Global Aircraft Ignition System Market Size, Share, Growth Analysis By Type (Electric Ignition, Magneto Ignition), By Aircraft Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, UAV), By Component (Igniters, Ignition Leads, Spark Plugs, Exciters, Others), By Engine Type (Turbofan Engine, Turboprop Engine, Turbojet Engine, Piston Engine), By End User (OEMs, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 11973

- Number of Pages: 344

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

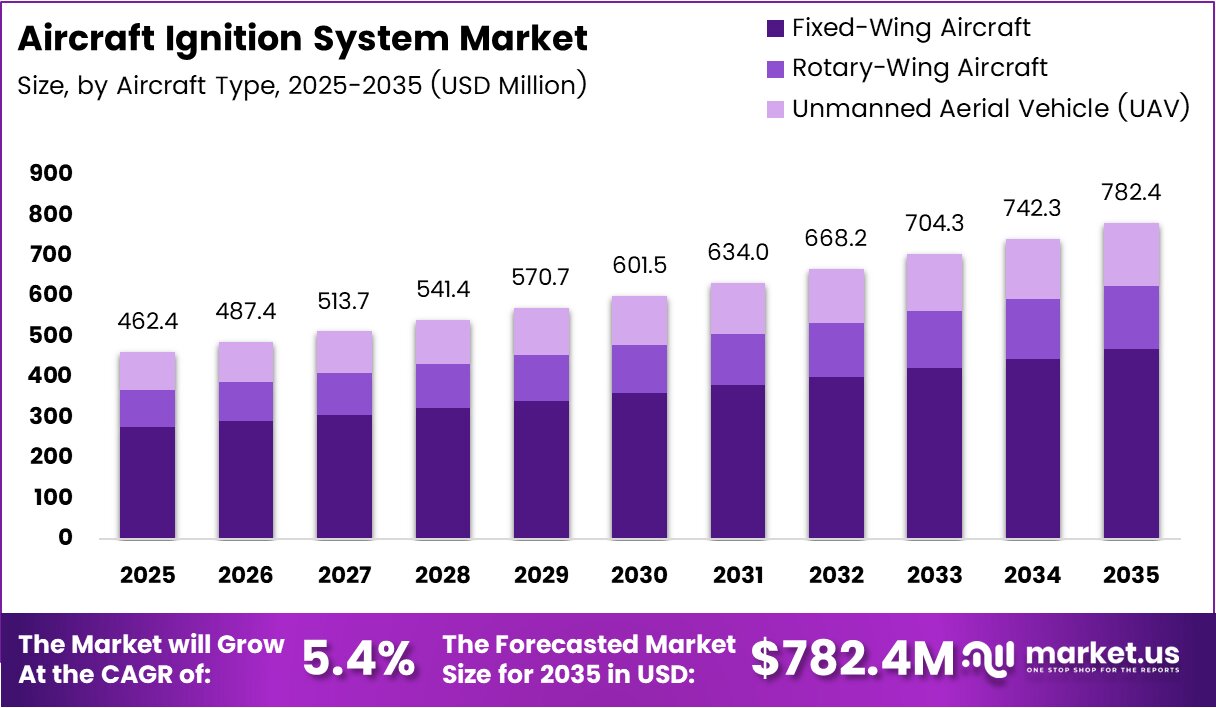

Global Aircraft Ignition System Market size is expected to be worth around USD 782.4 Million by 2035 from USD 462.4 Million in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

The aircraft ignition system market covers components that initiate fuel combustion across piston, turboprop, turbofan, and turbojet engines. These systems include igniters, spark plugs, ignition leads, and exciters. Their reliability directly determines engine start performance and in-flight safety across commercial, military, and unmanned aviation platforms.

Military modernization programs and rising commercial air travel continue to push OEM procurement cycles forward. Fixed-wing aircraft account for 72.9% of the market, reflecting the sheer scale of commercial fleet expansion globally. Airlines and defense agencies are now retiring older mechanical systems and replacing them with electronic alternatives, compressing the procurement window for legacy component suppliers.

Electric ignition systems hold 67.3% market share, signaling a structural preference among aircraft manufacturers for digital, programmable ignition over traditional magneto-based systems. This shift reflects OEM demand for systems with lower weight, better fuel efficiency, and integration capability with modern avionics platforms.

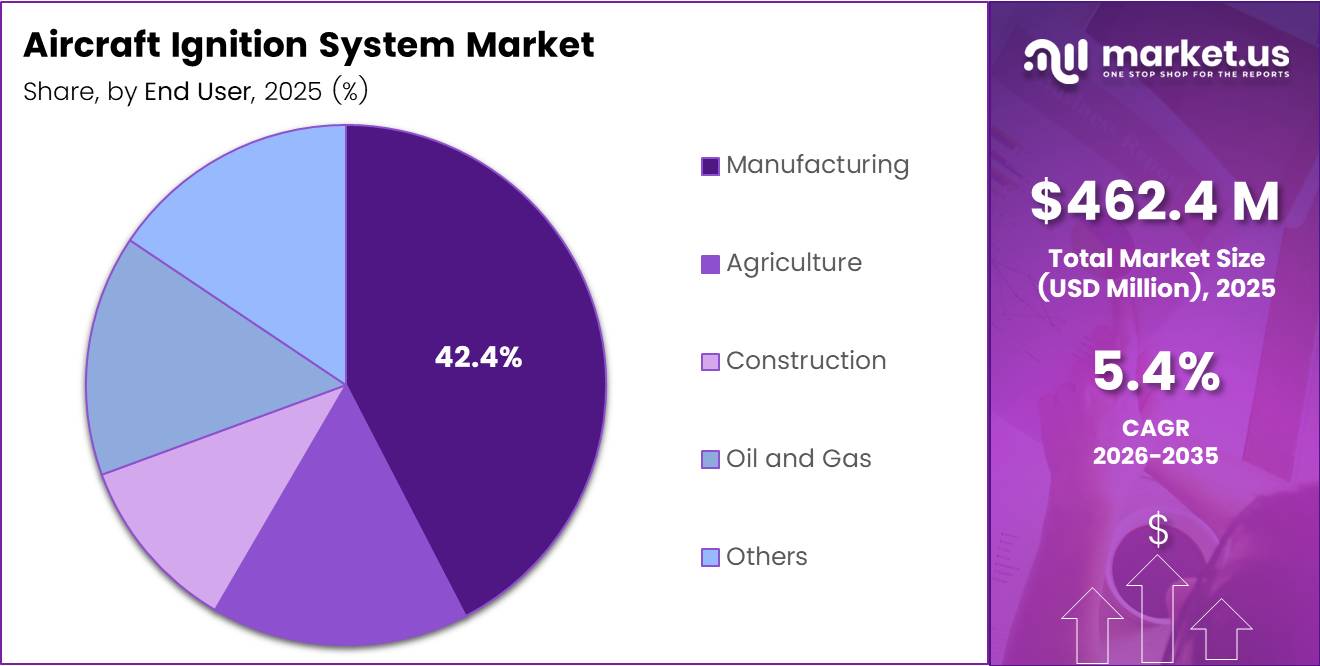

OEMs represent 77.1% of end-user demand, which means the majority of ignition system revenue is locked into long-term aircraft production contracts. This makes aftermarket activity a secondary but increasingly strategic segment, particularly as aging fleets require component replacements outside OEM warranty periods.

According to ResearchGate, the ignition probability within 10 seconds and approximately 700 J of arc energy exceeded 50% in controlled arc ignition tests on aircraft cables, with a 5% ignition probability recorded at just 2.38 seconds and 255 J for 100W direct current arc tests. This data signals that wiring system vulnerabilities create measurable safety risk — reinforcing demand for certified, precision-tested ignition components across all aircraft platforms.

According to ScienceDirect, a statistical model built on 1,350 experimental data points was developed to assess ignition probability of leaked aircraft fuel on hot surfaces under continuous parameter changes. This research directly informs how component manufacturers design ignition systems to operate safely under real-world thermal and fuel-leak scenarios — raising the technical bar for market entrants.

Key Takeaways

- The Aircraft Ignition System Market was valued at USD 462.4 Million in 2025 and is forecast to reach USD 782.4 Million by 2035.

- The market grows at a CAGR of 5.4% during the forecast period 2026 to 2035.

- Electric Ignition leads the By Type segment with a 67.3% market share in 2025.

- Fixed-Wing Aircraft dominates the By Aircraft Type segment with a 72.9% share.

- Igniters hold the largest component share at 37.8% within the By Component segment.

- Turbofan Engine leads the By Engine Type segment with a 43.2% share.

- Original Equipment Manufacturers (OEMs) account for 77.1% of end-user demand.

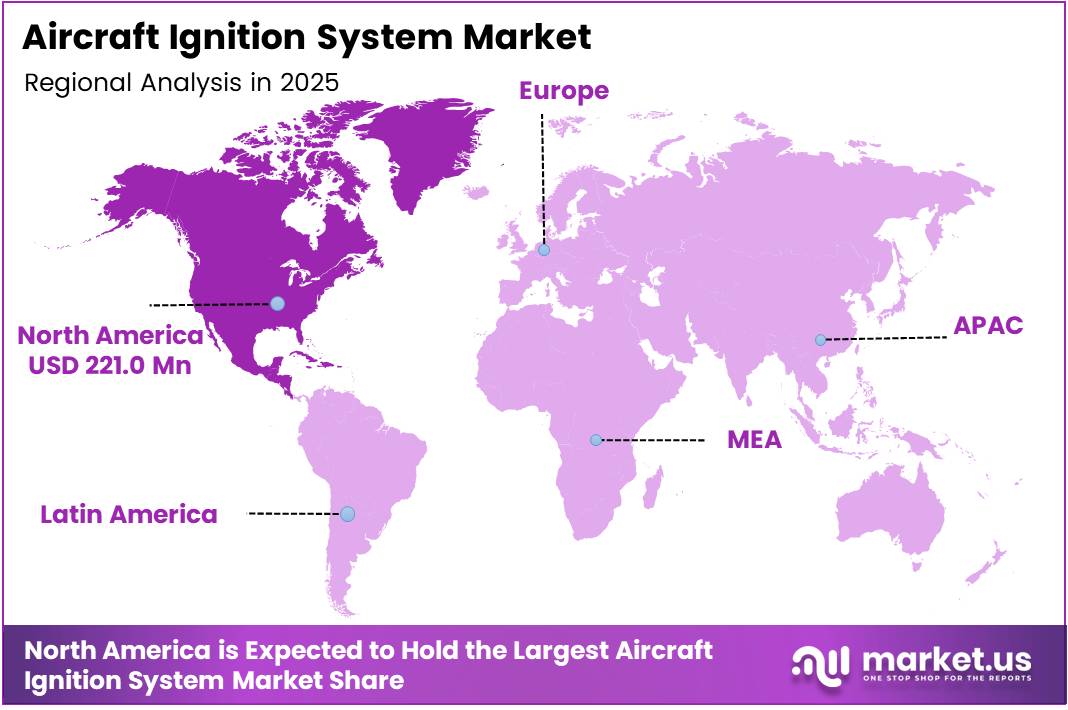

- North America dominates regional demand with a 47.80% share, valued at USD 221.0 Million.

Product Analysis

Electric Ignition dominates with 67.3% due to digital integration and fuel efficiency advantages.

In 2025, Electric Ignition held a dominant market position in the By Type segment of the Aircraft Ignition System Market, with a 67.3% share. Aircraft manufacturers prefer electronic systems because they deliver precise timing control, reduce fuel consumption, and integrate directly with modern avionics. This structural advantage makes electric ignition the default choice for new aircraft programs at major OEMs.

Magneto Ignition serves as the established baseline for piston-engine aircraft and legacy military platforms. Magnetos operate independently of the aircraft’s electrical system, making them a reliable fallback in power-failure scenarios. However, the March 2025 FAA PMA approval of Hartzell Engine Technologies’ PowerUP magnetos as direct replacements for Bendix S-20 and S-200 series units shows this segment is consolidating around certified, drop-in alternatives.

Aircraft Type Analysis

Fixed-Wing Aircraft dominates with 72.9% due to commercial fleet scale and OEM contract volume.

In 2025, Fixed-Wing Aircraft held a dominant market position in the By Aircraft Type segment of the Aircraft Ignition System Market, with a 72.9% share. Commercial passenger and cargo aircraft fleets represent the largest installed base of ignition systems globally. Airlines operating high-frequency routes create predictable, high-volume replacement cycles that underpin stable OEM and aftermarket revenue streams.

Rotary-Wing Aircraft carries concentrated demand from military and emergency services operators. Helicopter ignition systems require high-reliability specifications under vibration and thermal stress. This segment benefits from defense budget allocations directed at fleet upgrades, particularly in rotary-wing military platforms undergoing modernization across NATO member states.

Unmanned Aerial Vehicle (UAV) differentiates through miniaturized ignition requirements suited to fuel-powered drone platforms. As defense and logistics operators scale UAV fleets, demand for lightweight, durable ignition components with extended service intervals rises. This sub-segment remains smaller in absolute value but carries above-average growth potential as autonomous aviation programs expand procurement budgets.

Component Analysis

Igniters dominate with 37.8% due to critical role in engine start and relight sequences.

In 2025, Igniters held a dominant market position in the By Component segment of the Aircraft Ignition System Market, with a 37.8% share. Igniters function as the primary energy-discharge components in turbine engine ignition sequences, including high-altitude relight events. Their high replacement frequency across commercial turbofan fleets drives consistent aftermarket revenue independent of new aircraft production cycles.

Ignition Leads function as the high-voltage transmission pathway between exciters and igniters. Lead degradation under thermal cycling creates a steady replacement demand, particularly on engines with high daily cycle counts. Their per-unit cost is lower than igniters, but replacement frequency across large commercial fleets sustains meaningful revenue volume for component distributors.

Spark Plugs serve as the ignition interface in piston and turboprop engines, where combustion reliability under varying altitudes and temperatures is critical. Certified aviation spark plugs face strict FAA and EASA approval requirements, limiting the number of qualified suppliers and sustaining price discipline within this component category.

Exciters generate the high-energy electrical discharge required to trigger igniters during engine start sequences. Modern exciters are increasingly integrated with digital engine control units, shifting them from standalone hardware toward software-configurable components. This integration trend raises switching costs and strengthens OEM-supplier relationships.

Others within the component segment include wiring harnesses, mounting hardware, and secondary ignition support equipment. These components generate recurring revenue through scheduled maintenance intervals and are often bundled into MRO service contracts, providing a stable revenue base that is less sensitive to new aircraft build rates.

Engine Type Analysis

Turbofan Engine dominates with 43.2% due to commercial aviation fleet concentration.

In 2025, Turbofan Engine held a dominant market position in the By Engine Type segment of the Aircraft Ignition System Market, with a 43.2% share. Turbofan engines power the majority of commercial narrow-body and wide-body aircraft in active service. High daily flight cycles on routes served by carriers in Asia, North America, and Europe generate above-average ignition component wear rates and replacement demand.

Turboprop Engine platforms anchor regional aviation markets, particularly in Africa, Southeast Asia, and remote connectivity routes. Turboprop ignition systems benefit from fleet renewal programs at regional carriers adopting newer-generation aircraft. The reliability requirements for short-cycle, high-frequency operations give certified ignition suppliers a structural pricing advantage in this segment.

Turbojet Engine applications remain concentrated in legacy military aircraft and early-generation business jets. Replacement parts for turbojet ignition systems carry long service life cycles and limited new-program exposure. However, military sustainment contracts provide predictable, multi-year revenue for suppliers holding approved parts manufacturer certifications.

Piston Engine ignition systems serve the general aviation segment, including training aircraft, private pilots, and light sport platforms. This sub-segment drives meaningful aftermarket demand because piston-engine fleets are older on average and require frequent magneto and spark plug replacements. Suppliers with broad FAA/PMA approval portfolios hold a distinct competitive advantage here.

End-User Analysis

OEMs dominate with 77.1% due to long-term aircraft production contract lock-in.

In 2025, Original Equipment Manufacturers (OEMs) held a dominant market position in the By End User segment of the Aircraft Ignition System Market, with a 77.1% share. OEM procurement decisions are made years ahead of aircraft delivery, embedding preferred ignition suppliers into production supply chains. This creates high switching costs and long contract durations that effectively limit competitor access to the majority of market revenue.

Aftermarket demand captures the remaining end-user revenue through MRO activity, unscheduled replacements, and fleet upgrades. As commercial and military fleets age beyond original warranty periods, aftermarket spend per aircraft increases. Suppliers with FAA/PMA approvals for drop-in replacements gain ground in this segment by offering certified alternatives at competitive pricing against OEM original parts.

Key Market Segments

By Type

- Electric Ignition

- Magneto Ignition

By Aircraft Type

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

- Unmanned Aerial Vehicle (UAV)

By Component

- Igniters

- Ignition Leads

- Spark Plugs

- Exciters

- Others

By Engine Type

- Turbofan Engine

- Turboprop Engine

- Turbojet Engine

- Piston Engine

By End User

- Original Equipment Manufacturers (OEMs)

- Aftermarket

Drivers

Military Modernization and Commercial Fleet Expansion Drive OEM Ignition System Procurement

Global defense budgets are directing capital toward fighter jet upgrades and next-generation aircraft platforms, directly increasing OEM orders for certified ignition components. Commercial aviation network expansion — particularly across Asia-Pacific and Middle East routes — is simultaneously adding new turbofan-powered aircraft to service. Together, these forces sustain multi-year procurement pipelines for ignition system suppliers.

The shift toward digital and electronic ignition systems accelerates OEM adoption decisions. Aircraft manufacturers building fuel-efficient narrow-body and wide-body platforms now specify electronic ignition as a standard requirement rather than an option. In March 2024, Hartzell Engine Technologies launched the POWERUP Aircraft Ignition Systems product line, including FAA/PMA-approved magnetos, harnesses, replacement parts, and repair kits — a clear signal that suppliers are investing to meet certified product demand at scale.

According to arXiv, a statistical ignition probability model for lean-burn aeronautical gas turbines demonstrated that ignition behaves as a stochastic process, with experimental ignition maps recoverable through probabilistic flame kernel trajectory analysis. This research validates the technical complexity behind modern ignition design and explains why airlines and OEMs pay premium prices for components that deliver consistent, repeatable ignition performance across variable operating conditions.

Restraints

High Technical Complexity and Stringent Certification Requirements Slow Ignition System Commercialization

Modern aircraft ignition systems require FAA, EASA, and military airworthiness certification before entering commercial service. This approval process adds 18 to 36 months to product development timelines and significant cost to qualification programs. Smaller component suppliers face an uneven barrier: large OEM-aligned vendors can absorb certification costs, while independent entrants struggle to compete on approved parts lists.

The maintenance burden of electronic ignition systems adds operational cost at the airline and MRO level. Unlike magnetos, which technicians can inspect and overhaul using established procedures, electronic ignition units often require specialized diagnostic equipment and factory-trained personnel. This raises labor cost per maintenance event and extends aircraft-on-ground time, which airline operators translate directly into route revenue loss.

Regulatory constraints also limit the pace of technology adoption. Aviation authorities require extensive flight-test evidence and failure-mode analysis before approving new ignition architectures on type-certificated aircraft. This means that even well-funded developers of next-generation ignition solutions face a constrained commercialization path — slowing the rate at which market participants can replace legacy product revenue with higher-margin advanced system sales.

Growth Factors

Hybrid Aircraft Programs and IoT Integration Open New Revenue Streams for Ignition Suppliers

Hybrid and electric propulsion programs now include ignition requirements for range-extender combustion engines and turbogenerators. This creates a new design and certification workstream for component suppliers outside their traditional aircraft categories. In May 2025, Hartzell Engine Technologies acquired E-MAG, a specialist in electronic aircraft ignition systems, with plans to advance certification for general aviation — directly targeting this emerging propulsion segment.

IoT-enabled predictive maintenance platforms are creating a secondary revenue layer for ignition system providers. Suppliers who embed sensor technology into ignition components can offer subscription-based condition monitoring services alongside hardware sales. This shifts the revenue model from one-time part sales toward recurring service contracts, improving margin visibility and deepening customer relationships with airline MRO operations.

According to arXiv, turbulence was identified as the dominant variable affecting successful ignition events in aircraft engine relight simulations, demonstrating that stochastic flow conditions significantly influence ignition outcomes. This finding supports the business case for intelligent ignition systems that adapt firing sequences to real-time engine conditions — a capability that opens premium pricing opportunities for suppliers investing in adaptive ignition hardware.

Emerging Trends

Lightweight Materials, AI Diagnostics, and Modular Design Reshape Aircraft Ignition Architecture

Aircraft manufacturers apply weight reduction targets to every subsystem, and ignition components are no exception. Suppliers now develop ignition leads, exciters, and mounting hardware using advanced alloys and composite materials to cut system weight without compromising thermal or electrical performance. Lower ignition system weight directly reduces aircraft fuel burn — a measurable benefit that OEM procurement teams quantify in procurement decisions.

AI-driven diagnostic platforms now analyze ignition performance data in real time, identifying degradation patterns before component failure occurs. Airlines adopting these tools shift from time-based replacement schedules to condition-based maintenance, reducing unnecessary part changes and extending component service life. According to ITM Conferences, experimental studies show that ignition on hot surfaces depends critically on surface temperature and fuel behavior — confirming that condition monitoring tools must account for dynamic thermal variables to deliver reliable failure predictions.

Modular ignition system architectures allow airlines and MRO operators to upgrade individual components without replacing entire assemblies. This design philosophy lowers total lifecycle cost and reduces aircraft-on-ground time during maintenance. For suppliers, modular platforms create recurring upgrade revenue as new ignition technologies reach certification — converting each aircraft in service into a long-term revenue opportunity rather than a one-time sale.

Regional Analysis

North America Dominates the Aircraft Ignition System Market with a Market Share of 47.80%, Valued at USD 221.0 Million

North America holds a 47.80% share valued at USD 221.0 Million, anchored by the United States’ position as the world’s largest single-country aviation market. Dense commercial airline networks, active military procurement programs, and a mature FAA certification infrastructure concentrate both OEM production and aftermarket MRO activity within this region — giving established suppliers a structural advantage over international competitors.

Europe Aircraft Ignition System Market Trends

Europe’s ignition system demand centers on commercial narrowbody and widebody MRO activity, driven by Airbus production programs and high-frequency short-haul operations. EASA’s dual-certification requirement with FAA creates a two-step approval burden for non-European suppliers. However, established European MRO hubs in Germany, France, and the UK provide consistent aftermarket volume for certified ignition component distributors.

Asia Pacific Aircraft Ignition System Market Trends

Asia Pacific represents the fastest-expanding regional demand base, driven by fleet additions at carriers in China, India, and Southeast Asia. Airline order backlogs at Boeing and Airbus translate directly into multi-year OEM ignition component supply commitments for the region. Additionally, growing defense budgets in Japan, South Korea, and India are directing spend toward military aircraft upgrades requiring certified ignition system replacements.

Middle East and Africa Aircraft Ignition System Market Trends

The Middle East hosts major hub carriers that operate large widebody turbofan fleets on long-haul international routes, creating above-average per-aircraft ignition component consumption rates. Gulf state aviation authorities are aligning certification standards closer to EASA frameworks, which progressively reduces the regulatory friction for European and North American ignition suppliers seeking market access in this region.

Latin America Aircraft Ignition System Market Trends

Latin America’s ignition system market relies heavily on aftermarket supply for aging commercial and regional aircraft fleets. Brazilian and Mexican carriers operate a mix of turbofan and turboprop platforms that generate steady replacement demand. Infrastructure constraints and local currency volatility limit large-scale OEM procurement activity, keeping the region weighted toward lower-margin parts distribution rather than first-fit supply contracts.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Aero Accessories positions itself as a specialist distributor and overhaul provider for general aviation ignition components. Its competitive advantage lies in depth of FAA/PMA-approved inventory and fast-turnaround MRO services for piston and turboprop operators. In markets where aircraft-on-ground time directly costs operators revenue, suppliers with wide approved parts inventories and rapid fulfillment capability hold measurable pricing power.

Champion Aerospace has built its market position through a broad portfolio of spark plugs, igniters, and exciter systems covering piston and turbine engine applications. Its strength lies in simultaneous coverage of OEM production supply and aftermarket replacement demand — a dual-channel strategy that reduces revenue concentration risk and maintains commercial relationships across the full aircraft lifecycle from new-build through retirement.

Electroair differentiates through electronic ignition system development specifically targeting the general aviation retrofit market. Its systems replace conventional magnetos on certified piston aircraft, offering fuel efficiency and maintenance interval improvements that appeal directly to cost-conscious private operators. This retrofit positioning allows Electroair to capture aftermarket revenue without competing head-to-head against OEM supply chain incumbents on new aircraft programs.

Hartzell Engine Technologies has executed the most visible acquisition strategy in this market during the past 18 months. Its acquisition of E-MAG in May 2025 and the March 2025 FAA PMA approval for PowerUP magnetos as direct Bendix S-20 replacements signal a deliberate move to own both the legacy magneto replacement market and the next-generation electronic ignition segment simultaneously — a two-track strategy that hedges against technology transition timing risk.

Key Players

- Aero Accessories

- Air Power Inc.

- Champion Aerospace

- Electroair

- G31

- Hartzell Engine Technologies

- Sky Dynamics

- SureFly

- Tempest Aero Group

- Trans Digm Group

Recent Developments

- December 2024 — Woodward signed a definitive agreement to acquire the Safran Electronics & Defense electromechanical actuation business based in the United States, Mexico, and Canada. This move strengthened Woodward’s aerospace electromechanical and electronic controls portfolio, expanding its footprint across certified aircraft systems adjacent to ignition and engine control platforms.

- July 2025 — Woodward completed the acquisition of Safran’s North American electromechanical actuation business, adding intellectual property, operations assets, talent, and long-term customer agreements to its portfolio. The deal includes Horizontal Stabilizer Trim Actuation systems used on aircraft including the Airbus A350, deepening Woodward’s integration into major commercial aircraft programs.

Report Scope

Report Features Description Market Value (2025) USD 462.4 Million Forecast Revenue (2035) USD 782.4 Million CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Electric Ignition, Magneto Ignition), By Aircraft Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, UAV), By Component (Igniters, Ignition Leads, Spark Plugs, Exciters, Others), By Engine Type (Turbofan Engine, Turboprop Engine, Turbojet Engine, Piston Engine), By End User (OEMs, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Aero Accessories, Air Power Inc., Champion Aerospace, Electroair, G31, Hartzell Engine Technologies, Sky Dynamics, SureFly, Tempest Aero Group, Trans Digm Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Aircraft Ignition System MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Aircraft Ignition System MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Aero Accessories

- Air Power Inc.

- Champion Aerospace

- Electroair

- G31

- Hartzell Engine Technologies

- Sky Dynamics

- SureFly

- Tempest Aero Group

- Trans Digm Group

Our Clients

- 11973

- Feb 2026