Global Anti Spam Software Market Size, Share Analaysis Report By Component(Software, Services), By Deployment (On-premises, Cloud-based), By Enterprise Size(Small & Medium Enterprises (SMEs), Large Enterprises), By Industry (Vertical, BFSI, IT & Telecom, Healthcare, Government, Retail, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Jul 2025

- Report ID: 153924

- Number of Pages: 239

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

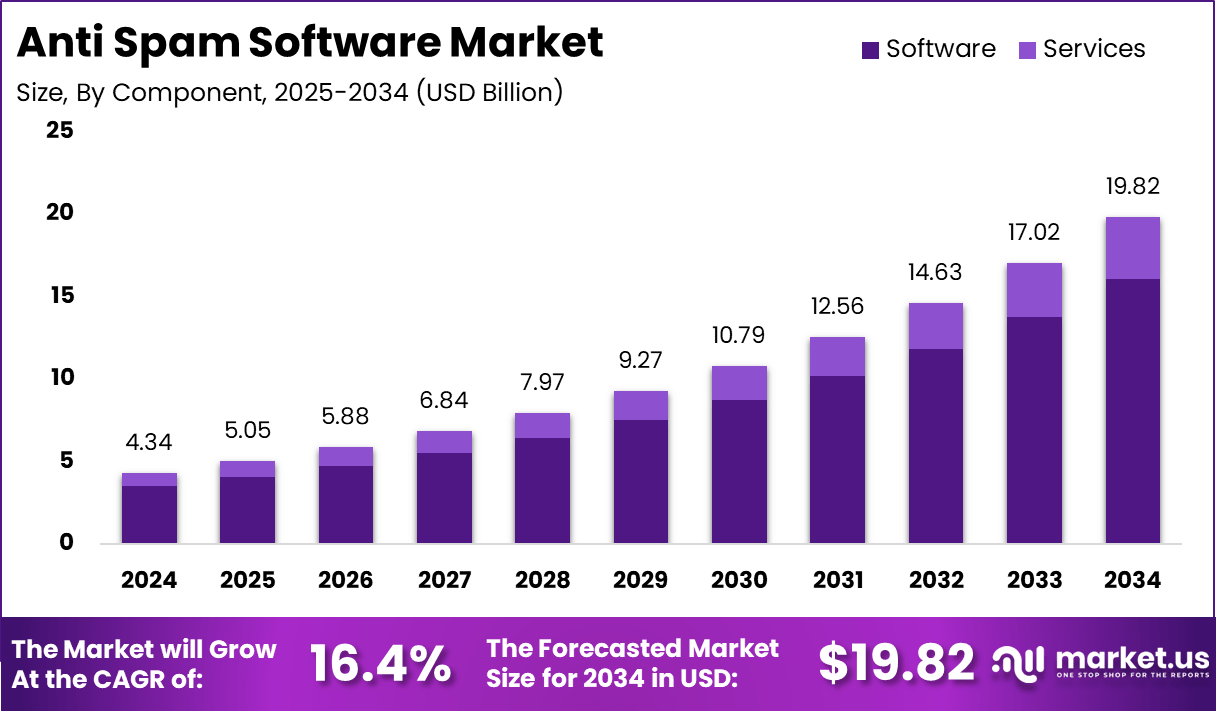

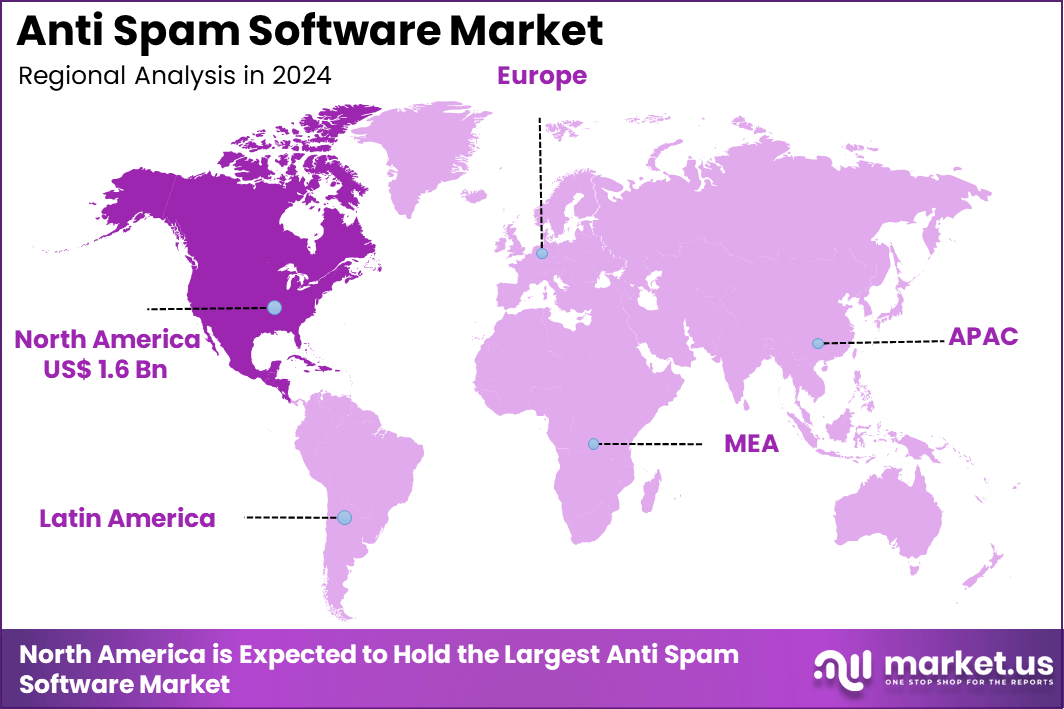

The Global Anti Spam Software Market size is expected to be worth around USD 19.82 Billion By 2034, from USD 4.34 billion in 2024, growing at a CAGR of 16.4% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 40% share, holding USD 1.6 Billion revenue.

The Anti‑Spam Software Market reflects a sector dedicated to solutions that automatically detect and filter unwanted or malicious email communications. Core techniques such as Bayesian filtering, rule‑based detection, DNS‑based blacklists, authentication protocols and real‑time content analysis are commonly deployed. Deployment models span both on‑premise systems and cloud‑based platforms that integrate seamlessly with email infrastructures, enabling organizations to maintain productivity and security.

Based on data from 9cv9 Blog, Organizations using Keepnet Labs have seen up to a 90% drop in risky employee behavior, showing how well training works against phishing. In Australia, cybercrime rose by 13% in 2022, with around 76,000 cases, highlighting the urgent need for stronger anti-spam tools. Keepnet also earned a 95% willingness-to-recommend score, proving customer trust and strong results in email threat protection.

The platform has helped reduce phishing attack risk by 92% and cut security incidents by 85%, offering real value for businesses aiming to stay secure. Companies using these tools avoid losses of nearly $1 million each year due to fewer spam-related breaches. Also, about 75% of organizations now rely on AI-based spam filters, which block threats faster and more accurately than old systems.

Market Size and Growth

Report Features Description Market Value (2024) USD 4.34 Bn Forecast Revenue (2034) USD 19.82 Bn CAGR(2025-2034) 16.4% Leading Segment Software: 81% Largest Market North America [40% Market Share] Largest Country US: USD 1.6 Billion Market Revenue, CAGR: 20.6% The growth drivers in this market can be attributed to rapidly escalating volumes of spam and associated cybersecurity threats, notably phishing and malware delivery via email. The burden on enterprise productivity and the risk of data compromise necessitate robust anti‑spam defenses. Additional impetus is provided by regulatory frameworks enforcing data protection standards and explicit consent for email communication. These combined pressures have catalyzed investment in advanced anti‑spam tools.

Demand for anti-spam software has surged as both private and public sectors contend with the escalating number of malicious emails targeting sensitive information and financial data. Increasing cloud adoption, more diverse digital channels, and hybrid work models fuel demand further. This expanding need is clear across sectors, from finance – where customer trust is paramount – to healthcare and education, where privacy and compliance are non-negotiable.

Key Takeaways

- By component, Software dominated with an 81% share, driven by demand for advanced spam filters, AI-powered classification engines, and machine learning integration.

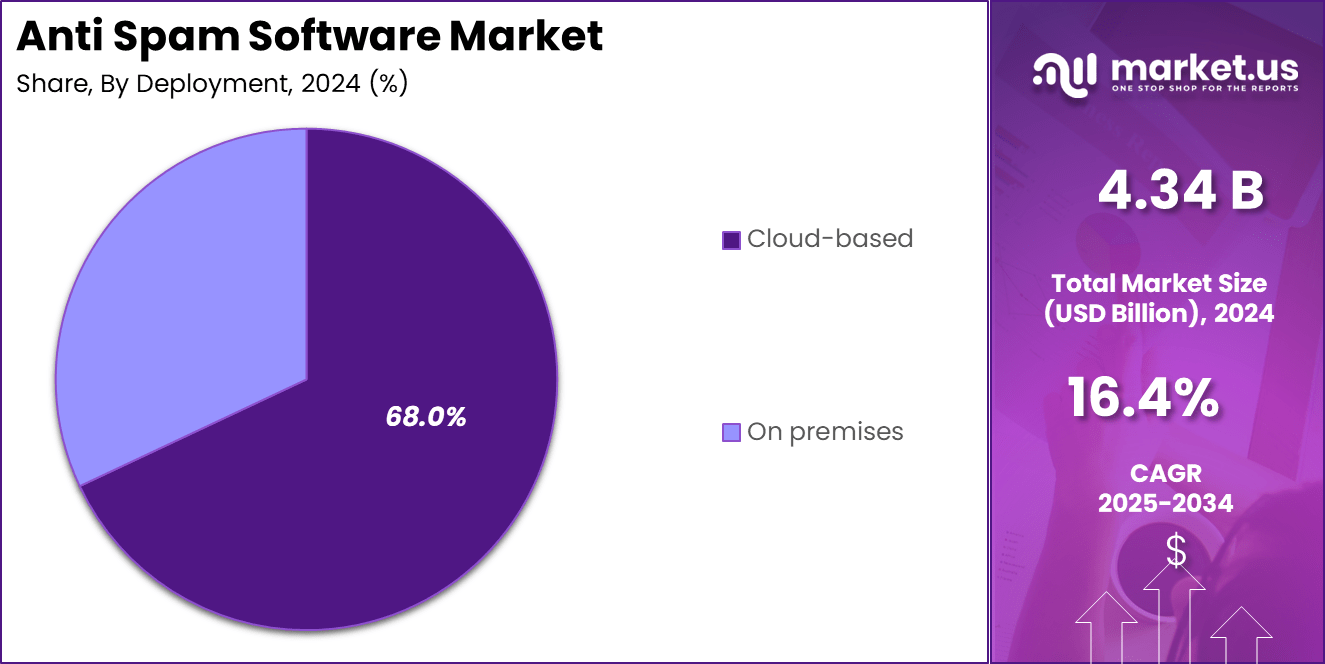

- Cloud-based deployment accounted for 68%, highlighting a growing preference for scalable, remotely managed security solutions.

- Large Enterprises held a commanding 60% share, leveraging anti-spam software to secure vast email volumes and sensitive communications.

- The IT & Telecom industry led all verticals with 34%, as this sector faces higher exposure to email-based threats and stringent data protection requirements.

- In 2024, North America led the global market with over 40% share, generating USD 1.6 Billion in revenue.

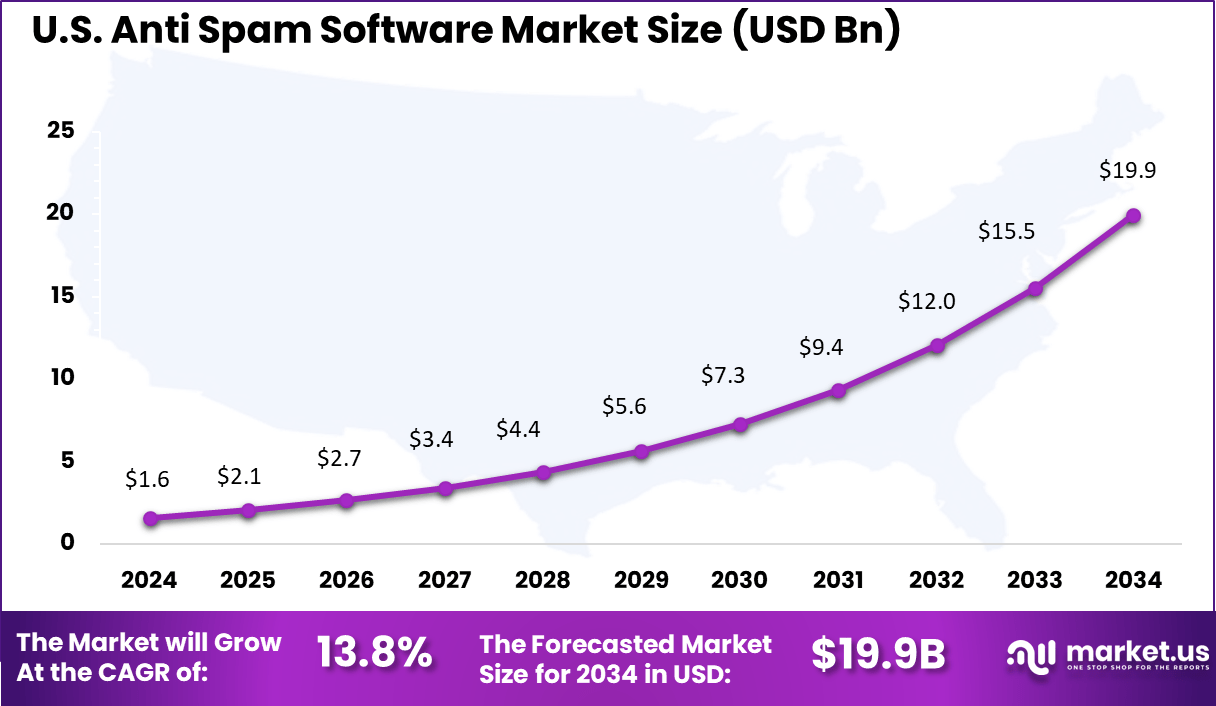

- The United States alone contributed USD 1.6 Billion, registering a CAGR of 13.8%, reflecting strong cybersecurity mandates and enterprise-scale adoption.

Size of the U.S. Market

The U.S. Anti Spam Software Market was valued at USD 1.6 Billion in 2024 and is anticipated to reach approximately USD 19.9 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 13.8% during the forecast period from 2025 to 2034.

In 2024, the United States held a dominant position in the global anti-spam software market, largely due to its advanced cybersecurity infrastructure and widespread enterprise digitization. The country faces a high volume of cyber threats, particularly phishing attacks and email-based malware, which significantly elevates the demand for robust anti-spam solutions.

Businesses across sectors such as finance, healthcare, and government rely heavily on secure communication systems, reinforcing the need for proactive email protection technologies. Furthermore, the prevalence of remote and hybrid work arrangements has intensified the push for scalable, cloud-based anti-spam tools across devices and locations.

In 2024, North America held a dominant market position, capturing more than a 40% share, accounting for USD 1.6 billion in revenue. This regional leadership is driven by the high volume of targeted email threats and advanced phishing attacks, particularly in the United States.

Businesses in North America are under growing pressure to safeguard sensitive communications, especially in sectors such as banking, insurance, healthcare, and public administration. With email still serving as a core communication tool, enterprises are rapidly adopting intelligent spam-filtering systems that integrate with broader cybersecurity frameworks.

The region’s strong regulatory environment also plays a crucial role. Laws like the CAN-SPAM Act in the U.S. and CASL in Canada mandate strict oversight on unsolicited emails, encouraging the deployment of compliance-focused anti-spam software. North America also benefits from high investments in artificial intelligence and cloud computing, which are being used to develop adaptive, real-time filtering technologies.

Component Analysis

In 2024, The software segment accounted for a dominant 81% share in the Anti-Spam Software Market. This leadership can be attributed to the flexibility, scalability, and real-time threat detection capabilities provided by software solutions. These platforms often come with automated updates, behavioral learning features, and customizable filters that can adapt to evolving spam tactics.

Additionally, the integration of artificial intelligence and machine learning has made software tools more accurate in identifying and blocking phishing attempts, spoofing attacks, and malicious attachments. With increased enterprise reliance on email communication, the need for intelligent and continuously updated software tools has grown.

Unlike hardware-based filters that require physical infrastructure and regular maintenance, software products are easier to deploy and update. Enterprises also prefer multi-layered software-based protection to ensure continuity in business communication and reduce operational disruption. These benefits have made software the default choice for both individual and enterprise-level email security needs.

Deployment Analysis

In 2024, Cloud-based deployment held the leading position with a share of 68% in 2024. Cloud-based anti-spam tools are widely preferred for their low upfront cost, rapid deployment capabilities, and flexible scalability. These solutions enable users to access real-time spam filtering updates and threat intelligence from centralized data centers without having to manage hardware or complex IT environments.

For global businesses with distributed teams, cloud-based tools ensure consistent spam protection across geographies. The growing adoption of hybrid work models and remote operations has increased the dependence on cloud platforms for secure communication.

Cloud deployment also supports easier compliance with international regulations through centrally managed audit trails and data encryption. Moreover, vendors are increasingly offering Software-as-a-Service models that simplify integration with enterprise email services, further reinforcing cloud-based deployment as the dominant approach.

Enterprise Size Analysis

In 2024, Large enterprises represented 60% of the market share due to their higher risk exposure and greater investment capacity in cybersecurity. These organizations typically handle vast volumes of email communication and are frequent targets for advanced phishing and ransomware attacks.

To safeguard sensitive business data and maintain operational continuity, large enterprises deploy comprehensive anti-spam solutions as part of broader email security infrastructures. These firms also operate under stringent regulatory frameworks that require robust data protection measures.

The need to comply with standards such as GDPR, HIPAA, and PCI-DSS drives the adoption of advanced spam detection tools with reporting and logging features. Furthermore, large enterprises often integrate anti-spam tools with endpoint security, identity verification, and threat intelligence platforms to create a holistic defense posture. This makes them the primary consumers of enterprise-grade anti-spam technologies.

Industry Vertical Analysis

In 2024, the IT & Telecom sector emerged as the dominant vertical, capturing 34% of the overall market. This industry is inherently dependent on continuous and secure digital communication, making it highly vulnerable to spam-related risks. With email being a primary mode of customer support, technical correspondence, and project coordination, organizations in this sector require uninterrupted, secure messaging environments.

Anti-spam software ensures this by filtering out harmful content and reducing the threat of social engineering attacks. Furthermore, IT & Telecom firms are typically early adopters of cloud and AI technologies, which align with the features of next-generation anti-spam solutions.

Their digital-first infrastructure makes it easier to integrate cloud-based spam filtering tools that support real-time monitoring, adaptive filtering, and compliance tracking. As the sector continues to grow and digitize, its reliance on secure email systems will further drive the adoption of anti-spam software solutions.

Growth Factors

Growth Factor Description Rising Cybersecurity Threats More attacks like phishing, malware, and data breaches are pushing businesses to adopt anti-spam software for protection. Increase in Email Usage A sharp rise in business and personal emails makes filtering essential to productivity and security. Remote Work and Digitalization As companies shift to digital work, protecting remote communications from spam becomes critical. Regulatory Compliance Requirements Laws like GDPR and CAN-SPAM force organizations to invest in email security to avoid fines and maintain trust. Advanced Technologies (AI/ML) Machine learning and AI have made spam detection smarter and more accurate, improving defenses against new threats. Key Features and Latest Trends

Key Feature / Trend Description AI and Machine Learning Detection These technologies help software adapt quickly to new spam tactics and improve detection rates. Cloud-Based Anti-Spam Solutions Cloud deployments offer scalability and easy updates, making them attractive, especially for small businesses. Real-Time Threat Analysis Software now monitors and reacts instantly to suspicious messages, limiting damage. Integration with Other Security Tools Anti-spam solutions are now built to work with broader cybersecurity suites and existing email platforms. User-Friendly Management Improved dashboards and easy setup reduce the burden on IT staff. Focus on Reducing False Positives New features aim to stop junk mail but let real messages through, so productivity isn’t hurt. Drivers

The growth of the Anti-Spam Software Market is driven by several key factors, primarily the increasing volume and sophistication of email-based cyber threats such as phishing, ransomware, and business email compromise (BEC). With over 91% of cyberattacks originating from email, organizations are prioritizing advanced spam filtering to safeguard sensitive data and ensure operational security.

The widespread adoption of cloud-based email platforms like Microsoft 365 and Google Workspace has further accelerated the demand for scalable, real-time anti-spam solutions. Additionally, strict data protection regulations such as GDPR, HIPAA, and CCPA are compelling businesses to implement robust email security systems to maintain compliance.

The integration of AI and machine learning into anti-spam tools has significantly enhanced detection accuracy and adaptability against evolving threats. Moreover, the shift to remote and hybrid work environments, increased use of mobile email access, and the availability of cost-effective SaaS models are contributing to widespread adoption, especially among SMEs. These drivers collectively reinforce the critical need for efficient and intelligent anti-spam software across sectors.

Restrains

Despite its strong growth, the Anti-Spam Software Market faces several restraining factors that can limit its adoption. One of the primary challenges is the high cost of advanced enterprise-grade solutions, which may be unaffordable for small and medium-sized businesses with limited IT budgets. Additionally, false positives- where legitimate emails are mistakenly marked as spam – can disrupt communication and reduce user trust in the software.

The complexity of integration with existing IT systems, especially in legacy environments, can also slow down deployment and adoption. In some cases, a lack of awareness or understanding about the evolving nature of email threats leads to underinvestment in proper spam protection, particularly in smaller organizations.

Furthermore, the constant evolution of spam techniques – such as AI-generated phishing emails – makes it difficult for traditional filters to keep up, requiring frequent updates and monitoring. These factors collectively create barriers to broader implementation, particularly in cost-sensitive or less tech-savvy environments.

Opportunities

The Anti-Spam Software Market presents several promising opportunities as digital communication continues to expand. One of the most significant opportunities lies in the integration of artificial intelligence (AI) and machine learning (ML) to create smarter, self-learning spam filters that can detect and respond to emerging threats in real time.

As more organizations transition to cloud-based infrastructures, there is growing demand for cloud-native anti-spam solutions that offer flexibility, scalability, and remote protection. The rise of mobile email usage and Bring Your Own Device (BYOD) policies also opens up opportunities for mobile-focused anti-spam tools.

Additionally, increasing regulatory pressures around data privacy and cybersecurity are encouraging businesses, especially in regulated industries like finance and healthcare, to invest in more comprehensive email protection. Emerging markets, where digital transformation is accelerating, offer untapped potential for vendors to expand their reach. These factors create a favourable environment for innovation and expansion within the anti-spam software space.

Challenges

The Anti-Spam Software Market faces several challenges that could impact its growth and effectiveness. One of the biggest challenges is the rapid evolution of spam and phishing techniques, often powered by AI, which makes it difficult for traditional filters to keep up.

Cybercriminals are constantly finding new ways to bypass detection systems, making spam harder to identify without causing false positives. Another major challenge is the difficulty in balancing security with user experience – overly aggressive filters can block legitimate emails, disrupting communication and causing frustration.

Another challenge is the high rate of false positives, where legitimate emails are mistakenly classified as spam. This can disrupt business communication, lower productivity, and cause frustration among users, particularly in organizations that rely heavily on external email traffic. Striking the right balance between security and usability remains a critical concern. Integration complexities also pose a hurdle, especially for large enterprises with diverse IT environments.

Key Market Segments

By Component

- Software

- Services

By Deployment

- On-premises

- Cloud-based

By Enterprise Size

- Small & Medium Enterprises (SMEs)

- Large Enterprises

By Industry Vertical

- BFSI

- IT & Telecom

- Healthcare

- Government

- Retail

- Others

Key Regions and Countries Covered

-

North America

- The US

- Canada

-

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

-

APAC

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

-

Latin America

- Brazil

- Mexico

- Rest of Latin America

-

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Several key players dominate the anti-spam software market by offering advanced email protection, threat detection, and filtering capabilities. Symantec Corporation, Trend Micro Inc., and Cisco Systems Inc. are known for integrating artificial intelligence and machine learning into their spam detection engines. These companies focus on minimizing phishing attacks and spam threats in enterprise and consumer settings.

Vendors such as Barracuda Networks Inc., Proofpoint Inc., Mimecast Limited, and Sophos Group plc offer strong cloud-based spam protection tools. These firms have prioritized multi-layered filtering, sandboxing, and email encryption as key strategies. Their scalable solutions are popular among SMEs and global enterprises.

Other notable participants include Fortinet Inc., McAfee LLC, Kaspersky Lab, F-Secure Corporation, Comodo Group Inc., and GFI Software. These vendors continuously enhance their spam filtering algorithms and integrate anti-malware features. Emerging companies like SpamTitan Technologies, ZEROSPAM Security Inc., AppRiver LLC, Clearswift Ltd., and Hornetsecurity GmbH are gaining traction by offering customized, compliance-ready solutions.

Top Key Players

- Symantec Corporation

- Trend Micro Inc.

- Cisco Systems Inc.

- Barracuda Networks Inc.

- Proofpoint Inc.

- Mimecast Limited

- Sophos Group plc

- Fortinet Inc.

- McAfee LLC

- Kaspersky Lab

- F-Secure Corporation

- Comodo Group Inc.

- GFI Software

- SolarWinds MSP

- FireEye Inc.

- SpamTitan Technologies

- ZEROSPAM Security Inc.

- AppRiver LLC

- Clearswift Ltd.

- Hornetsecurity GmbH

- Other Key Players

Recent Developments

- June 2025: TitanHQ’s SpamTitan (Skellig 9.07) update garnered industry awards, achieving a malware and phishing catch rate of 100%, a spam catch rate of 99.9%, and a negligible false positive rate. Enhanced display name anti-spoofing and more granular control features highlight the leap in usability and security for managed service providers and business users alike.

- September 2024: Bharti Airtel introduced India’s first network-native, AI-powered spam detection system. This solution scans over 1 trillion records in real time, flags 100 million spam calls and 3 million SMSes each day, and aims to drastically reduce consumer exposure to digital spam. It automatically protects Airtel’s customers nationwide, requiring no user intervention.

Report Scope

Report Features Description Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component(Software, Services), By Deployment (On-premises, Cloud-based), By Enterprise Size(Small & Medium Enterprises (SMEs), Large Enterprises), By Industry (Vertical, BFSI, IT & Telecom, Healthcare, Government, Retail, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Symantec Corporation, Trend Micro Inc., Cisco Systems Inc., Barracuda Networks Inc., Proofpoint Inc., Mimecast Limited, Sophos Group plc, Fortinet Inc., McAfee LLC, Kaspersky Lab, F-Secure Corporation, Comodo Group Inc., GFI Software, SolarWinds MSP, FireEye Inc., SpamTitan Technologies, ZEROSPAM Security Inc., AppRiver LLC, Clearswift Ltd., Hornetsecurity GmbH, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Symantec Corporation

- Trend Micro Inc.

- Cisco Systems Inc.

- Barracuda Networks Inc.

- Proofpoint Inc.

- Mimecast Limited

- Sophos Group plc

- Fortinet Inc.

- McAfee LLC

- Kaspersky Lab

- F-Secure Corporation

- Comodo Group Inc.

- GFI Software

- SolarWinds MSP

- FireEye Inc.

- SpamTitan Technologies

- ZEROSPAM Security Inc.

- AppRiver LLC

- Clearswift Ltd.

- Hornetsecurity GmbH

- Other Key Players

Our Clients

- 153924

- Jul 2025