Quick Navigation

Overview

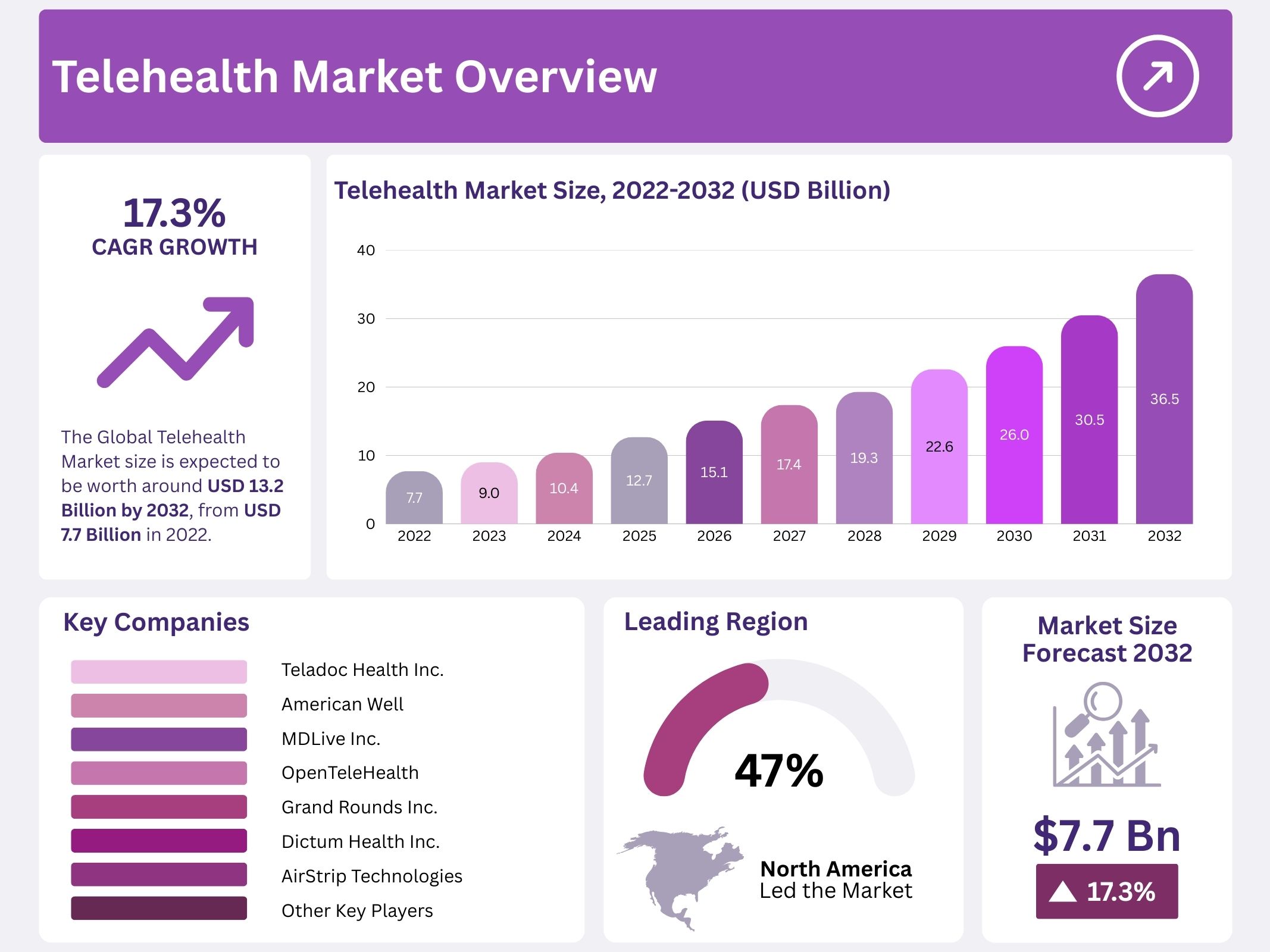

The Global Telehealth Market is projected to reach USD 36.5 billion by 2032. It was valued at USD 7.7 billion in 2022, growing at a compound annual growth rate (CAGR) of 17.3% from 2023 to 2032. This growth can be attributed to the rising demand for remote healthcare services and increasing acceptance of digital health platforms across the globe.

Telehealth refers to delivering healthcare services without in-person visits. These services are mainly provided via the internet using smartphones, tablets, or computers. The COVID-19 pandemic significantly accelerated the adoption of telehealth solutions. However, the foundation for telehealth was already laid before the crisis, with several healthcare systems integrating digital tools into their operations.

The market is driven by several factors. These include growing internet penetration, widespread smartphone usage, and increased investments in IT infrastructure. The rising preference for convenient and real-time access to medical services is also fueling demand. Moreover, cloud-based telehealth platforms are gaining popularity due to their scalability and ease of deployment. As a result, the cloud-based delivery segment is expected to witness the highest growth over the forecast period.

Healthcare providers are using telehealth not only for consultations but also to monitor patient health data in real-time. This enables physicians to gain valuable insights during ongoing treatments. The growing use of telehealth apps has further expanded access to medical care, especially in rural and underserved regions. For example, during the pandemic, Greece used telehealth technology to enhance public health education and bridge access gaps.

Strategic developments by leading market players are also contributing to growth. These include partnerships, mergers, acquisitions, and new product launches focused on telemedicine. The aim is to enhance patient engagement and improve clinical outcomes using innovative digital health tools. As healthcare systems continue to modernize, the telehealth market is expected to see robust expansion worldwide.

Key Takeaways

- The global telehealth market was valued at USD 7.7 billion in 2022 and is forecasted to grow at a 17.30% CAGR through 2032.

- Telehealth delivers healthcare services remotely via smartphones, tablets, or computers, reducing the need for in-person clinical visits.

- Digital Shift: The rising demand for convenient, digital-first healthcare services is accelerating the global adoption of telehealth solutions.

- Based on Type Analysis, Software Segment dominates due to its use in workflow management and integration within open medical care systems.

- Based On Application, the Patient monitoring section is the fastest-growing segment, supported by increased elderly care and chronic disease management needs.

- In End-User Segment, the Hospitals are the primary users of telehealth, while homecare emerges as a flexible and adaptable growth area.

- Technology Gaps: Technological limitations in developing countries hinder widespread implementation of telehealth infrastructure.

- Emerging Economies: Nations like India, Brazil, China, and South Africa offer strong potential due to growing healthcare investments.

- North America Leads: North America held a 47.0% market share in 2022, driven by advanced infrastructure and favorable health policies.

Regional Analysis

North America held the leading share in the global telehealth market in 2022, accounting for 47.0%.

This dominance is attributed to high healthcare IT investments and widespread internet and smartphone penetration. These factors have supported the adoption of digital health services. The region has also seen favorable reimbursement policies and regulatory frameworks that promote telehealth integration. Furthermore, the growing demand for remote care, coupled with the strong presence of leading telehealth providers, continues to support regional growth. This makes North America a mature and influential market for virtual healthcare solutions.

This growth is primarily driven by increasing chronic disease cases and a shift in patient preferences toward remote healthcare. A large portion of the population suffers from ongoing health issues requiring frequent monitoring. The ability to access treatment for both acute and chronic conditions through virtual platforms is proving vital. Additionally, policy initiatives promoting digital health equity are expected to accelerate adoption. As a result, the region is positioned to maintain its dominant market share during the forecast period.

Asia Pacific is projected to be the fastest-growing region in the global telehealth market

This growth is supported by a rapidly ageing population in countries such as Japan and India. The increasing burden on traditional healthcare systems is being eased through telemedicine. Improvements in healthcare infrastructure and growing investments in digital platforms are driving adoption. Furthermore, rising smartphone usage and internet access in rural areas are increasing reach. Government support and national digital health missions are expected to further enhance regional growth and create a competitive market environment for telehealth solutions.

The region benefits from a large population base and ongoing urbanization, both of which are expanding healthcare demand. Rising awareness of digital health services and the efforts of regional players to offer localized solutions are crucial growth drivers. Additionally, cost-effective healthcare alternatives like telemedicine are gaining popularity in low-income areas. These conditions, coupled with strategic partnerships and technological advancements, are anticipated to strengthen the telehealth ecosystem. The region is likely to emerge as a key contributor to global market expansion.

Segmentation Analysis

The software segment is identified as the most lucrative in the global telehealth market during the forecast period. This growth can be attributed to rising demand for streamlined medical care systems and efficient workflow management. Software systems are continuously upgraded to improve the performance of telehealth platforms. These improvements contribute to better user experiences and enhanced clinical outcomes. Moreover, the increased adoption of cloud-based solutions supports scalability and accessibility. As a result, software continues to lead revenue generation across the telehealth ecosystem.

In terms of application, telemedicine, patient monitoring, and continuous medical education are the key segments. Among these, patient monitoring is expected to register the fastest growth rate. This is due to the increasing demand for real-time health tracking, particularly among the elderly. Smart wearable devices are being widely used for continuous patient evaluation. The market is further supported by advancements in connectivity and mobile technologies. These developments enable remote care and drive demand for monitoring services, especially for chronic disease management.

Regarding end users, hospitals dominate the global telehealth market and are projected to maintain their lead. The adoption of telemedicine tools helps reduce operational burdens on medical staff. These technologies also improve clinical efficiency and reduce healthcare costs. Meanwhile, the homecare segment is emerging as the most adaptable. This is fueled by rising awareness about hospital-acquired infections and a preference for home-based care. Older adults, in particular, prefer receiving treatment at home. Therefore, homecare services are expected to accelerate telehealth adoption significantly.

Key Players Analysis

Several emerging players in the global telehealth market are actively adopting strategic initiatives to expand their presence in international markets. These companies are primarily focusing on scaling operations, enhancing research and development capabilities, and increasing technological collaborations. Portfolio diversification remains a key objective, supported through investments and innovation. For instance, Koninklijke Philips N.V. and GE Healthcare have strengthened their product portfolios by introducing scalable virtual care platforms, while maintaining cost competitiveness. Such strategies are aimed at increasing market share, enhancing service delivery, and addressing growing demand for digital healthcare solutions.

The telehealth industry is witnessing increased investment activity, particularly in product development and technological upgrades. Mergers and acquisitions have become central to business expansion and competitive positioning. In June 2020, Prophet successfully secured a 69.2% stake in Cerner Corporation, signaling a strong move toward portfolio consolidation. Similarly, Philips introduced the Acute Care Telehealth platform, which enables customizable virtual care solutions. These initiatives demonstrate a clear focus on expanding offerings while addressing the rising need for integrated and accessible telehealth infrastructure worldwide.

Post-acquisition, companies such as Cerner and Philips are expected to concentrate on developing advanced healthcare analytics platforms and expanding their regulatory footprint. These players aim to improve healthcare accessibility by combining digital innovation with broader market reach. Moreover, portfolio synergies and operational integration are anticipated to improve service efficiency and strengthen strategic positions. As competition intensifies, companies are adapting to regulatory changes and increasing their investments in regional markets to tap into the growing need for remote healthcare delivery.

The global telehealth market is moderately fragmented due to the presence of numerous local and regional providers. Companies are employing various strategies—such as investments, partnerships, and product launches—to gain a competitive edge. Marketing campaigns focused on raising awareness and enhancing product visibility are also being prioritized. Additionally, pricing strategies and value-based offerings are being adopted to meet diverse consumer needs. Larger firms with strong brand equity and expansive distribution networks continue to challenge smaller players, pushing the overall market toward innovation-driven growth.

- Teladoc Health Inc.

- American Well

- MDLive Inc.

- OpenTeleHealth

- Grand Rounds Inc.

- Dictum Health Inc.

- AirStrip Technologies

- INTeleICU

- Masimo

- Other Key players

Conclusion

The global telehealth market is showing strong and steady growth, driven by the increasing demand for remote healthcare services. Digital platforms are helping patients access care conveniently, especially in rural and underserved areas. Hospitals, homecare services, and healthcare providers are rapidly adopting telehealth for consultations and patient monitoring. Advancements in cloud technology and wearable devices support this trend. North America remains the largest market, while Asia Pacific is expected to grow the fastest. Companies are investing in innovation, partnerships, and new products to stay competitive. With continued support from governments and improved digital infrastructure, telehealth is becoming an essential part of modern healthcare systems.

Get in Touch with Us:

Contact Person: Lawrence John.

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]