Global Bionematicides Market Size, Share Analysis Report By Product Type (Microbials, Biochemicals, Integrated), By Mode of Application (Seed Treatment, Soil Treatment, Foliar Spray, Others), By Crop (Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183817

- Number of Pages: 210

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

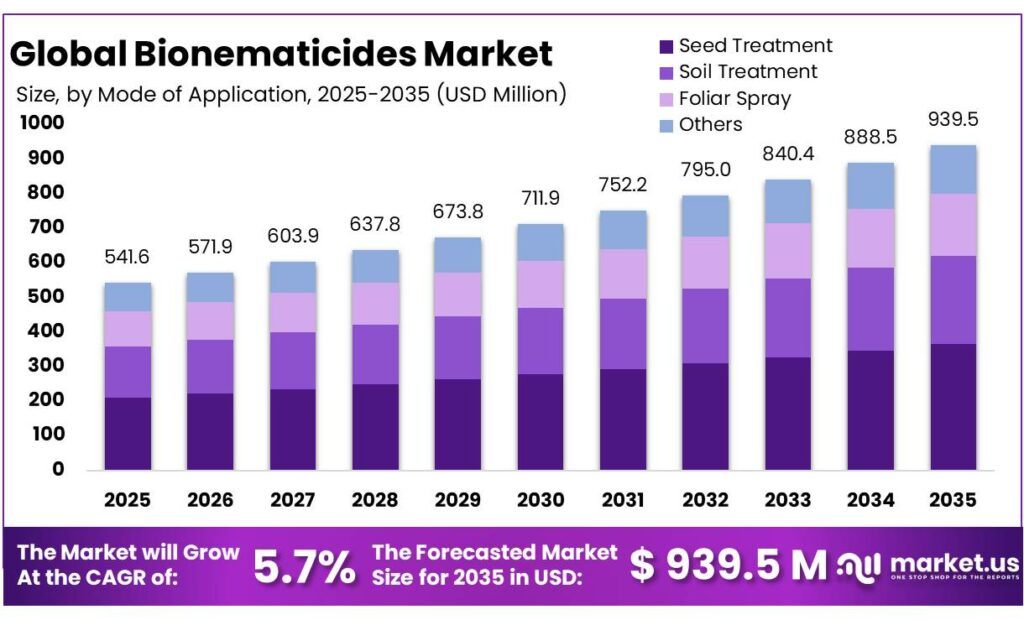

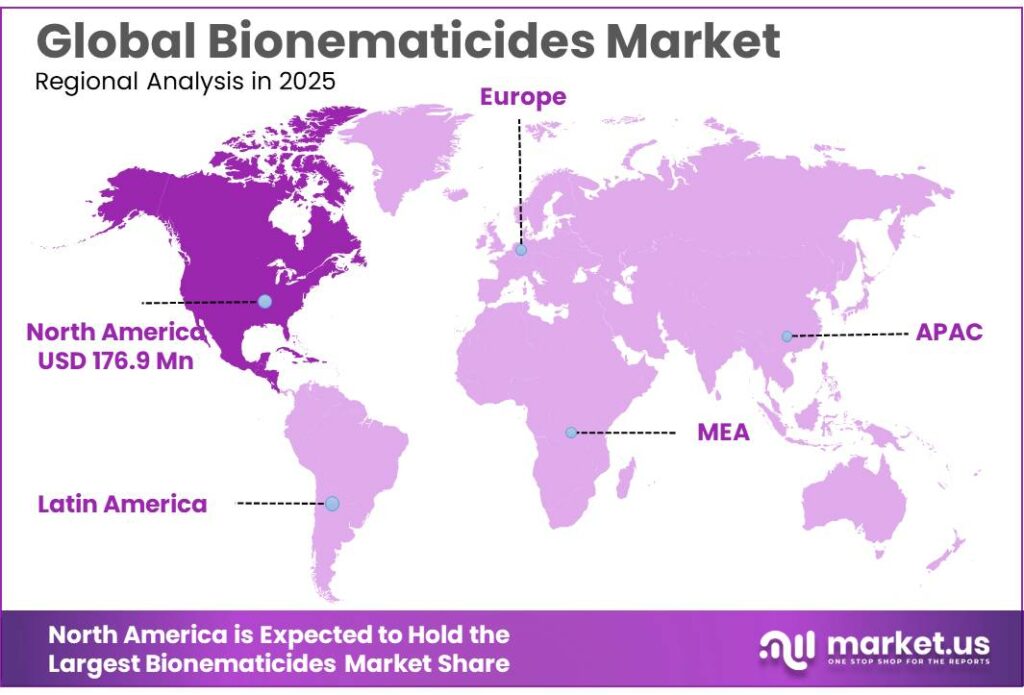

The Global Bionematicides Market size is expected to be worth around USD 939.5 Million by 2035, from USD 541.6 Million in 2025, growing at a CAGR of 5.7% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 32.7% share, holding USD 176.9 Million revenue.

Bionematicides are emerging as a strategically important part of biological crop protection because they target plant-parasitic nematodes through naturally derived or microbial modes of action, while fitting into residue-sensitive and resistance-management programs. Their relevance is increasing as food systems face mounting pest pressure: FAO states that plant pests and diseases reduce global crop yields by 20% to 40% every year, and it also notes that trade losses linked to plant pests exceed USD 220 billion annually, with invasive pests causing at least USD 70 billion in global economic losses.

The category is benefiting from the wider scale and commercialization capabilities of large crop-protection companies rather than from speculative market estimates. Bayer reported €22,259 million in Crop Science sales for 2024, demonstrating the commercial breadth through which biological and nematode-management solutions can be distributed globally.

BASF reported €9,798 million in 2024 Agricultural Solutions sales, with €1,938 million EBITDA before special items, underscoring that biological solutions are increasingly being embedded within large integrated portfolios rather than treated as stand-alone experiments. This matters for bionematicides because adoption often depends on formulation stability, field support, channel reach, and compatibility with existing crop programs.

The main growth drivers are regulatory pressure, sustainability targets, and grower demand for lower-residue alternatives that can be used in integrated pest management. In the European Union, the European Commission’s policy framework continues to target a 50% reduction in the use and risk of chemical pesticides and a 50% reduction in the use of more hazardous pesticides by 2030.

Policy direction does not automatically replace conventional nematicides, but it clearly improves the long-term positioning of biological alternatives, particularly where retailers, processors, and export-oriented growers are tightening residue expectations. FAO also notes that global agricultural trade has reached USD 1.7 trillion, which increases the commercial value of compliant and sustainable crop-protection systems.

Recent 2025 developments support this transition. In January 2025, Bayer announced a distribution agreement with Ecospray for a garlic-sourced liquid nematicide under the Velsinum™ brand, with commercialization across Europe, the Middle East, and parts of Africa starting in 2026. Separately, Bayer’s May 2025 Crop Science investor webinar identified a new BLX-containing nematicide mixture with about €2 billion in expected peak sales potential, showing that nematode control remains a meaningful innovation priority.

Key Takeaways

- Bionematicides Market size is expected to be worth around USD 939.5 Million by 2035, from USD 541.6 Million in 2025, growing at a CAGR of 5.7%.

- Microbials held a dominant market position, capturing more than a 49.5% share.

- Feather Reed Grass held a dominant market position, capturing more than a 39.4% share.

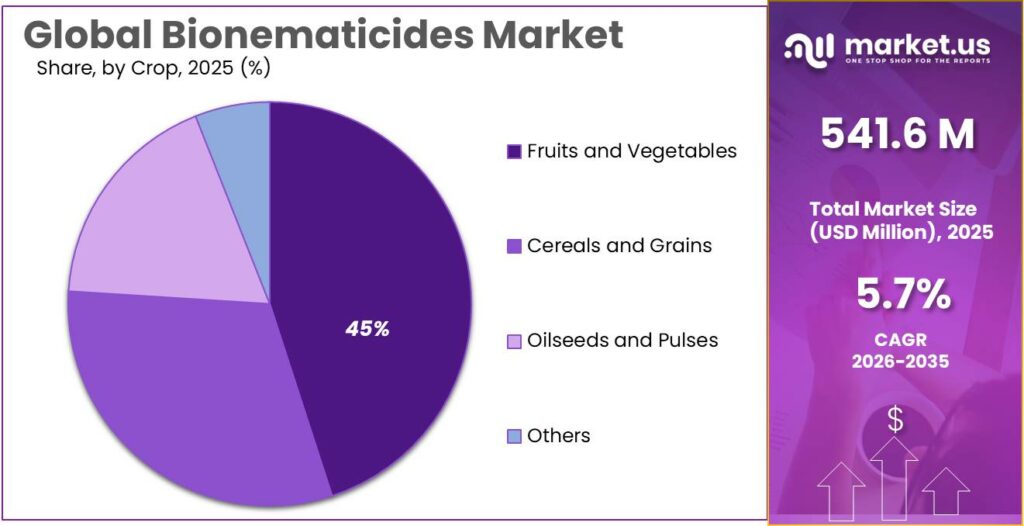

- Fruits and Vegetables held a dominant market position, capturing more than a 45.8% share.

- North America held a dominant market position in the bionematicides market, accounting for 32.7% of the global share and reaching a value of USD 176.9 million.

By Product Type Analysis

Microbials dominates with 49.5% share in 2025, supported by strong grower preference for residue-safe and soil-friendly nematode control.

In 2025, Microbials held a dominant market position, capturing more than a 49.5% share in the bionematicides market by product type. This leadership mainly comes from the growing use of beneficial bacteria, fungi, and other naturally derived microorganisms that help control harmful nematodes in the soil without affecting crop safety. Growers are increasingly choosing microbial-based solutions because they fit well into modern farming practices focused on soil health, sustainable yield improvement, and lower chemical dependence. These products are widely preferred in fruits, vegetables, and other high-value crops where root protection directly affects output quality and farm returns.

By Mode of Application Analysis

Seed Treatment leads with 39.4% share in 2025, helped by early root protection and easy use at planting.

In 2025, Feather Reed Grass held a dominant market position, capturing more than a 39.4% share in the bionematicides market by mode of application under the Seed Treatment segment. This strong position is mainly linked to the growing preference for treating seeds before sowing, which helps protect young roots from nematode attacks at the earliest growth stage. Farmers prefer this method because it offers targeted protection right where the crop begins its development, improving root strength and supporting better plant establishment.

By Crop Analysis

Fruits and Vegetables lead with 45.8% share in 2025, driven by higher root protection needs and premium crop value.

In 2025, Fruits and Vegetables held a dominant market position, capturing more than a 45.8% share in the bionematicides market by crop. This leading share is mainly supported by the high sensitivity of fruit and vegetable crops to root-knot and cyst nematodes, which can quickly reduce plant vigor, fruit quality, and marketable yield. Growers in this segment are usually more focused on preventive crop care because even minor root damage can directly affect size, color, shelf life, and export acceptance. Bionematicides are widely preferred here because they provide targeted root-zone protection while supporting residue-safe production practices, which is especially important for fresh produce and premium horticulture.

Key Market Segments

By Product Type

- Microbials

- Biochemicals

- Integrated

By Mode of Application

- Seed Treatment

- Soil Treatment

- Foliar Spray

- Others

By Crop

- Fruits and Vegetables

- Cereals and Grains

- Oilseeds and Pulses

- Others

Emerging Trends

Microbial Seed Treatment Integration Is the Latest Trend in Bionematicides

One of the most important latest trends in the bionematicides market is the rapid shift toward microbial seed treatment integration. Instead of relying only on post-sowing soil drenches, growers are increasingly using microbial bionematicides directly on seeds to give crops early-stage root protection.

This trend is becoming stronger because it improves product placement exactly where nematodes attack first—at the emerging root zone. A recent 2025 scientific review highlighted that plant-parasitic nematodes continue to cause nearly USD 157 billion in annual crop losses worldwide, which is pushing the industry toward more precise and preventive biological control systems.

Multi-Omics Discovery and Smarter Biological Formulations Are Expanding Innovation

Another major trend is the use of multi-omics research and smarter formulation science to improve consistency in biological nematode control. In 2025, new studies showed that advanced tools such as metabolomics, proteomics, and metagenomics are helping researchers identify stronger microbial strains and naturally occurring nematicidal compounds faster than before.

This is a major step because one of the older challenges in bionematicides was uneven field performance across different soils. Better strain mapping and formulation stabilization are now helping companies develop products with longer shelf life, stronger rhizosphere colonization, and improved survival after application. FAO’s broader sustainable agriculture programs continue to emphasize the need for resilient crop systems, and the organization notes that agriculture must continue producing more food under tighter environmental conditions.

Drivers

Rising Crop Losses Are a Major Growth Driver for Bionematicides

One of the biggest reasons the bionematicides market is growing is the rising pressure to reduce crop losses caused by soil-borne pests, especially nematodes. Farmers are increasingly looking for safer and more effective ways to protect roots because nematode damage often goes unnoticed until yields are already affected. According to FAO, up to 40% of global crop production is lost every year due to plant pests and diseases, creating an economic loss of more than USD 220 billion annually.

This level of loss is pushing growers toward preventive biological solutions that can be applied through seed treatment, soil drenching, and drip systems. Bionematicides are gaining preference because they help manage nematodes early while supporting healthier root zones and better nutrient uptake. As growers focus more on yield protection rather than late-stage crop recovery, the demand for biological nematode control continues to rise steadily across vegetables, fruits, and row crops.

Government and Global Food Security Programs Are Supporting Adoption

Another strong driver is the growing support from governments and global food agencies for sustainable crop protection and integrated pest management. FAO highlights that global food production needs to increase by around 50% by 2050 to meet future demand, making crop protection more critical than ever.

At the same time, public institutions are promoting lower-chemical farming practices to improve soil health and reduce environmental impact. This is creating a favorable environment for biological products such as bionematicides, especially in export-oriented and residue-sensitive crops. Government-backed plant health initiatives, pest surveillance systems, and farmer education programs are also helping improve awareness around preventive nematode control.

Restraints

Limited Field Consistency Remains a Major Restraint for Bionematicides

One of the biggest restraints for the bionematicides market is the inconsistent field performance under different soil and climate conditions. Unlike chemical nematicides, biological products depend heavily on moisture, temperature, soil organic matter, and microbial survival after application. This means the same product may perform very well in one farm and show slower results in another, making some growers hesitant about large-scale use. FAO noted in its 2025 integrated pest management guidance that pests and diseases continue to cause around USD 220 billion in global agricultural losses every year, which keeps farmers focused on highly reliable solutions when yield risk is high.

Government Push for Sustainable Farming Helps, But Adoption Still Takes Time

Government and food-agency initiatives are clearly supporting biological crop protection, but the pace of farmer adoption remains a restraint in the short term. FAO’s 2025 IPM training programs show that even after previous outreach, many farmers still struggle with correct pest monitoring, product timing, and field-level decision making, which directly affects confidence in biological solutions. In one recent FAO-backed program, only 20 selected farmer representatives were initially trained, with knowledge expected to reach 50 additional farmers through local networks.

Opportunity

Protected Cultivation and High-Value Crops Create the Biggest Growth Opportunity

One of the strongest growth opportunities for bionematicides is the rapid expansion of protected cultivation and high-value fruit and vegetable farming, where root health directly affects yield quality and shelf life. In greenhouse vegetables, berries, peppers, cucumbers, and leafy crops, nematode pressure can quickly reduce plant vigor, making preventive biological control highly valuable.

FAO has repeatedly emphasized that future food systems must produce more from the same land area, and in its sustainable crop production framework it highlights that yield gains in maize under improved systems increased from 300 kg/ha to more than 1.5 tonnes/ha, showing how productivity-led farming systems reward better soil and root-zone management.

Government-Led Biological Farming Programs Are Expanding Commercial Use

A second major opportunity comes from government-backed biological crop protection initiatives and climate-smart farming programs. In 2025, FAO and government counterparts in Vietnam launched a biological plant protection project running from March to December 31, 2025, focused on strengthening regulation, farmer training, and wider adoption of biological plant protection products. The program specifically supports research, production, registration, and field use of biological crop protection tools, creating a stronger commercial pathway for products such as bionematicides.

This kind of policy-backed ecosystem is important because it reduces one of the biggest barriers in biologicals: grower confidence and technical know-how. As more countries invest in climate-resilient agriculture, nature-based pest control, and integrated pest management, bionematicides gain a direct route into institutional recommendations and subsidy-linked farming systems. The growth opportunity is therefore not only product demand, but also scalable market access through public extension networks, legal frameworks, and residue-safe export agriculture, which can significantly improve long-term adoption across commercial farming systems.

Regional Insights

North America dominates the Bionematicides market with 32.7% share, reaching USD 176.9 Mn on the back of advanced biological crop protection adoption.

In 2025, North America held a dominant market position in the bionematicides market, accounting for 32.7% of the global share and reaching a value of USD 176.9 million. The region’s leadership is strongly supported by its advanced agricultural practices, early adoption of biological crop protection products, and strong institutional backing for sustainable pest management.

The United States Department of Agriculture (USDA) continues to strengthen biological and microbial pest management pathways through its National Program 304 Action Plan 2025–2030, which focuses on environmentally compatible pest control tools, digital agriculture, and microbial-based biopesticides for resilient farming systems. USDA also notes that specialty and row crops together cover around a quarter of a billion acres in the U.S., representing more than USD 115 billion in annual value, which creates a large commercial base for nematode management solutions.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF remains a strong strategic player in the bionematicides space through its Agricultural Solutions business, which reported €9,587 million in sales in 2025. The company’s strength comes from its BioSolutions platform, where microbial and biologically derived crop protection products are being positioned for soil health and nematode management in high-value crops. BASF’s strong investment capacity is supported by its scale, helping expand microbial formulations, seed treatment compatibility, and root-zone application technologies.

Bayer AG is one of the most influential companies in biological nematode management, supported by its Crop Science sales of €21.622 billion in 2025. The company continues to expand its biological pipeline, including microbial and plant-derived nematode control technologies that fit integrated pest management systems. Bayer’s scale in seed treatment, digital farming, and biological crop protection makes it highly competitive in this market.

Corteva Agriscience is strengthening its presence in bionematicides through biological crop protection innovation and seed-applied microbial technologies. In 2025, the company projected net sales between $17.6 billion and $17.8 billion, supported by strong crop protection demand. Corteva’s expertise in seed science and soil health solutions gives it an important edge in microbial nematode control, especially for corn, soybean, and vegetable systems. Its increasing investment in new biological actives and seed treatment platforms supports scalable commercial adoption.

Top Key Players Outlook

- BASF

- Bayer AG

- Syngenta

- Corteva Agriscience

- FMC Corporation

- UPL

- Sumitomo Chemical Co., Ltd.

- Mitsui & Co., Ltd.

- Bioceres Crop Solutions

- Koppert

Recent Industry Developments

In 2025, Amcor reported USD 15.0 billion in net sales, operated 400+ manufacturing sites, and expanded its post-merger workforce to more than 75,000 employees, giving it the scale to serve global crop input brands with specialized agricultural packaging formats.

In 2025, BASF’s Agricultural Solutions segment generated €9,587 million in sales, with €2,081 million in EBITDA before special items, showing the company’s strong financial capacity to scale microbial crop protection technologies globally.

In 2025, Bayer reported €21.6 billion in Crop Science sales, giving it the financial scale to support product development, registrations, and global distribution in this field.

Report Scope

Report Features Description Market Value (2025) USD 541.6 Mn Forecast Revenue (2035) USD 939.5 Mn CAGR (2026-2035) 5.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Microbials, Biochemicals, Integrated), By Mode of Application (Seed Treatment, Soil Treatment, Foliar Spray, Others), By Crop (Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF, Bayer AG, Syngenta, Corteva Agriscience, FMC Corporation, UPL, Sumitomo Chemical Co., Ltd., Mitsui & Co., Ltd., Bioceres Crop Solutions, Koppert Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BASF

- Bayer AG

- Syngenta

- Corteva Agriscience

- FMC Corporation

- UPL

- Sumitomo Chemical Co., Ltd.

- Mitsui & Co., Ltd.

- Bioceres Crop Solutions

- Koppert

Our Clients

- 183817

- April 2026