Global Conductive Silicone Rubber Market Size, Share Analysis Report By Product (Thermally Conductive, Electrically Conductive, Others), By Application (Automotive And Transportation, Electrical And Electronics, Industrial Machines, Packaging, Construction, Food And Beverage, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 177746

- Number of Pages: 324

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

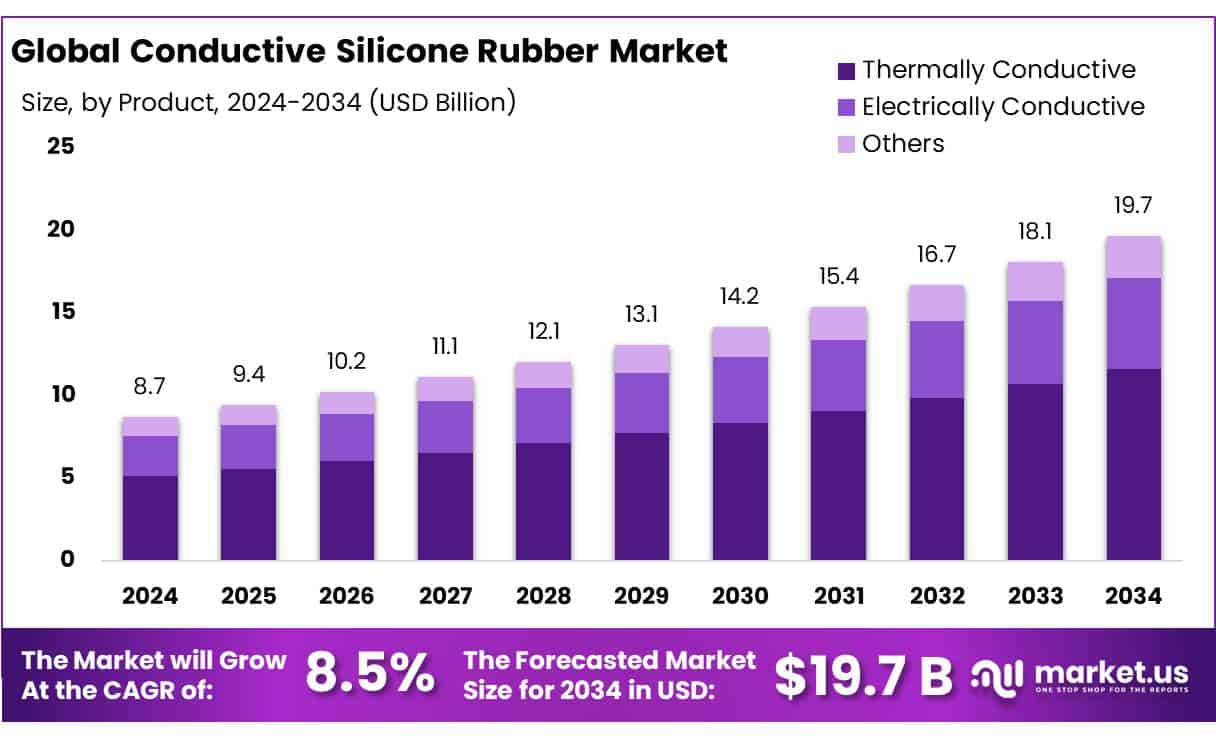

The Global Conductive Silicone Rubber Market is expected to be worth around USD 19.7 Billion by 2034, up from USD 8.7 Billion in 2024, and is projected to grow at a CAGR of 8.5% from 2025 to 2034. The Asia Pacific segment maintained 43.5%, supporting a Psychedelic Mushrooms value of USD 3.7 Bn.

Conductive silicone rubber is a modified silicone elastomer filled with conductive media to deliver controlled electrical conductivity while retaining silicone’s heat stability, flexibility, and weather resistance. In industrial systems, it is selected where electrical continuity and sealing must coexist—for example, EMI shielding gaskets for enclosures, conductive keypads and connectors, static-dissipative seals around sensitive electronics, and thermal/electrical interface pads used to manage both heat and grounding. Market tracking also reflects this broad adoption, with one widely cited estimate placing the conductive silicone rubber market at USD 8.84 billion in 2024.

Industrial demand is being pulled by electronics scale-up and electrification. The semiconductor cycle is a clear proxy for downstream electronics intensity: global semiconductor sales reached US$791.7 billion in 2025, up 25.6% year-on-year, reflecting strong demand from AI, cloud infrastructure, and advanced electronics that typically require tighter electromagnetic compatibility and more robust shielding/grounding materials.

At the same time, electric mobility expands CSR’s use in battery packs, power electronics enclosures, charging interfaces, and high-voltage connectors; the IEA reports electric car sales exceeded 17 million in 2024 and crossed 20% of global car sales, reinforcing a large addressable base for conductive sealing and shielding in EV platforms.

Government initiatives amplify this trajectory by encouraging domestic electronics capacity and higher compliance standards: the European Commission notes the Chips Act is backed by more than €43 billion in policy-driven investment support through 2030, while India’s Semicon India programme carries a financial outlay of ₹76,000 crore aimed at building a sustainable semiconductor and display ecosystem.

CSR also benefits from “clean and compliant” industrial requirements, including food processing, where silicone’s cleanability and thermal stability are valued for seals and gaskets. In regulated food-contact applications, U.S. rules for rubber articles intended for repeated food contact specify extraction limits such as ≤175 mg/in² total extractives in the first 7 hours (n-hexane reflux) and ≤4 mg/in² in the succeeding 2 hours, pushing processors toward higher-quality, better-controlled elastomer formulations and traceable compliance documentation.

Key Takeaways

- Conductive Silicone Rubber Market is expected to be worth around USD 19.7 Billion by 2034, up from USD 8.7 Billion in 2024, and is projected to grow at a CAGR of 8.5%.

- Thermally Conductive held a dominant market position, capturing more than a 59.8% share.

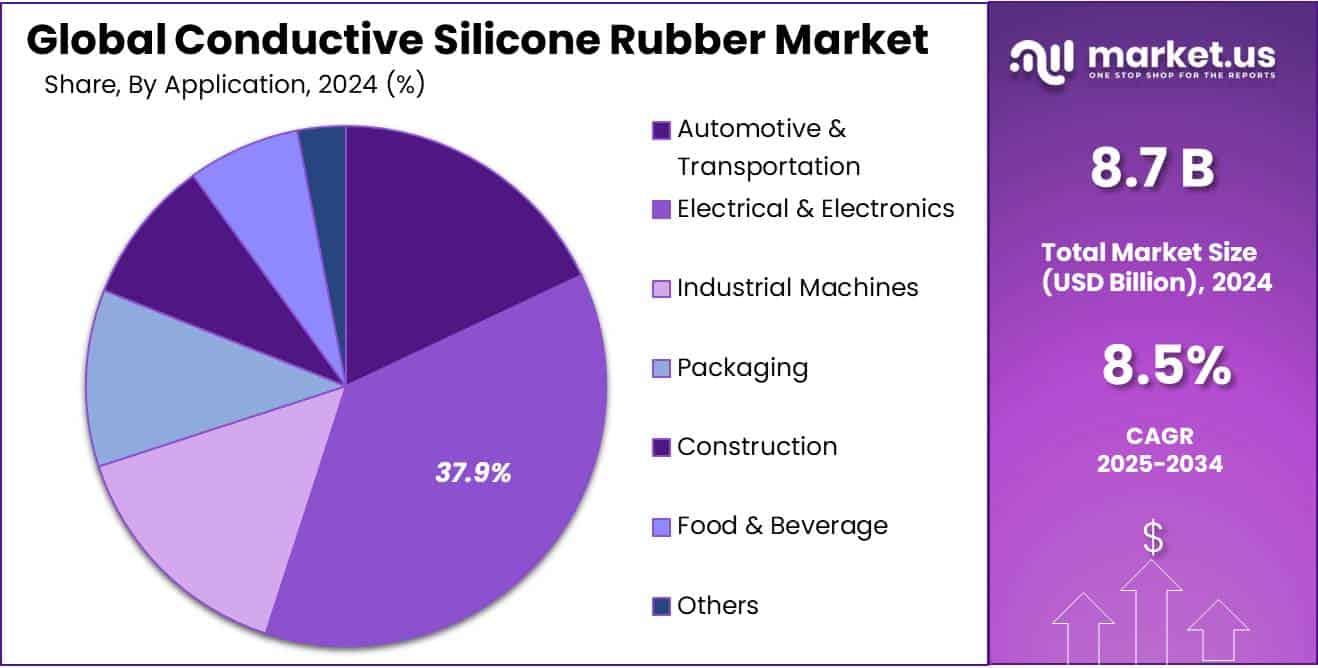

- Electrical & Electronics held a dominant market position, capturing more than a 37.9% share.

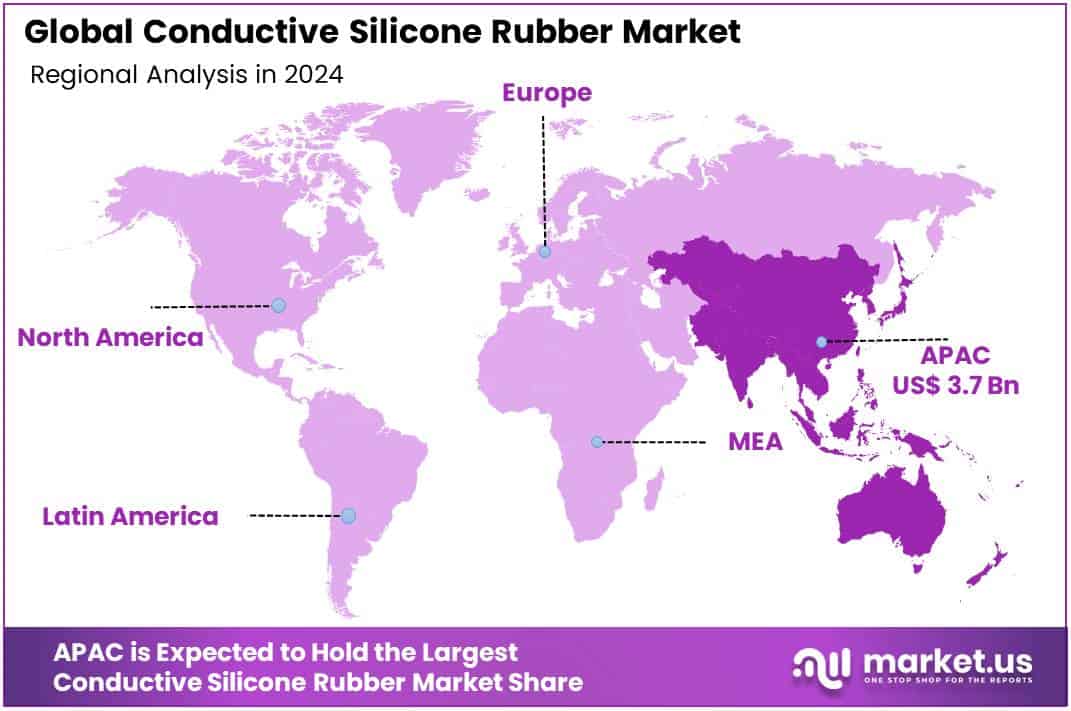

- Asia Pacific remains the dominating region in the Conductive Silicone Rubber market, accounting for 43.5% share and reaching $3.7 Bn.

By Product Analysis

Thermally Conductive leads strongly with 59.8% share, driven by rising heat management needs across electronics and EV systems

In 2024, Thermally Conductive held a dominant market position, capturing more than a 59.8% share. This strong performance reflects the growing need for advanced heat dissipation solutions across industries where compact electronics and high-power systems are becoming standard. As devices continue to shrink in size while delivering higher output, managing internal heat has become critical to maintaining performance and extending product life. Thermally conductive silicone rubber is widely preferred because it combines flexibility, sealing capability, and stable thermal conductivity in demanding environments.

By Application Analysis

Electrical & Electronics takes the lead with 37.9% share, backed by rising device complexity and shielding needs

In 2024, Electrical & Electronics held a dominant market position, capturing more than a 37.9% share. This leadership reflects the expanding demand for reliable materials that can provide both electrical conductivity and environmental sealing in compact electronic systems. As modern devices become smaller and more powerful, the need to manage electromagnetic interference, ensure grounding, and protect sensitive components has intensified. Conductive silicone rubber has become a preferred solution in this space because it combines flexibility, durability, and stable electrical performance under varying temperatures.

Key Market Segments

By Product

- Thermally Conductive

- Electrically Conductive

- Others

By Application

- Automotive & Transportation

- Electrical & Electronics

- Industrial Machines

- Packaging

- Construction

- Food & Beverage

- Others

Emerging Trends

Hybrid “seal + shield + heat” parts are becoming the go-to choice in smart food factories

A major latest trend in conductive silicone rubber is the shift toward multi-function compounds that do more than just conduct—especially parts that can seal against water/chemicals, block EMI, reduce ESD risk, and also manage heat in one gasket, pad, or molded interface. This trend is showing up clearly in food processing and packaging plants, where factories are adding more electronics but still operate in tough conditions like washdowns, vibration, temperature swings, and constant run time. Instead of using separate components for sealing and shielding, equipment builders increasingly prefer a single engineered elastomer part that simplifies assembly and reduces failure points. Conductive silicone rubber is well-suited for this because it stays flexible and stable while maintaining a conductive path across a flange, door, connector, or enclosure seam.

Food organizations are a strong proof point for why this “multi-function” approach is taking off. Nestlé reported CHF 91.4 billion in sales in 2024, reflecting a very large global production footprint where even small improvements in uptime and maintenance speed have big value. PepsiCo reports nearly $92 billion in net revenue in 2024, and notes its products are enjoyed more than one billion times a day across more than 200 countries and territories—a scale that helps explain why packaging and processing lines are being upgraded continuously, not occasionally.

Regulation is also nudging factories toward more connected hardware, which supports this trend. FDA’s FSMA Food Traceability Rule work includes a referenced date of July 20, 2028 tied to FDA’s intention not to enforce the rule before that date, following congressional direction. Even with that runway, many companies are already installing scanning points, data capture systems, and upgraded control cabinets. As more electronics are added near wet or dusty zones, the need for gaskets that seal reliably while maintaining consistent conductivity becomes a practical requirement.

Drivers

Food factories going digital is a quiet but powerful demand driver for conductive silicone rubber

One major driving factor for conductive silicone rubber is the fast shift toward more electronics inside food processing and packaging plants—and the need to keep those electronics reliable in wet, vibration-heavy, and high-throughput environments. Large food manufacturers run enormous, always-on operations, and even small improvements in uptime or product protection justify upgrades in automation, sensing, and connected controls.

That matters because every extra control panel, sensor node, inspection camera, VFD cabinet, or smart conveyor adds more enclosures, connectors, and interfaces that must be sealed against moisture and washdown while also handling grounding, antistatic (ESD) protection, and EMI shielding. Conductive silicone rubber fits this exact job: it behaves like a robust gasket and, at the same time, creates a stable conductive path where electronics need protection from interference or static build-up.

The scale of the food industry helps explain why this electronics build-out is continuous rather than cyclical. Nestlé reported CHF 91.4 billion in sales for 2024, showing how large global packaged food production remains and how much capital is available for plant modernization across multiple regions. PepsiCo states it generated nearly $92 billion in net revenue in 2024, and that its products are enjoyed more than one billion times a day in 200+ countries and territories—an indicator of the sheer volume moving through manufacturing, warehousing, and packaging networks that depend on reliable electronics and automation.

Regulation is amplifying this shift because compliance increasingly depends on data capture and electronic recordkeeping, not manual logs. In the U.S., FDA communication around the FSMA Food Traceability Rule highlights a move toward extended enforcement timing, referencing July 20, 2028 as the date FDA intends not to enforce prior to, based on congressional direction.

Restraints

High conductive-filler cost and price swings make adoption harder in cost-sensitive food manufacturing

One major restraining factor for conductive silicone rubber is the high and volatile cost of conductive fillers, especially for grades that rely on precious-metal pathways to hit low resistance targets. In real procurement terms, buyers are not just paying for silicone chemistry—they are paying for a formulation where the conductive fraction can dominate the bill of materials. That becomes a hurdle when plant teams compare a conductive gasket or seal against lower-cost non-conductive elastomers plus “good enough” grounding workarounds, particularly for large enclosures and long sealing runs used around food processing and packaging lines.

This cost pressure is made worse when metals move sharply year to year. Silver’s annual average price shows the kind of swing that makes long-term contracting difficult: 2024 averaged $28.46/oz, while 2025 averaged $40.11/oz on the same historical series—an increase that can ripple straight into conductive compound pricing and lead to redesigns or delayed approvals. Even when buyers are convinced on performance, many prefer to re-qualify lower-loading designs, shift to alternative shielding approaches, or reserve conductive silicone only for “must-have” interfaces (connector flanges, door gaskets on sensitive cabinets) rather than rolling it out plant-wide.

Food manufacturers feel this squeeze because their capital decisions are made under constant margin and input-cost scrutiny. Nestlé’s 2024 underlying trading operating profit margin was 17.2%, which is strong for the sector, but it still signals that efficiency and cost discipline remain central when approving plant upgrades. PepsiCo also emphasizes the reality of commodity inflation; in its full-year 2024 materials, it notes pressures from higher commodity costs across inputs such as grains and packaging, highlighting how quickly costs can shift and force reprioritization.

Regulatory timing can also slow purchasing decisions, even when regulation ultimately supports digitization. For example, FDA communication on the FSMA Food Traceability Rule explains that FDA intends not to enforce the rule before July 20, 2028, following congressional direction.

Opportunity

Traceability-driven “smart food” factories are opening a big runway for conductive sealing and shielding

One major growth opportunity for conductive silicone rubber is the multi-year upgrade cycle in food processing and packaging, where companies are adding more electronics for traceability, inspection, and connected automation—and they need those electronics to survive washdowns, vibration, and electrical noise. Conductive silicone rubber sits in a sweet spot here because it can act like a dependable seal while also providing grounding, EMI shielding, and ESD control at the same interface. As more food lines move from basic panels to sensor-rich, data-logged operations, the number of doors, ports, and cable entries that must be both sealed and electrically “clean” rises quickly.

The scale of leading food organizations shows why this opportunity is durable rather than a short-term spike. Nestlé reported CHF 91.4 billion in sales in 2024, reflecting a huge global production base where even incremental automation upgrades translate into thousands of retrofits and new line builds. PepsiCo states it generated nearly $92 billion in net revenue in 2024, and its products are enjoyed more than one billion times a day in 200+ countries and territories—a simple way to understand how many factories and packaging sites are under constant pressure to run faster, safer, and with fewer stoppages.

Regulatory and customer requirements make the modernization wave more predictable, which is why it looks like an opportunity. In the U.S., FDA states it intends not to enforce the Food Traceability Rule prior to July 20, 2028, following congressional direction. That date matters because it effectively creates a runway for companies to phase in hardware and software upgrades—labeling, scanning points, data capture at critical steps, and more connected devices at the line level.

Government manufacturing initiatives also support the opportunity indirectly by expanding the availability of electronics used in industrial equipment. India’s Union Budget FY 2026–27 increased the outlay for the Electronics Components Manufacturing Scheme to ₹40,000 crore, signaling a strong push to scale electronics component capacity. More local electronics output generally means more competitive pricing and faster supply of sensors, control hardware, and enclosures—exactly the equipment base where conductive silicone rubber is specified for conductive gaskets, keypad mats, and grounded seals.

Regional Insights

Asia Pacific dominates at 43.5% share ($3.7 Bn), powered by electronics manufacturing depth and fast EV scale-up

Asia Pacific remains the dominating region in the Conductive Silicone Rubber market, accounting for 43.5% share and reaching $3.7 Bn, supported by the region’s unmatched concentration of electronics assembly, component ecosystems, and high-volume industrial production. The demand base is strengthened by the fact that Asia Pacific is widely recognized as the largest regional semiconductor market, keeping downstream requirements strong for EMI shielding, grounding, and ESD-safe sealing used in devices, connectors, enclosures, and automation hardware.

In 2024–2025, the region’s momentum is closely tied to the growth of electrification and power electronics, where conductive elastomers are used in gaskets and seals around sensitive control systems. The International Energy Agency notes electric-car sales growth into 2025, with more than 4 million electric cars sold globally in Q1 2025 and about 60% of those sold in China—illustrating how concentrated EV-related electronics demand is within Asia Pacific.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Saint-Gobain participates through engineered materials and industrial solutions where elastomers and performance components are specified for protection, durability, and compliance. In 2024, the group reported €46.6 billion in sales and employed more than 161,000 people. It also delivered €5.30 billion operating income and €2.05 billion in capital expenditure, reflecting continued investment in manufacturing and process capability—important for customers seeking consistent quality and high-throughput supply for sealing and shielding applications.

WACKER is a major silicone producer, and its silicones portfolio is closely aligned with conductive silicone rubber value chains (base polymers, specialty silicone materials, and industrial-grade formulations). In 2024, WACKER posted €5.7 billion in total sales and €763 million EBITDA, with 16,637 employees. The Silicones division generated €2,805 million in sales in 2024 (up from €2.74 billion in 2023), showing resilience in specialty mix.

Western Rubbers (India) serves industrial sealing and rubber component demand where conductive elastomers can be used for antistatic interfaces and grounded sealing in equipment. Financial tracking sources report revenue of ₹17.3 crore for the financial year ending March 31, 2024. Company datasets also list an estimated 125 employees and $7.8 million revenue (profile-based), which signals a mid-sized operation supporting customized rubber part supply.

Top Key Players Outlook

- Dow

- Saint-Gobain

- Wacker Chemie AG

- Western Rubbers

- Western Polyrub India Pvt. Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Specialty Silicone Products, Inc.

- KCC CORPORATION

- Reiss Manufacturing, Inc.

- MESGO S.p.A.

- Jan Huei K.H. Industry Co., Ltd.

Recent Industry Developments

In 2024, Dow delivered approximately $43 billion in sales globally and continues to invest in materials that combine mechanical reliability with electrical performance for advanced manufacturing environments.

WACKER reported €5.72 billion in total sales in 2024, and its Silicones segment alone delivered €2.81 billion in 2024 sales (up from €2.74 billion in 2023), helped by a better specialty mix—important because specialty silicone materials are where conductive and performance-driven elastomer formulations typically sit.

Report Scope

Report Features Description Market Value (2024) USD 8.7 Bn Forecast Revenue (2034) USD 19.7 Bn CAGR (2025-2034) 8.5% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Thermally Conductive, Electrically Conductive, Others), By Application (Automotive And Transportation, Electrical And Electronics, Industrial Machines, Packaging, Construction, Food And Beverage, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Dow, Saint-Gobain, Wacker Chemie AG, Western Rubbers, Western Polyrub India Pvt. Ltd., Shin-Etsu Chemical Co., Ltd., Specialty Silicone Products, Inc., KCC CORPORATION, Reiss Manufacturing, Inc., MESGO S.p.A., Jan Huei K.H. Industry Co., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Conductive Silicone Rubber MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Conductive Silicone Rubber MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Dow

- Saint-Gobain

- Wacker Chemie AG

- Western Rubbers

- Western Polyrub India Pvt. Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Specialty Silicone Products, Inc.

- KCC CORPORATION

- Reiss Manufacturing, Inc.

- MESGO S.p.A.

- Jan Huei K.H. Industry Co., Ltd.

Our Clients

- 177746

- Feb 2026