Quick Navigation

Overview

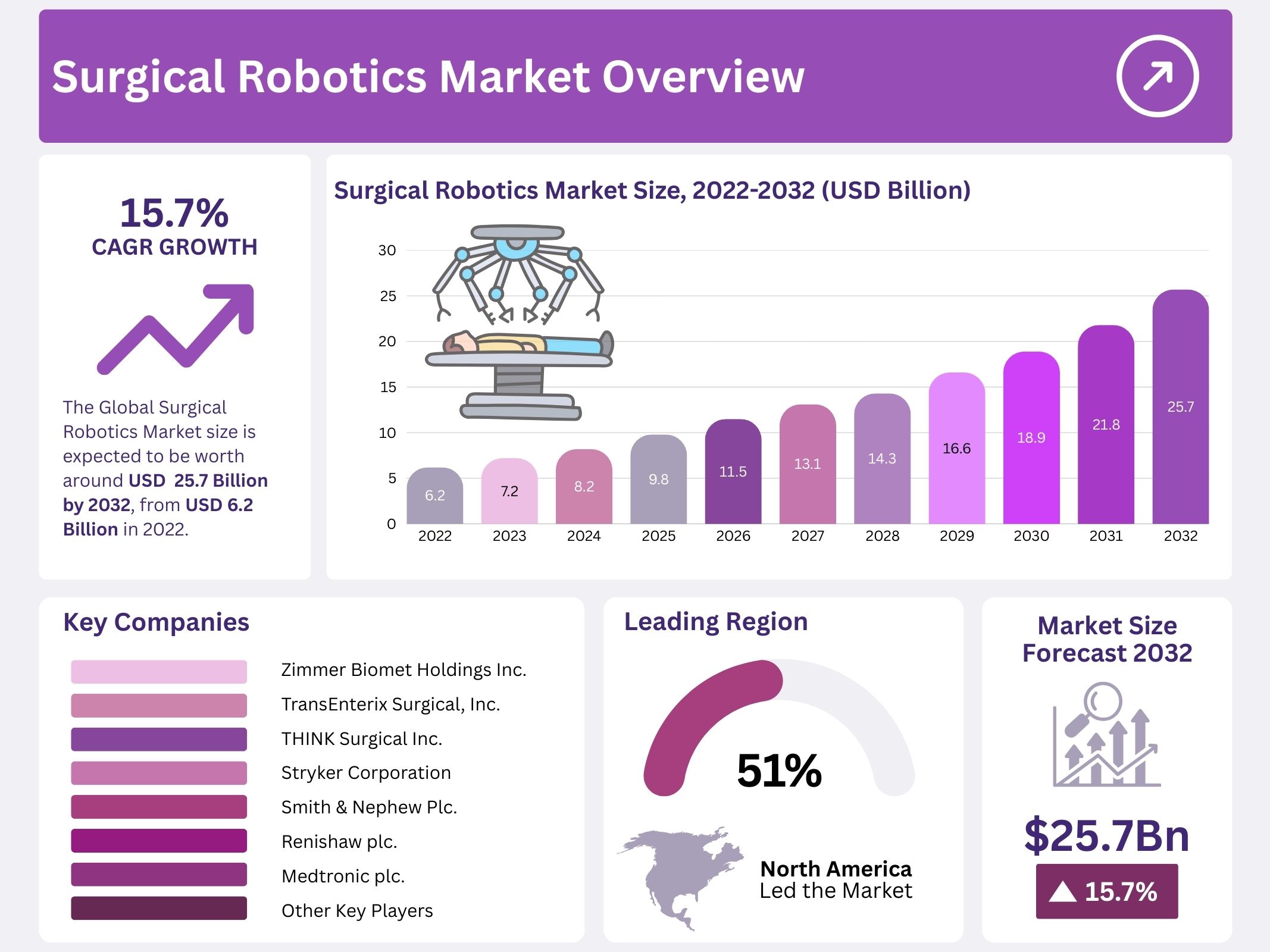

Global Surgical Robotics Market Size was USD 6.2 billion in 2022. It is projected to reach USD 25.7 billion by 2032. A CAGR of 15.70% is expected for 2023 to 2032. Growth is underpinned by adoption of robotic platforms. Demand is increasing across minimally invasive procedures. Precision, control, and reproducibility are being enhanced. Workflow standardization is improving outcomes. Hospitals pursue differentiation and capacity gains. Vendor pipelines remain active. Strategic partnerships strengthen distribution and training ecosystems. Clinical evidence is accumulating across specialties. Reimbursement clarity is improving in priority markets.

Surgical robotics denotes systems designed to assist surgeons during diverse procedures. These systems enable minimally invasive access with improved dexterity and visualization. A global shortfall of surgeons and physicians is intensifying adoption. Automated equipment is being preferred for consistency and precision. Operating room efficiency is improved through instrument articulation and tremor filtration. Training modules and simulators are standardizing skills. As awareness rises, patient referrals are redirected to robotic centers. Perceived benefits include smaller incisions and faster recovery. Conversion rates to open surgery are reduced.

Rising investment by international and regional players has accelerated innovation. New platforms integrating artificial intelligence and cloud connectivity are being introduced. Performance gains and workload reduction have been reported. Capital programs are supported by leasing and managed services. Orthopedic use cases are expanding rapidly. Degenerative bone disorders are increasing knee and hip replacement volumes. Osteoporosis and arthritis prevalence is driving case mix shifts. Robotic planning and execution improve alignment and implant positioning. Consequently, adoption curves in orthopedics are steepening across hospitals and ambulatory centers.

Cost remains the principal restraint. Robot-assisted procedures are costlier than conventional minimally invasive surgeries. Capital, service, and disposable costs increase per-case economics. Learning curves demand dedicated training time and proctoring. Surgical errors, though infrequent, remain a public health concern. Standardized protocols are required to mitigate risks. Payer scrutiny persists where economic superiority is unproven. Professional guidance remains cautious. The American College of Obstetricians and Gynecologists recommends robotic hysterectomy mainly for complex or unusual cases. Consequently, value demonstration and cost reduction will be decisive for broader penetration.

Key Takeaways

- Experts project the Surgical Robotics Market to expand at an average annual growth rate of 15.7%, highlighting its strong future potential.

- By 2032, the global market size is anticipated to reach an impressive USD 25.7 billion, reflecting rising adoption across healthcare sectors.

- Growth is fueled by advanced technologies, including 3D HD imaging sensors, precision cameras, robotics-based calculations, and remote navigation systems enabling improved surgical performance.

- The accessory segment, comprising robotic components, is projected to command around 49% of total market share, making it the largest contributor.

- Neurosurgery remained a lucrative segment in 2022 and is expected to continue dominating due to rising demand for advanced brain surgical interventions.

- Hospitals emerged as the key end-users in 2022, accounting for 73% of the market, and are predicted to maintain dominance moving forward.

- North America secured a 51% revenue share in 2022, establishing itself as the leading regional market for surgical robotics adoption.

- The Asia Pacific region is expected to witness remarkable growth from 2023 to 2032, driven by improving healthcare infrastructure and increasing robotic investments.

Regional Analysis

North America held the largest share of the global surgical robotics market, accounting for about 51% of total revenue, in 2022. This dominance is supported by strong adoption of robotic-assisted surgeries across hospitals and specialty clinics. Limited availability of skilled surgeons has accelerated the reliance on automated systems. The U.S. healthcare system is focusing heavily on advanced technology integration. This shift has fueled a demand for surgical robots, strengthening North America’s position as the most lucrative regional market.

The U.S. market is particularly driving regional growth, with growing patient dependence on advanced surgical care solutions. Adoption of robotic-assisted surgical instruments continues to rise, supported by increasing healthcare infrastructure. Hospitals are upgrading facilities with advanced automation tools to improve accuracy, reduce surgical errors, and enhance patient recovery. These factors collectively support the rapid integration of robotic systems in clinical workflows. As healthcare providers seek cost-effective and efficient treatment, demand for surgical robots is set to expand.

Rising cases of chronic diseases such as cancer, cardiovascular disorders, and diabetes are also creating significant demand for robotic surgery solutions in North America. These conditions require precision-based treatments, which robotic systems provide more effectively than traditional surgical approaches. As chronic disease prevalence rises, healthcare facilities are prioritizing minimally invasive procedures to improve patient outcomes. This trend is pushing the adoption of surgical robots at a faster pace. Consequently, North America continues to remain a strong revenue contributor in this industry.

The Asia Pacific region, on the other hand, is projected to grow at a lucrative rate during the forecast period. Rapid population growth is increasing demand for healthcare services, while advanced automated surgical devices are gaining acceptance. Countries such as China, Japan, and India are investing in novel healthcare facilities. Growing awareness about the benefits of robotic surgeries and rising acceptance of modern medical technology are strengthening regional growth. With improving infrastructure and healthcare investments, Asia Pacific is set to emerge as a high-potential market.

Segmentation Analysis

The surgical robotics market, based on components, is segmented into accessories, systems, and services. Among these, the accessory segment emerges as the most lucrative. Increasing geriatric populations and the rising prevalence of chronic disorders such as diabetes, HIV, AIDS, and arthritis are driving the adoption of robotic solutions. The demand for disposable and reusable robotic accessories supports recurring revenue generation. Additionally, the services segment is expected to expand steadily due to the growing volume of robot-assisted surgeries worldwide, fueling market development.

The market, when analyzed by surgery type, includes gynecology, neurosurgery, general surgery, orthopedic, urology, and other procedures. Neurosurgery is estimated to be the most lucrative segment. Robotic systems in neurosurgery offer higher precision compared to traditional methods, enhancing treatment accuracy. The rising prevalence of neurological conditions and cancer-related procedures boosts the adoption of robotic-assisted treatments. Furthermore, orthopedic surgeries hold a significant share, largely driven by injuries from accidents and the growing demand for minimally invasive procedures, particularly laparoscopic surgeries.

By end-user, the market is categorized into hospitals and ambulatory surgical centers. The hospital segment dominates with a revenue share of 73% and is projected to grow at a robust CAGR. Hospitals adopt surgical robots to enhance efficiency, improve patient outcomes, and handle large volumes of complex surgical procedures. Expanding hospital infrastructure and skilled healthcare professionals further strengthen this segment. In addition, emerging economies with growing hospital capacities create new opportunities. Rising surgical admissions and advanced robotic adoption in hospital environments continue to drive strong market growth.

Key Players Analysis

Emerging novel players in the global surgical robotics market are focusing on diverse strategic policies to expand their presence in international markets. These players are aiming to strengthen their market position by emphasizing new-generation robotic equipment and adopting advanced technologies. The rising demand for automated surgical instruments is also creating growth opportunities for innovative companies. This shift in demand is pushing new entrants to invest in research and development, ensuring their competitiveness in the global market.

Key players are also engaging in mergers, collaborations, and acquisitions to expand their market footprint and improve competitiveness. Such strategic moves are helping companies strengthen their product portfolio and enhance global reach. The adoption of advanced robotic technologies is further intensifying competition. Moreover, the focus on establishing new and efficient equipment is driving innovation across the sector. These collective strategies are shaping the market landscape, ensuring that both established leaders and emerging players remain active contributors to market growth.

Conclusion

The surgical robotics market is on a strong growth path, supported by rising adoption of advanced technologies and growing demand for minimally invasive surgeries. Hospitals and clinics are increasingly investing in robotic platforms to improve patient outcomes, reduce recovery time, and enhance surgical precision. Expanding use cases in areas such as neurosurgery and orthopedics highlight the versatility of these systems. While high costs and training requirements remain challenges, ongoing innovation and strategic partnerships are helping to address these barriers. With improving awareness and expanding healthcare infrastructure worldwide, surgical robotics is set to become a key driver of modern surgical care in the coming years.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Robotic Flight Simulator Surgery Market || Robotic Dentistry Market || Robotic Endoscopy Devices Market || Robotic Prosthetics Market