Global Active Phased Array Radar Market Size, Share, Growth Analysis By Function (Air Traffic Control, Early Warning, Anti-Ship Warfare, Ballistic Missile Defense), By Platform (Land-Based, Naval, Airborne, Spaceborne), By Antenna Type (Phased Array, Planar, Conformal), By Power Output (Medium Power, Low Power, High Power), By Frequency Band (X-Band, S-Band, C-Band, Ka-Band, W-Band), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 184053

- Number of Pages: 364

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

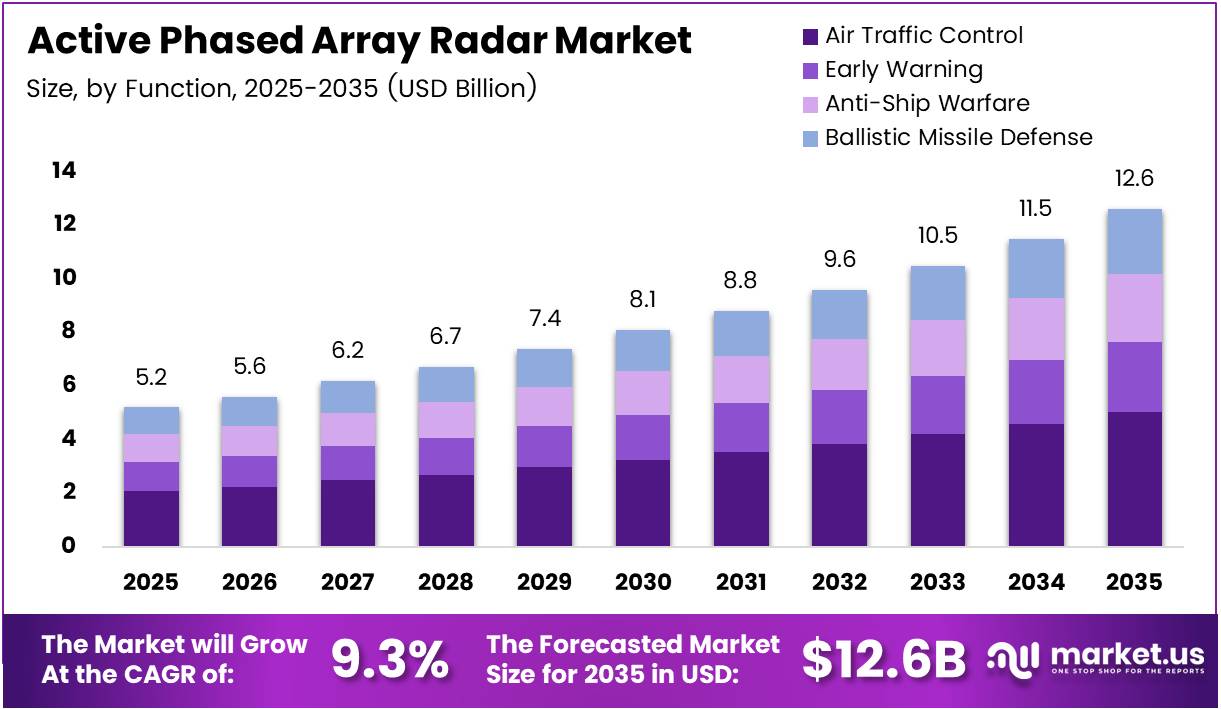

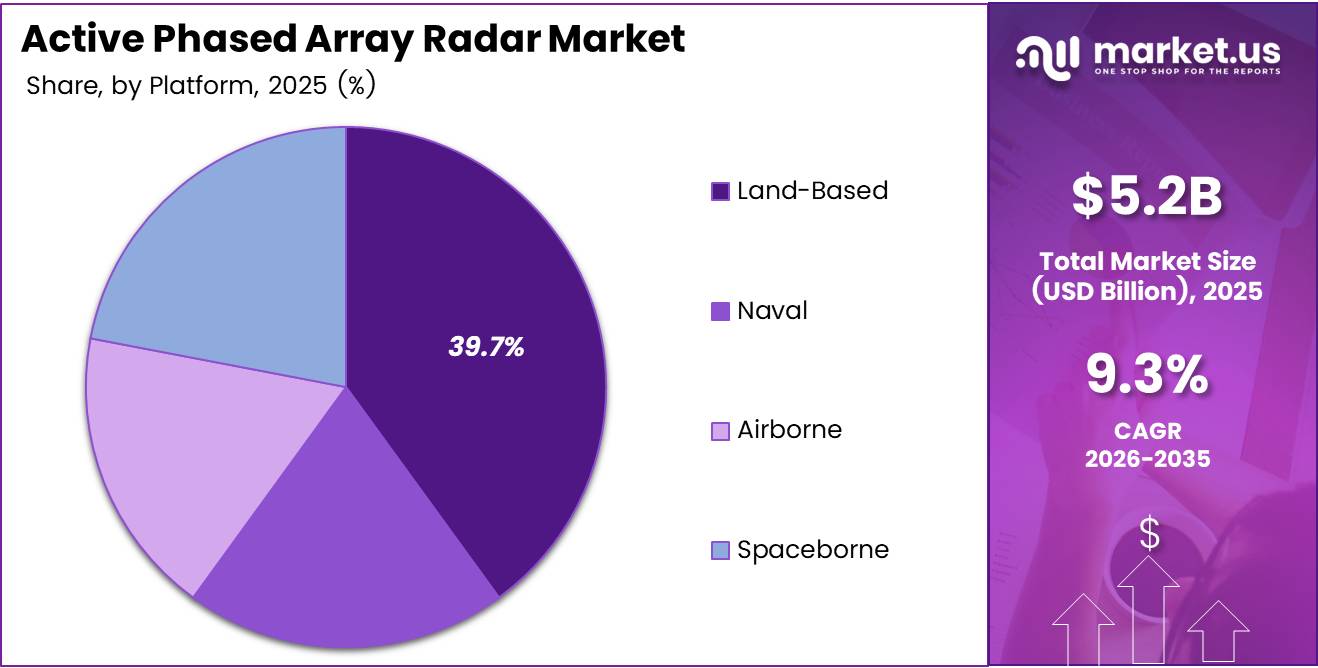

Global Active Phased Array Radar Market size is expected to be worth around USD 12.6 Billion by 2035 from USD 5.2 Billion in 2025, growing at a CAGR of 9.3% during the forecast period 2026 to 2035.

Active phased array radar systems electronically steer beam direction without mechanical rotation, enabling simultaneous multi-target tracking, rapid scan switching, and multi-mission operation across surveillance, fire control, and communications. This architecture fundamentally changes how military and defense operators manage threats across land, naval, airborne, and space platforms.

Unlike mechanically scanned arrays, active electronically scanned array (AESA) systems distribute transmit and receive functions across hundreds to thousands of individual modules. This design eliminates single-point failure risk and reduces maintenance requirements substantially — two factors that drive defense procurement decisions at the platform level.

Military modernization programs across NATO member states, Asia-Pacific nations, and the Middle East are placing long-term procurement orders for AESA-equipped platforms. These commitments represent multi-year revenue pipelines for radar prime contractors and tier-two component suppliers, particularly those producing GaN-based transmit/receive modules.

Missile defense, air defense, and border surveillance applications collectively represent the deepest demand pool in this market. Governments are not just upgrading legacy radar infrastructure — they are reconfiguring entire sensor networks around AESA-capable systems that can simultaneously track, communicate, and execute electronic warfare tasks.

In April 2024, General Atomics Aeronautical Systems announced an internally funded AESA antenna upgrade for the EagleEye radar on the Gray Eagle 25M UAV, projecting detection range improvements of more than double the current capability. This investment signals that unmanned platforms are becoming a primary growth vector for compact AESA deployments. Additionally, in April 2025, Raytheon’s LTAMDS GaN-based 360° AESA radar achieved U.S. Army Milestone C, entering low-rate initial production with capacity targeting 12 radars per year — confirming that production scalability is now a strategic priority for defense buyers.

According to drone-system.com, industrial-grade AESA systems achieve a data update rate under 0.1 seconds for single target tracking, range resolution down to 0.3 meters, and a scan angle of ±60 degrees in both azimuth and elevation with 256 to 1,024 scalable T/R module elements. These performance benchmarks explain why defense planners are accelerating replacement of legacy mechanically scanned systems — the operational advantage at the sensor level directly translates to faster engagement timelines and reduced crew workload.

According to drone-system.com, a phased array radar deployment at a maritime port recorded a 60% reduction in undetected unauthorized entries within the first six months, with maintenance costs declining sharply due to the solid-state, no-moving-parts AESA design. This real-world operational data is compelling for procurement officials in both military and homeland security roles, reinforcing investment cases beyond traditional battlefield applications.

Key Takeaways

- The Global Active Phased Array Radar Market was valued at USD 5.2 Billion in 2025 and is forecast to reach USD 12.6 Billion by 2035, at a CAGR of 9.3%.

- By Function, Air Traffic Control leads with a 33.9% share, reflecting strong civil and military airspace management demand.

- By Platform, Land-Based systems dominate with a 39.7% share, driven by extensive ground-based air defense deployments.

- By Antenna Type, Phased Array holds a 59.1% share, indicating widespread preference for electronically steered architectures.

- By Power Output, Medium Power systems account for 49.6% of the market, balancing detection range with platform integration constraints.

- By Frequency Band, X-Band leads at 37.3%, favored for high-resolution tracking in both air defense and naval applications.

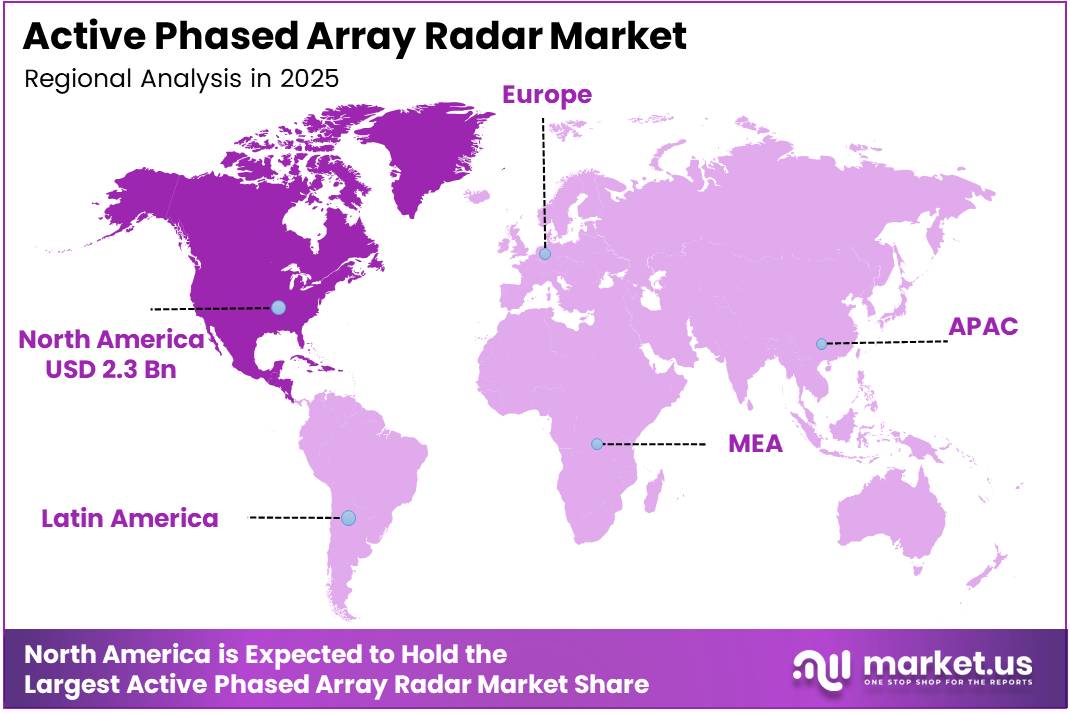

- North America holds the largest regional share at 45.8%, valued at USD 2.3 Billion, underpinned by sustained U.S. defense procurement and NATO obligations.

Function Analysis

Air Traffic Control dominates with 33.9% due to dual military-civil airspace mandate.

In 2025, Air Traffic Control held a dominant market position in the By Function segment of the Active Phased Array Radar Market, with a 33.9% share. ATC applications require simultaneous multi-aircraft tracking, rapid scan updates, and high positional accuracy — performance attributes that mechanical radar architectures cannot match at scale. AESA systems deliver these capabilities while reducing maintenance downtime, a critical factor at high-traffic civil and military aerodromes.

Early Warning radar functions serve as the strategic first layer of national and theater-level air defense architecture. These systems demand the longest detection ranges and the highest target throughput rates, requiring high-power AESA configurations capable of tracking ballistic, cruise, and hypersonic threats simultaneously. Defense planners prioritize early warning upgrades as the foundational investment before downstream fire control and intercept systems can operate effectively.

Anti-Ship Warfare radar applications operate across naval surface combatants and maritime patrol aircraft, where detection speed and frequency agility directly determine platform survivability. AESA architectures allow rapid frequency hopping that counters electronic jamming, a capability that mechanically scanned naval radars cannot replicate. Rising naval fleet modernization programs in Asia-Pacific and the Middle East are expanding procurement volumes for this function category.

Ballistic Missile Defense represents the highest unit-value application in this market. Systems such as the AN/TPY-2 are purpose-built for tracking fast-moving ballistic trajectories at extreme range, requiring the most advanced GaN-based T/R module configurations available. In May 2025, Raytheon delivered the first AN/TPY-2 radar with a complete GaN-populated array to the U.S. Missile Defense Agency, with Raytheon VP Jon Norman confirming the GaN upgrade doubles effective detection range while improving energy efficiency — a performance leap that reinforces why ballistic missile defense commands the highest per-unit procurement budgets.

Platform Analysis

Land-Based dominates with 39.7% due to extensive ground air defense network deployments.

In 2025, Land-Based systems held a dominant market position in the By Platform segment of the Active Phased Array Radar Market, with a 39.7% share. Ground-based AESA radar installations form the backbone of national air defense networks, covering fixed air defense sites, mobile battlefield radars, and border surveillance posts. The volume of land platform installations across NATO members, India, and the Asia-Pacific region generates the highest unit counts in this market segment.

Naval platforms represent the fastest-evolving deployment environment for AESA radar technology. The AN/SPY-6(V)1 naval AESA radar uses scalable 2×2×2-foot Radar Modular Assembly building blocks with GaN semiconductor technology for power efficiency, digital beamforming for rapid search and tracking, and seamless integration with the Aegis Combat System — with the U.S. Navy planning deployment across more than 60 ships over the next decade, naval procurement represents a structurally large and sustained revenue stream for prime suppliers.

Airborne platforms integrate compact AESA radars into fighter aircraft, maritime patrol planes, and unmanned aerial vehicles. Weight, size, and power constraints drive significant component miniaturization requirements, which in turn push GaN adoption and advanced packaging technologies. Modern fighter programs now treat AESA radar capability as a baseline requirement rather than an upgrade option, ensuring sustained airborne segment demand tied to aircraft production schedules.

Spaceborne AESA radar represents an early-stage but structurally important growth segment. Satellite-based radar surveillance enables persistent, wide-area coverage that ground and airborne assets cannot replicate. As sovereign space programs expand and commercial satellite operators explore radar payloads, spaceborne AESA procurement will shift from government-only to dual-use, broadening the addressable buyer base over the forecast period.

Antenna Type Analysis

Phased Array dominates with 59.1% due to superior electronic beam steering capability.

In 2025, Phased Array antenna configurations held a dominant market position in the By Antenna Type segment of the Active Phased Array Radar Market, with a 59.1% share. Electronic beam steering without mechanical movement delivers faster target handoff, higher reliability, and lower lifecycle maintenance cost — attributes that make phased array the default choice for virtually all modern defense radar procurements across platform types.

Planar antenna designs offer a cost-efficient flat-panel construction suited to applications where installation space is constrained and aperture flexibility is less critical than production cost. Planar configurations are common in ground-based surveillance posts and fixed installation ATC radars, where procurement volume requirements favor standardized, lower-cost antenna architectures over the premium performance of fully active conformal systems.

Conformal antennas conform to the surface geometry of the host platform — aircraft fuselages, ship hulls, or vehicle bodies — enabling radar coverage without external protrusions that increase radar cross-section. This design advantage makes conformal antenna systems particularly valuable for stealth aircraft and next-generation naval platforms where aerodynamic and signature management requirements constrain sensor placement options.

Power Output Analysis

Medium Power dominates with 49.6% due to optimal range-to-platform-size balance.

In 2025, Medium Power systems held a dominant market position in the By Power Output segment of the Active Phased Array Radar Market, with a 49.6% share. Medium power configurations deliver the detection ranges required for most air defense, naval surveillance, and ATC applications without the platform size, cooling, and power generation demands that high-power systems impose. This balance makes medium power the default specification for the broadest range of defense procurement programs.

Low Power AESA systems serve tactical and short-range applications including battlefield surveillance, UAV-mounted sensors, and compact vehicle-mounted radars for forward deployed units. GaN semiconductor advances are progressively improving detection performance at lower power levels, which will expand the mission envelope of low-power configurations and make them viable for applications currently requiring medium-power architectures.

High Power systems occupy the specialized end of the market, serving long-range ballistic missile defense, strategic early warning, and space surveillance applications. These systems require dedicated power generation infrastructure and advanced thermal management, limiting platform compatibility. However, the per-unit contract value for high-power systems is the largest in the market, and procurement decisions involve the longest program lifecycles and highest switching costs.

Frequency Band Analysis

X-Band dominates with 37.3% due to high-resolution tracking in air and naval defense.

In 2025, X-Band held a dominant market position in the By Frequency Band segment of the Active Phased Array Radar Market, with a 37.3% share. X-Band frequencies deliver the fine range resolution and target discrimination required for precision tracking of aircraft, missiles, and surface vessels. The AN/TPY-2 ballistic missile defense radar and the AN/APG-82 fighter radar both operate in X-Band, anchoring this frequency’s dominance across both the highest-value and highest-volume procurement programs.

S-Band radar systems provide longer detection ranges at lower resolution than X-Band, making them well suited to volume surveillance of wide airspace sectors. Naval ATC, long-range air defense search radars, and weather radar applications draw heavily on S-Band configurations. NOAA’s phased array radar Advanced Technology Demonstrator operates in S-Band and delivers scan updates every 1 minute during rapidly evolving storms — a 5× improvement over the legacy 5-minute NEXRAD Doppler cycle — demonstrating the practical operational gains available from modern phased array architectures at this frequency.

C-Band frequency systems serve mid-range applications including battlefield surveillance, fire control, and certain maritime patrol roles, offering a compromise between the high resolution of X-Band and the wide-area coverage of S-Band. C-Band radars are commonly deployed on platforms where a single radar must perform both search and tracking functions sequentially or simultaneously.

Ka-Band and W-Band configurations represent emerging and niche applications at millimeter-wave frequencies, where very high resolution is achievable at shorter ranges. These frequency bands are relevant for precision terminal guidance, autonomous vehicle sensing, and advanced UAV-based radar payloads — applications where demand will grow as autonomous defense platforms proliferate across the forecast period.

Key Market Segments

By Function

- Air Traffic Control

- Early Warning

- Anti-Ship Warfare

- Ballistic Missile Defense

By Platform

- Land-Based

- Naval

- Airborne

- Spaceborne

By Antenna Type

- Phased Array

- Planar

- Conformal

By Power Output

- Medium Power

- Low Power

- High Power

By Frequency Band

- X-Band

- S-Band

- C-Band

- Ka-Band

- W-Band

Drivers

Military Modernization Programs and Missile Defense Commitments Drive Sustained AESA Procurement Across NATO and Asia-Pacific

NATO member states and Asia-Pacific defense ministries are running structured radar replacement programs that replace legacy mechanically scanned systems with AESA platforms across fighter fleets, naval surface combatants, and ground-based air defense sites. These are not discretionary upgrades — they are treaty-aligned capability requirements with multi-year budget commitments. That structural characteristic insulates procurement volumes from short-term defense budget fluctuations.

According to pib.gov.in, India’s Ministry of Defence signed a ₹2,906 crore (~USD 346 million) contract with Bharat Electronics Limited in March 2025 for the DRDO-developed Ashwini AESA radar, capable of 360° azimuth coverage, 250 km detection range, and 4D target tracking. This single contract illustrates the scale of government commitment to indigenous AESA capability — a trend that simultaneously creates procurement volume and accelerates domestic supply chain development in countries previously dependent on imported radar systems.

The integration of phased array radar into missile defense and air defense systems deepens the technology’s lock-in across national defense architectures. Once a nation fields AESA-based air defense networks, sustainment contracts, upgrade cycles, and interoperability requirements create durable revenue streams for prime contractors over program lifetimes measured in decades. This lifecycle economics profile makes AESA radar one of the most structurally secure long-term markets in the global defense sector.

Restraints

High Development Costs and Complex Integration Requirements Constrain Market Participation to Well-Capitalized Defense Primes

AESA radar development requires sustained R&D investment in GaN semiconductor fabrication, advanced packaging, digital beamforming architecture, and software-defined signal processing — capabilities that only a small number of vertically integrated defense contractors possess. This concentration narrows competitive supply, limits cost pressure on incumbents, and creates procurement dependency for buyer nations without domestic radar industrial bases.

According to milmag.pl, the U.S. Missile Defense Agency awarded two contracts totaling USD 966.7 million to Raytheon in March 2026 under the AN/TPY-2 X-band radar program alone. Contract values of this magnitude reflect not just system capability but the embedded integration and sustainment complexity that makes switching suppliers impractical mid-program. Buyers effectively commit to a single vendor ecosystem for decades once a radar architecture is fielded, which constrains competitive dynamics and limits cost benchmarking across procurement cycles.

Complex integration requirements also slow deployment timelines for new market entrants and smaller nations seeking to field modern air defense networks. The technical interfaces between AESA radar hardware, combat management systems, communications networks, and battle management software require extensive systems engineering — costs that multiply when integrating across multi-vendor, multi-national defense platforms. This integration burden functions as a structural barrier that limits both buyer agility and the competitive addressable market for non-incumbent suppliers.

Growth Factors

Space-Based Surveillance, UAV Integration, and Electronic Warfare Investment Open New Revenue Vectors for AESA Suppliers

Satellite-based AESA radar payloads represent a structurally new market segment that extends surveillance capability beyond the horizon constraints of ground and airborne platforms. Sovereign space programs and commercial satellite operators are evaluating persistent wide-area radar coverage for maritime domain awareness, border monitoring, and strategic reconnaissance — applications that expand the addressable buyer base well beyond traditional defense ministry procurement channels.

According to ou.edu, NOAA’s Phased Array Radar Advanced Technology Demonstrator delivers weather scan updates every 1 minute during rapidly evolving storms, compared to every 5 minutes for legacy NEXRAD Doppler systems — a 5× improvement in data refresh rate, with over 300 hours of hazardous weather data collected since 2021. This performance delta confirms that phased array architectures deliver operationally decisive refresh rate improvements, and the same logic applies to defense surveillance applications where faster data cycles directly reduce threat response timelines. In August 2025, the U.S. Navy’s AN/SPY-6(V)4 AESA radar completed its first live maritime test in Hawaii, successfully tracking air and surface targets under varied conditions — generating the first live performance dataset for this configuration ahead of planned deployment across more than 60 Navy ships.

The development of compact AESA radars for tactical ground vehicles and autonomous defense platforms addresses a rapidly expanding equipment category. As armed forces integrate unmanned ground vehicles and autonomous logistics platforms into forward operations, the requirement for onboard situational awareness drives demand for miniaturized AESA sensors. Parallel investment in next-generation electronic warfare systems — particularly counter-stealth and low-probability-of-intercept technologies — creates additional demand for wideband AESA apertures that support simultaneous radar, jamming, and communications functions within a single aperture.

Emerging Trends

GaN Technology, AI-Enabled Signal Processing, and Multi-Function Apertures Redefine AESA System Architecture

GaN-based transmit/receive modules are displacing legacy GaAs devices across AESA front-ends, delivering higher power density, improved thermal performance, and lower system-level size, weight, power, and cost — the SWaP-C metrics that determine whether a radar system fits a given platform without requiring redesign of the host vehicle’s power and cooling infrastructure. This semiconductor transition is not incremental: it enables performance gains that justify complete system replacements rather than component-level upgrades.

According to defensescoop.com, Raytheon completed flight testing of its Cognitive Algorithm Deployment System in February 2025 — an AI/ML-enabled upgrade to the ALR-69A digital radar warning receiver. CADS uses an embedded GPU and AI algorithms to analyze enemy radar signals in real time, helping air crews prioritize threats when managing 100+ simultaneous signal detections, with U.S. Air Force procurement expected in 2025 following 6 lab tests and 5 flight tests. This development confirms that AI integration in radar signal processing has crossed from research concept to operational procurement — a shift that redefines buyer expectations for all future radar warning and AESA system acquisitions.

The convergence of radar, electronic warfare, and communications into single wideband apertures represents the most architecturally significant trend in this market. Multi-function radar systems reduce platform sensor count, simplify integration, and lower lifecycle cost — making them attractive for both new platform designs and mid-life upgrade programs. Northrop Grumman’s February 2026 unveiling of the Valen AESA radar — a fully 3D-printed multifunction array combining radar, electronic warfare, and communications in a single aperture — illustrates how additive manufacturing and advanced packaging are enabling system configurations that were not manufacturable at acceptable cost three years ago.

Regional Analysis

North America Dominates the Active Phased Array Radar Market with a Market Share of 45.8%, Valued at USD 2.3 Billion

North America commands a 45.8% share valued at USD 2.3 Billion, anchored by the U.S. Department of Defense’s multi-decade investment across missile defense, naval, and airborne AESA programs. The United States operates the world’s most advanced AESA procurement infrastructure — from the F-35 APG-85 and F-15EX APG-82 fighter radars to SPY-6 naval arrays and AN/TPY-2 ballistic missile defense systems — creating a structurally dominant position that no other region can match in program scale or procurement consistency.

Europe Active Phased Array Radar Market Trends

Europe is consolidating air defense radar procurement around NATO capability requirements, with member states signing bilateral and multilateral AESA acquisition agreements. In January 2024, Lithuania signed a €126.7 million agreement to acquire Thales Ground Master 200 Multi-Mission Compact 4D AESA radars, reflecting how smaller NATO members are making structured investments to meet alliance commitments. European defense spending trajectories post-2022 indicate sustained procurement growth through the forecast period.

Asia Pacific Active Phased Array Radar Market Trends

Asia Pacific represents the fastest-growing regional market, driven by territorial disputes, naval fleet expansions, and indigenous defense industrial programs across India, China, South Korea, and Japan. India’s ₹2,906 crore DRDO Ashwini AESA radar contract with BEL demonstrates that regional demand is shifting from import-dependent to domestically produced systems, creating new supply chain participants and competition dynamics that will reshape regional market structure over the forecast period.

Middle East and Africa Active Phased Array Radar Market Trends

Middle Eastern defense ministries are investing in integrated air defense networks that combine early warning, missile defense, and naval surveillance AESA systems. Gulf Cooperation Council states with established U.S. and European defense partnerships are procuring advanced radar platforms as part of broader air defense architecture upgrades. This procurement activity creates a structurally reliable regional market where geopolitical risk drives defense budget floors rather than ceilings.

Latin America Active Phased Array Radar Market Trends

Latin America remains an emerging market for AESA radar technology, with procurement concentrated in border surveillance, maritime domain awareness, and air traffic management applications. Budget constraints limit the pace of advanced radar acquisition, but partnerships with U.S. and European defense primes on technology transfer and co-production create a longer-term pathway for regional market development beyond direct import procurement models.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Northrop Grumman holds a distinct structural advantage through vertical integration of AESA radar design, GaN semiconductor fabrication, and advanced systems packaging at its Microelectronics Center. The February 2026 unveiling of the Valen — a fully 3D-printed multifunction AESA array combining radar, electronic warfare, and communications — demonstrates that Northrop is competing on manufacturing innovation, not just engineering performance, a positioning that addresses both cost and lead-time pressures in defense procurement.

Raytheon Technologies dominates the high-end AESA radar segment through its APG-82(V)X fighter radar, AN/SPY-6 naval array, and AN/TPY-2 ballistic missile defense system — a portfolio that covers every major application category in this market. The September 2025 unveiling of the APG-82(V)X with GaN enhancement for the F-15EX, combined with the $1.7 billion LTAMDS production contract and the $966.7 million AN/TPY-2 award, confirms Raytheon’s position as the single largest revenue beneficiary across current active procurement programs.

Lockheed Martin leverages its dominant position as prime contractor on the F-35 program to sustain demand for integrated AESA radar systems across all three F-35 variants. Its radar systems engineering competence extends across airborne, naval, and ground-based platforms, and the company’s role in Aegis Combat System integration creates natural adjacency to SPY-6 naval radar deployment programs — an indirect competitive position that generates pull-through demand without requiring standalone radar program wins.

Thales Group targets the export radar market with multi-mission AESA products including the Ground Master family, positioning itself as the preferred European alternative to U.S. suppliers for NATO allies that face political or industrial offset pressures limiting American procurement. Lithuania’s January 2024 €126.7 million GM200 MM/C contract exemplifies Thales’s strategy — winning NATO-aligned tenders where European industrial content requirements create a structural competitive advantage over U.S. primes.

Key Players

- Northrop Grumman

- Raytheon Technologies

- Lockheed Martin

- Thales Group

- BAE Systems

- Leonardo S.p.A.

- Hensoldt

- Israel Aerospace Industries

- Saab AB

Recent Developments

- January 2024 — Lithuania’s Defence Material Agency signed a €126.7 million agreement with Dutch procurement agency COMMIT to acquire Thales Ground Master 200 Multi-Mission Compact 4D AESA radars, strengthening national and NATO air defence and counter-battery capabilities.

- February 2024 — General Radar Corporation launched “Radar-as-a-Service,” offering scalable AESA phased array radar data on a subscription basis to dramatically shorten deployment timelines for government and commercial customers, introducing a new commercial delivery model to the sector.

- June 2025 — RTX’s Raytheon received a $646 million U.S. Navy contract option to continue production, modernization, and sustainment of AN/SPY-6 AESA radars under a hardware production and sustainment agreement, extending a program originally signed in 2022.

- August 2025 — The U.S. Army awarded RTX a $1.7 billion contract for production and fielding of the LTAMDS next-generation air and missile defense AESA radar, covering nine radars for the U.S. and Poland plus associated engineering and support services.

- September 2025 — Raytheon received a $602.9 million firm-fixed-price U.S. Navy contract to repair and provide spare parts for F/A-18 AESA radar assemblies over a five-year period, securing a long-term sustainment revenue stream.

- October 2025 — Saab received a contract from Spain’s Ministry of Defence to deliver its Giraffe 4A multifunction AESA radar system integrated with command-and-control capabilities to strengthen Spain’s ground-based air defence architecture.

- November 2025 — Saab received an order from Sweden’s Defence Materiel Administration for additional Giraffe family AESA radars and command systems as part of building a new brigade-level air defence capability.

- February 2026 — Northrop Grumman unveiled the Valen AESA radar — a fully 3D-printed, internally funded multifunction array combining radar, electronic warfare, and communications into a single wideband aperture, flight-tested on a CRJ-700 aircraft.

- March 2026 — The U.S. Missile Defense Agency awarded two contracts totaling $966.7 million to Raytheon under the AN/TPY-2 X-band phased array ballistic missile defense radar program, with GaN-upgraded arrays replacing legacy GaAs modules to increase range, accuracy, and energy efficiency.

Report Scope

Report Features Description Market Value (2025) USD 5.2 Billion Forecast Revenue (2035) USD 12.6 Billion CAGR (2026-2035) 9.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Function (Air Traffic Control, Early Warning, Anti-Ship Warfare, Ballistic Missile Defense), By Platform (Land-Based, Naval, Airborne, Spaceborne), By Antenna Type (Phased Array, Planar, Conformal), By Power Output (Medium Power, Low Power, High Power), By Frequency Band (X-Band, S-Band, C-Band, Ka-Band, W-Band) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Northrop Grumman, Raytheon Technologies, Lockheed Martin, Thales Group, BAE Systems, Leonardo S.p.A., Hensoldt, Israel Aerospace Industries, Saab AB Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Active Phased Array Radar MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Active Phased Array Radar MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Northrop Grumman

- Raytheon Technologies

- Lockheed Martin

- Thales Group

- BAE Systems

- Leonardo S.p.A.

- Hensoldt

- Israel Aerospace Industries

- Saab AB

Our Clients

- 184053

- Apr 2026