Quick Navigation

Report Overview

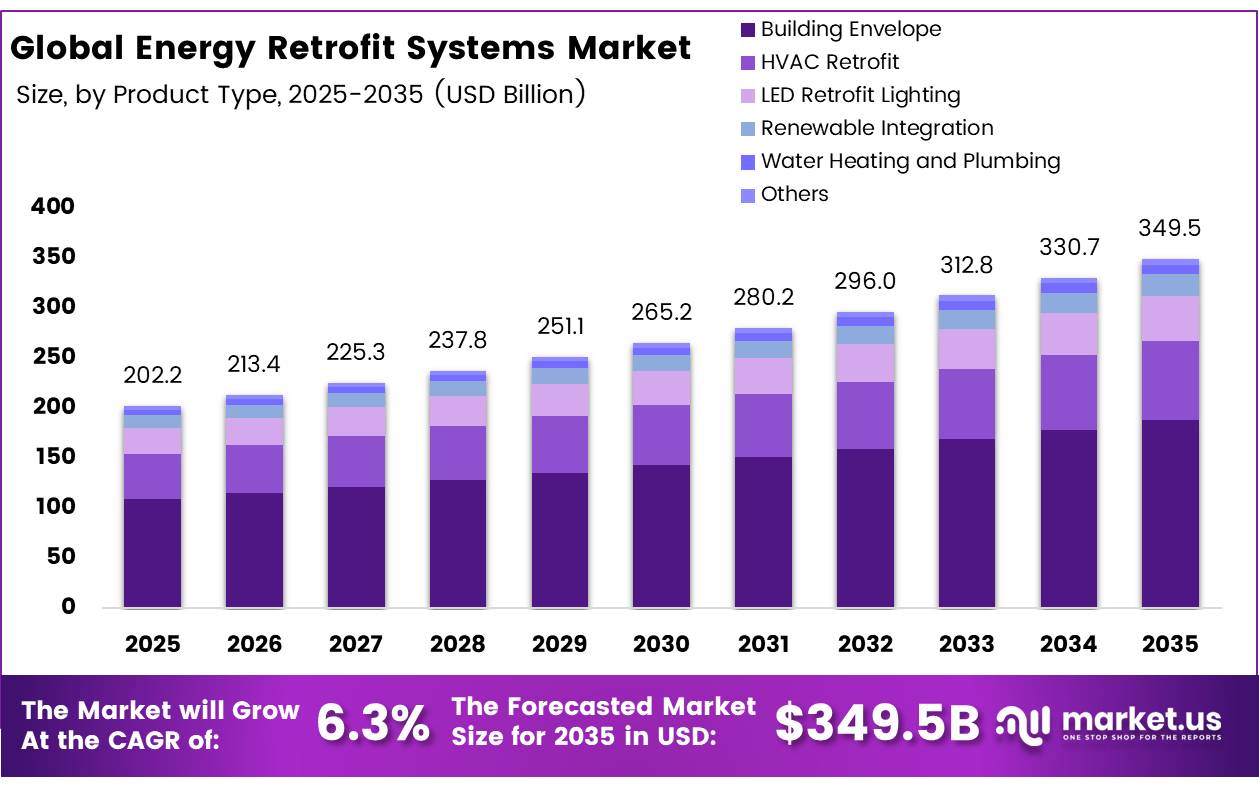

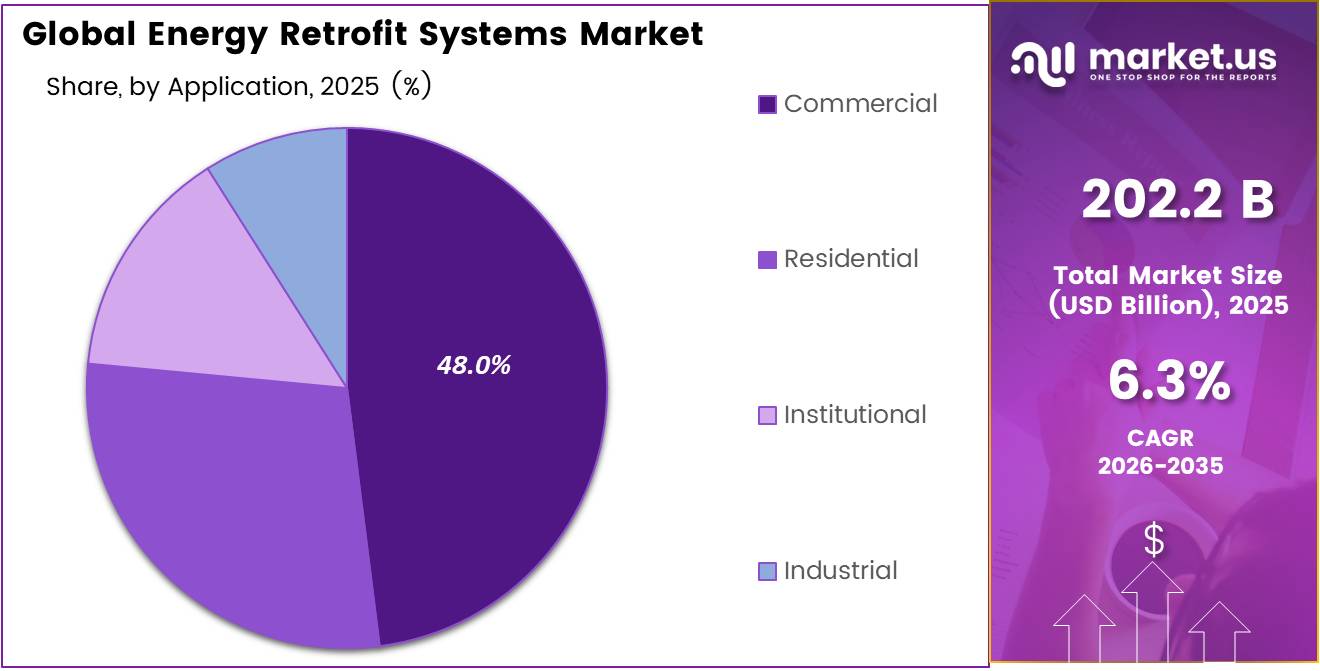

In 2025, the Global Energy Retrofit Systems Market was valued at US$202.2 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 6.3%, reaching about US$349.5 billion by 2035. North America held a dominant Market position, capturing more than a 40.2% share, holding USD 81.2 billion in revenue.

Key Takeaways

- The global Energy Retrofit Systems market was valued at US$202.2 billion in 2025.

- The market is projected to grow at a CAGR of 6.3% and is estimated to reach US$349.5 billion by 2035.

- Based on the product type, the building envelope segment dominated the global energy retrofit systems market, accounting for 54.1% of the total market share.

- Based on application, the commercial segment held the largest share in the energy retrofit systems market, contributing 48.5% of the overall market revenue.

- Among retrofit depth categories, shallow/light energy retrofits dominated the market, representing approximately 61.5% of the total market share.

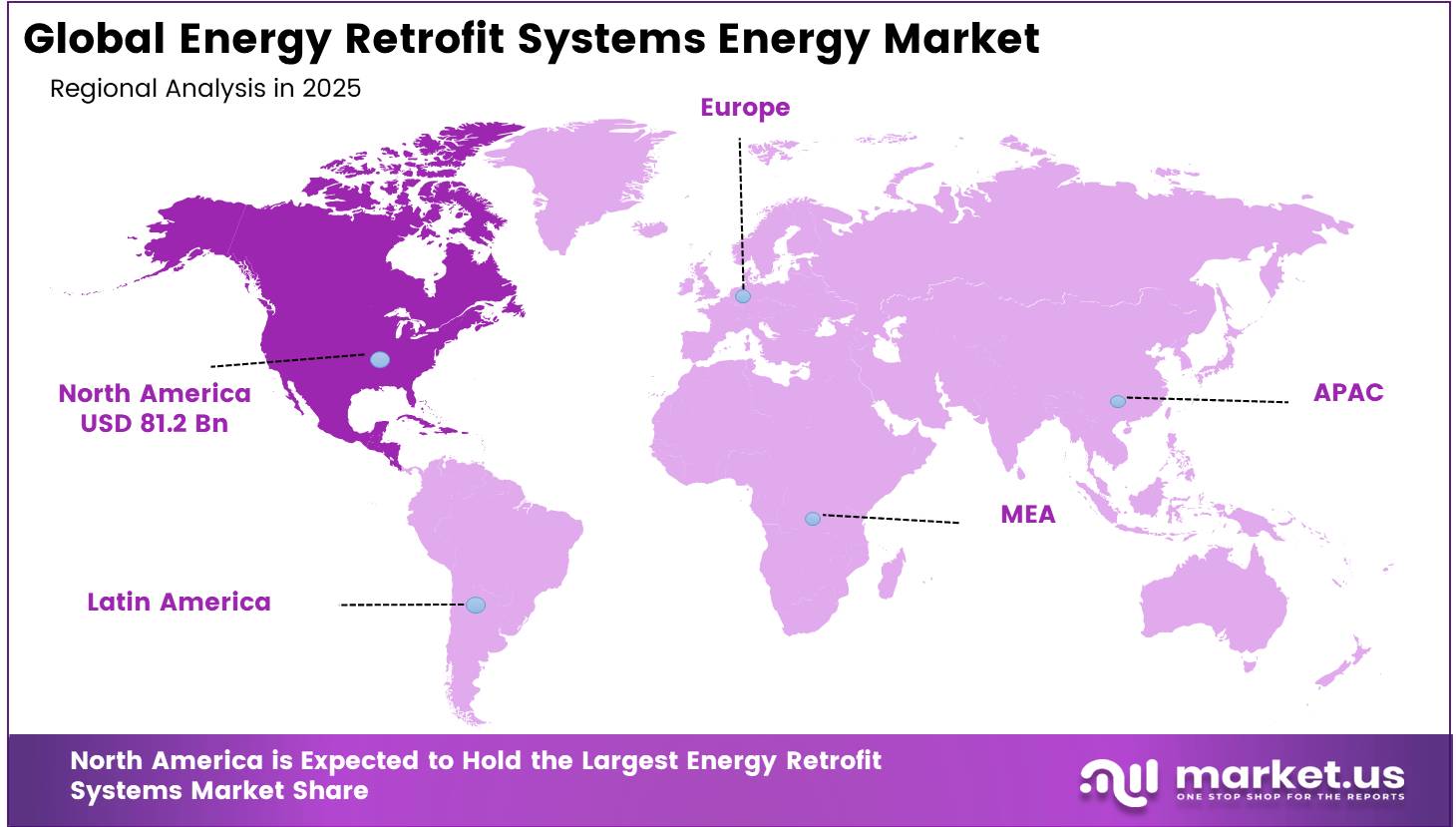

- In 2025, North America emerged as the leading regional market for energy retrofit systems, accounting for 40.2% of the global market share.

The Energy Retrofit Market is predominantly led by the Building Envelope segment in terms of having the largest market share. The reason behind this structural characteristic is the inherent fact that insulations and other improvements to the exterior of the building reduce energy usage before the mechanical systems and lights can be considered. HVAC Retrofit follows closely, followed by LED Retrofit Lighting and Renewable Integration, with Water Heating & Plumbing completing the top five segments.

- According to the International Energy Agency’s Energy Efficiency 2025 assessment, worldwide final energy consumption exceeded 450 exajoules in 2024, increasing by around 25 exajoules since 2019. Buildings accounted for approximately 30% of global energy demand and contributed nearly 20% of the increase in total demand recorded since 2019.

In the case of end-user market structure, Commercial dominates due to the sheer size of the commercial buildings, relatively quick payback periods, and increasing regulations for corporations to reach certain energy performance targets. Residential and Institutional sectors follow as meaningful contributors, while Industrial users represent a smaller but structurally distinct segment where process-heat considerations often take precedence over envelope

- The UK Department for Energy Security and Net Zero stated in its March 2026 statistical release that Great Britain had installed approximately 9 million energy-efficiency measures across 2.9 million households between 2013 and the end of 2025, highlighting sustained growth in residential energy-efficiency retrofit programs.

The shallow or light retrofits take up most of the retrofit depths, suggesting that the focus of market dynamics continues to be on phased, gradual improvements on existing systems rather than a holistic transformation of the building. Regionally, North America dominates the rest, owing to its advanced regulatory regime, existing infrastructure of contractors, and supportive energy efficiency policies.

- Australian Government data updated in February 2026 showed that buildings accounted for around 19% of national energy use and 18% of direct carbon emissions. Residential buildings alone consumed approximately 24% of Australia’s electricity and generated more than 10% of total carbon emissions.

Energy Retrofit Systems Market Segmentation

Product Type Analysis

Building envelope is a significant product type

Building envelope retrofit systems control the worldwide energy retrofit systems market, accounting for 54.1% of total market share. This segment’s domination stems mostly from a growing emphasis on increasing building energy efficiency, lowering heating and cooling losses, and improving indoor environmental performance. Building envelope retrofits, which include insulation upgrades, energy-efficient windows, roofing systems, and air sealing solutions, are crucial in reducing energy consumption in both residential and commercial structures.

- In 2024, The U.S. Department of Energy estimates that buildings account for approximately 40% of total energy consumption nationally, with commercial and residential structures representing the largest opportunity for efficiency gains through targeted retrofit programs.

Demand for HVAC retrofit systems remains robust, driven by the accelerating replacement of aging heating and cooling infrastructure with energy-efficient technologies that deliver measurable reductions in energy consumption while improving indoor air quality. LED retrofit lighting continues to gain traction across commercial and institutional buildings, underpinned by its low power draw, extended operational lifespan, and significantly reduced maintenance burden compared to conventional lighting systems.

Application Analysis

Commercial Segment dominates the market

The commercial segment leads demand, accounting for 48% of total market activity, driven by regulatory pressure, corporate sustainability mandates, and the need to optimize operational costs across office complexes, retail facilities, and healthcare infrastructure. Asset owners are increasingly prioritizing retrofit investments to meet green building certification requirements and align with evolving energy performance standards.

Institutional and industrial applications round out the market, with public-sector energy reduction targets driving steady retrofit investment across educational facilities, government buildings, and healthcare campuses. The industrial segment, though comparatively smaller, presents growing opportunities in energy management systems and process-level efficiency improvements where energy expenditure represents a material operational cost.

Retrofit Depth Analysis

Shallow/Light Energy Retrofits leads the market

Shallow/light energy retrofits account for the dominant share of market activity by 61.5%, reflecting a broad preference among property owners for phased, lower-capital interventions that deliver near-term returns without requiring comprehensive building overhauls. These retrofits typically encompass targeted upgrades such as LED lighting conversions, HVAC system optimizations, and basic insulation improvements measures that offer relatively straightforward implementation, shorter payback periods, and minimal disruption to building occupants and operations.

- A U.S. Department of Energy and Lawrence Berkeley National Laboratory assessment of commercial-building retrofit projects found that integrated system retrofits represented less than 20% of all projects. This indicates that more than 80% of the projects in the reviewed dataset primarily relied on individual equipment or component upgrades, such as lighting, chillers and controls.

Deep energy retrofits, while representing a smaller portion of current market activity, are gaining strategic relevance as regulatory frameworks tighten and the limitations of incremental upgrades become more apparent. These comprehensive interventions encompassing full envelope replacement, mechanical system overhauls, and integrated renewable energy installations are increasingly being pursued by institutional and commercial property owners with long-term asset value and compliance obligations in mind.

Key Market Segments

By Product

- Building Envelope

- HVAC Retrofit

- LED Retrofit Lighting

- Renewable Integration

- Water Heating and Plumbing

- Others

By Application

- Commercial

- Residential

- Institutional

- Industrial

By Retrofit Depth

- Deep Energy Retrofits

- Shallow/Light Energy Retrofits

Driver Analysis

EPBD compliance-led deep renovation demand

The strongest 2026 demand catalyst is the EU’s revised Energy Performance of Buildings Directive, which entered into force on 28 May 2024 and requires Member States to transpose it by 29 May 2026, while also requiring average primary-energy reduction in residential buildings of 16% by 2030 and 20–22% by 2035. That timing matters commercially because retrofit system vendors are selling into a regulation-forced conversion window rather than a purely discretionary capex cycle; once national transposition is finalized, owners, ESCOs, and general contractors must shift from isolated component upgrades toward bundled envelope-HVAC-controls packages that can document compliance and measurable energy reduction.

The market effect is especially powerful in the EU core because National Building Renovation Plans had draft deadlines by 31 December 2025 and final plans by 31 December 2026, forcing countries to map stock condition, investment needs, and financing sources, which effectively converts policy ambition into near-bookable project pipelines for audits, controls retrofits, insulation systems, heat-pump integration, and building automation layers. This is why the driver adds an estimated +2.4 percentage points to baseline CAGR: the regulation shortens sales cycles for compliant solution bundles, expands demand beyond premium green buildings into mid-tier stock, and increases replacement intensity in aging residential and non-residential assets where deferred modernization is no longer viable.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPBD compliance-led deep renovation demand | +2.4% | EU core, UK spill-over, EEA-adjacent service markets | Short term (≤ 2 years) |

| Public funding and incentive-backed retrofit execution | +1.9% | North America core, EU, selected APAC public-building programs | Short term (≤ 2 years) |

| Energy-cost savings and payback compression | +1.6% | North America, EU, urban APAC corridors | Medium term (2-4 years) |

| Electrification of HVAC and controls modernization | +1.8% | U.S., EU, Japan, South Korea, Tier-1 China metros | Medium term (2-4 years) |

| Digital audits, EPCs, and measured-performance procurement | +1.2% | EU core, U.S. institutional markets, advanced APAC cities | Short term (≤ 2 years) |

| Long-horizon decarbonisation targets and renovation planning pipelines | +1.5% | EU core, federal North America, OECD retrofit ecosystems | Long term (≥ 4 years) |

Restraint Analysis

Retrofit cost inflation

Retrofit system adoption remains constrained by elevated input and installed-equipment costs, because the most common retrofit bundles HVAC replacement, controls, insulation upgrades, and electrification-enabling balance-of-system work are still being priced against a construction environment that has not fully normalized in 2026; in the U.S., producer prices for final demand were up 6.5% year over year in May 2026, while HVAC and commercial refrigeration equipment PPI moved from roughly 231.0 in June 2025 to 236.6 by April 2026, indicating continued equipment cost pass-through rather than deflation, and Sweden’s official construction cost index still showed annual growth of 2.3% in May 2026, reinforcing that labor, materials, and transport are keeping project budgets above pre-2022 planning assumptions.

For retrofit owners, that translates into CapEx overruns commonly in the high-single-digit range on rebid cycles, forced scope thinning on envelope and controls layers first, and margin compression for ESCOs and mechanical integrators that are unable to reprice fixed bids fast enough; strategically, this delays board approvals, reduces attachment rates for deeper retrofits versus partial replacements, and lowers conversion on mid-market projects where a 10% to 15% installed-cost increase can push simple payback beyond internal hurdle thresholds.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retrofit cost inflation | -1.4% | North America core, EU, APAC metros | Short term (≤ 2 years) |

| Skilled labor scarcity | -1.1% | North America core, EU, GCC, ANZ | Short term (≤ 2 years) |

| Code and permit friction | -0.9% | U.S. states, EU, India urban corridors | Medium term (2-4 years) |

| Refrigerant transition disruption | -0.8% | U.S., EU, Japan, Korea | Short term (≤ 2 years) |

| Financing and payback pressure | -1.2% | EU, North America, developed APAC | Medium term (2-4 years) |

| M&V and contract complexity | -0.7% | Public sector and large commercial globally | Long term (≥ 4 years) |

Opportunity Analysis

BPS compliance platforms

This is an opportunity rather than a baseline driver because the current market already benefits from generic efficiency spending, while the untapped upside lies in turning tightening building performance standards into a recurring compliance-and-upgrade revenue stack that combines audit software, controls retrofits, electrification design, and financed execution; the white space is especially strong because DOE notes that BPS programs are being supported with dedicated financing pathways rather than just one-time capex, while the EU Renovation Wave aims to renovate 35 million buildings by 2030 and at least double annual renovation rates, creating a large addressable pipeline of owners who will need data, sequencing, and compliance services rather than only hardware sales.

Commercial retrofit vendors that package monitoring plus guaranteed-performance upgrades can lift revenue intensity per building by an estimated 20% to 35%, raise software-attached gross margin by 500 to 900 basis points, and reduce customer-acquisition cost by roughly 15% to 25% through regulation-led selling; assuming only 8% to 12% of the addressable noncompliant stock in BPS-active cities converts to multi-year compliance contracts by 2030, that alone can plausibly add about +2.4 percentage points above baseline market CAGR because it monetizes a layer of compliance workflow and measurement that standard retrofit projects often leave uncaptured.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| BPS compliance platforms | +2.4% | North America core, EU | Short term (≤ 2 years) |

| Affordable multifamily electrification | +2.1% | U.S., Canada, EU | Short term (≤ 2 years) |

| Public-building ESCO roll-ups | +1.8% | U.S., EU, APAC public sector | Medium term (2-4 years) |

| Retrofit-as-a-service financing | +1.6% | North America, EU, APAC cities | Medium term (2-4 years) |

| Resilience retrofit bundles | +1.9% | U.S., Japan, Australia, EU | Medium term (2-4 years) |

| Data-center adjacent retrofits | +1.5% | U.S., Nordics, Western Europe, Singapore | Long term (≥ 4 years) |

Challenges Analysis

Retrofit-skilled labor gap

Persistent shortages of retrofit-relevant skills HVAC technicians, building energy auditors, insulation installers, controls engineers, and commissioning agents are creating structural execution risk that slows annual project throughput, even in markets with strong policy support. Government and intergovernmental assessments of the energy efficiency workforce indicate that more than 80% of energy efficiency employers in advanced economies report hiring difficulties, with some U.S. surveys showing around 83% of firms struggling to fill technical roles and similar pressures in EU construction trades tasked with delivering higher performance building envelopes.

At the same time, the EU’s Renovation Wave targets renovation of roughly 35 million buildings by 2030, while sector pacts estimate that upskilling on the order of 3 million construction workers (about 25% of the construction labor force) is required between 2022 and 2027 to deliver on these targets, creating a gap between policy ambition and workforce capacity.

This imbalance translates into project lead times that can extend from 6–9 months to 12–18 months for complex commercial retrofits, and capacity utilization in high-skill trades often above 90%, forcing developers to phase work or reduce annual completion volumes by 10–20% relative to demand. From a financial perspective, labor bottlenecks raise installed system costs by an estimated 5–10% through wage premiums, overtime, and scheduling inefficiencies, while also raising the variance of project completion time (standard deviation of completion timelines increasing from, for example, 20–25 days to 40–60 days on large multi‑measure retrofits).

Over a five- to seven-year forecast window where decarbonization pathways suggest aggressive retrofit rates, this skills gap subtracts roughly 1.4 percentage points from the market’s potential CAGR by capping the number of buildings that can be practically upgraded each year, and it forces firms to invest disproportionately in in-house training pipelines, multi‑year apprenticeship programs (often 2–4 years per technician), and cross‑border labor sourcing strategies just to hold current growth trajectories. Strategic navigation requires OEMs and ESCOs to co‑design curricula with vocational institutes, secure multi‑year workforce development grants where available (for example, DOE building efficiency workforce initiatives or EU skills pacts), and shift toward standardized retrofit “kits” that reduce per‑project labor intensity by 15–25% and compress on‑site workdays, partially offsetting the structural drag until workforce depth normalizes beyond 2030.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Retrofit-skilled labor gap | -1.4% | North America, EU, UK, developed APAC | Long term (≥ 4 years) |

| Fragmented building data & audits | -1.1% | North America, EU regulatory hubs, OECD Asia | Medium term (2-4 years) |

| Supply chain & component volatility | -0.9% | EU, UK, North America, import-reliant APAC | Medium term (2-4 years) |

| Policy execution and permitting drag | -1.0% | EU Renovation Wave, India, Southeast Asia, LATAM metros | Long term (≥ 4 years) |

| Capital cycling & performance risk | -0.8% | North America core, EU green finance hubs, urban Asia | Medium term (2-4 years) |

| Digital interoperability & legacy assets | -0.7% | Global tier-1 cities, industrial retrofit clusters | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Energy security concerns and geopolitical shifts are accelerating global building retrofit investments.

The rising geopolitical risks and the growing urgency for energy independence have become significant indirect drivers for energy retrofit projects. Indeed, the Russia-Ukraine War highlighted how dependent economies were on fossil fuels and made governments prioritize the implementation of programs aimed at improving building efficiency as a strategy to decrease energy imports. As a result, energy retrofit is becoming increasingly important in the context of global geopolitics, and incentive programs have been implemented to encourage the modernization of buildings faster than initially planned.

Another factor that market stakeholders must account for is trade policy trends, especially the emergence of tariffs on imported construction products such as insulation materials. However, as domestic production receives a boost through key pieces of legislation such as the Inflation Reduction Act, new challenges will arise in terms of logistics and the availability of some components for retrofit projects. Nevertheless, the combination of geopolitical drivers and trade policies makes the topic of energy retrofit particularly relevant, especially as supply chains continue to be reorganized due to recent events.

Regional Analysis

North America Held the Largest Share of the Global Energy Retrofit Systems Market.

In 2025, North America dominates the worldwide energy retrofit systems market, accounting for a 40.2% market share, holding 81.2 billion in revenue, owing to a mature regulatory environment and ongoing policy-driven investment in energy efficiency. Canada’s innovative provincial energy standards and retrofit incentive programs strengthen regional demand, cementing North America’s position as the global norm for retrofit activity.

Europe follows closely, driven by binding EU energy performance mandates and dedicated green financing mechanisms targeting its extensive stock of aging, energy-inefficient buildings. Asia Pacific is emerging as the fastest-growing region, with China, Japan, and South Korea advancing aggressive green building policies aligned with their respective net-zero commitments.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Growing emphasis on building decarbonization and energy performance optimization is encouraging energy retrofit system providers to enhance their competitive strategies through innovation, integrated solutions, and strategic collaborations. Companies are investing heavily in advanced insulation technologies, high-efficiency HVAC equipment, and intelligent building management systems to improve retrofit effectiveness. At the same time, leading market participants are increasingly delivering comprehensive retrofit packages that combine building envelope improvements, equipment upgrades, and renewable energy systems, helping customers reduce energy consumption, lower operating costs, and meet sustainability objectives more efficiently.

Strategic alignment with green financing institutions and energy performance contracting frameworks allows providers to overcome the upfront capital barrier that has previously hampered adoption, while vertical integration with material suppliers and construction service networks promotes supply chain stability and cost control. Investment in IoT-enabled monitoring platforms and AI-driven energy analytics is further differentiating market offerings, allowing providers to deliver verifiable performance outcomes and strengthen long-term positioning within high-value commercial and institutional application segments.

The Major Players in The Industry

- Johnson Controls International

- Schneider Electric SE

- Siemens AG

- Trane Technologies PLC

- Daikin Industries Ltd.

- ENGIE S.A.

- Honeywell International Inc.

- Eaton Corporation PLC

- Ameresco Inc.

- AECOM

- Signify N.V. (Philips Lighting)

- Carrier Global Corporation

- Orion Energy Systems Inc.

- Emerson Electric Co.

- General Electric (GE Vernova)

Key Development

- In April 2026, Schneider Electric SE reported first-quarter revenue of €9.77 billion, representing 2% organic growth, while its Energy Management business increased by 12.8%, showing strong demand for electrical modernization and digital energy systems.

- In February 2026, Johnson Controls International company agreed to acquire Alloy Enterprises, whose liquid-cooling components can improve thermal-management efficiency by up to 35% and reduce pressure loss by up to 75%, supporting lower energy use in data centres and other high-load buildings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$202.2 Bn |

| Forecast Revenue (2035) | US$349.5 Bn |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Building Envelope, HVAC Retrofit, LED Retrofit Lighting, Renewable Integration, Water Heating and Plumbing, and Others), By Application (Commercial, Residential, Institutional, and Industrial), By Retrofit Depth (Deep Energy Retrofits and Shallow/Light Energy Retrofits) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Johnson Controls International, Schneider Electric SE, Siemens AG, Trane Technologies PLC, Daikin Industries Ltd., ENGIE S.A., Honeywell International Inc., Eaton Corporation PLC, Ameresco Inc., AECOM, Signify N.V. (Philips Lighting), Carrier Global Corporation, Orion Energy Systems Inc., Emerson Electric Co., General Electric (GE Vernova). |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions (FAQ)

The global market size was USD 148.23 billion in 2021 and is projected to surpass USD 233.96 billion by 2032.

Registering a CAGR of 4.2%, the market will exhibit a decent growth rate during the forecast period (2023-2032).

The global energy retrofit systems market size was estimated at USD 148.8 billion in 2021 and is expected to reach USD 233.96 billion in 2032.

The global energy retrofit systems market is expected to grow at a compounded annual growth rate of 4.2% from 2023 to 2032 to reach USD 233.96 billion by 2032.

The major players operating in the energy retrofit systems market are Trane, Daikin Industries Ltd., Eaton Corporation PLC, Siemens, Ameresco, Johnson Control, Schneider Electric, AECOM Energy, Chevron Energy Solutions, E.ON Energy Services, Orion Energy Systems Inc., Engie SA, Alectra Energy Solutions, General Electric and Signify N.V.

Europe dominated the energy retrofit systems market in 2021 and will lead in the forecast period.

Growing concerns about Greenhouse Gas emissions, widespread adoption of air conditioning appliances in various industries, and rapid urbanization are major growth factors for the energy retrofit systems market.