Global Automotive Junction Box Market Size, Share, Growth Analysis By Type (Passive, Smart, Others), By Function (Automotive Power Switching, Vehicle Body Control), By Vehicle (Passenger Cars, Commercial Vehicles), By Sales Channel (OEM, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179887

- Number of Pages: 345

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

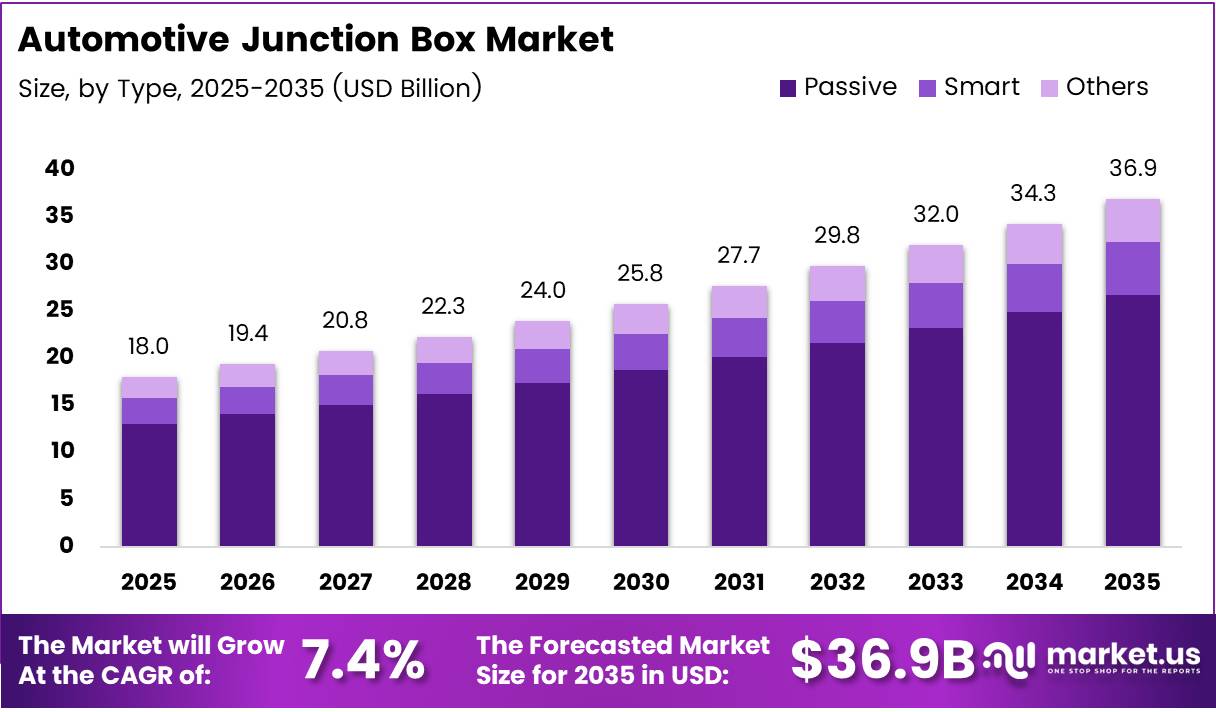

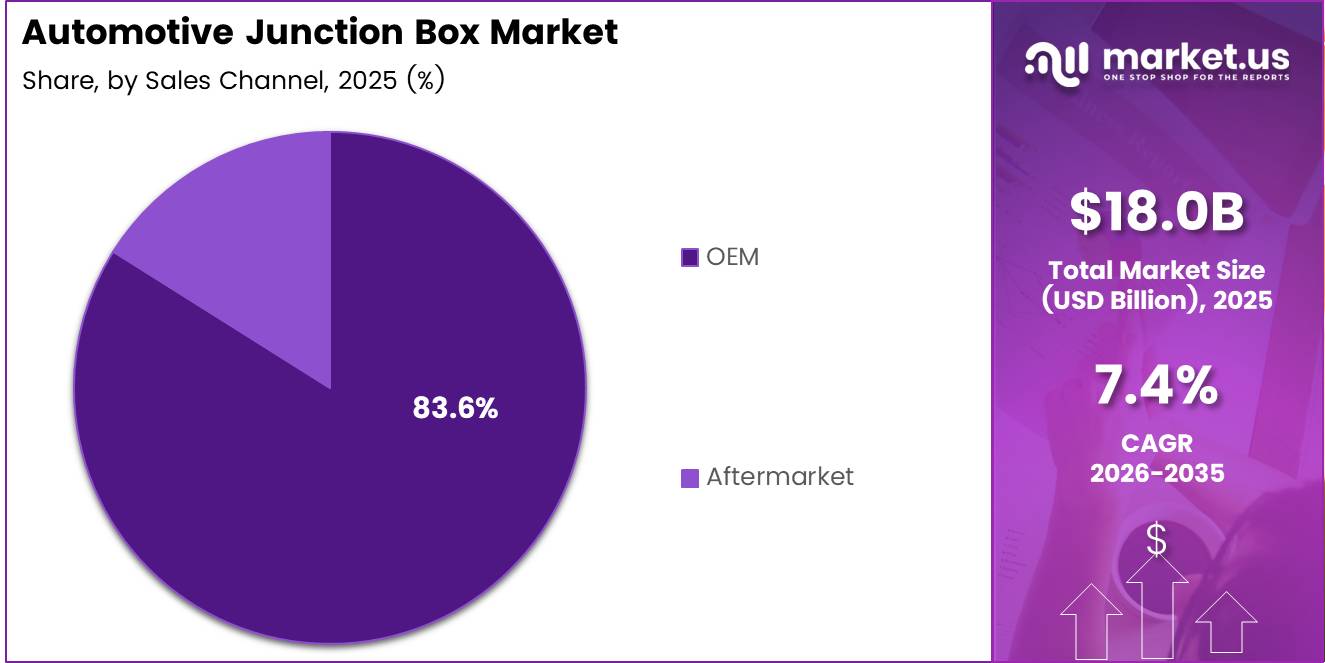

Global Automotive Junction Box Market size is expected to be worth around USD 36.9 Billion by 2035 from USD 18.0 Billion in 2025, growing at a CAGR of 7.4% during the forecast period 2026 to 2035.

Automotive junction boxes serve as the central nodes of a vehicle’s electrical distribution architecture. They manage power routing, circuit protection, and signal distribution across powertrain, body control, and safety systems. As vehicles carry more electronic content per unit, the junction box transitions from a passive component to a critical system-level asset.

The structural shift toward vehicle electrification reshapes every layer of this market. OEMs no longer design electrical systems around a single 12V architecture. Hybrid and battery electric platforms introduce 48V and high-voltage bus requirements that demand new junction box configurations with higher current ratings and thermal management capability. This complexity directly expands the addressable value per vehicle.

ADAS proliferation compounds this demand. As safety systems become standard equipment across vehicle lines, the number of protected circuits per vehicle rises sharply. Each additional electronic control unit adds load-carrying and protection requirements that junction box suppliers must accommodate within tighter packaging constraints.

Regulatory frameworks in North America, Europe, and China mandate minimum safety electronics content, which establishes a non-discretionary replacement cycle for compliant electrical distribution components. This regulatory floor limits downside risk for OEM-aligned suppliers while creating pricing leverage for those who meet homologation requirements early.

In January 2024, Aptiv completed the acquisition of Intercable Automotive Solutions, strengthening its position in high-voltage busbar and electrical distribution — a move that signals consolidation pressure among Tier 1 suppliers competing for electrification-era contracts. This acquisition pattern reflects the broader market reality: scale and high-voltage capability now determine supplier selection at the OEM level.

According to the International Energy Agency, global electric car sales reached 14 million units in 2023, representing about 18% of total car sales. This volume translates directly into junction box demand, as each EV platform requires purpose-engineered high-voltage power distribution units that conventional 12V designs cannot serve.

According to the International Energy Agency, electric car sales exceeded 17 million units in 2024, accounting for more than 20% of global new car sales. This acceleration confirms that EV platforms are becoming the primary design context for junction box engineers — shifting product development timelines, material choices, and qualification standards across the entire supply chain.

Key Takeaways

- The global Automotive Junction Box Market was valued at USD 18.0 Billion in 2025 and is forecast to reach USD 36.9 Billion by 2035, at a CAGR of 7.4%.

- By Type, Passive junction boxes dominate with a 72.5% market share in 2025.

- By Function, Automotive Power Switching leads with 57.2% share in 2025.

- By Vehicle, Passenger Cars account for 75.9% of the market in 2025.

- By Sales Channel, OEM accounts for 83.6% of market revenue in 2025.

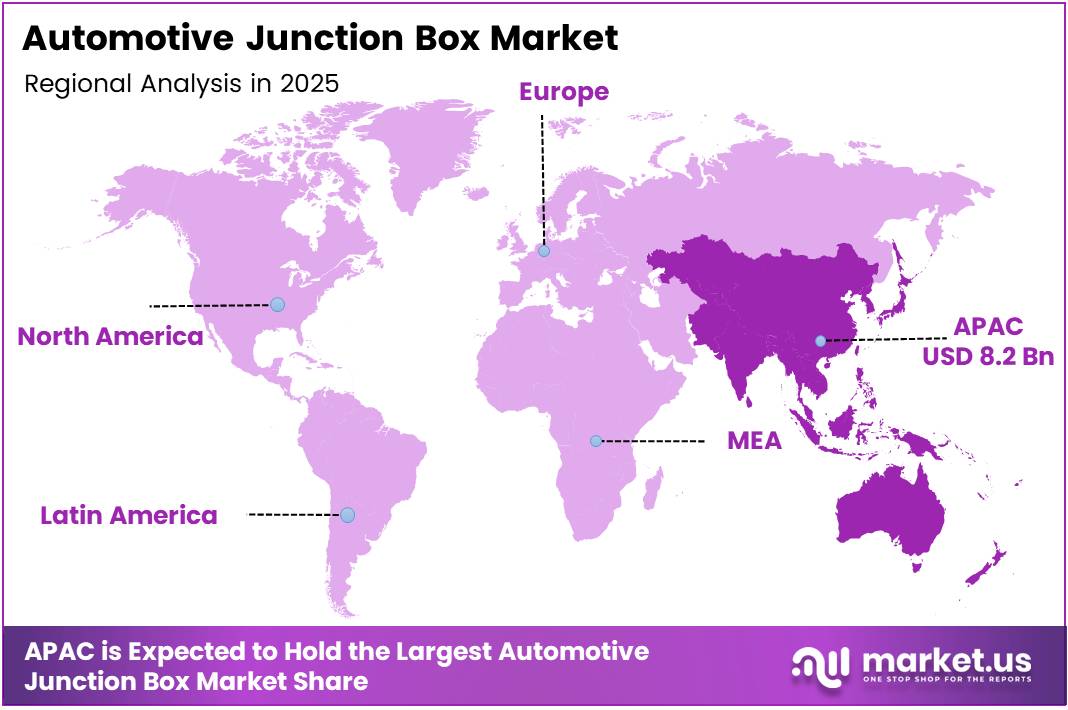

- Asia Pacific leads all regions with 45.80% market share, valued at USD 8.2 Billion in 2025.

Type Analysis

Passive junction boxes dominate with 72.5% due to lower cost and universal compatibility.

In 2025, Passive junction boxes held a dominant market position in the By Type segment of the Automotive Junction Box Market, with a 72.5% share. Their mechanical simplicity and proven reliability across ICE and entry-level hybrid platforms sustain this dominance. OEMs standardize passive designs across high-volume vehicle lines to control per-unit cost, which consolidates volume toward established suppliers with existing tooling and qualification approvals.

Smart junction boxes carry the highest growth potential within the By Type segment. They integrate embedded diagnostics, load management logic, and communication interfaces — capabilities that OEMs now require for EV and ADAS-intensive platforms. Smart units command a meaningful price premium over passive alternatives, which makes them commercially attractive even at lower initial volumes compared to the mature passive segment.

Others in the type segment covers specialized configurations such as high-voltage battery junction boxes and modular multi-box architectures. These serve niche but fast-growing applications in commercial EV platforms and purpose-built autonomous vehicle designs. Their unit economics differ substantially from standard junction boxes, and they increasingly attract dedicated product lines from Tier 1 electrical system suppliers.

Function Analysis

Automotive Power Switching dominates with 57.2% due to universal presence across all powertrain types.

In 2025, Automotive Power Switching held a dominant market position in the By Function segment of the Automotive Junction Box Market, with a 57.2% share. Power switching functions underpin every junction box deployment regardless of vehicle type or voltage architecture. The shift to higher-voltage platforms expands the technical requirements for this function — demanding higher-rated switches, thermal management integration, and faster fault response — which supports sustained revenue growth within this category.

Vehicle Body Control functions manage lighting, door systems, mirrors, and HVAC electrical distribution. As OEMs add comfort and convenience features across broader model lines, body control content per vehicle rises. This category benefits from connectivity and personalization trends, as software-defined vehicle architectures require more granular switching and protection at the body control layer.

Vehicle Analysis

Passenger Cars dominate with 75.9% due to highest global production volume and electronic content density.

In 2025, Passenger Cars held a dominant market position in the By Vehicle segment of the Automotive Junction Box Market, with a 75.9% share. Passenger car platforms carry the broadest range of electronic systems — from basic body control to full ADAS suites — making junction box content per vehicle the highest in this category. EV adoption within passenger cars accelerates high-voltage junction box integration, reinforcing this segment’s revenue lead.

Hatchback platforms prioritize compact electrical architecture due to packaging constraints. Junction boxes in this segment balance cost efficiency with protection requirements for urban-use electronics. Hatchbacks increasingly serve as the entry point for mild hybrid and EV technology in emerging markets, which expands the addressable base for next-generation power distribution units.

Sedan platforms support mid-to-premium electronic content and serve as the primary deployment vehicle for ADAS features in volume markets. Sedans drive consistent demand for structured junction box assemblies that accommodate both standard and optional electronics packages without redesign across trim levels.

SUV platforms carry the highest per-unit junction box content among passenger car body styles. Their larger electrical architectures accommodate advanced safety, infotainment, and electrified powertrain systems simultaneously. Premium SUV programs often serve as the launch platform for new junction box technologies before broader adoption across lower-priced segments.

Commercial Vehicles represent a structurally distinct segment with longer product cycles and lower annual volumes than passenger cars. However, the electrification of commercial fleets — particularly in urban logistics — introduces new high-voltage junction box requirements that differ materially from ICE-based commercial electrical systems, opening a differentiated product opportunity for suppliers.

LCV (Light Commercial Vehicle) platforms face accelerating electrification pressure from urban emission zone regulations in Europe and China. These requirements force fleet operators to transition to EV platforms, which directly generates demand for purpose-built high-voltage junction boxes that differ from both passenger car and heavy commercial architectures.

HCV (Heavy Commercial Vehicle) junction boxes operate under sustained high-current loads and demanding thermal cycles that standard passenger car designs cannot satisfy. Suppliers targeting this segment invest in specialized materials and contact technologies. HCV electrification timelines lag behind passenger cars, but early movers in high-voltage HCV power distribution stand to capture durable supply relationships with major fleet operators.

Sales Channel Analysis

OEM dominates with 83.6% due to captive supply contracts and vehicle platform integration requirements.

In 2025, OEM held a dominant market position in the By Sales Channel segment of the Automotive Junction Box Market, with an 83.6% share. OEM contracts determine junction box design specifications, qualification timelines, and pricing — creating long-term revenue visibility for Tier 1 suppliers who secure platform awards. The technical integration depth of junction boxes within vehicle electrical architecture makes post-production substitution impractical, which further entrenches OEM channel dominance.

Aftermarket junction box demand is driven by vehicle age and failure replacement cycles. The segment carries higher margin potential than OEM volume pricing but faces constraints from limited standardization and lower demand predictability. Aftermarket suppliers who offer cross-vehicle compatibility and faster delivery lead times differentiate effectively in this channel.

Key Market Segments

By Type

- Passive

- Smart

- Others

By Function

- Automotive Power Switching

- Vehicle Body Control

By Vehicle

- Passenger Cars

- Hatchback

- Sedan

- SUV

- Commercial Vehicles

- LCV

- HCV

By Sales Channel

- OEM

- Aftermarket

Drivers

Vehicle Electrification and ADAS Expansion Drive Compound Demand for Advanced Power Distribution Systems

EV platforms introduce high-voltage and high-current architectures that standard 12V junction boxes cannot serve. OEMs designing for 400V and 800V battery systems require purpose-engineered power distribution units with thermal management, fault isolation, and higher contact ratings. This creates a non-interchangeable product category that commands higher average selling prices per vehicle.

According to the National Highway Traffic Safety Administration, Automatic Emergency Braking became standard on 94.9% of new light-duty vehicles sold in the United States in 2023. This near-universal adoption rate means ADAS circuit protection requirements now appear on essentially every new vehicle program — transforming junction box content from optional to mandatory across virtually the entire production volume.

In June 2024, onsemi announced a strategic agreement with Volkswagen Group to supply next-generation silicon carbide power modules for EV platforms. This agreement illustrates how semiconductor-level innovation directly reshapes junction box design requirements, as SiC-based power stages operate at higher frequencies and temperatures that demand new protection and switching specifications at the distribution layer.

Restraints

Design Complexity and Raw Material Volatility Compress Supplier Margins Across Compact Vehicle Electrical Architectures

Modern vehicle electrical architectures pack more circuits, voltage levels, and functional requirements into shrinking physical envelopes. Junction box engineers must accommodate multi-voltage bus coexistence, electromagnetic compatibility requirements, and crash-zone positioning — all within package dimensions that do not grow proportionally with electrical content. This design compression increases engineering cost per program and extends qualification timelines.

According to the National Highway Traffic Safety Administration, Adaptive Cruise Control was standard on 68.8% of new vehicles sold in the United States in 2023. While this confirms broad ADAS adoption, it also signals the integration challenge: each additional driver assistance function adds protected circuits that must coexist within a single electrical distribution assembly, compounding routing complexity and increasing failure-mode analysis scope.

Raw material price volatility — particularly for copper, aluminum, and engineering thermoplastics — directly erodes the cost structure of electrical distribution components. Junction boxes carry significant material content relative to their selling price, which means commodity cycles compress supplier margins faster than contract repricing mechanisms allow. Suppliers without hedged procurement strategies or vertical material integration face structural profitability risk during commodity upswings.

Growth Factors

48V Mild Hybrid Adoption, Autonomous Vehicle Development, and Lightweighting Demand Create Next-Generation Junction Box Opportunities

The transition to 48V mild hybrid systems creates a distinct product tier between conventional 12V junction boxes and full high-voltage EV units. This architecture requires new switching and protection specifications that existing passive junction box designs do not satisfy. Suppliers who develop qualified 48V-ready product platforms position themselves to capture content on the broad base of mild hybrid programs launching across European and Asian OEM lineups.

Autonomous vehicle development imposes redundant power distribution requirements that conventional single-path junction box architectures cannot meet. Redundant power paths demand either dual junction box assemblies or architecturally complex single-unit solutions. According to the National Highway Traffic Safety Administration, Lane Departure Warning systems were standard on 91.5% of new U.S. light-duty vehicles in 2023 — confirming that the sensor load requiring redundant power protection already exists in nearly all new vehicles.

OEM adoption of modular wiring harness platforms creates demand for standardized, scalable junction box interfaces that accommodate across multiple vehicle derivatives without full redesign. Simultaneously, lightweighting mandates push suppliers toward miniaturized electrical distribution units using advanced thermoplastics and aluminum busbars. These two forces together reward suppliers who invest in platform-level product architectures rather than vehicle-specific custom designs.

Emerging Trends

Smart Junction Boxes, Solid-State Switching, and Zonal Architecture Redefine Electrical Distribution Design Standards

Smart junction boxes with embedded diagnostics and communication functions shift the product from a passive protection device to an active system node. These units report real-time load data, execute remote switching commands, and flag fault conditions before circuit damage occurs. OEMs designing software-defined vehicles treat smart junction boxes as software-addressable hardware — fundamentally changing the supplier capability requirements for future platform awards.

In September 2024, NXP Semiconductors introduced its MC33777 battery junction box controller designed for EV high-voltage battery management systems. This product launch illustrates how semiconductor suppliers now compete directly in the functional space historically owned by junction box assemblers — compelling Tier 1 electrical system suppliers to integrate semiconductor IP or risk losing design authority at the component level.

According to the U.S. Energy Information Administration, battery electric vehicles accounted for 7.6% of U.S. light-duty vehicle sales in 2023, up from 5.9% in 2022. This volume growth coincides with the automotive industry’s adoption of zonal electrical architecture, which consolidates domain controllers and redistributes power via fewer, smarter junction nodes — a structural shift that rewards suppliers capable of delivering high-current, multi-function zonal power distribution units.

Regional Analysis

Asia Pacific Dominates the Automotive Junction Box Market with a Market Share of 45.80%, Valued at USD 8.2 Billion

Asia Pacific commands 45.80% of the global market, valued at USD 8.2 Billion in 2025. China’s position as the world’s largest EV production base anchors this dominance. Chinese OEMs and their Tier 1 supply chains design and manufacture high-voltage junction boxes at scale that no other region matches — creating a structural cost and volume advantage that sustains APAC’s lead through the forecast period.

North America Automotive Junction Box Market Trends

North America benefits from mandatory ADAS content regulations, a growing EV production base, and large commercial vehicle fleets undergoing electrification. U.S. federal safety mandates create a regulatory floor for electronic content per vehicle, which sustains junction box demand independent of consumer preference cycles. Tier 1 suppliers serving domestic OEM programs maintain strong pricing discipline within this channel.

Europe Automotive Junction Box Market Trends

Europe’s CO2 emissions standards compel OEMs to electrify model lines faster than in most other markets. This regulatory timeline accelerates OEM investment in high-voltage electrical architectures — and directly expands junction box content per vehicle across the region’s premium and volume segments alike. Germany and France lead junction box engineering activity, reflecting the concentration of OEM headquarters and Tier 1 development centers.

Latin America Automotive Junction Box Market Trends

Latin America’s junction box market follows ICE-dominant vehicle production with selective EV introduction in Brazil and Mexico. Local OEM assembly operations import electrical components from North American and Asian supply chains, limiting the emergence of regional junction box manufacturing. Market activity tracks global OEM platform rollouts rather than locally driven electrification policy.

Middle East and Africa Automotive Junction Box Market Trends

The Middle East and Africa market operates primarily through vehicle imports, which limits direct junction box manufacturing activity in the region. However, GCC fleet electrification initiatives and rising commercial vehicle sales create aftermarket replacement demand. South Africa serves as the region’s primary OEM assembly hub and represents the most organized channel for junction box distribution and servicing.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BorgWarner positions itself at the intersection of powertrain electrification and electrical distribution, leveraging its transition from combustion-era drivetrain components to EV-compatible power management systems. Its acquisition-led growth strategy builds breadth across high-voltage architectures, which reduces customer concentration risk and expands its content per EV platform — a meaningful structural advantage as OEMs consolidate supplier counts.

Bosch integrates junction box development within its broader vehicle electronics portfolio, which allows it to bundle power distribution with sensor systems, ECUs, and software — a bundling strategy that individual junction box specialists cannot replicate. This integration depth makes Bosch a preferred partner for OEMs designing fully consolidated electrical architectures, even when per-unit component pricing exceeds single-category alternatives.

Continental anchors its junction box strategy within its intelligent transportation systems and vehicle networking divisions. By connecting power distribution design to software-defined vehicle platform development, Continental offers OEM customers a single engineering interface across electrical, network, and control layers. This convergence approach limits competitive substitution risk and supports longer contract durations at the OEM design-win stage.

Denso benefits from its deep integration within Toyota Group’s vehicle programs, which provides captive volume across passenger car, hybrid, and fuel cell platforms. This structural relationship gives Denso consistent design authority over junction box specifications on some of the world’s highest-volume vehicle programs. Denso’s materials and thermal management expertise applies directly to high-voltage junction box requirements on hybrid and BEV platforms.

Key Players

- BorgWarner

- Bosch

- Continental

- Denso

- Eaton

- Johnson Control

- Lear Corporation

- ON Semiconductor

- Valeo

- Yazaki

Recent Developments

- November 2024 – Infineon Technologies launched new automotive smart power switch solutions supporting 12V and 48V vehicle power distribution architectures, expanding its product range to serve both conventional and mild hybrid electrical systems across multiple vehicle segments.

- February 2025 – TE Connectivity announced expansion of its high-voltage automotive contactor and power distribution manufacturing capacity in Europe, strengthening its ability to supply European OEM electrification programs with locally manufactured high-voltage components.

- April 2025 – Yazaki Corporation opened a new engineering center in Germany focused on advanced vehicle electrical distribution systems, positioning the company to collaborate directly with European OEM engineering teams on next-generation platform designs.

- May 2025 – Dorman Products launched new aftermarket automotive power distribution and smart junction box solutions for multiple vehicle models, targeting the growing vehicle parc of late-model cars requiring replacement or upgraded electrical distribution components.

Report Scope

Report Features Description Market Value (2025) USD 18.0 Billion Forecast Revenue (2035) USD 36.9 Billion CAGR (2026-2035) 7.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Passive, Smart, Others), By Function (Automotive Power Switching, Vehicle Body Control), By Vehicle (Passenger Cars – Hatchback, Sedan, SUV; Commercial Vehicles – LCV, HCV), By Sales Channel (OEM, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BorgWarner, Bosch, Continental, Denso, Eaton, Johnson Control, Lear Corporation, ON Semiconductor, Valeo, Yazaki Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Automotive Junction Box MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Automotive Junction Box MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BorgWarner

- Bosch

- Continental

- Denso

- Eaton

- Johnson Control

- Lear Corporation

- ON Semiconductor

- Valeo

- Yazaki

Our Clients

- 179887

- Feb 2026