforms), By Region Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Thales, IAI (Israel Aerospace Industries), General Dynamics Corporation, L3Harris Technologies Inc., AIRBUS, BAE Systems, Rohde & Schwarz, Leonardo S.p.A., HENSOLDT, Ultra Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Defense Communication Intelligence MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Defense Communication Intelligence MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Thales

- IAI (Israel Aerospace Industries)

- General Dynamics Corporation

- L3Harris Technologies, Inc.

- AIRBUS

- BAE Systems

- Rohde & Schwarz

- Leonardo S.p.A.

- HENSOLDT

- Ultra

Our Clients

- 183681

- Apr 2026