Quick Navigation

Overview

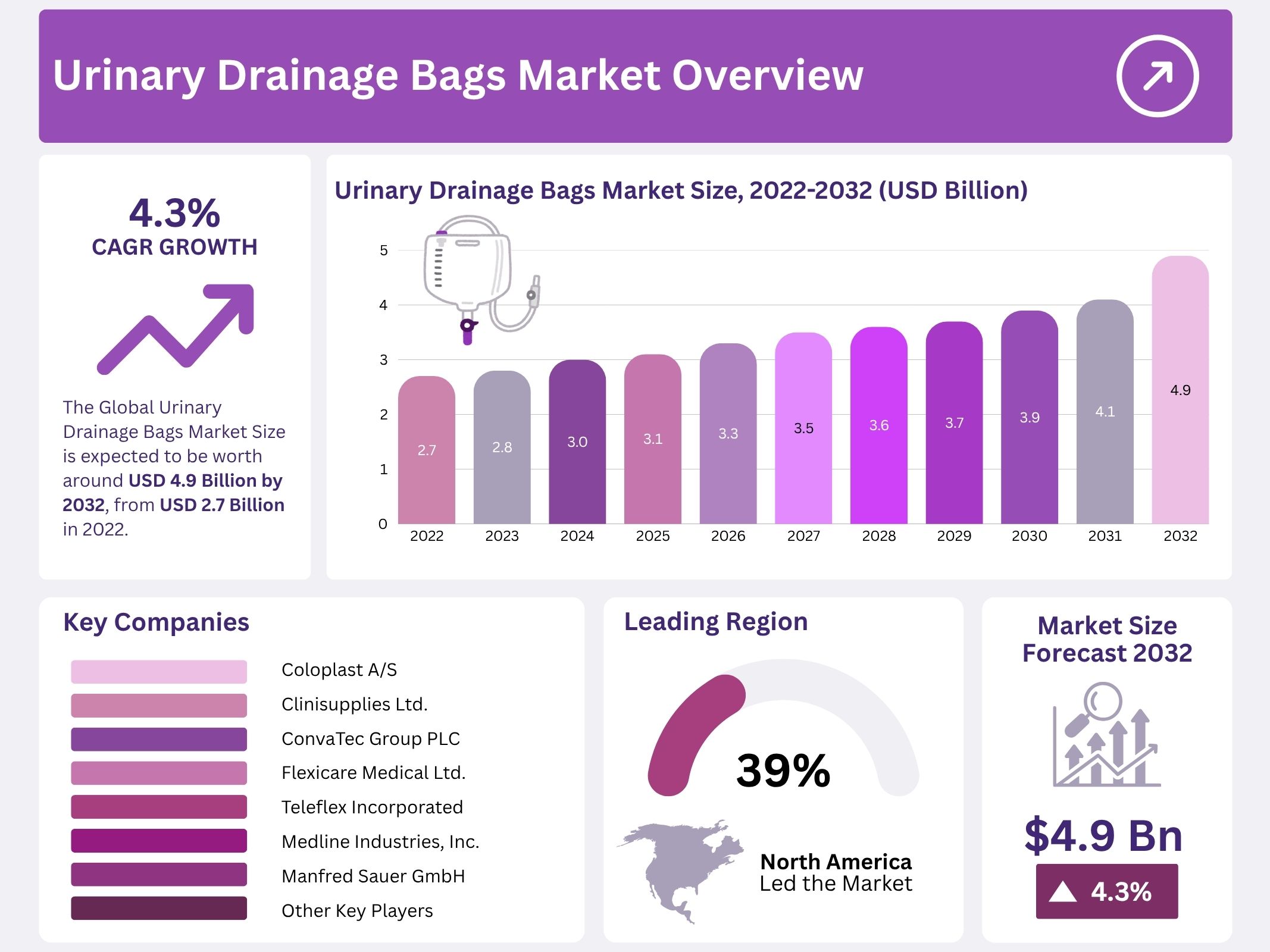

The Global Urinary Drainage Bags Market is projected to reach approximately US$ 4.9 billion by 2032, up from US$ 2.7 billion in 2022, reflecting a compound annual growth rate (CAGR) of 4.3% from 2023 to 2032. This steady rise is driven by major demographic and healthcare shifts, notably the rapid ageing of the world population. The United Nations estimates that people aged 65 years and above will increase from 761 million in 2021 to 1.6 billion by 2050, expanding the base of patients requiring urinary management systems.

Ageing is strongly associated with urinary incontinence and lower urinary tract disorders. These conditions often demand the use of catheters and drainage systems for effective management. The expansion of the elderly population thus directly fuels the demand for both short-term and long-term urinary drainage products in hospitals, nursing homes, and home-care settings. This demographic transformation represents a structural driver that will sustain consistent market growth throughout the forecast period.

The growing prevalence of urological diseases, particularly benign prostatic hyperplasia (BPH), reinforces this demand. According to the U.S. National Institute of Diabetes and Digestive and Kidney Diseases, BPH affects 29–33% of men aged 65 and older, making it one of the most common prostate disorders globally. Frequent urinary retention associated with BPH results in regular catheterization and the need for reliable drainage systems, supporting ongoing consumption across both acute and chronic care environments.

Rising surgical volumes globally add another dimension to market expansion. Major surgeries such as hip and knee replacements typically involve short-term catheter use. OECD data reveal average rates of 172 hip replacements and 119 knee replacements per 100,000 population across member nations in 2021. Each procedure creates immediate demand for closed urinary drainage systems during hospitalization and recovery, reinforcing consistent product utilization in surgical care and rehabilitation centers.

Infection Control, Reimbursement, and Care Shifts

Infection prevention standards and guidelines strongly shape product turnover and quality requirements. The U.S. Centers for Disease Control and Prevention (CDC) recommends maintaining a sterile, closed drainage system and replacing it whenever sterility is compromised. Such mandates lead hospitals and long-term care facilities to maintain ample stock and ensure regular replacement, driving sustained purchases. Similar infection-control frameworks in the United Kingdom encourage safe catheter care at home, further increasing product adoption in community health services.

Reimbursement policies continue to play a vital role in supporting market stability. In the United States, Medicare coverage for urinary catheters and external drainage devices ensures that patients with permanent incontinence or retention receive essential supplies regularly. By minimizing financial barriers, these policies encourage ongoing product use and create predictable demand patterns across home healthcare channels. Similar reimbursement schemes in Europe and Japan maintain strong product penetration in aging populations.

The market is also benefiting from a major shift toward home and community-based care. Health systems worldwide now emphasize home management for patients discharged with long-term catheters. National health services recommend continuous supply of drainage bags and accessories to support patient comfort and infection control. As a result, product demand is increasingly migrating from hospitals to pharmacies, primary-care providers, and home-care distributors, diversifying revenue channels for manufacturers.

Increased awareness and professional training have also improved adherence to best practices, contributing to higher usage of single-use drainage components. Educational programs by organizations such as the CDC emphasize maintaining closed systems and replacing equipment when contamination is suspected. Facilities focused on reducing catheter-associated urinary tract infections (CAUTIs) favor frequent replacement to meet infection-control benchmarks. Together, these factors—policy compliance, reimbursement, and home-care adoption—ensure durable and volume-driven growth in the urinary drainage bags market worldwide.

Key Takeaways

- The urinary drainage bags market is projected to reach US$ 4.9 billion by 2032, expanding at a 4.3% CAGR from US$ 2.7 billion in 2022.

- Leg bags (500–1000 ml) dominate with 58% market share, ensuring enhanced mobility and minimizing backflow risk among users.

- Single-chamber bags lead the segment, primarily due to increasing surgical procedures, while two-chamber bags are witnessing rapid adoption.

- Disposable urinary drainage bags generate the highest revenue, driven by ease of use and reduced urinary tract infection risks.

- Hospitals account for 44% of market share, supported by the high number of surgeries and advanced healthcare infrastructure.

- Ambulatory surgical centers are expected to record notable growth, while home care settings are preferred for managing chronic urinary conditions.

- The market growth is primarily driven by the rising prevalence of urinary incontinence, particularly among the elderly population.

- A lack of awareness, especially in developing regions, continues to restrict market penetration and overall expansion.

- The growing geriatric population is creating substantial opportunities for urinary drainage bags and associated surgical procedures.

- North America leads with 39% market share, while the Asia-Pacific region exhibits the fastest growth due to expanding distribution networks.

Regional Analysis

The North America region accounted for a significant share of the global urinary drainage bags market, capturing around 39.0% of the total revenue. This dominance can be attributed to the growing prevalence of urological disorders, such as urinary incontinence and overactive bladder. The region’s advanced healthcare infrastructure and high awareness among patients further contribute to the market’s expansion. Moreover, the increasing adoption of home healthcare solutions across the United States and Canada supports consistent demand for urinary drainage bags.

The strong presence of key market players in North America has further strengthened the region’s dominance. Companies continuously invest in product innovation, advanced materials, and design improvements to enhance patient comfort and safety. According to the Urology Care Foundation, millions of Americans are affected by overactive bladder conditions each year. This rising disease burden drives continuous demand for efficient urinary drainage solutions. Furthermore, supportive reimbursement policies and access to quality healthcare facilities create favorable market conditions.

Asia-Pacific is projected to witness the fastest growth in the urinary drainage bags market during the forecast period. This growth is primarily driven by the rising population and increasing awareness regarding urological health in emerging economies such as China, India, and Japan. Additionally, improved access to medical care and the introduction of cost-effective urinary drainage products stimulate market expansion. Government initiatives to strengthen healthcare systems and increase medical spending also play a vital role in market development across this region.

The rapid expansion of distribution networks in Asia-Pacific further boosts market penetration. Growing healthcare expenditure and investments by major players in developing countries enhance product accessibility. The increasing prevalence of chronic conditions, aging population, and higher surgical procedure volumes collectively support rising product demand. Furthermore, the adoption of disposable and reusable drainage bags in hospitals and home care settings is expected to accelerate regional market growth. Overall, Asia-Pacific is positioned as a key contributor to the global urinary drainage bags market in coming years.

Segmentation Analysis

Based on product type, the global urinary drainage bags market is divided into large-capacity bags (1000–2000 ml) and leg bags (500–1000 ml). The leg bags segment held a dominant share of 58% and is expected to expand significantly. These bags enhance user independence, allowing easy emptying and improved privacy. Their comfort and anti-reflux valves reduce urine backflow, further boosting adoption. Large-capacity bags, the second-largest category, are anticipated to grow due to their increasing use in hospitals and healthcare facilities owing to cost efficiency.

By the number of chambers, the market is segmented into single, two, and three chambers. The single-chamber urinary drainage bags segment is projected to dominate due to the growing number of surgical procedures and the wide product availability from key players. However, two-chamber bags are expected to record a faster growth rate. Their better comfort and wearability make them preferred among users seeking improved convenience and hygiene standards in medical and home care applications.

Based on usage, the market is categorized into reusable and disposable bags. The disposable segment accounted for the highest revenue share and is expected to maintain its lead. Users widely prefer disposable bags as they are easy to use and handle. They also reduce the risk of urinary tract infections caused by improper cleaning. Additionally, their convenience—no need to empty frequently and easy disposal—further supports market expansion and drives continuous adoption among healthcare professionals and patients.

On the basis of end users, the market is classified into hospitals, clinics, ambulatory surgical centers, home care, and others. The hospital segment accounted for 44% of the market share due to the high volume of urinary-related surgeries and strong healthcare infrastructure. Ambulatory surgical centers are projected to grow rapidly due to increasing outpatient procedures. Furthermore, the rising preference for home care among elderly patients managing chronic diseases is expected to boost the home care segment’s growth during the forecast period.

Key Players Analysis

The urinary drainage bags market is witnessing significant growth due to the wide product range and robust global distribution network of leading companies. The demand for these products is increasing due to the rising prevalence of urinary disorders and post-surgical care requirements. Key manufacturers focus on enhancing product quality, comfort, and hygiene to meet patient needs. Strong brand presence and innovative designs have further strengthened their market position across developed and emerging economies.

Coloplast A/S is a leading contributor to market expansion. Its strong global presence and comprehensive product offerings help it dominate the urinary drainage bags market. The company emphasizes effective distribution channels across multiple regions, ensuring consistent supply and customer reach. ConvaTec Group PLC and Medline Industries, Inc. also play vital roles with advanced product portfolios and efficient healthcare partnerships. These companies collectively drive technological improvements and increase accessibility of urinary drainage products worldwide.

Other significant participants include Teleflex Incorporated, Flexicare Medical Ltd., and Clinisupplies Ltd. These companies continuously invest in product development to enhance patient convenience and clinical outcomes. Their focus on quality, reliability, and cost-effective solutions enables them to cater to a wide range of healthcare facilities. Innovation in material use and design efficiency further supports their market growth. Their strategic initiatives are strengthening their position in the competitive global landscape.

Additional market contributors such as BD, Braun Melsungen, Cardinal Health, Inc., and McKesson Medical Surgical, Inc. are expanding their operations through product diversification and regional collaborations. Companies like Moore Medical LLC, Manfred Sauer GmbH, and Leboo Healthcare Products Limited also hold a notable share through specialized offerings. The competitive environment is defined by continuous innovation, strategic partnerships, and rising global healthcare expenditure, collectively fostering sustained market growth for urinary drainage bags.

Market Key Players

- Coloplast A/S

- Clinisupplies Ltd.

- ConvaTec Group PLC

- Flexicare Medical Ltd.

- Teleflex Incorporated

- Medline Industries, Inc.

- Manfred Sauer GmbH

- BD

- Braun Melsungen

- Cardinal Health, Inc.

- Becton, Dickinson and Company

- Moore Medical LLC

- McKesson Medical Surgical, Inc.

- Leboo Healthcare Products Limited

- Other Key Players

Conclusion

The global urinary drainage bags market is expected to grow steadily due to the increasing elderly population, rising cases of urinary disorders, and growing surgical procedures. Continuous improvements in infection control practices and strong reimbursement support are helping sustain product demand. The shift toward home healthcare and the introduction of user-friendly disposable bags are also driving market expansion. Leading manufacturers are focusing on innovation, quality, and comfort to meet patient needs and strengthen their presence. Overall, the market is projected to maintain consistent growth as healthcare systems emphasize patient safety, convenience, and long-term urinary care solutions.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]