Quick Navigation

Overview

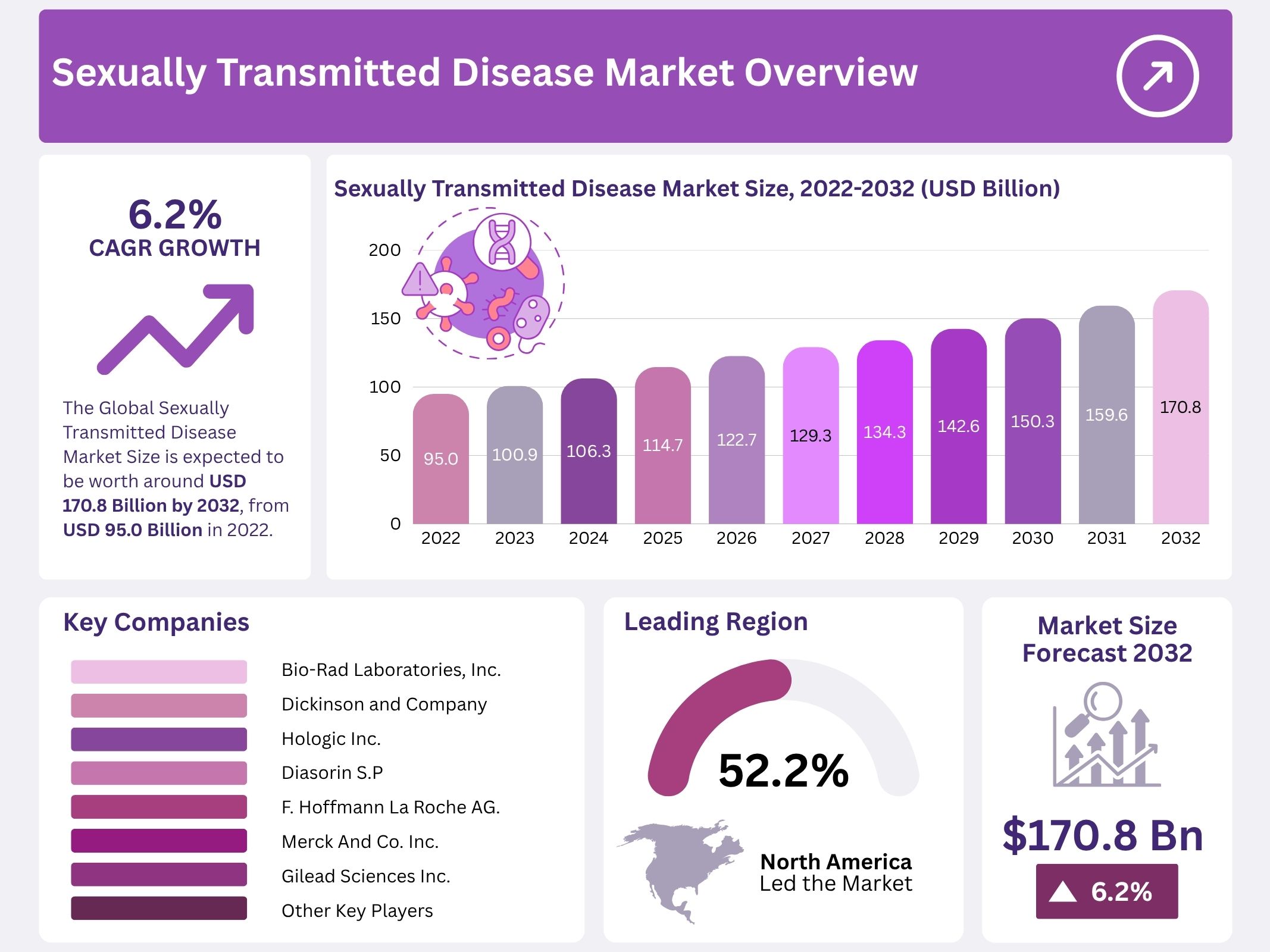

The Global Sexually Transmitted Disease (STD) Market is projected to reach USD 171 billion by 2032, rising from USD 95 billion in 2022. Growth is expected at a CAGR of 6.17% during the forecast period. The market expansion is driven by the rising prevalence of infections such as chlamydia, gonorrhea, syphilis, HPV, and herpes. Changing sexual patterns, reduced condom usage, and limited awareness in developing regions continue to elevate disease burden and support market demand.

The increasing adoption of screening programs has strengthened diagnostic uptake. Government initiatives, workplace testing, and educational campaigns have raised the number of individuals undergoing routine checks. Rapid tests and molecular assays, including nucleic acid amplification tests, have improved detection accuracy. Early diagnosis is being prioritized by healthcare systems to control transmission. Technological progress in diagnostic tools has improved sensitivity and reduced turnaround time, which has supported steady demand across public and private settings.

Expansion of high-risk populations has contributed to rising infection rates. Growth in urban migration, socio-economic gaps, and limited access to healthcare services creates vulnerability, especially among individuals with multiple partners and men who have sex with men. These demographic shifts continue to influence disease patterns. As infection rates climb, demand increases for preventive products, treatment drugs, and follow-up diagnostics. This trend reinforces long-term market growth in both mature and emerging economies.

Government agencies and global organizations have intensified their efforts to manage STD incidence. Investments in public awareness, free or subsidized testing, and accessible treatment programs are improving detection and treatment coverage. International funding has strengthened surveillance systems and enhanced healthcare infrastructure in low-income regions. These initiatives expand access to care and support the distribution of diagnostic kits, vaccines, and therapeutic drugs, thereby driving additional market opportunities worldwide.

Technological advancement in prevention and treatment has further supported market expansion. Uptake of HPV vaccines, progress in long-acting HIV prevention regimens, and research toward new STD vaccines are creating new avenues for investment. Efforts to develop treatments for antibiotic-resistant pathogens are increasing pharmaceutical innovation. Growing awareness promoted through digital platforms and the rising use of at-home testing kits have improved patient engagement. Improved regulatory frameworks and better reimbursement systems continue to encourage sustained market growth.

Key Takeaways

- The global STD market was described as expanding steadily, reaching nearly USD 171 billion by 2032 from USD 95 billion in 2022 at a 6.17% CAGR.

- Growth was attributed to increased unprotected sexual activity, rising public awareness, and supportive government programs encouraging regular testing and early diagnosis.

- Chlamydia was identified as the most commonly tested STD in 2022, driven by limited protective measures and insufficient public awareness.

- Syphilis was highlighted as a rapidly expanding segment, projected to represent over 20% of the STD testing market by 2022.

- Laboratory testing was reported as the dominant testing location, reflecting the reliance on specialized diagnostic procedures for accurate detection.

- Market segmentation was outlined across disease types, testing locations, and device categories, reflecting diverse diagnostic needs and technological adoption.

- Rising global STD prevalence, particularly among young adults, was linked to increased testing demand driven by risky behaviors and limited awareness.

- Expanding diagnostic demand and improved disease awareness were recognized as key opportunities, supported by evolving treatment approaches and advanced testing technologies.

- Market trends included growing infection rates, enhanced educational outreach, and government-led initiatives improving early screening and treatment uptake.

- Advanced NAAT-based diagnostics were acknowledged for delivering higher sensitivity and specificity, especially in detecting chlamydia and gonorrhea infections.

- North America was presented as the leading regional market, accounting for 52.2% of diagnostic revenue, with strong testing infrastructure.

- China was expected to drive Asia-Pacific market expansion with a projected CAGR of 7.2% from 2022 to 2032.

Regional Analysis

North America is dominating the sexually transmitted disease testing market. The region is expected to retain the largest revenue share because demand for advanced STD diagnostic tests continues to rise. It is estimated that North America will hold about 52.2% of global diagnostics revenue. Growth in the United States is further strengthening this position. A CAGR of 7.7% between 2022 and 2032 has been projected for the U.S. market. This growth is supported by high infection rates and increased testing awareness across the country.

Chlamydia remains the most common sexually transmitted infection in the United States. Its rising incidence is driving significant demand for diagnostic testing. Young women between 15 and 25 years of age account for a major portion of confirmed cases. As testing expands in this demographic group, market demand is expected to grow steadily over the forecast period. The increasing need for early detection is contributing to market expansion and shaping the regional outlook for STD diagnostics.

Asia Pacific is projected to secure the second-largest share of the global market. Growth in this region is supported by strong demand in China. China’s wide availability of diagnostic test inventories is expected to increase adoption rates. The market in China is anticipated to grow at a CAGR of 7.2% from 2022 to 2032. Other regions, including the United Kingdom, South Korea, and Japan, are expected to show slower growth. Limited awareness and delayed testing continue to restrict diagnostics adoption and reduce market potential in these areas.

Segmentation Analysis

The sexually transmitted disease (STD) testing market has been shaped by a wide range of infections, including chlamydia, gonorrhea, herpes simplex virus, syphilis, and human papillomavirus. Chlamydia accounted for the largest share in 2022. This dominance was supported by limited public awareness and low adoption of barrier protection. The market growth has been driven by the rising global incidence of multiple infections. These include trichomoniasis, chancroid, vaginitis, hepatitis B, and HIV. Bacterial and viral STDs continue to influence testing demand.

Chlamydia generated significant revenue in earlier years, with an estimated value of over USD 6 billion in 2014. However, the rising spread of syphilis has strengthened its role in diagnostic testing demand. Syphilis testing is expected to represent more than 20% of the market by 2022. This segment has grown at a strong pace due to increasing reported cases worldwide. Elevated awareness, improved diagnostic tools, and expanded public health screening programs have supported this growth trend. These factors continue to shape overall market dynamics.

The market is segmented by disease type, testing location, and diagnostic devices. Laboratory testing holds the largest share because most STD tests are processed in clinical laboratories. This preference is supported by higher accuracy and advanced equipment. Point-of-care testing also plays a growing role due to faster results. Device segmentation includes laboratory devices and point-of-care devices. These categories serve different diagnostic settings. Their adoption is influenced by healthcare infrastructure, testing speed, and clinical requirements. Together, these segments define the structure of the STD testing industry.

Key Market Segments

Based on Disease Type

- Chlamydia

- Gonorrhea

- Herpes Simplex Virus

- Syphilis

- Human Papillomavirus

- Cancroid

- Other Diseases

Based on Location

- Laboratory Testing

- Point of Care (POC) Testing

Key Players Analysis

The competitive landscape of the sexually transmitted disease (STD) diagnostics market is shaped by steady investments in advanced testing technologies. Growth is driven by increasing disease prevalence and wider adoption of molecular diagnostics. Key players are expanding product portfolios through innovation in CT/NG tests and rapid assays. The progress of FDA-cleared diagnostic tools has strengthened market confidence, and demand has been supported by rising awareness and screening programs. These developments have created strong incentives for companies to pursue strategic expansion across global regions.

Strategic collaborations have become a central approach for enhancing market penetration. Partnerships, mergers, and joint ventures are being used to broaden distribution networks and accelerate product availability. Companies are strengthening their presence in both clinical laboratory and point-of-care settings. This coordinated activity has supported faster adoption of at-home testing services. Initiatives such as free home delivery programs and online diagnostic pathways have encouraged market acceptance and created favorable conditions for growth among established diagnostic manufacturers.

Product innovation has been visible in nucleic acid amplification tests, rapid diagnostic kits, and automated laboratory systems. The increasing shift toward home-based testing and self-collection methods has expanded opportunities for manufacturers. Firms known for molecular diagnostics and clinical testing solutions are investing in improved accuracy and workflow efficiency. Players such as Qiagen, Hologic, Bio-Rad Laboratories, and Becton Dickinson are contributing to this transition. Their advanced platforms have supported reliable detection and contributed to the wider clinical adoption of modern STD testing solutions globally.

The market also includes pharmaceutical and biotechnology companies focused on complementary therapeutic and diagnostic capabilities. Firms such as Merck, Gilead Sciences, Inovio Pharmaceuticals, and AbbVie support the ecosystem through research related to prevention and treatment. Additional diagnostic specialists, including Diasorin, Roche, Biomerieux, Orasure Technologies, Everlywell, CTK Biotech, and AdvaCare Pharma, strengthen overall competition. Their presence has diversified product availability and improved global access. This broad participation has reinforced market expansion and is expected to support sustained growth through 2032.

Market Key Players

- Bio-Rad Laboratories, Inc.

- Dickinson and Company

- Hologic Inc.

- Diasorin S.P

- F. Hoffmann La Roche AG.

- Merck And Co. Inc.

- Gilead Sciences Inc.

- Inovio Pharmaceuticals Inc.

- BIOGENIX Inc. Pvt.

- Other Key Players.

Conclusion

The sexually transmitted disease market is expected to grow steadily as infections continue to rise and testing becomes more widely used. Demand is being supported by greater awareness, improved diagnostic tools, and stronger public health programs. The market is also benefiting from better access to care, increased use of home testing kits, and ongoing advancements in prevention and treatment. Leading companies are expanding their technologies to offer faster and more accurate results, which is improving testing uptake across regions. Continued investment in diagnostics, vaccines, and digital awareness campaigns is expected to support long-term market growth and strengthen global disease control efforts.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]