Global Carrier Billing Market By Content Type (Gaming, Video-on-Demand / OTT, Music and Audio Streaming), By Device Platform (Android Smartphones, iOS /iPadOS Devices), By Payment Flow (One-off (event-based), Subscription / Recurring), By Operator Type (Mobile Network Operators (MNOs), Mobile Virtual Network Operators (MVNOs)), By End-User Segment (Banked Consumers, Unbanked / Under-banked Consumers), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 175605

- Number of Pages: 224

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Key Insights

- Content Type Analysis

- Device Platform Analysis

- Payment Flow Analysis

- Operator Type Analysis

- End-User Segment Analysis

- Key Reasons for Adoption

- Benefits

- Usage

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

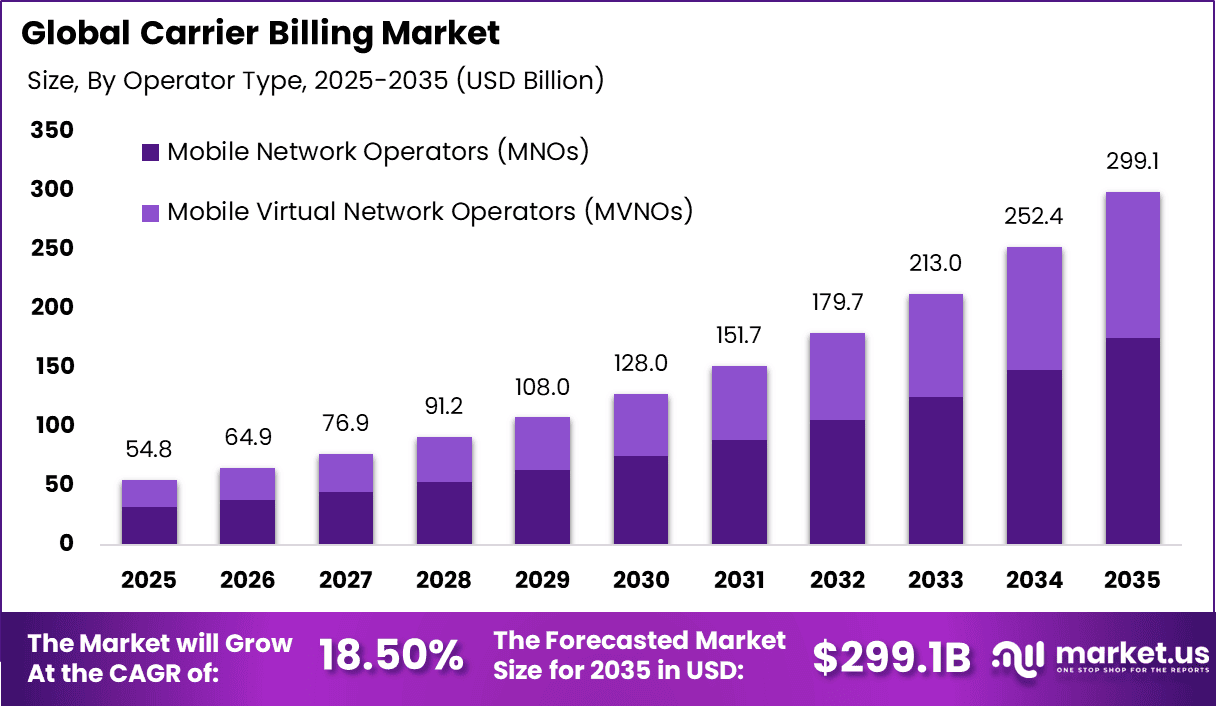

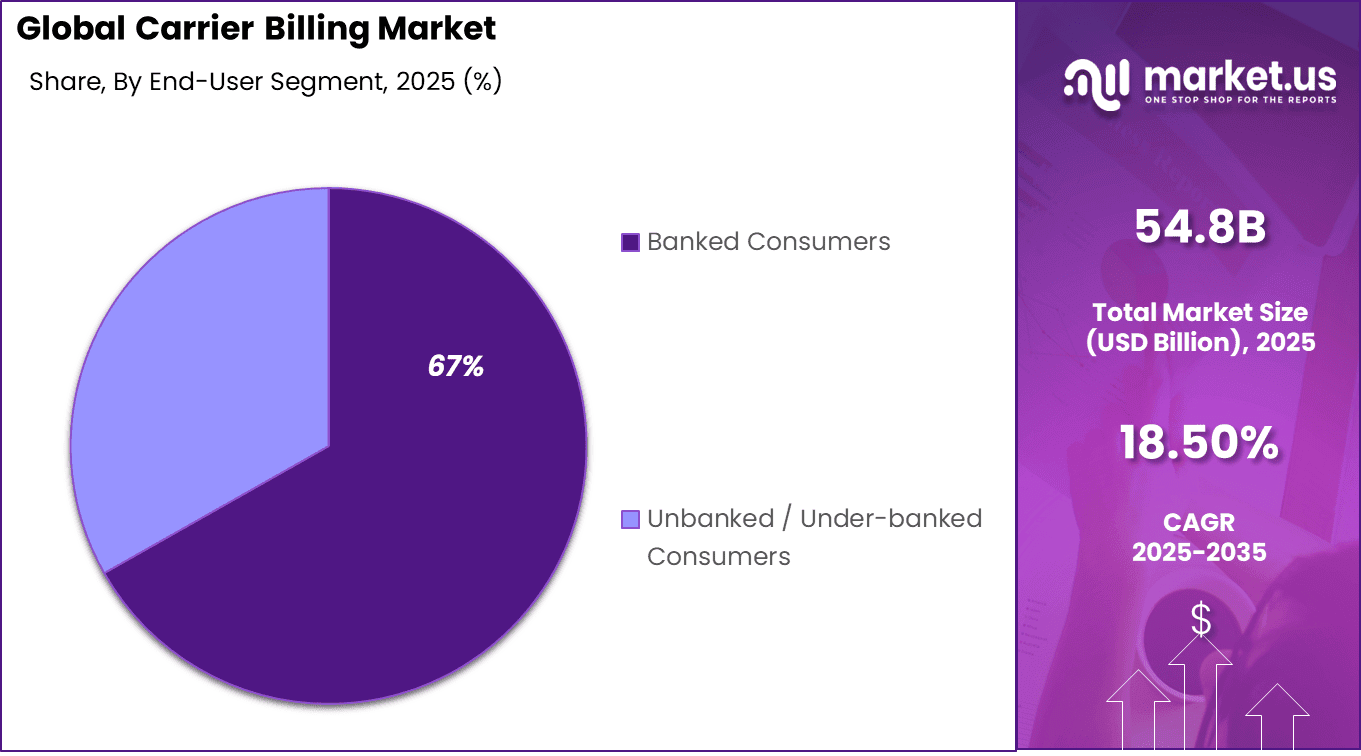

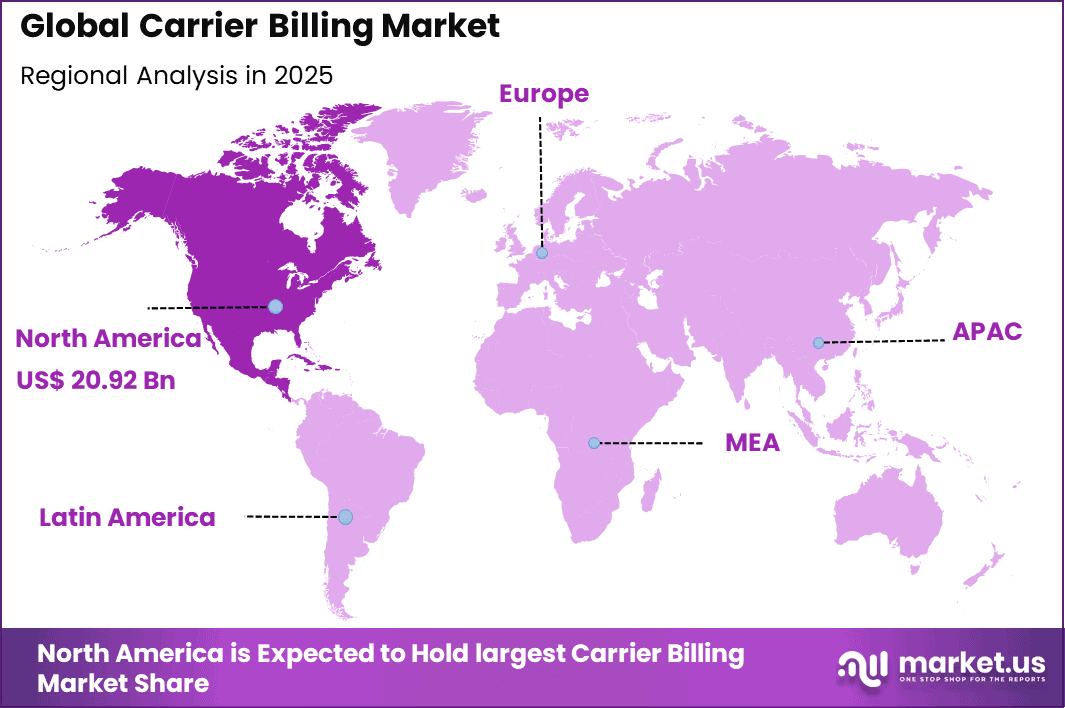

The Global Carrier Billing Market generated USD 54.8 billion in 2025 and is predicted to register growth from USD 64.9 billion in 2026 to about USD 299.1 billion by 2035, recording a CAGR of 18.50% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 38.2% share, holding USD 20.92 Billion revenue.

The Carrier Billing Market refers to payment solutions that allow users to charge digital purchases directly to their mobile phone bill or prepaid balance. This model enables consumers to pay for digital content, subscriptions, apps, games, tickets, and services without using credit or debit cards. Carrier billing is widely used in mobile first economies where card penetration is limited. The market has gained importance as mobile devices become primary transaction tools.

Carrier billing operates through partnerships between mobile network operators and digital merchants. Payments are authorized via the mobile network, simplifying checkout processes. Industry observations indicate that more than 45% of mobile users in emerging markets prefer carrier billing for small value digital transactions. This preference supports continued relevance of the market.

One of the main driving factors is low access to traditional banking and card based payment methods in many regions. Large populations rely on mobile phones as their primary financial interface. Carrier billing removes the need for bank accounts or cards. This accessibility drives adoption among unbanked and underbanked users.

Demand for carrier billing is strong in digital content markets such as gaming, video streaming, and music services. These sectors rely on microtransactions and recurring subscriptions. Studies show that checkout abandonment can drop by more than 20% when carrier billing is offered as a payment option. This performance benefit encourages merchant adoption.

Investment opportunities in the carrier billing market exist in platforms that support cross operator and cross region billing. Aggregation services that connect multiple networks offer higher value to global merchants. Investors favor scalable platforms with broad operator coverage. This aggregation model supports long term expansion.

There are also opportunities in value added services layered on carrier billing. Subscription management and fraud analytics enhance platform differentiation. These services increase revenue per transaction. Innovation beyond basic billing attracts sustained investment interest.

Top Market Takeaways

- By content type, gaming led the carrier billing market with 40.4% share, monetizing in-app purchases and microtransactions directly through mobile carriers.

- By device platform, Android smartphones captured 48.3%, dominating due to widespread adoption and seamless integration with carrier networks.

- By payment flow, subscription/recurring payments held 64.4%, supporting ongoing services like streaming and premium content access.

- By operator type, mobile network operators (MNOs) accounted for 58.7%, leveraging their billing infrastructure for frictionless transactions.

- By end-user segment, banked consumers dominated at 66.8%, preferring carrier billing for convenience despite having traditional banking options.

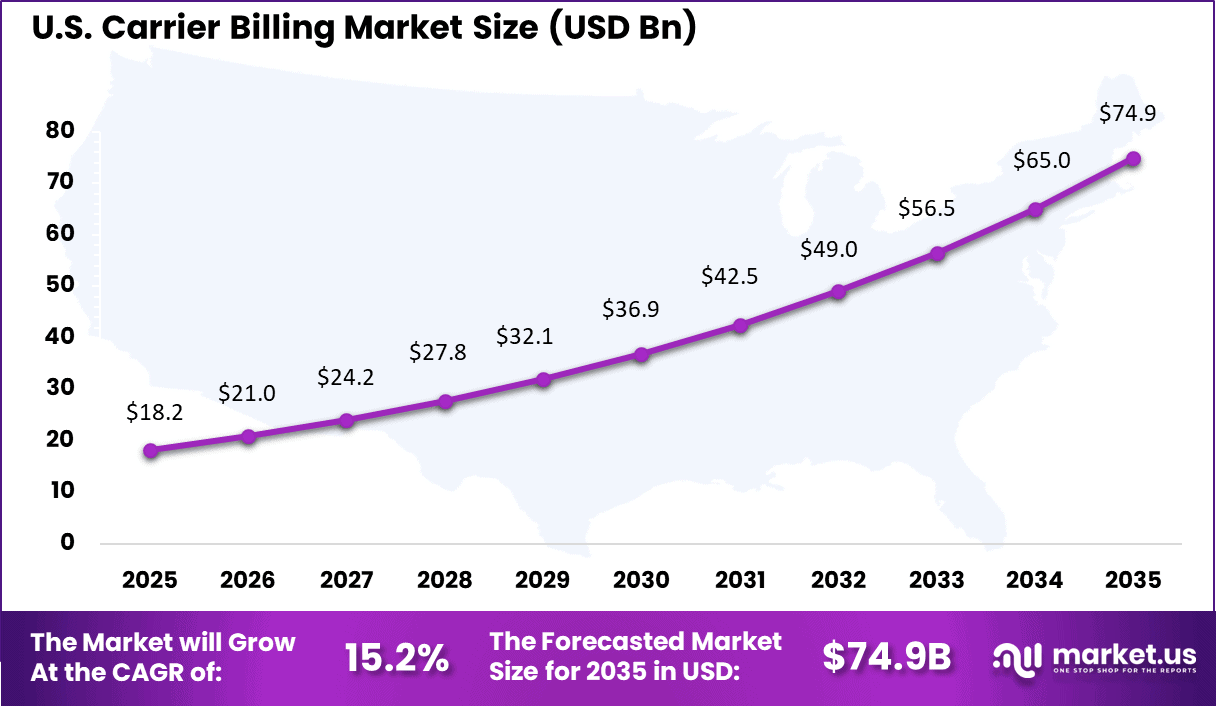

- North America represented 38.2% of the global market, with the U.S. valued at USD 18.20 billion and growing at a CAGR of 15.2%.

Key Insights

Platform and User Demographics

- Operating system: Android leads the market with about 72% to 76% share in 2024, mainly due to wide use in emerging markets and support across many devices.

- Financial inclusion: Unbanked users made up 58% of total Direct Carrier Billing usage in 2024, showing its importance in regions where credit card access is limited.

- Transaction value: Average transaction amounts differ by region, ranging from USD 5.96 in Western Europe to USD 1.48 in Latin America, reflecting differences in income levels and spending habits.

Content Type Analysis

By content type, gaming accounted for 40.4% of usage. Mobile games rely heavily on in app purchases and downloadable content. Carrier billing supports impulse purchases by reducing payment steps. This improves conversion rates for game publishers.

Gaming platforms benefit from higher completion rates compared to card based payments. Users can make purchases without leaving the game environment. This creates a smoother experience and supports monetization. As mobile gaming expands, carrier billing remains closely tied to this segment.

Live events and seasonal game content further increase transaction volumes. Limited time offers drive quick purchasing decisions. Carrier billing supports these dynamics effectively. Gaming continues to be the leading content category.

Device Platform Analysis

By device platform, Android smartphones represented 48.3% of adoption. Android devices dominate global smartphone volumes. This provides a large user base for carrier billing integration. App stores and developers prioritize Android compatibility. Android platforms offer flexible payment APIs. This simplifies integration for content providers.

Carrier billing is often enabled by default in many regions. This has supported consistent usage growth. Emerging markets also contribute to Android dominance. Many users rely on mobile billing instead of cards. This reinforces Android as the primary platform for carrier billing transactions.

Payment Flow Analysis

Subscription and recurring payments account for 64.4% of the carrier billing market, indicating strong usage for ongoing digital services. This includes gaming passes, streaming services, and premium content subscriptions. Carrier billing simplifies recurring payments by automating charges through mobile accounts, reducing payment failures.

For service providers, recurring billing improves revenue predictability and customer retention. Users benefit from convenience and uninterrupted access to services. The strong dominance of this segment reflects growing demand for subscription-based digital content supported by simple and reliable payment flows.

Operator Type Analysis

Mobile network operators account for 58.7% of the operator type segment, making them the primary facilitators of carrier billing services. MNOs provide the billing infrastructure and customer relationships needed to support direct carrier payments. They enable seamless integration between content providers and end users.

From a market structure view, MNO involvement ensures wide reach and trusted billing mechanisms. Operators also benefit from revenue sharing and increased service usage. The strong presence of this segment reflects the central role of MNOs in enabling and scaling carrier billing ecosystems.

End-User Segment Analysis

Banked consumers represent 67% of the end-user segment, showing that carrier billing is widely used even among users with access to traditional banking. These users value carrier billing for convenience and speed, especially for low-value digital purchases. The ability to avoid card entry supports faster transactions.

From a behavior perspective, banked consumers use carrier billing as an alternative rather than a replacement for cards. It is often preferred for digital content and subscriptions. The strong share of this segment reflects consumer preference for simple and trusted payment options within mobile environments.

Key Reasons for Adoption

- Mobile phone usage is widespread, enabling payments through existing subscriber accounts

- Consumers seek simple payment methods without sharing card or bank details

- Digital content providers need higher conversion rates for small-value transactions

- Financial inclusion goals are supported by reaching users without bank access

- Telecom operators are expanding digital service offerings beyond connectivity

Benefits

- Payment convenience is improved through direct billing to mobile accounts

- Transaction completion rates are increased with fewer payment steps

- User security is strengthened by avoiding card or bank data entry

- Revenue opportunities are expanded for telecom operators and merchants

- Access to digital services is broadened for underbanked users

Usage

- Used for purchasing digital content such as games, music, and videos

- Applied in subscription services for recurring digital payments

- Deployed in app stores for in-app purchases

- Utilized in online services offering low-value digital transactions

- Integrated with mobile networks for seamless billing and settlement

Emerging Trends

Key Trend Description Expansion beyond digital content Carrier billing moves from games and streaming into physical goods, transport, and utilities. Integration with wallets and super apps Carrier billing is embedded inside wallets and super apps as one of several payment options. Subscription and recurring billing focus Platforms support sophisticated recurring models for OTT, gaming, and SaaS services. 5G and IoT payment use cases Connected devices such as wearables, TVs, and cars initiate carrier-billed micro-payments. Enhanced risk and compliance controls Stronger KYC, spending controls, and dispute tools reduce fraud and regulatory risk. Growth Factors

Key Factors Description Rising smartphone and data usage Growing mobile internet adoption directly increases the addressable base for carrier billing. Low card and bank penetration In many markets, unbanked and underbanked users rely on carrier billing as their primary online payment method. Surge in digital content consumption Growth in mobile gaming, video streaming, and in-app purchases drives transaction volumes. Demand for frictionless checkout One-tap payment on the phone bill reduces friction and boosts conversion for merchants. Telco-merchant partnerships Bundled offers and revenue-share models between operators and content providers expand use cases and reach. Key Market Segments

By Content Type

- Gaming

- Video-on-Demand / OTT

- Music and Audio Streaming

- ePublishing (e‑books, comics, news)

- Ticketing and Transit

- Cloud & Utility Software

By Device Platform

- Android Smartphones

- iOS / iPadOS Devices

- Feature-phones

- Connected TVs & Game Consoles

By Payment Flow

- One-off (event-based)

- Subscription / Recurring

By Operator Type

- Mobile Network Operators (MNOs)

- Mobile Virtual Network Operators (MVNOs)

By End-User Segment

- Banked Consumers

- Unbanked / Under-banked Consumers

Regional Analysis

North America accounted for 38.2% share, supported by high smartphone penetration and strong consumption of digital content and subscription based services. Carrier billing has been widely adopted to simplify payments for digital media, gaming, streaming, and app based services by allowing charges to be added directly to mobile bills.

Demand has been driven by consumer preference for convenient payment methods that do not require cards or bank details. The region’s mature telecom infrastructure and strong partnerships between mobile operators and content providers have reinforced steady adoption.

The U.S. market reached USD 18.20 Bn and is projected to grow at a 15.2% CAGR, reflecting strong demand from digital content providers, gaming platforms, and app developers. Adoption has been driven by the need to reduce payment friction and reach a wider customer base. Carrier billing has helped U.S. businesses increase user acquisition and support impulse purchases with minimal checkout steps.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver Analysis

Growth in Digital Content and Mobile Usage

A primary driver for the carrier billing market is the rising consumption of digital content and the increasing reliance on mobile devices for purchasing services. Consumers are spending more on games, video streaming, in-app purchases, and subscriptions through their smartphones, and carrier billing allows these transactions to be charged directly to their mobile phone accounts.

This payment option simplifies checkout and matches user behaviour in markets where mobile commerce is dominant, making it an appealing choice for both consumers and content providers. In regions with strong mobile penetration and growing demand for digital services, this trend supports broader adoption of carrier billing as an alternative to traditional credit card or bank payments.

Merchants and telecom partners see value in offering quick, familiar ways for users to pay for content and services without the need for separate registration or banking credentials. As a result, more players in the payments ecosystem are integrating carrier billing to capture mobile-first spending.

Restraint Analysis

Regulatory Variations and High Transaction Fees

A significant restraint on the carrier billing market relates to regulatory differences and the cost structure associated with the service. Regulations and compliance requirements vary across countries, creating complexities for service providers that must adjust their offerings to meet local legal frameworks. This uneven regulatory environment can slow roll-out and limit uniform solutions across markets.

High transaction fees charged by mobile operators also present a challenge for merchants considering carrier billing. These fees can be comparatively larger than those for other payment methods, which may reduce merchant interest in adopting carrier billing as a primary payment route. Cost concerns combined with regulatory uncertainty can temper adoption, particularly where alternative digital payment options are widely available.

Opportunity Analysis

Inclusion of Unbanked and Subscription Markets

A notable opportunity in the carrier billing market is its potential to serve unbanked or under-banked populations who lack access to traditional bank accounts or credit cards. Carrier billing enables users in these segments to pay for digital services directly through their mobile accounts, unlocking participation in the digital economy. In many emerging markets, this characteristic makes carrier billing a bridge to financial inclusion and expanded digital consumption.

Another opportunity arises from the growth of subscription-based business models in entertainment, cloud services, and applications. Carrier billing can be integrated into recurring payment flows, offering a convenient and reliable method for users to manage ongoing digital subscriptions. Partnerships between content providers and telecom operators have the potential to expand the reach of carrier billing beyond one-time purchases into long-term revenue streams.

Challenge Analysis

Security and Fraud Management in Mobile Payments

A key challenge in the carrier billing market is managing security and fraud risk in mobile payment transactions. Carrier billing systems can be vulnerable to unauthorized charges or SIM-related fraud if safeguards are not sufficiently robust. Ensuring secure authentication and transaction monitoring is critical to maintain consumer trust and protect both merchants and mobile operators from financial losses.

This challenge is intensified by the complexity of mobile networks and the broad range of devices and user behaviours involved. Providers must invest in advanced risk management systems and clear processes for dispute resolution to address potential misuse or errors. Without well-developed security frameworks, growth can be hindered by concerns over liability and customer protection.

Competitive Analysis

Specialized direct carrier billing providers such as Boku Inc., Bango plc, and DIMOCO Payments GmbH play a central role in the carrier billing market. Their platforms connect merchants with telecom operators to enable payments charged directly to mobile bills. Strong compliance controls and fraud management systems support digital content transactions. Digital Virgo SA and Fortumo OÜ strengthen global reach. Demand is driven by digital subscriptions, gaming, and app store purchases.

Regional and merchant-focused billing providers such as Centili Ltd., NTH Mobile Payment Ltd., and SweePay AG emphasize localized operator integrations. Xsolla supports gaming monetization through carrier billing options. Kaleyra Inc. adds messaging-based transaction support. These players benefit from expanding mobile penetration and demand for frictionless micro-payments.

Telecom operators such as Orange Group SA, Vodafone Group plc, Telefónica S.A., China Mobile Communications Group Co., Ltd., and MTN Group Ltd. integrate billing capabilities directly into their networks. Globe Telecom Inc. and Telenor LinX AS expand digital payment ecosystems. Other vendors enhance competition and regional coverage across the carrier billing landscape.

Top Key Players in the Market

- Boku Inc.

- Bango plc

- DIMOCO Payments GmbH

- Infomedia Ltd.

- Digital Virgo SA

- Fortumo OÜ (an ROKU company)

- DOCOMO Digital Ltd.

- NETMOBILE AG

- NTH Mobile Payment Ltd.

- Centili Ltd.

- Xsolla (USA) Inc.

- SweePay AG

- Kaleyra Inc.

- Telenor LinX AS

- Globe Telecom Inc.

- Orange Group SA

- Vodafone Group plc

- Telefónica S.A.

- China Mobile Communications Group Co., Ltd.

- MTN Group Ltd.

- Others

Future Outlook

Growth in the Carrier Billing market is expected to remain steady as digital content and mobile based services continue to expand. Carrier billing allows users to charge purchases directly to their mobile phone bill, which supports simple and secure payments without cards or bank details.

Rising use of smartphones, digital subscriptions, and in app purchases is supporting demand. Over time, better fraud controls, wider merchant acceptance, and integration with digital platforms are likely to improve trust and usage.

Recent Developments

- September, 2025 – Digital Virgo stepped up at the Global Carrier Billing Summit in Amsterdam, moderating panels on DCB challenges like compliance and mobile money integration to push industry cooperation.

- March, 2025 – DIMOCO Payments deepened ties with Deutsche Telekom, rolling out carrier billing for their online shop to handle physical goods payments smoothly via the Agent Model.

Report Scope

Report Features Description Market Value (2025) USD 54.8 Billion Forecast Revenue (2035) USD 299.1 Billion CAGR(2025-2035) 18.50% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Content Type (Gaming, Video-on-Demand / OTT, Music and Audio Streaming), By Device Platform (Android Smartphones, iOS /iPadOS Devices), By Payment Flow (One-off (event-based), Subscription / Recurring), By Operator Type (Mobile Network Operators (MNOs), Mobile Virtual Network Operators (MVNOs)), By End-User Segment (Banked Consumers, Unbanked / Under-banked Consumers) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Boku Inc., Bango plc, DIMOCO Payments GmbH, Infomedia Ltd., Digital Virgo SA, Fortumo OÜ (an ROKU company), DOCOMO Digital Ltd., NETMOBILE AG, NTH Mobile Payment Ltd., Centili Ltd., Xsolla (USA) Inc., SweePay AG, Kaleyra Inc., Telenor LinX AS, Globe Telecom Inc., Orange Group SA, Vodafone Group plc, Telefónica S.A., China Mobile Communications Group Co., Ltd., MTN Group Ltd. Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Boku Inc.

- Bango plc

- DIMOCO Payments GmbH

- Infomedia Ltd.

- Digital Virgo SA

- Fortumo OÜ (an ROKU company)

- DOCOMO Digital Ltd.

- NETMOBILE AG

- NTH Mobile Payment Ltd.

- Centili Ltd.

- Xsolla (USA) Inc.

- SweePay AG

- Kaleyra Inc.

- Telenor LinX AS

- Globe Telecom Inc.

- Orange Group SA

- Vodafone Group plc

- Telefónica S.A.

- China Mobile Communications Group Co., Ltd.

- MTN Group Ltd.

- Others

Our Clients

- 175605

- Feb. 2026