Global Core Banking Modernization Market By Component (Solutions, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), By Modernization Type (Complete System Replacement, Incremental Modernization (APIs, Microservices), Front-End/Channel Modernization), By End-User (Banks, Credit Unions, Other Financial Institutions), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 176739

- Number of Pages: 301

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Key Market Insights

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component

- By Deployment Mode

- By Organization Size

- By Modernization Type

- By End User

- Emerging Trends

- Growth Factors

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

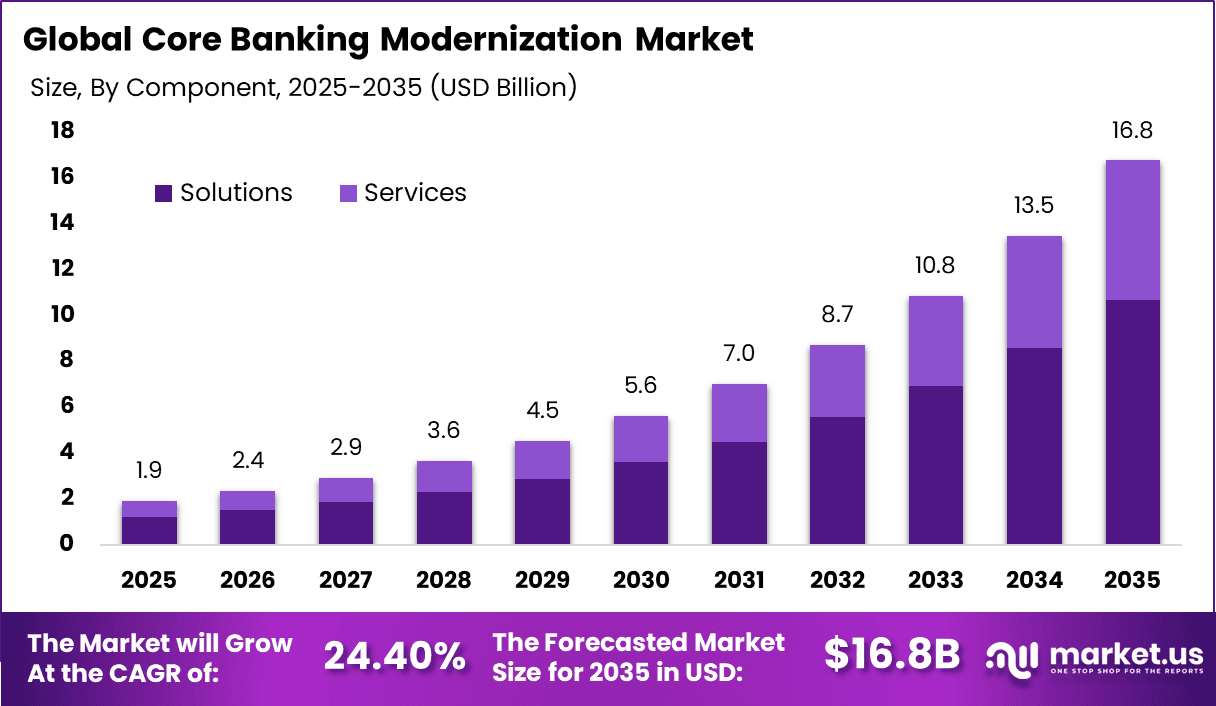

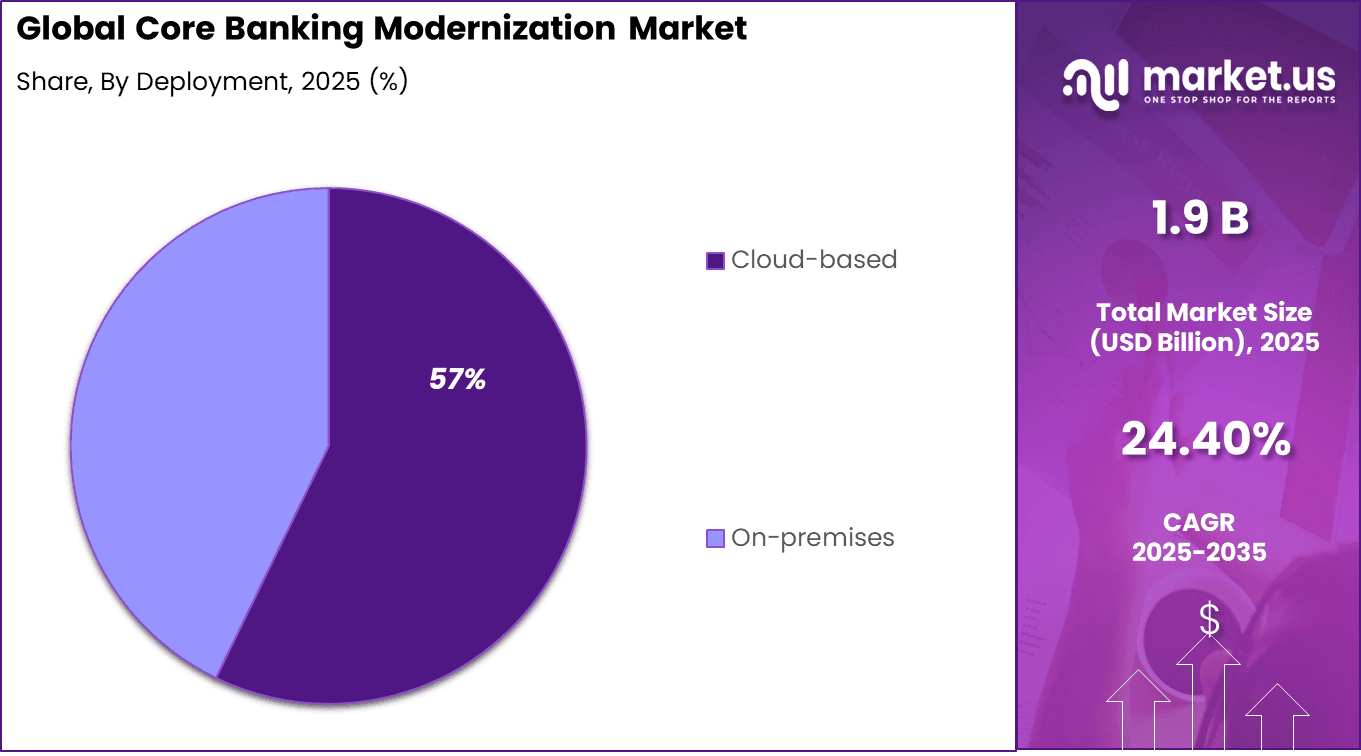

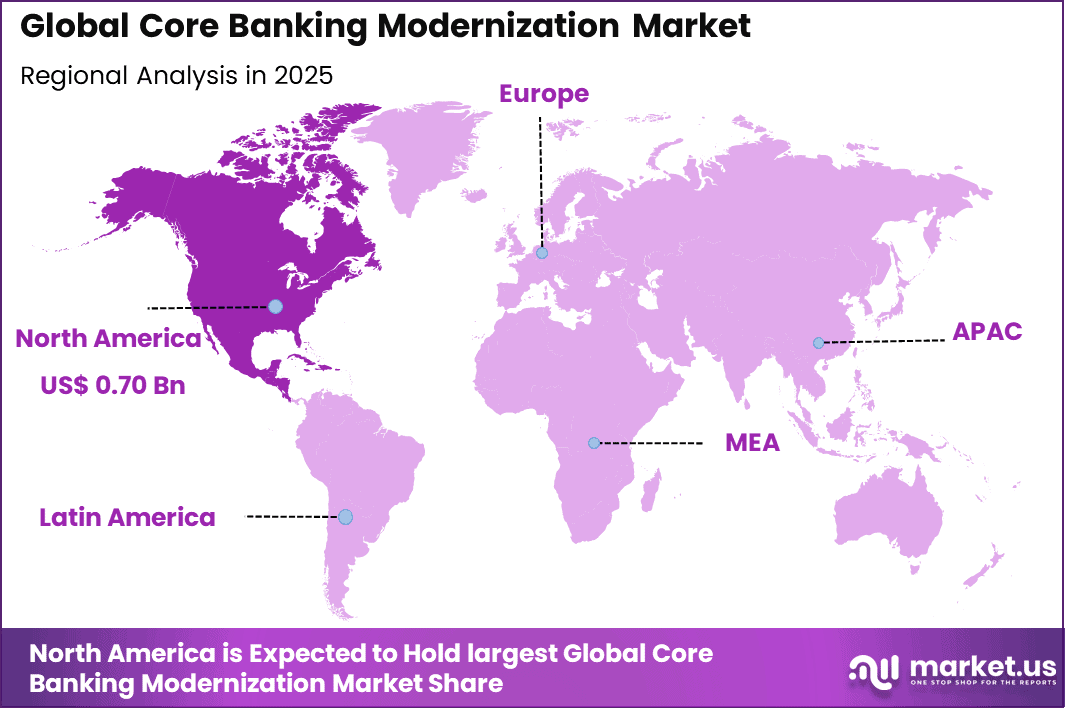

The Global Core Banking Modernization Market generated USD 1.9 billion in 2025 and is predicted to register growth from USD 2.4 billion in 2026 to about USD 16.8 billion by 2035, recording a CAGR of 24.40% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 37.5% share, holding USD 0.70 Billion revenue.

The Core Banking Modernization Market refers to the transformation of legacy banking systems into modern, flexible, and digitally enabled core platforms. These initiatives focus on replacing or upgrading monolithic systems that manage deposits, loans, payments, and customer accounts. Modern core banking platforms support real time processing, open integration, and scalable operations. Modernization is increasingly treated as a strategic necessity rather than a technology refresh.

Banks rely on core systems as the foundation of all financial products and customer interactions. Legacy cores often limit speed, product innovation, and integration with digital channels. Industry observations indicate that more than 60% of banks operate on systems that are over two decades old. This aging infrastructure has become a critical constraint on competitiveness and operational efficiency.

One of the primary drivers of core banking modernization is rising customer demand for real time and digital first banking services. Customers expect instant payments, immediate account updates, and seamless omnichannel experiences. Legacy systems designed for batch processing struggle to meet these expectations. Modern cores enable continuous processing and faster service delivery.

Demand for core banking modernization is strongest among mid to large banks facing technology constraints. These institutions manage high transaction volumes and complex product portfolios. Internal banking studies show that legacy core maintenance can consume more than 70% of annual IT budgets. This cost imbalance drives demand for more efficient platforms.

Top Market Takeaways

- By component, solutions account for 63.8% of the market, encompassing platforms for real-time processing, API integration, and legacy system upgrades.

- By deployment mode, cloud-based systems represent 57.2%, favored for scalability, agility, and reduced infrastructure costs in dynamic banking environments.

- By organization size, large enterprises hold 71.6% share, investing heavily in modernization to handle massive transaction volumes and regulatory demands.

- By modernization type, incremental modernization captures 48.7%, allowing phased transitions from legacy core systems without full disruptions.

- By end-user, banks command 78.5%, driven by needs for digital transformation, open banking compliance, and enhanced customer experiences.

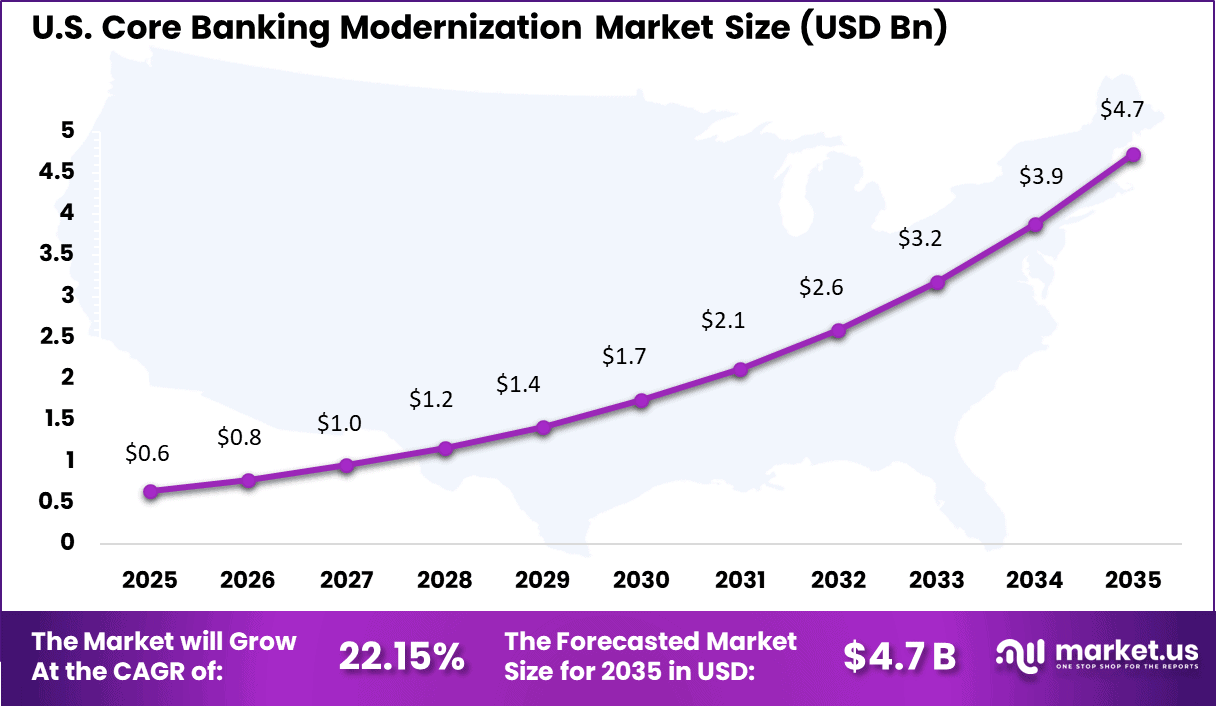

- By region, North America leads with 37.5% of the global market, where the U.S. is valued at USD 0.64 billion with a projected CAGR of 22.15%, fueled by FinTech innovation and competitive pressures.

Key Market Insights

- Market growth is strongly influenced by North America, which held a 42.2% share of the core banking software market in 2025, supported by early adoption of cloud and digital banking platforms.

- The shift toward SaaS based core systems is driven by demand for flexible and cloud ready architectures, with large banks accounting for 30.66% of market share and corporate banking representing 27.14%.

- Banks typically allocate between 15% and 20% of their total IT budgets to core system maintenance, highlighting the cost intensity of legacy platforms.

- Modernization initiatives remain challenging, as 60% of banks report cost related difficulties, 73% face rising maintenance expenses, and 63% experience concerns around system resilience.

- Core system modernization can deliver strong financial benefits, with some projects reducing technical debt and saving over 50% of the original budget through efficient code conversion.

- Modernized core platforms have been shown to improve return on equity by 8.3% points, reflecting gains in operational efficiency and scalability.

- From a strategic perspective, 44% of financial institutions prioritize security within core systems, while 42% focus on enhancing customer experience through AI driven personalization.

- Progressive modernization strategies, often described as a phased or hollow core approach, are widely adopted to lower risk by replacing legacy systems gradually over 5 to 10 years.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Accelerated replacement of legacy core banking systems +6.2% North America, Europe Short to medium term Rapid growth of digital banks and fintech competition +5.4% Europe, Asia Pacific Medium term Rising demand for real-time payments and instant processing +4.8% Global Short to medium term Regulatory pressure for transparency and reporting automation +4.1% North America, Europe Medium term Expansion of Banking-as-a-Service and open banking models +3.9% North America, Asia Pacific Medium to long term Restraints Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High cost and risk associated with core system migration -4.9% Global Short to medium term Complexity of data migration from legacy platforms -4.1% Global Medium term Shortage of skilled modernization and cloud banking talent -3.6% Asia Pacific, Latin America Medium term Operational disruption concerns among large incumbent banks -3.1% North America, Europe Medium term Data security and resilience concerns during transition -2.7% Global Medium to long term By Component

Solutions account for 63.8% of overall adoption in the Core Banking Modernization Market. This dominance reflects the strong demand for end to end platforms that modernize transaction processing, customer data management, and core operations. Banks increasingly prefer solution based offerings to address multiple modernization needs within a single framework.

The shift toward solutions is also driven by the complexity of legacy core systems. Fragmented architectures limit scalability and innovation. Integrated solutions simplify system consolidation and improve operational efficiency.

Solutions further support faster product deployment and digital service expansion. Configurable modules reduce customization effort and implementation risk. These advantages continue to reinforce solutions as the leading component segment.

By Deployment Mode

Cloud based deployment represents 57.2% of total adoption in the market. Cloud platforms provide scalability and high availability, which are essential for handling fluctuating transaction volumes. Centralized infrastructure improves system resilience and disaster recovery capabilities.

The adoption of cloud deployment is also influenced by cost optimization. Banks reduce capital expenditure by avoiding heavy on premises infrastructure investments. Operating expense models offer greater financial flexibility.

Cloud environments further enable faster innovation cycles. Regular updates and feature enhancements can be deployed without service disruption. These benefits sustain cloud based deployment as the preferred modernization approach.

By Organization Size

Large enterprises account for 71.6% of market demand by organization size. Large banks operate complex product portfolios and multi channel service models. Core modernization is critical to support these operational requirements.

The scale of large enterprises increases the need for real time processing and system reliability. Legacy systems struggle to meet performance and integration demands. Modern cores enable improved efficiency and responsiveness.

Regulatory compliance also drives adoption among large institutions. Modernized systems support audit readiness and reporting accuracy. These factors maintain strong demand from large enterprises.

By Modernization Type

Incremental modernization represents 48.7% of total adoption by modernization type. Banks prefer phased upgrades to minimize operational risk and avoid large scale disruptions. Incremental approaches allow gradual transition from legacy systems. This strategy enables banks to modernize critical functions first. High impact areas such as payments and customer onboarding are prioritized.

This improves return on investment and project control. Incremental modernization also supports coexistence of old and new systems. Data migration can be managed in stages. These advantages sustain the dominance of incremental modernization.

By End User

Banks account for 78.5% of total end user demand in the Core Banking Modernization Market. Core banking systems are foundational to all banking activities, including deposits, lending, and payments. Modernization is essential to maintain service continuity. Banks face increasing pressure to deliver digital services and real time experiences.

Modern cores enable faster product launches and improved customer engagement. This strengthens the case for modernization investment. Operational resilience is another key driver. Modern systems reduce downtime and improve system stability. These factors reinforce strong adoption among banking end users.

Emerging Trends

In the Core Banking Modernization market, a clear shift is observed toward modular and API-first architectures that replace monolithic legacy systems. Financial institutions are breaking down large, tightly coupled platforms into discrete service components that can be updated independently. This architectural trend enables faster deployment of new products, smoother integration with digital channels such as mobile and online banking, and improved interoperability with third-party platforms.

Another noticeable trend is the adoption of cloud-native environments that support elastic performance during peak activity and enhance data accessibility across distributed teams. Together, these changes are promoting agility and enabling core systems to adapt more easily to evolving customer needs and regulatory requirements.

Growth Factors

A primary growth factor in this market is the pressing need for improved operational efficiency and reduced technical debt. Many institutions continue to carry the burden of decades-old systems that are costly to maintain and slow to change. Modernization efforts are being driven by the imperative to replace these burdens with flexible platforms that support automated processes, real-time transaction processing, and streamlined data workflows.

Another important growth driver is the intensifying competitive landscape, where digital-first entrants and customer expectations for seamless experiences are pushing traditional banks to modernize. Modern core systems provide a foundation for innovation in services, faster product rollouts, and improved reliability, which together enhance user satisfaction and support long-term resilience in a rapidly evolving financial ecosystem.

Investor Type Impact Analysis

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Core banking software providers Very High Medium North America, Europe Strong long-term SaaS growth Cloud and infrastructure providers Very High Medium North America Backbone of modernization programs Banks and financial institutions High Medium Global Strategic modernization investment Private equity firms Medium Medium North America, Europe Platform consolidation opportunities Venture capital investors High High North America Focus on cloud-native core platforms Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline Cloud-native and SaaS core banking platforms +6.6% Scalability and cost efficiency Global Short term Microservices and API-first architecture +5.8% Faster product innovation Global Medium term Real-time processing and event-driven systems +5.1% Instant transaction handling Global Medium term AI-driven automation for operations and compliance +4.4% Reduced operating cost North America, Europe Medium to long term Integration with open banking and payment ecosystems +3.7% Ecosystem expansion Europe, Asia Pacific Long term Key Market Segments

By Component

- Solutions

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

By Modernization Type

- Complete System Replacement

- Incremental Modernization (APIs, Microservices)

- Front-End/Channel Modernization

By End-User

- Banks

- Credit Unions

- Other Financial Institutions

Regional Analysis

North America accounts for 37.5% of the core banking modernization market, supported by the region’s early transition toward digital-first banking models. Financial institutions are modernizing legacy core systems to improve transaction speed, system resilience, and regulatory reporting efficiency. Demand is also influenced by the need to support real-time payments, open banking frameworks, and seamless integration with digital channels.

The United States market is valued at USD 0.64 Bn and is growing at a CAGR of 22.15%, reflecting strong investment in replacing aging core platforms. Adoption is driven by rising customer expectations for always-on banking services and the operational limits of legacy infrastructure. Growth is further supported by increased focus on cloud migration, modular architectures, and scalable systems that enable faster product launches and long-term cost efficiency.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

Large banking technology and enterprise software providers such as FIS, Fiserv, Inc., and Oracle Corporation lead the core banking modernization market through end-to-end transformation programs. Their solutions support legacy replacement, modular upgrades, and regulatory compliance. Strong integration with payments, risk, and digital channels improves operational continuity. SAP SE and Temenos AG strengthen adoption with scalable architectures.

IT services and platform-led modernization specialists such as Tata Consultancy Services, Ltd., Infosys, Ltd., and EdgeVerve Systems, Ltd. focus on phased modernization and migration strategies. Finastra and NCR Corporation support banks with integration, managed services, and omnichannel capabilities. These players are widely adopted by regional and tier-two banks.

Cloud-native and next-generation core providers such as Mambu GmbH, Thought Machine Group, Ltd., and Avaloq enable API-driven and real-time banking models. Backbase B.V. and Jack Henry & Associates, Inc. address digital-first and mid-market institutions. Other vendors expand innovation and regional reach, supporting steady growth in core banking modernization globally.

Top Key Players in the Market

- FIS (Fidelity National Information Services, Inc.)

- Fiserv, Inc.

- Tata Consultancy Services, Ltd.

- Infosys, Ltd.

- Oracle Corporation

- SAP SE

- Temenos AG

- Jack Henry & Associates, Inc.

- Mambu GmbH

- Finastra

- Thought Machine Group, Ltd.

- NCR Corporation

- Avaloq (a part of NEC Corporation)

- Backbase B.V.

- EdgeVerve Systems, Ltd. (an Infosys company)

- Others

Future Outlook

The future outlook for the Core Banking Modernization Market is strong as banks and financial institutions continue to update legacy systems to stay competitive. Demand for modern, flexible core banking platforms is expected to rise because these systems support digital services, real-time processing, and improved customer experience.

Adoption of cloud technology, APIs, and automation will accelerate transformation and reduce operational costs. Growth can be attributed to rising customer expectations, pressure to comply with evolving regulations, and the need for scalable, efficient banking operations. Overall, market expansion is expected as institutions prioritize innovation and resilience.

Recent Developments

- February, 2026 – Fiserv expanded its ServiceNow partnership to deploy Now Assist generative AI across IT and customer service starting Q1 2026, aiming to modernize operations for banks and credit unions handling legacy workflows.

- December, 2025 – British Caribbean Bank completed its go‑live on Finastra’s Essence cloud‑native core platform after a 1.5‑year migration, enabling rapid product rollouts and lower IT overhead for regional growth.

Report Scope

Report Features Description Market Value (2025) USD 1.9 Billion Forecast Revenue (2035) USD 16.8 Billion CAGR(2025-2035) 24.40% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Solutions, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), By Modernization Type (Complete System Replacement, Incremental Modernization (APIs, Microservices), Front-End/Channel Modernization), By End-User (Banks, Credit Unions, Other Financial Institutions) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape FIS (Fidelity National Information Services, Inc.), Fiserv, Inc., Tata Consultancy Services, Ltd., Infosys, Ltd., Oracle Corporation, SAP SE, Temenos AG, Jack Henry & Associates, Inc., Mambu GmbH, Finastra, Thought Machine Group, Ltd., NCR Corporation, Avaloq (a part of NEC Corporation), Backbase B.V., EdgeVerve Systems, Ltd. (an Infosys company), Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Core Banking Modernization MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Core Banking Modernization MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- FIS (Fidelity National Information Services, Inc.)

- Fiserv, Inc.

- Tata Consultancy Services, Ltd.

- Infosys, Ltd.

- Oracle Corporation

- SAP SE

- Temenos AG

- Jack Henry & Associates, Inc.

- Mambu GmbH

- Finastra

- Thought Machine Group, Ltd.

- NCR Corporation

- Avaloq (a part of NEC Corporation)

- Backbase B.V.

- EdgeVerve Systems, Ltd. (an Infosys company)

- Others

Our Clients

- 176739

- Feb. 2026