Quick Navigation

Report Overview

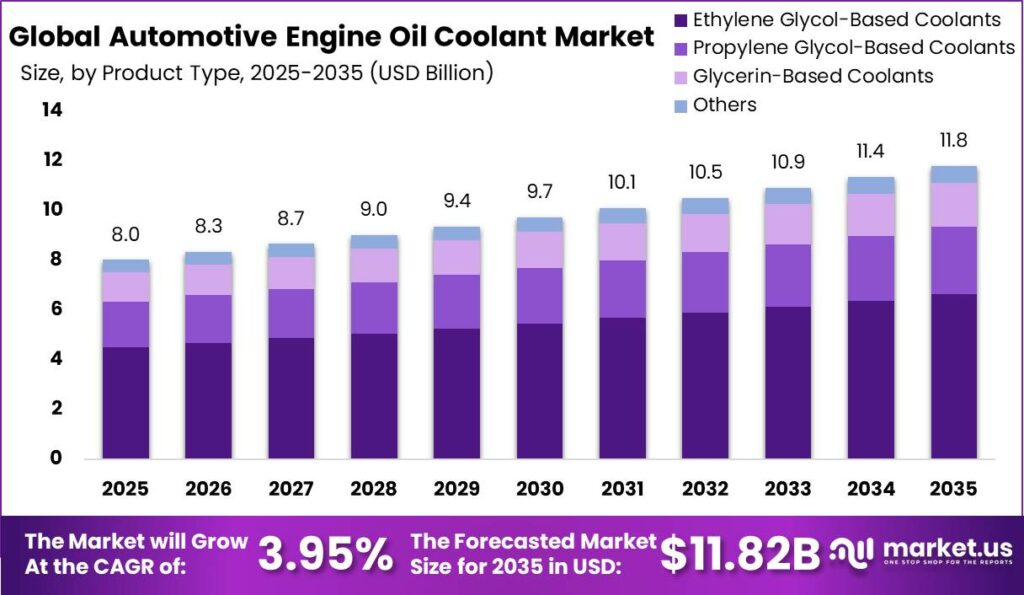

Global Automotive Engine Oil Coolant Market size is expected to be worth around USD 11.82 Billion by 2035 from USD 8.02 Billion in 2025, growing at a CAGR of 3.95% during the forecast period 2026 to 2035. This steady climb reflects a maturing yet resilient fluids category. Investors should read this as stable, volume-led returns rather than speculative upside, favoring scale and distribution over disruptive plays.

Therefore, understanding market structure matters before capital commitment. The Automotive Engine Oil Coolant Market covers heat-transfer fluids that regulate engine and powertrain temperature across passenger and commercial vehicles. Suppliers segment it by product chemistry, additive technology, vehicle type, and sales channel. This layered structure lets formulators target distinct margin pools, so buyers can match chemistry to fleet age and operating conditions with precision.

Key Takeaways

- Global market size reached USD 8.02 Billion in 2025 and is forecast to hit USD 11.82 Billion by 2035 at a CAGR of 3.95%.

- Ethylene Glycol-Based Coolants lead the By Product Type segment with a 56.20% share.

- Organic Additive Technology (OAT) dominates the By Technology segment at 42.10%.

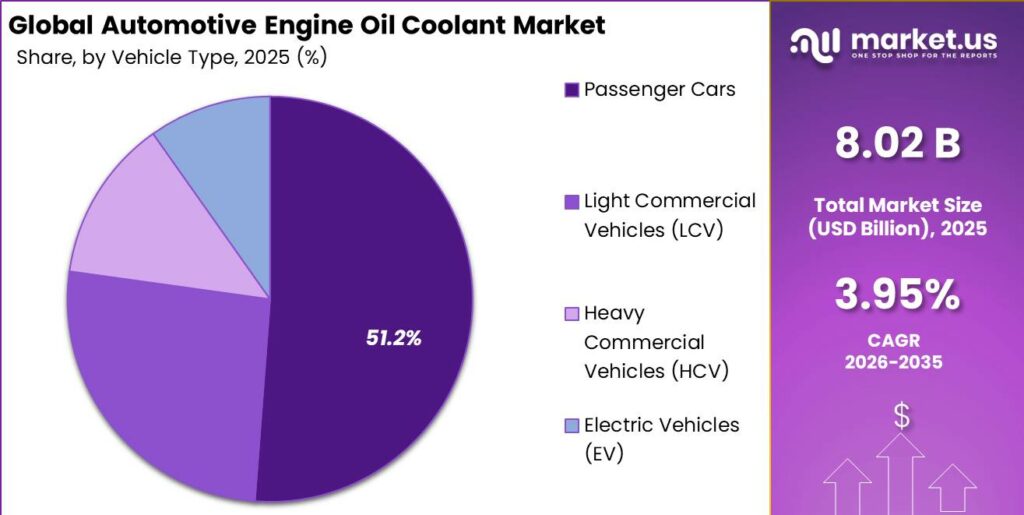

- Passenger Cars hold the largest By Vehicle Type share at 51.20%.

- The Aftermarket channel commands 67.50% of the By Sales Channel segment.

- Asia Pacific dominates regionally with a 38.40% share, valued at USD 3.08 Billion.

Government policy now shapes coolant demand as much as fleet size does. Euro 7 rules raise compliance costs for conventional powertrains and accelerate cleaner engine adoption across regulated markets. This shifts formulator investment toward advanced, longer-life chemistries. Suppliers who align product roadmaps with tightening emission mandates will protect OEM approvals and defend their position against lower-spec regional competitors.

Vehicle output anchors the recurring demand base. According to ACEA, global car manufacturing reached 75.5 million units in 2024, feeding large factory-fill and service demand for coolants. This scale gives formulators predictable volume visibility. As a result, producers can plan capacity and raw material contracts with confidence, lowering per-unit cost and strengthening bargaining power with feedstock suppliers.

Electrification reframes the long-term opportunity set. As reported by IEA, global electric car sales exceeded 20 million units in 2025, near 25% of all car sales, trimming future ICE coolant volume. This signals a two-track market. Investors should back suppliers building EV thermal fluid capability now, since single-chemistry ICE players face structural volume erosion within the decade.

Product Type Analysis

Ethylene Glycol-Based Coolants dominates with 56.20% due to superior heat transfer and low cost.

In 2025, Ethylene Glycol-Based Coolants held a dominant market position in the By Product Type segment of Automotive Engine Oil Coolant Market, with a 56.20% share. This chemistry delivers strong thermal conductivity at a low price point, making it the default for mass-market service fills. Formulators who scale ethylene glycol production capture the broadest addressable volume, protecting margin through purchasing leverage on bulk feedstock.

Propylene Glycol-Based Coolants serve buyers who prioritize lower toxicity and safer handling in sensitive applications. Fleet operators in food transport and agriculture favor this chemistry for spill safety. This creates a premium niche where suppliers command higher prices, letting mid-tier blenders differentiate away from crowded commodity competition and build loyalty with safety-conscious commercial accounts.

Glycerin-Based Coolants appeal to environmentally driven buyers seeking renewable, biodegradable formulations over petrochemical bases. Adoption remains focused in regulated markets with green procurement rules. This opens a defensible sustainability position for early movers. Suppliers who certify bio-based lines now can win long-term contracts before larger players commoditize the category and compress pricing.

Global vehicle output underpins demand across every chemistry tier. Data from OICA shows global motor vehicle production reached 95.36 million units in 2025, expanding the parc that needs factory-fill and aftermarket fluids. The remaining share sits with Others, which covers specialty and blended formulations. This breadth means formulators can cross-sell multiple chemistries into the same service network.

Technology Analysis

Organic Additive Technology (OAT) dominates with 42.10% due to long service life and corrosion protection.

In 2025, Organic Additive Technology held a dominant market position in the By Technology segment of Automotive Engine Oil Coolant Market, with a 42.10% share. OAT delivers extended drain intervals up to five years, cutting maintenance frequency for owners. This durability wins OEM factory-fill contracts, so formulators with proven OAT inhibitor packages secure high-volume, multi-year supply agreements with vehicle manufacturers.

Inorganic Additive Technology (IAT) still serves older commercial fleets and legacy engines built for silicate-based chemistry. Operators of aging trucks rely on IAT for compatibility and low upfront cost. This sustains steady aftermarket volume in emerging markets. Suppliers who keep IAT lines active retain access to price-sensitive fleets that modern chemistries cannot yet displace.

Hybrid Organic Acid Technology (HOAT) bridges IAT and OAT by combining organic acids with silicate protection for mixed fleets. Workshops servicing diverse vehicle parcs value its broad compatibility. This reduces wrong-coolant risk, so distributors carrying HOAT lower warranty exposure. Blenders offering reliable HOAT platforms ease stocking complexity for multi-brand aftermarket networks and win distributor preference.

Vehicle Type Analysis

Passenger Cars dominates with 51.20% due to the largest global vehicle parc base.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of Automotive Engine Oil Coolant Market, with a 51.20% share. Passenger cars form the deepest installed base needing routine coolant service. This scale makes the segment the primary volume engine for suppliers. Formulators targeting passenger service fills gain the most predictable, recurring aftermarket revenue stream.

Light Commercial Vehicles run high daily mileage in delivery and trade use, raising coolant consumption per vehicle. Operators schedule frequent service to avoid downtime. This creates dependable replacement demand. Suppliers who bundle coolant with fleet maintenance programs lock in LCV accounts and stabilize order flow across economic cycles.

Heavy Commercial Vehicles carry large cooling systems and demanding thermal loads over long hauls. As reported by ACEA, roughly 6 million trucks operated on EU roads in 2023 at an average age of 14.1 years, sustaining strong aftermarket need. This aging fleet guarantees repeat coolant sales, rewarding suppliers with heavy-duty formulations and wide distributor reach.

Electric Vehicles require specialized low-conductivity thermal fluids rather than conventional engine coolant. In June 2025, Castrol India signed an MoU with Tata Motors Commercial Vehicles to build a used-oil circularity ecosystem, signaling supplier moves toward sustainable powertrain fluids. This reframes EV as an adjacent opportunity. Suppliers who qualify EV-grade fluids early convert a threat into new premium revenue.

Sales Channel Analysis

Aftermarket dominates with 67.50% due to recurring service and replacement demand.

In 2025, Aftermarket held a dominant market position in the By Sales Channel segment of Automotive Engine Oil Coolant Market, with a 67.50% share. The aftermarket captures repeat coolant purchases across the vehicle lifecycle. This recurring pattern makes it the most resilient revenue pool. Suppliers with wide distributor and workshop networks convert fleet aging into steady, high-frequency sales.

OEM channels supply factory-fill coolant tied directly to vehicle production volumes and manufacturer specifications. Winning an OEM approval locks a supplier into every new unit built. This delivers large contracts but narrow margins. Formulators use OEM wins to build brand credibility, then monetize that trust across the higher-margin aftermarket segment.

Key Market Segments

By Product Type

- Ethylene Glycol-Based Coolants

- Propylene Glycol-Based Coolants

- Glycerin-Based Coolants

- Others

By Technology

- Organic Additive Technology (OAT)

- Inorganic Additive Technology (IAT)

- Hybrid Organic Acid Technology (HOAT)

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (EV)

By Sales Channel

- Aftermarket

- OEM

Regional Analysis

Asia Pacific Dominates the Automotive Engine Oil Coolant Market with a Market Share of 38.40%, Valued at USD 3.08 Billion

Asia Pacific leads the market with a 38.40% share worth USD 3.08 Billion, anchored by the world’s largest vehicle base. Data from OICA shows China recorded 34.39 million vehicle sales in 2025, making it the biggest coolant-consuming market. This concentration rewards suppliers with local blending capacity, since proximity lowers freight cost and shortens delivery cycles for high-volume regional accounts.

Latin America ranks among the faster-growing regions on rising vehicle production. As reported by ACEA, South American car production increased 1.7% in 2024, with Brazil producing about 1.9 million cars. This output growth expands service-fill demand. Suppliers entering early through local distributors capture share before the region’s aftermarket consolidates around established brands and pricing hardens.

North America remains a mature, high-value region despite softer output. ACEA found that North America produced 11.4 million cars in 2024, down 3.2% from 2023. In November 2025, Shell confirmed its EV-Plus Thermal Fluid enabled single-fluid cooling for a full battery electric powertrain. This innovation signals where advanced demand shifts, so regional suppliers must invest in EV thermal capability to defend value.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

The largest active push on the baseline comes from the expanding global in-use vehicle fleet, led by Asia Pacific, which held about 47.8% of global automotive engine oil demand in 2026. Rising vehicle miles across India, Indonesia, and Vietnam compound this. India’s vehicle production crossed 5.8 million units by 2025, with commercial output growing near 8 to 9%, driving recurring coolant top-ups and full-drain service demand.

Coolant use tracks engine operating hours, not just new sales, so the parc above 1.5 billion registered vehicles creates a stickier consumption base. This gives formulators aftermarket volume predictability. As a result, blenders run longer production, lift capacity use, and recover margin by 150 to 200 basis points versus spot orders. Against a 3.95% baseline CAGR, this driver adds an estimated 1.40%.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Global Vehicle Parc & Rising VMT | +1.40% | Asia Pacific, Latin America, Middle East & Africa | Short term (≤ 2 years) |

| OAT & HOAT Technology Upgrade Cycle | +0.85% | Global — led by North America & Europe | Medium term (2–4 years) |

| Rising Engine Maintenance Awareness in Emerging Markets | +0.65% | India, Southeast Asia, Sub-Saharan Africa | Short term (≤ 2 years) |

| Growth of Commercial Vehicle & Heavy-Duty Fleet Segments | +0.55% | China, India, Brazil, North America | Medium term (2–4 years) |

| Escalating Thermal Demands from Turbocharged & GDI Engines | +0.50% | Global — led by Europe & East Asia OEM clusters | Short term (≤ 2 years) |

Restraints

Pure battery electric vehicles remove the ethylene glycol engine coolant circuit entirely, deleting a multi-litre replaced fluid from each converted vehicle. In Europe, BEV share of new passenger car sales reached about 15 to 18% by 2025, while Euro 7 rules entering force on 29 November 2026 raise ICE compliance costs. China’s NEV penetration crossed 50% of monthly passenger sales in 2024, compressing the replacement coolant market in the largest volume market.

Each BEV replacing an ICE vehicle removes roughly 4 to 8 litres of coolant per drain and up to 3 to 4 drain events over ownership, cutting revenue by about USD 25 to 60 per vehicle. This means OEM aftermarket channels already see coolant SKU sales fall 10 to 15% yearly in high-BEV markets. Against the 3.95% baseline, this restraint drags an estimated 1.10% and will intensify.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery EV Penetration Displacing ICE Coolant Demand | -1.10% | Europe, China, North America | Medium term (2–4 years) |

| Extended Drain Interval Technology Reducing Volume Per Vehicle | -0.70% | Global — concentrated in mature OEM markets | Short term (≤ 2 years) |

| Chemical Restriction Legislation (REACH & Equivalent) on Additives | -0.45% | European Union, United Kingdom, South Korea | Short term (≤ 2 years) |

| Volatile Ethylene Glycol Feedstock Pricing Compressing Margins | -0.35% | Global — most acute in import-dependent markets | Short term (≤ 2 years) |

| Proliferation of Sub-Standard & Counterfeit Coolant Products | -0.30% | South Asia, Southeast Asia, Sub-Saharan Africa | Medium term (2–4 years) |

Challenges

The aftermarket spans coexisting standards, IAT, OAT, HOAT, and Si-OAT, each with distinct chemistry, compatibility windows, and service intervals from 2 years to 5 years. Mixing them risks gel formation and corrosion. In 2025, HOAT alone held about 42.5% of the global coolant concentrate market, yet distributors must stock 8 to 14 separate SKUs, inflating working capital by an estimated 20 to 30% versus a single-chemistry market.

The strain compounds down the chain. A mid-tier blender in India serves legacy IAT fleets, OAT passenger cars, and HOAT SUVs at once, with wrong-coolant claims eroding margin by 3 to 5% per reject batch. This means regional players need sustained R&D near 4 to 6% of revenue for universal platforms. As a result, installer training can take 5 to 7 years to cover fragmented networks.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Multi-Standard SKU Fragmentation Complexity | -0.60% | Global — most acute in aftermarket distribution | Long term (≥ 4 years) |

| Geopolitical Supply Chain Concentration Risk | -0.50% | Global — feedstock dependency on Middle East & East Asia | Medium term (2–4 years) |

| Technical Workforce & Lab Capability Gaps | -0.35% | South Asia, Southeast Asia, Africa | Long term (≥ 4 years) |

| Corrosion Inhibitor Shelf-Life & Degradation Management | -0.30% | Tropical & high-humidity markets — India, ASEAN, West Africa | Medium term (2–4 years) |

| OEM Specification Proliferation & Approvals Backlog | -0.25% | Europe, North America, Japan | Long term (≥ 4 years) |

Opportunities

EV and hybrid platforms need dielectric, low-conductivity thermal fluids that traditional coolant makers have not yet monetized at scale. These fluids require conductivity below 100 µS/cm, nitrite-free packages, and stability from -40°C to +105°C. The EV thermal management fluids segment posted a CAGR above 29% from 2025 to 2026, growing from USD 2.77 Billion to USD 3.61 Billion in one year, a trajectory ICE players largely ceded to specialty entrants.

An established blender pivoting 15 to 20% of capacity to EV-grade batches could lift gross margin by 8 to 14 percentage points versus commodity ethylene glycol coolant. This reflects premium additive complexity and long-term OEM supply deals. Fewer than 30% of legacy formulators hold qualified EV thermal fluid products today. As a result, early movers gain a certification advantage window of 2 to 4 years before the segment commoditizes.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| EV & Hybrid Dielectric Thermal Fluid Adjacency | +1.50% | China, Europe, North America, South Korea | Medium term (2–4 years) |

| Bio-Based & Renewable Coolant Formulations | +0.80% | Europe, North America, Japan, Australia | Long term (≥ 4 years) |

| Coolant-as-a-Service & Fleet Subscription Models | +0.55% | North America, Europe, GCC | Medium term (2–4 years) |

| Underpenetrated Rural & Tier-3 Aftermarket in South & Southeast Asia | +0.50% | India, Indonesia, Vietnam, Philippines | Short term (≤ 2 years) |

| Industrial & Off-Highway Coolant Cross-Segment Expansion | +0.40% | Global — led by North America, Australia, Middle East | Long term (≥ 4 years) |

Key Company Insights

Shell plc positions itself at the technology frontier of powertrain thermal management. The company confirmed its EV-Plus Thermal Fluid with PurePlus Technology enabled single-fluid cooling for a full battery electric powertrain. This advance links its legacy coolant base to the fast-growing EV segment. As reported by IEA, electric car sales exceeded 17 million units globally in 2024, so Shell’s early EV fluid capability protects it against ICE volume decline.

BP p.l.c. (Castrol) is reshaping its portfolio through active divestment. In May 2025, BP began selling its Castrol lubricants business, valued near USD 8 to 10 Billion, as part of asset restructuring. This move signals a strategic pivot away from mature fluids toward core energy assets. For buyers, the sale creates uncertainty over supply continuity, while rivals gain a window to capture Castrol’s aftermarket share.

Key Players

- Shell plc

- ExxonMobil Corporation

- BP p.l.c. (Castrol)

- Chevron Corporation

- BASF SE

- TotalEnergies SE

- Prestone Products Corporation

- Valvoline Inc.

- PEAK Commercial & Industrial

- Evans Cooling Systems

- Pentosin GmbH

- Fuchs Petrolub SE

Recent Developments

- September 2025 – BASF launched GLYSANTIN ELECTRIFIED Low Electrical Conductivity Coolants for electric vehicle battery cooling systems, expanding its automotive coolant portfolio.

- October 2025 – Prestone launched its brand platform “The Future Runs on Prestone” alongside next-generation coolant products focused on sustainable mobility and advanced thermal management.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 8.02 Billion |

| Forecast Revenue (2035) | USD 11.82 Billion |

| CAGR (2026-2035) | 3.95% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Ethylene Glycol-Based Coolants, Propylene Glycol-Based Coolants, Glycerin-Based Coolants, Others), By Technology (Organic Additive Technology (OAT), Inorganic Additive Technology (IAT), Hybrid Organic Acid Technology (HOAT)), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Electric Vehicles (EV)), By Sales Channel (Aftermarket, OEM) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Shell plc, ExxonMobil Corporation, BP p.l.c. (Castrol), Chevron Corporation, BASF SE, TotalEnergies SE, Prestone Products Corporation, Valvoline Inc., PEAK Commercial & Industrial, Evans Cooling Systems, Pentosin GmbH, Fuchs Petrolub SE |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |