Global Aeroponics Market Size, Share and Report Analysis By Solutions (Organic, Conventional), By Crop Type (Leafy Greens, Herbs And Microgreens, Fruits And Flowers), By Equipment (Lighting, Sensor, Irrigation Component, Climate Control, Others), By Application (Indoor, Outdoor), By End Use (Commercial, Residential) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 178549

- Number of Pages: 340

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

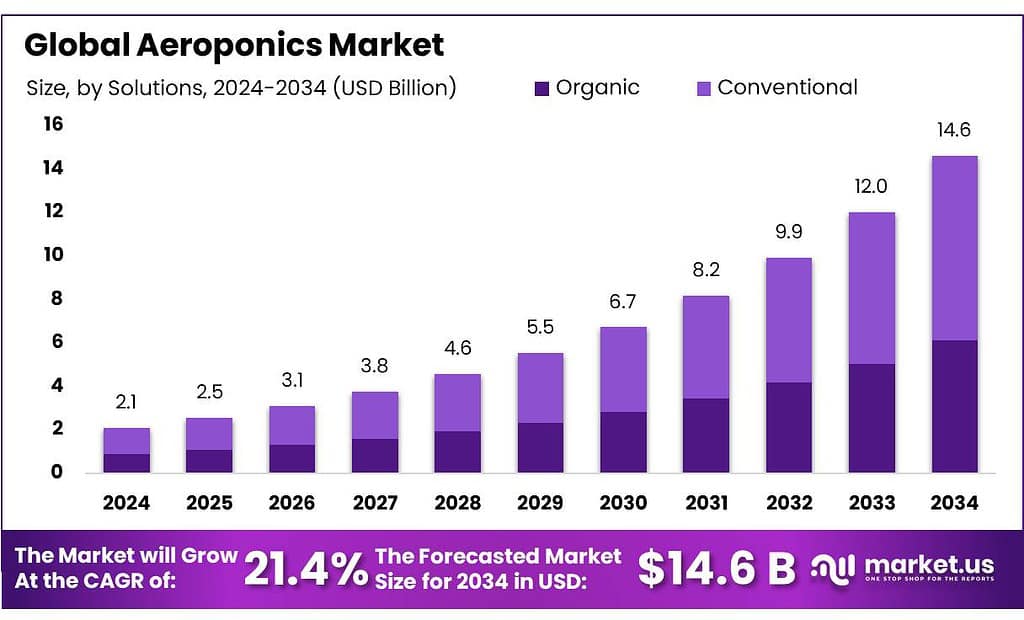

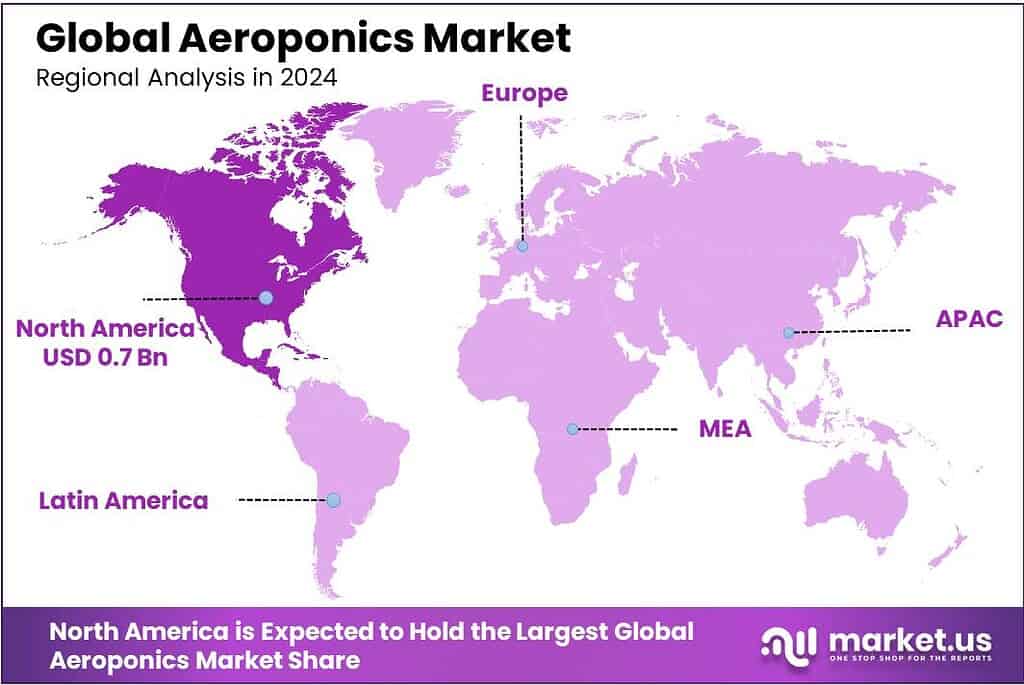

Global Aeroponics Market size is expected to be worth around USD 14.6 Billion by 2034, from USD 2.1 Billion in 2024, growing at a CAGR of 21.4% during the forecast period from 2025 to 2034. In 2024 North America held a dominant market position, capturing more than a 36.6% share, holding USD 0.7 Billion in revenue.

Aeroponics is a controlled-environment farming method where plants are grown without soil and their roots hang in air while a nutrient-rich mist is delivered in short cycles. In practice, aeroponics sits inside the broader controlled-environment agriculture toolbox and is used mainly for high-value, fast-turn crops. The core industrial promise is consistency: growers can target repeatable quality and year-round output by managing light, temperature, humidity, CO₂, and nutrient delivery, instead of relying on seasonal weather.

- The UN projects the global population to reach about 9.7 billion by 2050 —two trends that push food systems to supply more fresh produce closer to cities with tighter logistics and lower spoilage. At the same time, food system inefficiency remains a large global drag: FAO’s widely cited estimate puts food lost or wasted at roughly 1.3 billion tonnes per year. From a food-security lens, the challenge is still material—FAO reported about 673 million people experienced hunger in 2024.

Key driving factors are anchored in resource efficiency and food-system resilience. Water is a central pressure point: major international sources consistently note agriculture accounts for roughly 70% of global freshwater withdrawals, making efficiency gains strategically important for food production. In technical performance terms, peer-reviewed work on vertical farming water efficiency has reported that aeroponics increased water use efficiency by 114% compared with an ebb-and-flow system (a direct, quantitative indicator of the potential resource advantage when systems are well-designed and managed).

- Government and institutional support is also becoming more explicit, which reduces adoption friction. Public funding references also appear in official parliamentary documents: for example, Maharashtra sanctioned ₹96.11 lakh (2023–24) for a project on vertical farming/hydroponics/aeroponics via KVK Baramati, and ₹106.22 lakh is referenced under RKVY allocations for related activity.

Key Takeaways

- Aeroponics Market size is expected to be worth around USD 14.6 Billion by 2034, from USD 2.1 Billion in 2024, growing at a CAGR of 21.4%.

- Conventional held a dominant market position, capturing more than a 58.3% share.

- Leafy Greens held a dominant market position, capturing more than a 56.8% share.

- Irrigation Component held a dominant market position, capturing more than a 37.4% share.

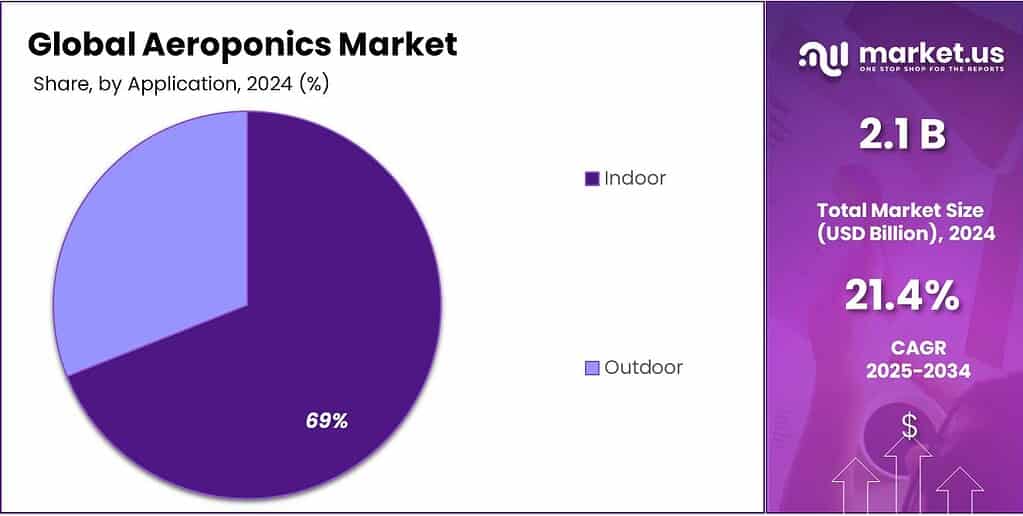

- Indoor held a dominant market position, capturing more than a 69.1% share.’

- Commercial held a dominant market position, capturing more than a 76.2% share.

- North America dominates Aeroponics with 36.6% share (USD 0.7 Bn) in 2024, backed by strong indoor-farming scale and retail demand.

By Solutions Analysis

Conventional leads the Aeroponics Market with 58.3% share in 2024 driven by cost efficiency and operational familiarity

In 2024, Conventional held a dominant market position, capturing more than a 58.3% share. This strong presence reflects the continued preference for proven, easy-to-manage aeroponic systems that are already well understood by commercial growers. Conventional systems are widely used in greenhouses, indoor farms, and research facilities because they are simpler to install and maintain compared to more advanced high-pressure setups. Farmers value their reliability, especially for leafy greens, herbs, and nursery crops where consistent misting and steady root oxygen exposure are enough to deliver stable yields.

By Crop Type Analysis

Leafy Greens dominate the Aeroponics Market with 56.8% share in 2024 driven by fast growth cycles and steady urban demand

In 2024, Leafy Greens held a dominant market position, capturing more than a 56.8% share. This leadership is largely linked to the natural suitability of aeroponics for crops like lettuce, spinach, kale, and arugula, which grow quickly and respond well to mist-based nutrient delivery. Growers prefer leafy greens because they have short harvest cycles, allowing multiple crop rotations within a year. This improves revenue stability and makes better use of indoor farming space. The controlled environment of aeroponics also helps maintain consistent leaf quality, color, and texture, which is important for retail and food service buyers.

By Equipment Analysis

Irrigation Component leads with 37.4% share in 2024 driven by its central role in nutrient delivery

In 2024, Irrigation Component held a dominant market position, capturing more than a 37.4% share. This segment forms the backbone of any aeroponic system, as precise misting and nutrient delivery directly determine plant health and yield quality. Pumps, nozzles, pipes, timers, and pressure regulators work together to ensure that roots receive a consistent nutrient spray at controlled intervals. Since aeroponics depends entirely on accurate moisture and nutrient control, growers prioritize reliable irrigation hardware when setting up or expanding facilities.

By Application Analysis

Indoor applications lead with 69.1% share in 2024 as controlled environments drive reliable production

In 2024, Indoor held a dominant market position, capturing more than a 69.1% share. This strong position reflects the natural alignment between aeroponics and indoor farming systems. Aeroponic technology depends on precise control of temperature, humidity, light, and nutrient delivery, which indoor facilities can manage effectively throughout the year. Growers prefer indoor setups because they reduce exposure to unpredictable weather, pests, and seasonal changes. This stability supports consistent crop cycles and predictable harvest schedules, which are important for meeting supply contracts with retailers and food service operators.

By End Use Analysis

Commercial use dominates with 76.2% share in 2024 as large-scale growers drive adoption

In 2024, Commercial held a dominant market position, capturing more than a 76.2% share. This leadership reflects the increasing involvement of professional growers, agribusiness firms, and controlled environment agriculture operators investing in aeroponic systems for large-scale production. Commercial farms focus on maximizing yield per square foot while maintaining uniform crop quality, and aeroponics supports this goal through precise nutrient delivery and faster crop cycles. The ability to produce consistent harvests throughout the year makes it attractive for meeting long-term supply agreements with supermarkets, restaurants, and food distributors.

Key Market Segments

By Solutions

- Organic

- Conventional

By Crop Type

- Leafy Greens

- Herbs & Microgreens

- Fruits & Flowers

By Equipment

- Lighting

- Sensor

- Irrigation Component

- Climate Control

- Others

By Application

- Indoor

- Outdoor

By End Use

- Commercial

- Residential

Emerging Trends

Aeroponics is moving from “pilot tech” to “policy-backed, insurable indoor farming”

A clear latest trend in aeroponics is the shift toward formal, government-supported adoption, where indoor farms are treated less like experimental projects and more like a recognized production system—with clearer subsidy norms, risk frameworks, and compliance pathways. This matters because aeroponics is highly controlled and asset-heavy: once a grower invests in an indoor setup, they need confidence that financing, protection, and operating rules will not be “grey areas.” In 2024 and into 2025, that confidence is improving in several markets, and it is helping aeroponics move from small trials into structured rollouts.

This kind of formal inclusion is more than a line in a document—it signals to growers, integrators, and lenders that soilless cultivation is being positioned as a mainstream horticulture tool. What strengthens this trend further is that operational cost norms are being spelled out. MIDH cost norms include Hydroponics and Aeroponics at Rs. 350 per sq. mt., with assistance at 50% for a maximum area of 1000 sqm per beneficiary, and the document notes 15% higher rates for specific priority geographies.

This policy-and-insurance shift is happening alongside steady growth in controlled environment production footprints, which creates a stronger base for aeroponics vendors and operators. USDA ERS reported that U.S. CEA operations increased from 1,476 in 2009 to 2,994 in 2019, and production volumes rose 56% to 7.86 million hundredweight over that period. When an industry is expanding in scale like this, it becomes easier for aeroponics to spread through training, standard operating procedures, supplier ecosystems, and buyer familiarity—even if each farm chooses different technical designs.

Drivers

Water scarcity is pushing growers toward ultra-efficient aeroponics

A major driver for aeroponics is simple: fresh water is becoming harder to secure for farming, and producers are under pressure to grow more food with less water. Global institutions consistently point out how big agriculture’s water footprint is. FAO notes that agriculture accounts for 70% of freshwater withdrawals worldwide, which means even small efficiency gains in farming have a large impact at country and basin level. UNESCO’s World Water Development Report echoes the same order of magnitude, stating agriculture accounts for roughly 70% of withdrawals globally.

Aeroponics works by keeping plant roots suspended and delivering nutrients as a fine mist. This targeted delivery matters because it avoids the “extra” water that often gets lost in soil systems through evaporation, runoff, and deep percolation. NASA’s published spinoff materials highlight why the method is frequently discussed in water-efficiency conversations: aeroponic systems can reduce water usage by 98% and fertilizer usage by 60%, and can even remove the need for pesticides in controlled settings. Those numbers are powerful for commercial operators because water savings are not just a sustainability story—they translate into operational resilience.

This water-efficiency push is not happening in isolation. Governments are also starting to name aeroponics explicitly in programs linked to protected cultivation and modern horticulture. In India, the revised MIDH guideline document notes that “new components like Hydroponics and Aeroponics will also be promoted under the Mission,” which signals growing policy comfort with soilless cultivation as a practical route to higher resource productivity.

Restraints

High initial investment and energy costs limit aeroponics expansion

One of the most significant restraining factors slowing the wider adoption of aeroponics is the high initial cost and ongoing energy burden that growers must bear to set up and operate these systems. Unlike traditional outdoor farming, aeroponic cultivation demands advanced infrastructure, climate control systems, artificial lighting, pumps, sensors, and automation tools, all of which require substantial capital before a single crop is planted. Controlled-environment agriculture has long faced economic hurdles due to these infrastructure demands.

Government initiatives do help to an extent, as seen where some agricultural policies now include support for protected cultivation and modern farming technologies. However, incentives such as tax breaks, grants, and training programs are still limited or unevenly distributed, which means many growers who could benefit most from aeroponics cannot easily cross the initial investment threshold. For aeroponics to reach mainstream scale, policymakers and industry stakeholders need to focus on reducing financial barriers, expanding renewable energy integration to lower operating costs, and broadening technical training programs so that both new and experienced farmers can confidently operate these advanced systems.

Technical complexity compounds this issue. Aeroponic systems are more sensitive than soil-based methods, requiring careful calibration of nutrient delivery, humidity, oxygen levels, and misting schedules. Without skilled technicians and reliable remote monitoring systems, early adopters risk crop failures that can negate expected returns—and these skilled professionals and smart hardware carry their own cost premiums.

Opportunity

Supplying fast-growing cities with local, fresher greens while cutting supply-chain waste

One major growth opportunity for aeroponics is scaling local, indoor production for urban consumers. The demand pull is structural: cities are getting bigger, and food systems are being asked to deliver fresher produce with fewer supply disruptions. The United Nations reports that 55% of the world’s population lives in urban areas today, and this is projected to rise to 68% by 2050. That shift matters for aeroponics because leafy greens and herbs—common aeroponic crops—are highly perishable and lose value quickly when they travel long distances. As more people live in cities, retailers and foodservice operators increasingly want steady, local supply that is less dependent on seasons and long-haul logistics. Source: UN DESA urbanization projections.

This urban demand links directly to a second, very practical opportunity: reducing food loss and waste. FAO has estimated that about one-third of all food produced for human consumption is lost or wasted each year, meaning a large share of resources (water, energy, land, labor) never turns into eaten food. Aeroponics, when deployed near consumption centers, can shorten the time from harvest to shelf and reduce damage in transport and storage—two common points where leafy produce gets discarded. It does not “solve” food waste on its own, but it can reduce the portion caused by long, fragile distribution chains for fresh greens. Source: FAO food loss/waste estimate.

The commercial runway for this opportunity is also visible in how controlled-environment agriculture is expanding in the U.S., creating a ready ecosystem for aeroponics. USDA’s Economic Research Service notes that U.S. CEA operations (a category that includes greenhouses and other controlled production methods) grew from 1,476 operations in 2009 to 2,994 in 2019, while production volume increased to 7.86 million hundredweight over the same period. This growth signals that more growers, buyers, and service partners are already comfortable with indoor production—making it easier for aeroponics to scale as a “next step” where higher water efficiency and tighter control are needed. Source: USDA ERS chart of note on CEA growth.

Regional Insights

North America dominates Aeroponics with 36.6% share (0.7 Bn) in 2024, backed by strong indoor-farming scale and retail demand

In 2024, North America dominated the Aeroponics Market with a 36.6% share (0.7 Bn), supported by the region’s established controlled-environment agriculture (CEA) base, strong year-round fresh-produce demand, and mature greenhouse supply chains. The U.S. already has sizable commercial greenhouse activity that helps aeroponics scale faster through retrofits and new indoor builds; USDA’s Economic Research Service reported greenhouse tomato sales valued at $470 million, showing the commercial depth of protected cultivation that aeroponics can plug into for leafy greens and herbs.

Canada reinforces this momentum with concentrated greenhouse production hubs and clear commercial scale. Statistics Canada reported that Ontario accounted for 67.5% of greenhouse fruit and vegetable sales in 2023, highlighting how clustered production ecosystems can accelerate technology adoption by improving access to skills, suppliers, and distribution partners.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AeroFarms is a U.S.-based vertical farming company specializing in aeroponic growing systems for leafy greens and microgreens. The company was founded in 2004 and operates advanced indoor farms using patented mist-based root technology. It has developed more than 550 plant varieties in controlled environments. AeroFarms’ facilities use up to 95% less water compared to field farming methods. The company focuses on pesticide-free production and year-round supply. Headquarters: United States. Core Segment: Commercial Indoor Aeroponics. Primary Crop Focus: Leafy Greens.

Aponic Ltd. develops vertical aeroponic farming solutions for urban food production. Founded in 2015, the company operates indoor growing systems focused on leafy greens and specialty crops. It integrates automated irrigation and climate control features to improve efficiency. Headquarters: Europe. Production Model: Indoor Vertical Farming. Water Saving Efficiency: Up to 90% compared to traditional farming. Target Market: Urban Commercial Growers. Core Technology: Mist-Based Nutrient Delivery Systems. Business Focus: Sustainable Fresh Produce Supply.

Aeroponic Systems Ltd. is a UK-based company providing modular aeroponic cultivation equipment for research and commercial farms. Established in 2008, the company designs high-pressure and low-pressure aeroponic systems for controlled agriculture. It offers nutrient delivery units, root chambers, and automated misting systems. Operations primarily serve Europe and the Middle East. Core Application: Greenhouse and Indoor Farming. System Type: Commercial Aeroponic Units. Focus Crops: Vegetables and Herbs. Business Model: Equipment Manufacturing and System Supply.

Top Key Players Outlook

- AeroFarms

- Aeroponic Systems Ltd.

- Aponic Ltd.

- Freight Farms

- Growcer

- Indoor Harvest Corp.

- Living Greens Farm

Recent Industry Developments

In 2025, AeroFarms expanded retail availability, holding over 70% share of the U.S. microgreens market, and continued commercial cultivation efforts at its Danville, Virginia farm using robotics, AI, and renewable energy to boost efficiency and sustainability.

In 2025, Growcer made a significant strategic move by acquiring the assets of U.S. container farm provider Freight Farms in a $2.6 million transaction, expanding its reach into 29 additional countries and increasing its customer base by over 500% after Freight Farms’ closure.

Report Scope

Report Features Description Market Value (2024) USD 2.1 Bn Forecast Revenue (2034) USD 14.6 Bn CAGR (2025-2034) 21.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Solutions (Organic, Conventional), By Crop Type (Leafy Greens, Herbs And Microgreens, Fruits And Flowers), By Equipment (Lighting, Sensor, Irrigation Component, Climate Control, Others), By Application (Indoor, Outdoor), By End Use (Commercial, Residential) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape AeroFarms, Aeroponic Systems Ltd., Aponic Ltd., Freight Farms, Growcer, Indoor Harvest Corp., Living Greens Farm Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- AeroFarms

- Aeroponic Systems Ltd.

- Aponic Ltd.

- Freight Farms

- Growcer

- Indoor Harvest Corp.

- Living Greens Farm

Our Clients

- 178549

- Feb 2026