Global Credit Decisioning Platform Market Size, Share and Analysis By Component (Software, Services), By Deployment Mode (Cloud-based, On-Premises), By Organization Size (Large Enterprises, Small & Medium Enterprises), By End-User (Banks & Traditional Financial Institutions, FinTech Lenders & Digital Banks, Credit Unions & Community Banks, Non-Banking Financial Companies (NBFCs), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: April 2026

- Report ID: 184217

- Number of Pages: 266

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

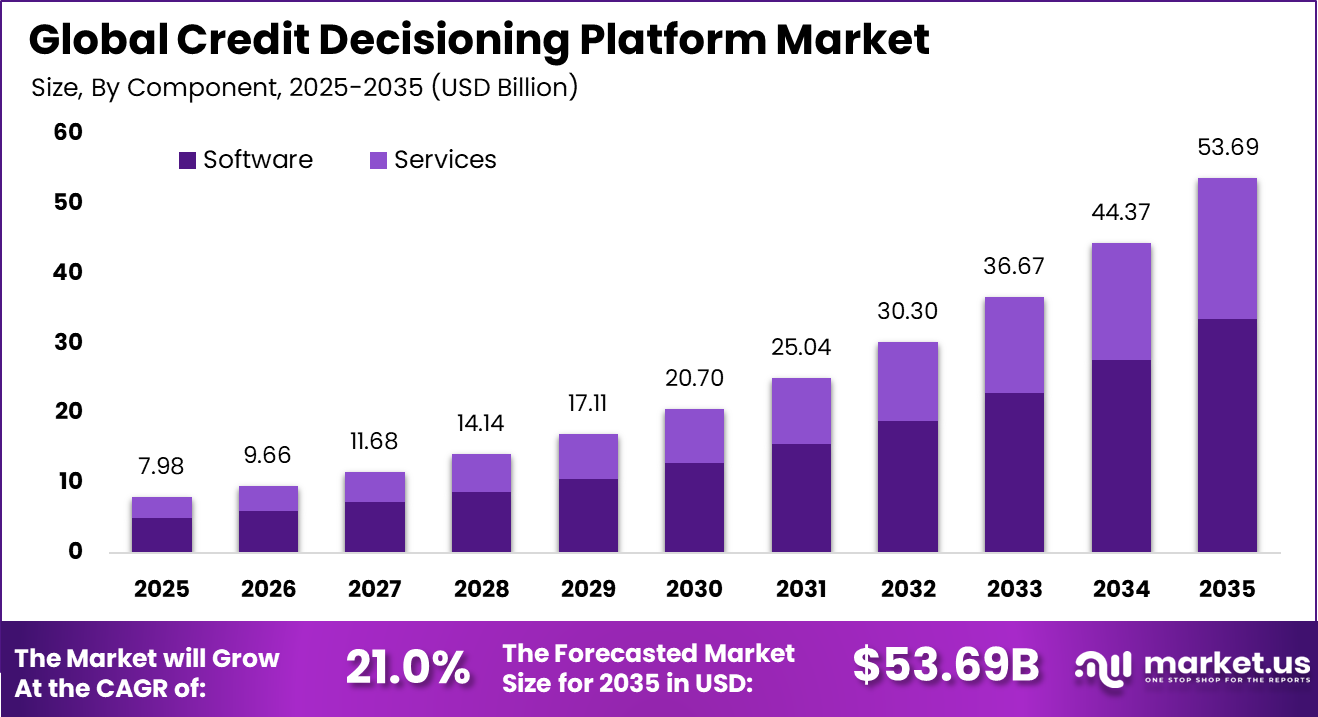

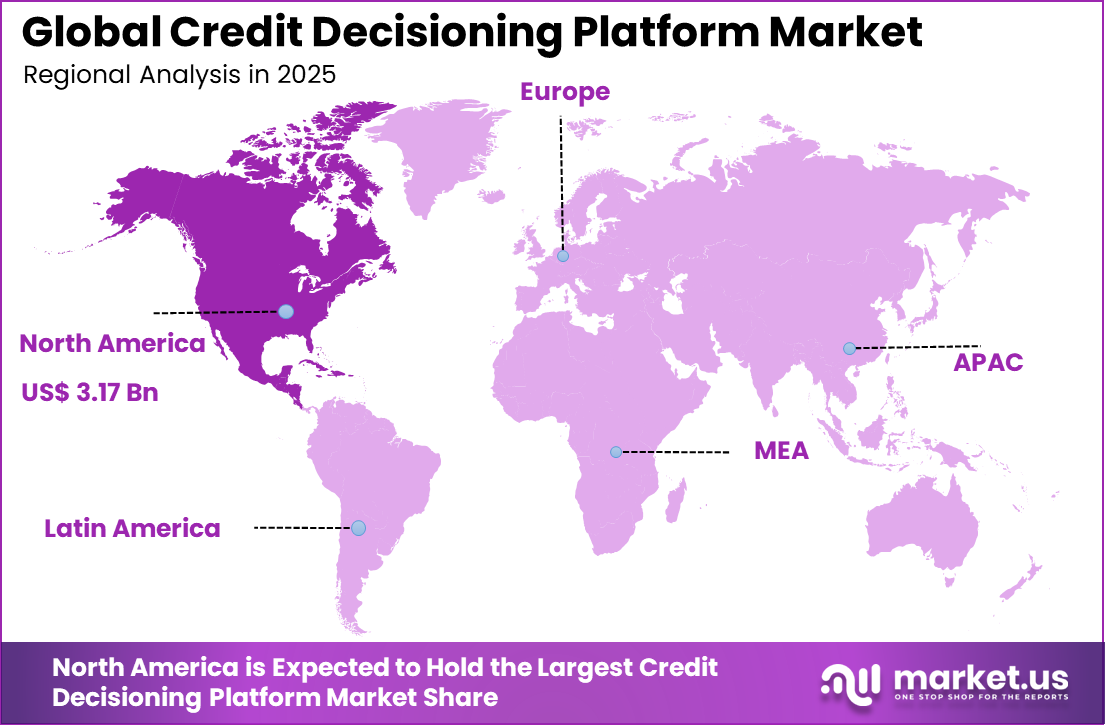

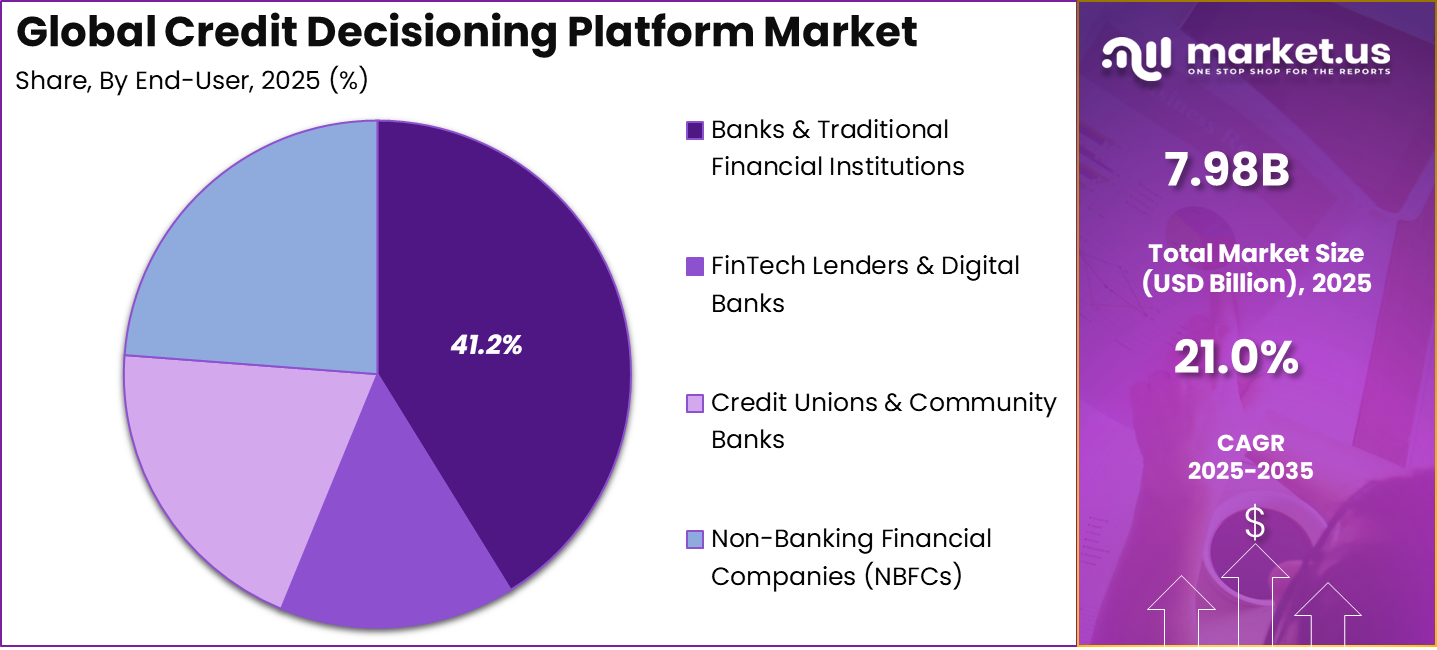

The Global Credit Decisioning Platform Market size is expected to be worth around USD 53.69 billion by 2035, from USD 7.98 billion in 2025, growing at a CAGR of 21.0% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 39.8% share, holding USD 3.17 billion in revenue.

Credit Decisioning Platform refers to a digital system used by lenders to evaluate loan applications and make approval decisions. It combines data, rules, and analytics to assess borrower risk and eligibility. The platform helps automate credit processes, improve accuracy, and speed up decision making while ensuring consistency and better control over lending outcomes.

Lenders are under strong pressure to speed up approvals while keeping risk under control. About 70% of loan applications now require a fast response, often within minutes, which is increasing the use of these platforms across banks. Customer expectations are also changing, as borrowers now look for quick and smooth decisions similar to modern online buying experiences.

The market for Credit Decisioning Platform is driven by the rising need for faster and more accurate lending decisions. Financial institutions are adopting these platforms to reduce manual work, improve risk assessment, and deliver smoother customer experiences. Growing digital loan applications, increasing use of data-based credit models, and the need for better compliance support are also encouraging wider market adoption.

Demand is rising because manual credit checks take more time and often create errors in decision-making. Banks have recognized that nearly 80% of routine credit reviews can be moved to automated systems, allowing teams to focus on more complex files. The growing number of customers with thin credit histories is also increasing reliance on these platforms.

For instance, in April 2026, Experian expanded its U.S. credit decisioning suite by integrating deeper alternative‑data underwriting for mass‑market and BNPL segments. The enhancement lets lenders in North America approve more thin‑file and underbanked customers while maintaining strong default control, underlining Experian’s role in shaping data‑driven lending rules.

Key Takeaway

- In 2025, the software segment led the global credit decisioning platform market with a share of 62.4%.

- The cloud-based segment accounted for 78.6%, reflecting strong demand for scalable and flexible decisioning platforms.

- Large enterprises held a dominant 70.5% share, supported by higher lending volumes and broader digital transformation initiatives.

- Banks and traditional financial institutions captured 41.2%, making them the leading end-user segment in the market.

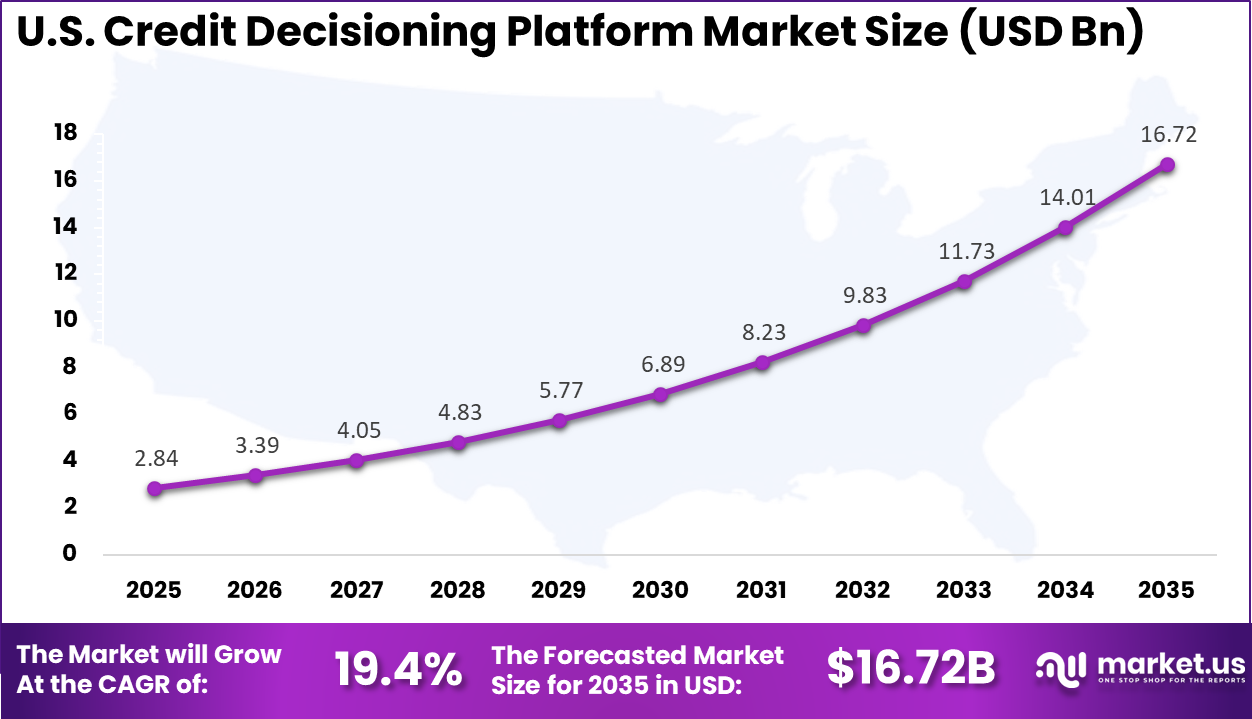

- The U.S. credit decisioning platform market was valued at USD 2.84 billion in 2025 and is projected to grow at a CAGR of 19.4%.

- North America held a dominant position in the global market with a share of more than 39.8% in 2025.

Key Insights Summary

- AI-powered credit decisioning systems can increase automated decisioning rates by 70% to 90%.

- These platforms can improve automated approvals by 30% to 50% and raise overall approval rates by 15% to 40%.

- Credit decisioning tools help reduce loss rates by 10% to 25%, supporting stronger risk control.

- Financial institutions can reduce processing time for high-risk accounts by nearly 50% through AI-led automation.

- In one platform example, combining rule engines, model batteries, and open banking data improved approval rates from 65% to 70%.

U.S. Market Size

The market for Credit Decisioning Platform within the U.S. is growing tremendously and is currently valued at USD 2.84 billion; the market has a projected CAGR of 19.4%. The market is growing due to the strong push for faster, more accurate lending decisions across banks and financial institutions.

Rising digital loan applications, growing use of AI in credit assessment, and demand for better risk control are supporting adoption. The market is also benefiting from open banking trends, higher customer expectations for instant approvals, and the need to reduce manual work while improving compliance and operational efficiency.

For instance, in March 2026, FICO reinforced U.S. dominance in credit decisioning by launching an enhanced AI-driven platform that integrates real-time behavioral data for faster, more accurate lending decisions. Based in Bozeman, Montana, FICO’s innovation helps American banks boost approval rates by 25% while cutting default risks, solidifying North America’s lead in advanced analytics and regulatory-compliant fintech solutions.

In 2025, North America held a dominant market position in the Global Credit Decisioning Platform Market, capturing more than a 39.8% share, holding USD 3.17 billion in revenue. This dominance is due to its advanced financial infrastructure and early adoption of digital lending technologies.

Strong presence of data-driven banking practices and high use of AI in credit assessment support faster decision making. Regulatory focus on transparency and risk management also drives platform adoption. In addition, high consumer demand for instant credit services and widespread use of digital channels continue to strengthen the region’s leading position.

For instance, in February 2026, Equifax from Atlanta, Georgia, expanded its credit decisioning capabilities with a new cloud-native platform featuring machine learning for instant risk scoring. This development empowers U.S. lenders to process millions of applications daily with 30% higher precision, underscoring North America’s forefront position in scalable, data-rich decision engines amid rising digital lending demands.

Component Analysis

In 2025, The Software segment held a dominant market position, capturing a 62.4% share of the Global Credit Decisioning Platform Market. This dominance is due to the central role of software in managing credit rules, workflows, and decision models across lending systems. It enables lenders to process applications with consistency and speed, while ensuring compliance with internal policies. The shift toward automated decision-making has further strengthened reliance on advanced software platforms.

Software continues to gain importance as lenders move away from manual reviews and fragmented systems. It supports integration of diverse data sources, improves decision transparency, and allows faster response times. Financial institutions depend on software to maintain accuracy, reduce operational friction, and enhance the overall efficiency of credit evaluation processes.

For Instance, in March 2026, FICO rolled out its FICO Score Credit Insights Lab, giving lenders a sandbox to test new scoring models and alternative‑data approaches around the core FICO Score ecosystem. This move strengthens its software footprint because it lets banks refine underwriting logic and experiment with more inclusive models without rebuilding entire systems from scratch.

Deployment Mode Analysis

In 2025, the Cloud-Based segment held a dominant market position, capturing a 78.6% share of the Global Credit Decisioning Platform Market. This dominance is due to the growing need for scalable and flexible infrastructure that can support continuous data processing and model updates. Cloud-based platforms allow lenders to manage large volumes of applications without system constraints, making them suitable for modern digital lending environments that require speed and adaptability.

Cloud adoption is also driven by easier integration with external data sources and internal systems. Lenders can access real-time information and deploy updates without disruption. This approach supports faster innovation, improves system reliability, and enables financial institutions to respond quickly to changing customer and regulatory requirements.

For instance, in March 2026, TransUnion introduced an AI Analytics Orchestrator Agent within its TruIQ analytics stack, which translates natural‑language prompts into governed, cloud‑based analytical workflows. This makes advanced credit models accessible to lenders without heavy data‑science teams and reinforces TransUnion’s shift toward cloud‑first decisioning infrastructure.

Organization Size Analysis

In 2025, The Large Enterprises segment held a dominant market position, capturing a 70.5% share of the Global Credit Decisioning Platform Market. This dominance is due to the complex operations handled by large enterprises, which require structured and advanced credit decisioning systems. These organizations manage high transaction volumes and diverse portfolios, making it essential to maintain consistent policies and strong governance across all lending activities.

Large enterprises also invest more in technology to improve operational efficiency and risk management. They adopt advanced platforms to handle regulatory requirements, monitor performance, and streamline processes. This helps them maintain control while scaling operations and delivering faster, more reliable credit decisions across their customer base.

For Instance, in February 2026, SAP enhanced the risk and decisioning modules inside its enterprise platform to support complex credit policies across multiple business units. Large global banks use this layer to align decision logic with corporate risk appetite, which helps them standardize underwriting across geographies and product lines.

End-User Analysis

In 2025, The Banks & Traditional Financial Institutions segment held a dominant market position, capturing a 41.2% share of the Global Credit Decisioning Platform Market. This dominance is due to the critical role of banks and traditional institutions in formal lending activities. These entities rely on structured systems to ensure accurate credit assessment, compliance, and risk control. Credit decisioning platforms help them manage large volumes of applications while maintaining consistency in approvals and rejections.

Banks continue to adopt these platforms to improve customer experience and expand credit access. They use advanced tools to analyze borrower profiles more effectively and support quicker decisions. This allows them to remain competitive while maintaining strong risk management practices and delivering reliable financial services to a wide range of customers.

For Instance, in February 2026, Experian launched a combined credit, cash‑flow, and alternative‑data score tailored for banks that want to widen access to prime and near‑prime borrowers. The model is embedded into banks’ existing onboarding platforms, letting them make more nuanced decisions without overhauling core systems.

Emerging trends

The credit decisioning platform market is rapidly transitioning toward fully automated and AI-driven lending systems. Modern platforms use machine learning, real-time data ingestion, and rule-based engines to evaluate borrower profiles instantly. These systems analyze multiple data sources, including transaction history, behavioral data, and alternative credit indicators, enabling faster and more accurate decision-making.

Another key trend is the growing use of alternative data and explainable AI in credit evaluation. Traditional credit scoring models are being enhanced with additional data sources such as utility payments and digital behavior, allowing lenders to assess individuals with limited credit history. This trend is supporting financial inclusion while improving risk assessment accuracy.

Growth Factors

Open banking is improving data availability, allowing lenders to access detailed financial behavior and make more accurate credit decisions. Platforms can process higher volumes of applications without increasing workforce size. This operational shift has helped reduce processing costs by 25-35%, improving efficiency and scalability for financial institutions.

AI-driven models continue to evolve by learning from new lending data, enhancing their ability to predict repayment behavior over time. This continuous improvement builds confidence among lenders and supports better risk-taking. Adoption of adaptive AI systems has increased by 50%, highlighting strong momentum in advanced credit decision technologies.

Key Market Segments

By Component

- Software

- Services

- Professional Services

- Managed Services

By Deployment Mode

- Cloud-based

- On-Premises

By Organization Size

- Large Enterprises

- Small & Medium Enterprises

By End-User

- Banks & Traditional Financial Institutions

- FinTech Lenders & Digital Banks

- Credit Unions & Community Banks

- Non-Banking Financial Companies (NBFCs)

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Rising Need for Fast Decisions

Lenders are under growing pressure to deliver quick credit decisions as borrowers increasingly expect fast and smooth service. Manual review processes often slow approvals and create delays that affect customer satisfaction. This is pushing financial institutions to adopt credit decisioning platforms that can support faster and more consistent outcomes.

These platforms help lenders review applications in less time while maintaining proper control over risk. They also improve workflow efficiency by reducing repetitive tasks for internal teams. As digital lending expands across consumer and business segments, the need for faster decision-making continues to support steady market growth.

For instance, in April 2026, TransUnion introduced TruIQ Credit Strategy Studio, designed to slash prescreen and strategy build cycles from months to days. The solution lets teams collaborate in a shared workspace, test strategies instantly, and visualize performance, allowing lenders to refine and launch new credit offers at the pace of digital consumer demand.

Restraint

Compliance Complexity

Compliance remains a key restraint because lending decisions must follow strict rules related to fairness, transparency, and risk control. Credit decisioning platforms need to align with changing regulations, which can make implementation more difficult. Many institutions move carefully because they must ensure that automated decisions remain clear and properly documented.

The challenge becomes greater when lenders operate across different products or regions with varying requirements. Internal teams must regularly review models, workflows, and decision rules to avoid compliance issues. This adds time, cost, and oversight demands, which can slow adoption for institutions that lack strong governance structures.

For instance, in March 2026, Experian launched Express offerings using VantageScore 4.0 that combine trended credit data with machine‑learning models, while also layering in fraud‑prevention tools such as Fraud Shield and PreciseID. These capabilities help lenders manage risk, but they must also align with evolving data‑privacy and consumer‑protection rules, which lengthen implementation and testing phases.

Opportunities

Broader Credit Access

A major opportunity in this market lies in expanding credit access to borrowers who are often overlooked by traditional lending methods. Many people and small businesses have limited credit histories, which makes standard assessments less effective. Credit decisioning platforms can use broader financial signals to support more inclusive evaluations.

This creates room for lenders to serve new customer groups while improving the overall reach of their credit products. Better decision tools can help institutions identify reliable borrowers who may have been missed before. As financial inclusion becomes more important, this opportunity is expected to support wider platform adoption.

For instance, in February 2026, FICO reported that Grab Finance in Southeast Asia had raised credit‑offer eligibility rates for its users by nearly half after deploying FICO’s decisioning platform across six countries. The solution enabled 22 distinct decision workflows to be implemented in under eight months, helping more digital‑first consumers qualify for small loans and credit products they might have been denied through traditional scoring.

Challenges

Shortage of Skilled Experts

One of the main challenges in this market is the limited availability of skilled professionals who can manage advanced credit decisioning systems. These platforms often require expertise in data analysis, risk modeling, compliance, and system integration. Without the right talent, lenders may struggle to use these solutions effectively.

The shortage of skilled experts can also slow platform upgrades and reduce confidence in automated decision processes. Institutions need trained teams to monitor model performance, maintain accuracy, and respond to regulatory needs. This talent gap creates operational pressure, especially for lenders trying to modernize their credit functions quickly.

For instance, in April 2025, Zest AI stepped up its model‑development and training programmes for lender teams, offering workshops and embedded consulting to help institutions interpret and tune its machine‑learning decisioning models. The need for such support reflects how hard many banks find it to hire internal staff who can manage AI‑driven risk engines without external help.

Key Players Analysis

The Credit Decisioning Platform Market is led by major credit bureaus and analytics providers offering data-driven risk assessment solutions. FICO, Experian, Equifax, and TransUnion provide advanced credit scoring and decisioning platforms. SAS Institute enhances predictive analytics capabilities. These companies focus on data accuracy and compliance. Their solutions improve credit risk evaluation. This supports efficient lending decisions across financial institutions.

Enterprise software providers play a key role in integrating credit decisioning with broader financial systems. Oracle, SAP, and Pegasystems deliver scalable platforms for workflow automation and customer management. Actico and Provenir support real-time decisioning frameworks. These platforms enhance operational efficiency. Their integration capabilities improve end-to-end credit processing. This strengthens digital lending ecosystems.

Emerging AI-driven firms contribute to innovation in alternative data and intelligent credit scoring. Zest AI, LenddoEFL, CreditVidya, and Scienaptic AI offer machine learning-based credit assessment tools. GDS Link provides automated decisioning solutions. These companies focus on expanding financial inclusion. Other key players continue to enhance capabilities. This competitive landscape supports steady growth in credit decisioning platforms.

Top Key Players in the Market

- FICO

- Experian

- Equifax

- TransUnion

- SAS Institute

- Oracle

- SAP

- Pegasystems

- Actico

- Provenir

- LenddoEFL

- Zest AI

- CreditVidya

- Scienaptic AI

- GDS Link

- CRIF

- Tavant

- FinBox

- LendFoundry

- Others

Recent Developments

- In April 2026, FICO launched a new AI‑enabled “NextGen Decisioning Hub” for banks and fintechs, embedding real‑time behavioral scoring and explainable AI into its core platform. The update allows lenders to automate risk‑based pricing and limit approvals without heavy manual oversight, reinforcing FICO’s position as a leading global credit decisioning infrastructure provider.

- In April 2026, Equifax upgraded its AutoDecision Platform with new real‑time income‑verification and cash‑flow scoring modules, targeting U.S. auto and installment lenders. The move reduces reliance on static credit scores, enabling more dynamic risk‑based offers and giving Equifax a stronger foothold in transaction‑level decisioning.

Report Scope

Report Features Description Market Value (2024) USD 7.9 Bn Forecast Revenue (2034) USD 53.6 Bn CAGR(2025-2034) 21% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software, Services), By Deployment Mode (Cloud-based, On-Premises), By Organization Size (Large Enterprises, Small & Medium Enterprises), By End-User (Banks & Traditional Financial Institutions, FinTech Lenders & Digital Banks, Credit Unions & Community Banks, Non-Banking Financial Companies (NBFCs) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape FICO, Experian, Equifax, TransUnion, SAS Institute, Oracle, SAP, Pegasystems, Actico, Provenir, LenddoEFL, Zest AI, CreditVidya, Scienaptic AI, GDS Link, CRIF, Tavant, FinBox, LendFoundry, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Credit Decisioning Platform MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Credit Decisioning Platform MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- FICO

- Experian

- Equifax

- TransUnion

- SAS Institute

- Oracle

- SAP

- Pegasystems

- Actico

- Provenir

- LenddoEFL

- Zest AI

- CreditVidya

- Scienaptic AI

- GDS Link

- CRIF

- Tavant

- FinBox

- LendFoundry

- Others

Our Clients

- 184217

- April 2026