Global Data Warehouse Automation Market By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Data Integration, Data Quality, Metadata Management, Data Governance, Others), By End-User (BFSI, Healthcare, Retail and E-commerce, IT and Telecommunications, Manufacturing, Government, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Mar. 2026

- Report ID: 179892

- Number of Pages: 353

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component

- By Deployment Mode

- By Organization Size

- By Application

- By End-User

- Investor Type Impact Analysis

- Technology Impact Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

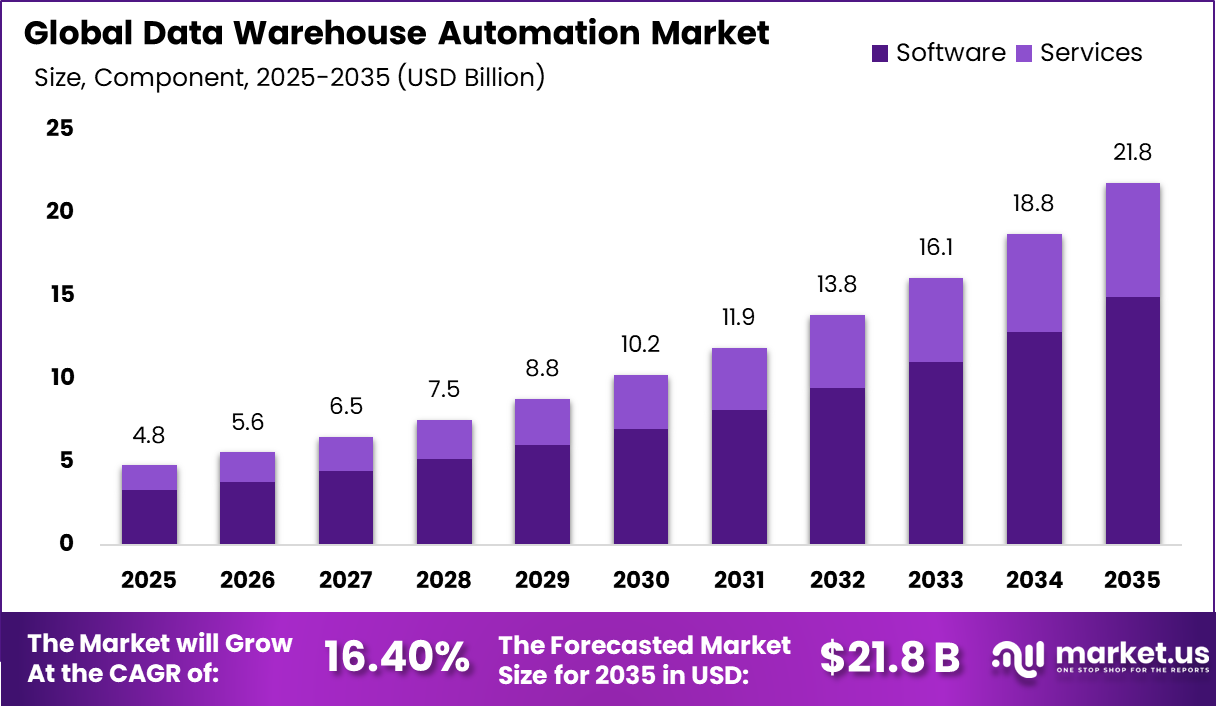

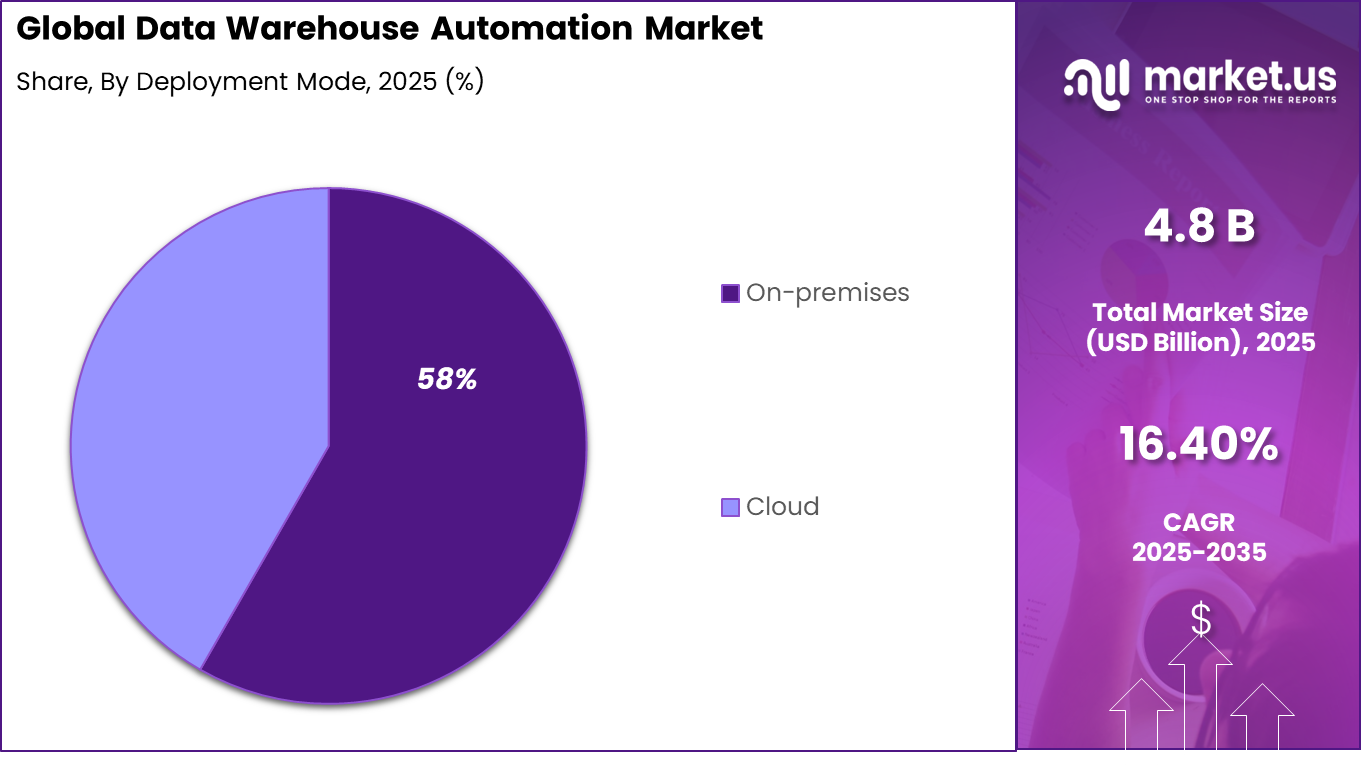

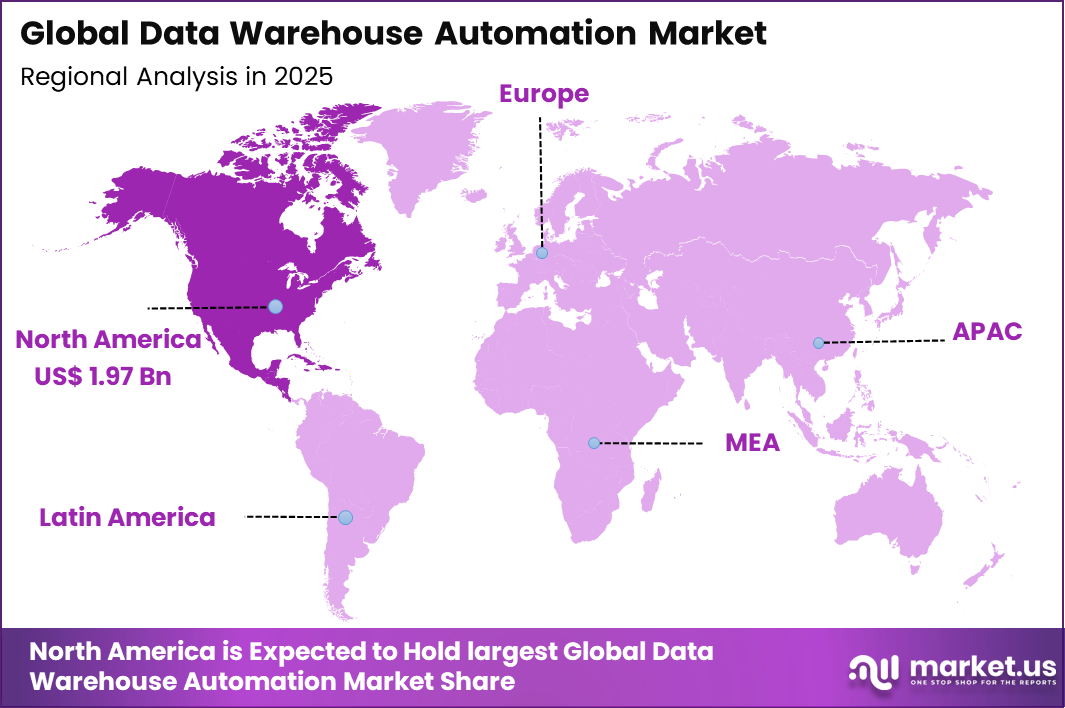

The Global Data Warehouse Automation Market generated USD 4.8 billion in 2025 and is predicted to register growth from USD 5.8 billion in 2026 to about USD 21.8 billion by 2035, recording a CAGR of 16.40% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 41.3% share, holding USD 1.97 Billion revenue.

The Data Warehouse Automation Market is advancing as organizations modernize their data infrastructure to support large scale analytics and business intelligence operations. Enterprises are increasingly adopting automated tools to streamline the design, deployment, and management of data warehouses.

Automation technologies reduce manual development efforts, improve data integration processes, and enable faster access to analytical insights. Market adoption trends highlight the dominance of software driven platforms, on premises infrastructure environments, and large enterprise implementation, particularly within the financial services sector.

According to SellersCommerce, By the end of 2026, nearly 4.69 million commercial warehouse robots are expected to be installed across more than 50,000 warehouses worldwide. Global logistics robot sales also rose sharply to over 450,000 units in 2025, up from 75,000 in 2019, showing a 500% increase over the period. The scale of modern warehouse activity is also increasing, with major e-commerce platforms managing hundreds of millions of active SKUs that require efficient handling of varied product sizes and shapes.

Around 25% of warehouses globally have already adopted some form of automation, while 10% now use advanced automation technologies, up from 5% a decade ago. Looking ahead, 31% of decision-makers in manufacturing, transportation, and logistics plan to move toward full automation by 2028, and 87% are either expanding or planning to expand warehouse capacity by 2026, with automation remaining a central investment priority.

Top Market Takeaways

- By Component, software dominates with 68.5% share, automating ETL pipelines, schema generation, and metadata management through low-code accelerators and AI-driven modeling.

- By Deployment Mode, on-premises captures 58.3%, ensuring governance over sensitive data lakes, hybrid cloud bursting, and compliance with strict residency requirements.

- By Organization Size, large enterprises hold 74.7%, scaling automation across petabyte repositories with self-service provisioning and DevOps-integrated warehouse ops.

- By Application, data integration leads at 38.9%, streamlining CDC from transactional systems, real-time streaming, and federated querying across siloed sources.

- By End-User, BFSI commands 37.7%, powering regulatory reporting, fraud detection warehouses, and customer 360 views with automated data lineage tracking.

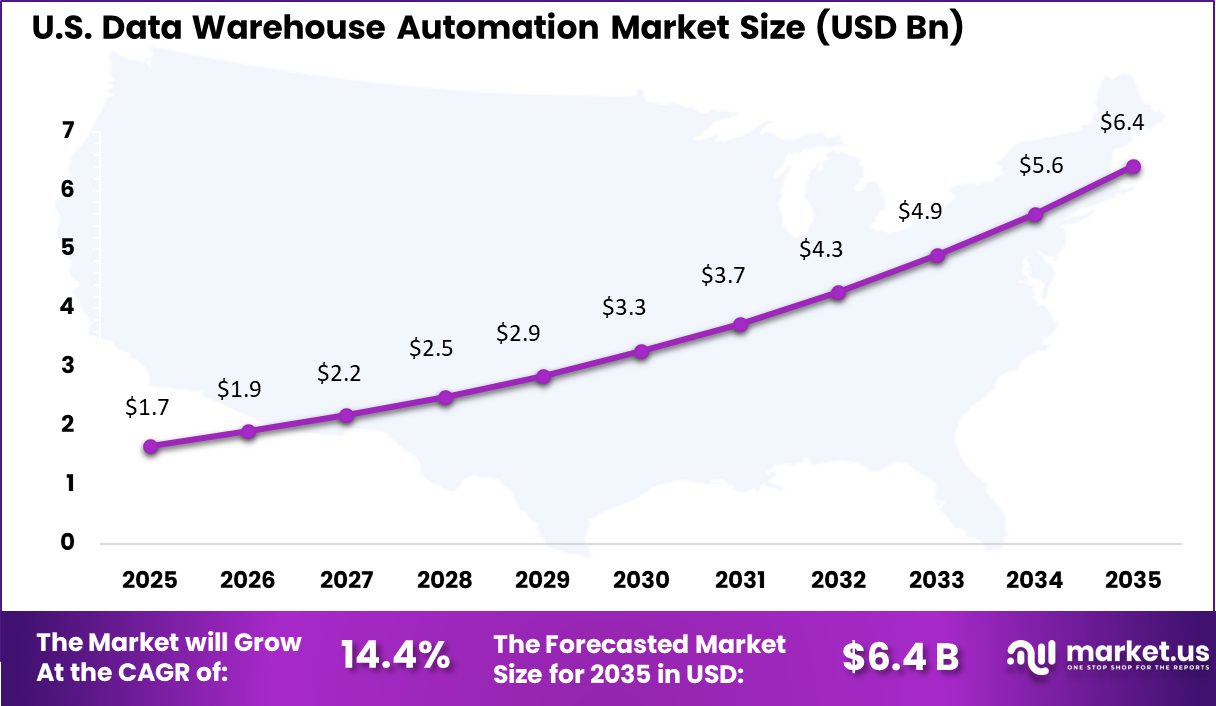

- Regionally, North America accounts for 41.3% global share, with the U.S. market valued at USD 1.67 billion and a CAGR of 14.4%, driven by AI/ML workload surges and cloud repatriation trends.

Drivers Impact Analysis

Key Drivers Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Strategic Importance Rising Enterprise Data Volumes +3.5% Global Short to Long Term Expands need for scalable automation Increasing Adoption of Cloud Data Warehousing +3.0% North America, Europe Medium Term Accelerates deployment flexibility Demand for Faster Time-to-Insight +2.6% Global Medium Term Drives automated modeling and ETL processes Shortage of Skilled Data Engineers +2.1% Global Medium to Long Term Encourages automation to reduce manual workload Integration with Business Intelligence Platforms +1.8% North America, APAC Medium Term Enhances real-time reporting capabilities Restraints Impact Analysis

Key Restraints Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Market Constraint Level High Initial Implementation Costs -2.2% Emerging Markets Short to Medium Term Budget limitations for mid-sized firms Integration Complexity with Legacy Systems -1.9% Europe, APAC Medium Term Extends migration timelines Data Security and Compliance Concerns -1.6% North America, Europe Medium Term Requires strict governance frameworks Dependence on Vendor Ecosystems -1.2% Global Medium Term Limits interoperability flexibility By Component

Software accounts for 68.5% of the market, reflecting the growing reliance on automated platforms that simplify the development and maintenance of enterprise data warehouses. These tools automate tasks such as schema design, code generation, data pipeline creation, and performance optimization. Automation reduces development cycles and helps organizations deploy data warehouse environments more efficiently.

The adoption of automation software also improves consistency across data management processes. Standardized workflows reduce human error and ensure that data structures remain aligned with governance requirements. As organizations process increasing volumes of enterprise data, automated software platforms continue to play a central role in modern data warehouse management.

By Deployment Mode

On premises deployment represents 58.3% of the market, highlighting the need for direct control over enterprise data environments. Many organizations manage highly sensitive operational and financial data that requires strict security and compliance frameworks. Maintaining data warehouse infrastructure within internal systems enables organizations to enforce detailed governance policies.

Internal deployment also allows integration with legacy enterprise systems and existing data repositories. Many large organizations operate complex infrastructure environments that rely on internal databases and customized analytics systems. As data governance requirements remain strict, on premises deployment continues to maintain strong adoption across industries.

By Organization Size

Large enterprises account for 74.7% of market adoption due to the scale and complexity of their data ecosystems. These organizations generate extensive datasets across multiple departments, requiring advanced data warehouse solutions to consolidate and analyze information. Automation tools enable large enterprises to manage data pipelines and reporting systems more efficiently.

Dedicated data management teams within large organizations also drive the adoption of automation technologies. Automated platforms reduce the time required to design and update data models, allowing analysts to focus on strategic insights. As enterprise data volumes continue to grow, large companies remain the primary users of automated data warehouse solutions.

By Application

Data integration represents 38.9% of the market, reflecting the importance of consolidating data from diverse operational systems. Enterprises often manage information from customer databases, financial systems, and operational platforms that must be unified for analytical purposes. Automated data integration tools simplify the process of combining these datasets into a centralized data warehouse.

Automation improves the accuracy and reliability of data pipelines by reducing manual transformation processes. Integrated data environments allow organizations to generate more accurate reports and predictive analytics. As enterprises prioritize data driven decision making, data integration remains a key application for warehouse automation platforms.

By End-User

The BFSI sector accounts for 37.7% of market adoption due to the high volume of financial and transactional data managed by financial institutions. Banks, insurance companies, and investment firms rely on advanced data warehouses to support risk analysis, regulatory reporting, and customer analytics. Automated data management platforms improve processing efficiency and reporting accuracy.

Strict regulatory requirements also require financial institutions to maintain detailed records and audit trails. Data warehouse automation tools help ensure consistent data structures and reporting standards across departments. As digital financial services continue to expand, the BFSI sector remains a leading adopter of automated data warehouse solutions.

Investor Type Impact Analysis

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Venture Capital High Medium to High North America Focus on AI-driven automation platforms Private Equity Medium to High Medium North America, Europe Stable enterprise SaaS revenue models Strategic Cloud Providers Medium to High Low to Medium Global Portfolio expansion into analytics ecosystems Institutional Investors Medium Medium Developed Markets Long-term enterprise IT allocation Corporate IT Service Firms Medium Low to Medium Global Integration with managed analytics services Technology Impact Analysis

Technology Enabler Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Adoption Momentum AI-driven Data Modeling Automation +3.7% North America, Europe Medium to Long Term Reduces manual schema design Cloud-native Data Warehouse Platforms +3.1% Global Short to Medium Term Supports elastic scalability Automated ETL and ELT Pipelines +2.5% Global Medium Term Improves deployment speed Metadata Management and Data Lineage Tools +1.9% Europe, North America Medium to Long Term Enhances compliance and governance Low-code Data Engineering Interfaces +1.5% APAC, North America Long Term Simplifies development workflows Key Challenges

- High setup effort is often required because existing data sources, formats, and business rules are not consistent across teams.

- Data quality issues can remain a major blocker, since automation will also move incorrect or incomplete data faster if controls are weak.

- Integration with legacy systems and mixed cloud environments can be difficult, leading to delays and higher implementation cost.

- Limited internal skills in data modeling, ETL, governance, and automation tools can slow adoption and increase dependency on vendors.

- Security, access control, and compliance requirements can be complex, especially when sensitive data is spread across multiple platforms.

Emerging Trends

In the Data Warehouse Automation market, a clear trend is the adoption of systems that reduce manual effort in building and maintaining data storage environments. Organisations are increasingly using tools that automate routine tasks such as schema design, data integration, and quality checks so that teams can focus on interpreting results instead of preparing them.

This shift helps reduce errors that often occur when repetitive work is done by hand, and it supports more consistent delivery of data for business use. Another pattern emerging is the emphasis on simple, step-by-step guidance within the automation workflow so that even team members with limited technical skills can understand how data moves through the warehouse and why each stage matters.

Growth Factors

A key growth driver in this market is the growing demand for timely and accurate data across functions such as finance, operations, and customer service. Organisations depend on data warehouses to provide a reliable foundation for reports and analytics, and manual delays in updating these systems can slow decision making. Automation helps speed these processes while making them more dependable, which strengthens confidence in the data.

Another important factor is the desire to reduce the burden on specialised data engineers, who are often stretched between new requests and maintenance tasks. By automating routine steps, teams can allocate their time to deeper analysis and strategic improvements that support better outcomes for the organisation. These needs are encouraging broader adoption of automation approaches that are clear, manageable, and aligned with how teams work.

Key Market Segments

By Component

- Software

- Services

By Deployment Mode

- On-Premises

- Cloud

By Organization Size

- Small and Medium Enterprises

- Large Enterprises

By Application

- Data Integration

- Data Quality

- Metadata Management

- Data Governance

- Others

By End-User

- BFSI

- Healthcare

- Retail and E-commerce

- IT and Telecommunications

- Manufacturing

- Government

- Others

Regional Analysis

North America accounted for 41.3% of the Data Warehouse Automation Market, supported by early adoption of cloud data platforms and strong demand for faster, more reliable analytics delivery. Automation has been used to reduce manual effort in data modeling, ETL and ELT development, and documentation, especially in large organizations managing complex data estates across multiple business units.

Higher expectations for data governance, audit readiness, and consistent reporting have also increased the use of automation frameworks, as repeatable pipelines and standardized metadata practices have been prioritized. Adoption has been most visible in data intensive sectors such as banking, insurance, healthcare, retail, and telecom, where data volumes are large and reporting cycles are frequent.

The United States remained the core contributor within the region, reaching USD 1.67 Bn and expanding at a 14.4% CAGR, as modernization programs and cloud migration continued across enterprises and mid sized firms. Strong investment has been directed toward automated pipeline generation, schema and lineage tracking, and controlled deployment practices, as data teams have been asked to deliver more outputs with leaner resources.

Demand has also been supported by tighter expectations around security controls, privacy management, and operational resilience, leading to wider use of automation to enforce consistent rules across environments. Over time, growth has been reinforced by the need to connect diverse sources, improve data quality at scale, and shorten delivery timelines for analytics and AI workloads.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The Data Warehouse Automation Market is led by global enterprise software and cloud platform providers that deliver scalable data integration and analytics infrastructure. Microsoft, Oracle, SAP, IBM, Snowflake, and Amazon Web Services provide integrated data warehouse environments that support automated data pipelines, schema generation, and performance optimization. These companies leverage strong cloud ecosystems and advanced analytics capabilities to support large scale enterprise data environments.

Specialized data integration and automation vendors contribute advanced tools that streamline warehouse design and deployment. Informatica, WhereScape, Talend, Teradata, and Qlik offer platforms that automate data modeling, ETL processes, and metadata management. Their technologies reduce development time and improve data consistency across enterprise systems. Continuous innovation in automated pipeline orchestration and data governance capabilities strengthens their market presence.

Consulting firms and emerging software providers further diversify the competitive landscape. HCL Technologies, Wipro, and Tata Consultancy Services support enterprise implementations through data engineering and cloud migration services. Vendors such as Denodo, Redgate Software, Datavault Builder, TimeXtender, and Bitwise focus on automation frameworks, data virtualization, and agile warehouse development tools.

Top Key Players in the Market

- Informatica

- WhereScape

- Talend

- Oracle

- SAP

- IBM

- Microsoft

- Snowflake

- Amazon Web Services (AWS)

- Teradata

- Qlik (Attunity)

- HCL Technologies

- Wipro

- TCS (Tata Consultancy Services)

- Informatica

- Denodo

- Redgate Software

- Datavault Builder

- TimeXtender

- Bitwise

- Others

Future Outlook

The future outlook for the data warehouse automation market is expected to remain positive as more organizations modernize analytics and move workloads to cloud data platforms. Demand is likely to be supported by the need to reduce manual coding, standardize data pipelines, and improve data quality through repeatable templates, metadata-driven workflows, and automated testing.

Wider use of real time reporting, self service analytics, and AI based insights is also expected to push adoption of faster data integration, scalable processing, and stronger governance controls. In the coming years, stronger focus is expected on security, regulatory compliance, and end to end lineage, with automation being used to shorten delivery cycles while keeping data operations more reliable.

Recent Developments

- June, 2025 – Informatica launched CLAIRE AI in Intelligent Data Management Cloud. It automates warehouse design and code generation. Enterprises deploy faster ELT pipelines. The platform optimizes for Snowflake and Azure Synapse. Metadata-driven flows reduce manual work. Informatica leads with end-to-end automation.

- February, 2026 – TimeXtender updated its platform for lakehouse architectures. It generates SQL for BigQuery and Databricks. Users report 50 percent faster modeling. The tool enforces governance from ingestion. Reusable patterns speed transformations. TimeXtender suits teams building analytics marts.

Report Scope

Report Features Description Market Value (2025) USD 4.8 Billion Forecast Revenue (2035) USD 21.8 Billion CAGR(2025-2035) 16.40% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Data Integration, Data Quality, Metadata Management, Data Governance, Others), By End-User (BFSI, Healthcare, Retail and E-commerce, IT and Telecommunications, Manufacturing, Government, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Informatica, WhereScape, Talend, Oracle, SAP, IBM, Microsoft, Snowflake, Amazon Web Services (AWS), Teradata, Qlik (Attunity), HCL Technologies, Wipro, TCS (Tata Consultancy Services), Informatica, Denodo, Redgate Software, Datavault Builder, TimeXtender, Bitwise, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Data Warehouse Automation MarketPublished date: Mar. 2026add_shopping_cartBuy Now get_appDownload Sample

Data Warehouse Automation MarketPublished date: Mar. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Informatica

- WhereScape

- Talend

- Oracle

- SAP

- IBM

- Microsoft

- Snowflake

- Amazon Web Services (AWS)

- Teradata

- Qlik (Attunity)

- HCL Technologies

- Wipro

- TCS (Tata Consultancy Services)

- Informatica

- Denodo

- Redgate Software

- Datavault Builder

- TimeXtender

- Bitwise

- Others

Our Clients

- 179892

- Mar. 2026