Quick Navigation

Introduction

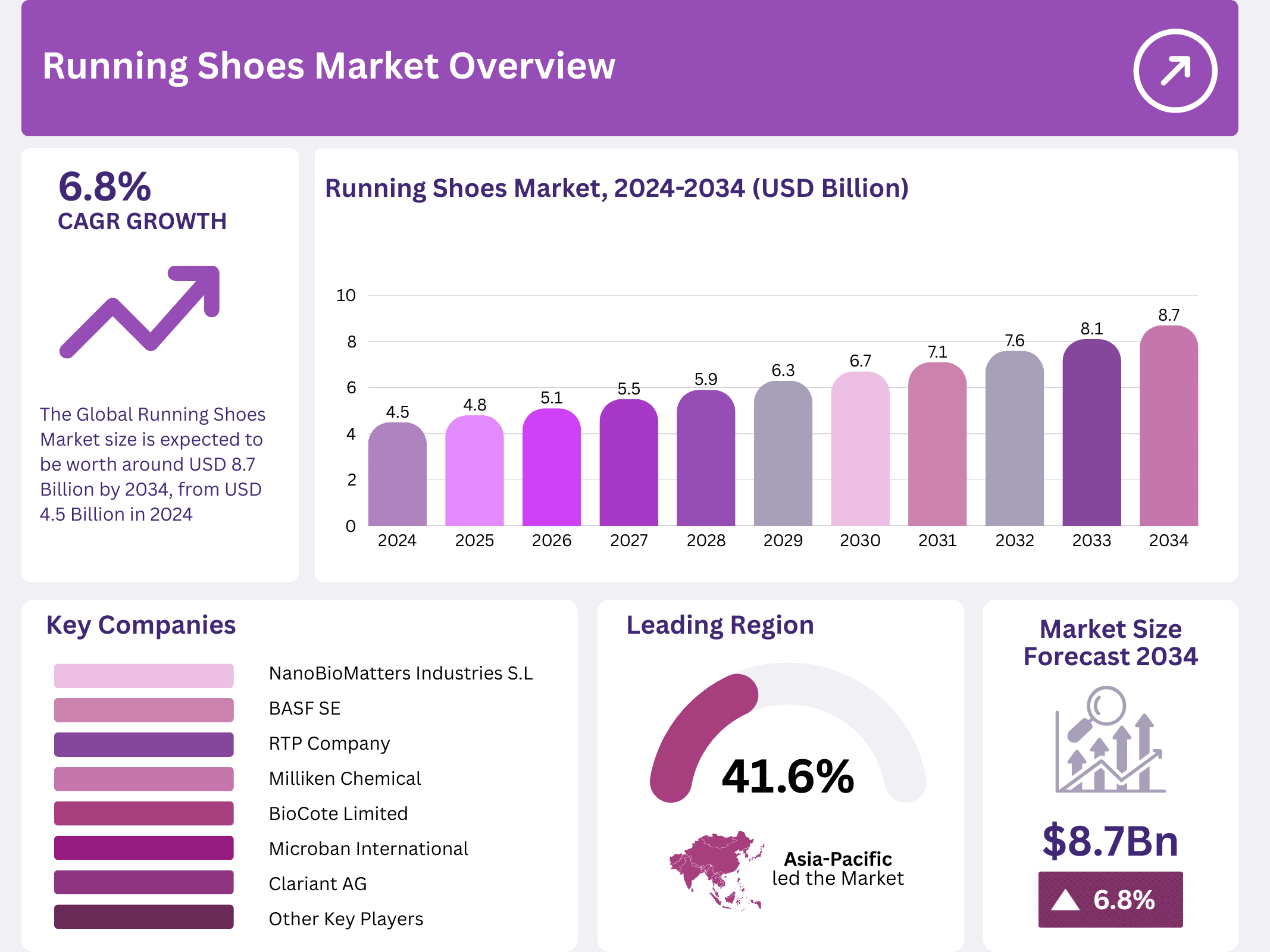

The global running shoes market is entering a transformative decade. Valued at USD 4.5 billion in 2024, the industry is projected to nearly double, reaching USD 8.7 billion by 2034. This robust expansion reflects a worldwide shift toward healthier, more active lifestyles at every demographic level.

Consequently, running is no longer a niche sport — it is a mainstream pursuit. With over 1.1 to 1.3 million people completing marathons annually, footwear demand continues to surge. Brands are responding with advanced materials, smarter designs, and a broader product range to match diverse consumer needs.

Furthermore, the market is being shaped by technological innovation. The average men’s running shoe weighs just 9.8 oz, while women’s models are 15% lighter at 8.4 oz. These precision-engineered designs highlight how performance demands are pushing manufacturers to continuously evolve their offerings.

Moreover, pricing dynamics reveal a maturing market. The average MSRP stands at $132.9, with 18.7% of shoes priced below $100. Premium carbon-plated road models command up to $205, demonstrating healthy appetite across both budget-conscious and performance-driven consumer segments.

In addition, sustainability is emerging as a pivotal force. Eco-conscious buyers are demanding greener production methods and recycled materials. As a result, manufacturers that embrace sustainable innovation are increasingly well-positioned to capture a larger share of this fast-growing global market.

Finally, the Asia Pacific region leads all others, holding a 41.6% market share in 2024, valued at USD 1.87 billion. Combined with strong momentum in North America and Europe, the running shoes market presents compelling opportunities for investors, brands, and supply chain stakeholders alike.

Key Takeaways

- The Global Running Shoes Market is projected to reach USD 8.7 Billion by 2034, growing from USD 4.5 Billion in 2024 at a CAGR of 6.8% from 2025 to 2034.

- The Inorganic segment dominates the market with a 54.3% share in 2024, driven by durable materials like OBPA, DCOIT, and Triclosan.

- The Plastics segment leads by application with a 36.0% market share in 2024, benefiting from its durability and structural support in running shoes.

- The Healthcare segment holds a 27.5% share in 2024, driven by ergonomic and orthopedic footwear demand among medical professionals.

- The APAC region leads the market with a 41.6% share in 2024, valued at USD 1.87 billion, fueled by a rising middle class and increasing fitness trends.

Market Segmentation Overview

The Inorganic segment commands the largest share by type, capturing 54.3% of the market in 2024. Compounds such as OBPA, DCOIT, and Triclosan are prized for their antimicrobial and durability properties. Additionally, Silver, Copper, and Zinc sub-segments contribute meaningfully through their bacteria-inhibiting and odor-resistant characteristics, enhancing foot hygiene and overall shoe longevity.

Turning to applications, the Plastics segment leads with a 36.0% share, as versatile plastics provide essential structural support in soles and frames. Meanwhile, the Silicone segment delivers superior cushioning and shock absorption. The Paints & Coatings segment adds waterproofing and aesthetic value, whereas Pulp & Paper contributes to eco-friendly packaging initiatives across the industry.

Regarding end-users, the Healthcare segment dominates with a 27.5% share, driven by demand from nurses and physicians requiring ergonomic, long-wearing footwear. Furthermore, the Food & Beverage and Packaging industries are emerging as significant end-user groups, with employees requiring slip-resistant, cushioned shoes. The Consumer Goods, Automotive, and Textile sectors also represent growing demand pools for performance-oriented running footwear.

Drivers

Enhanced Focus on Health and Fitness Awareness: A worldwide rise in health consciousness is a primary growth engine. As sedentary desk-based lifestyles become the norm, more consumers are turning to running as an accessible, cost-effective exercise. Brands are capitalizing on this shift by developing shoes that cater to both novice joggers and competitive athletes, broadening the market’s addressable audience significantly.

Technological Advancements in Shoe Design: Innovation in cushioning systems, lightweight materials, and performance-tracking technology is elevating consumer expectations. Carbon-plated road shoes, now retailing at up to $205, demonstrate buyers’ willingness to invest in cutting-edge footwear. Embedded sensors and adaptive stability features are further differentiating premium offerings, sustaining strong demand growth across all income brackets.

Use Cases

Professional and Recreational Running: With over 1.1 million marathon finishers annually, the demand for specialized running shoes is direct and measurable. Road-specific shoes averaging 9.7 oz and trail shoes at 10.4 oz address distinct performance needs. Both segments are growing as community running events and clubs continue to recruit new participants across urban and suburban populations worldwide.

Healthcare and Occupational Footwear: Beyond athletics, running shoes are increasingly adopted in professional settings. Healthcare workers — including nurses and doctors — depend on ergonomic, shock-absorbing footwear for long shifts. Similarly, warehouse, logistics, and food service workers require durable, slip-resistant footwear. This occupational use case represents a steady, recession-resistant demand stream that is diversifying the market’s revenue base.

Major Challenges

High Cost of Premium Products: Advanced running shoes featuring the latest cushioning and stability technology can retail at over $200, limiting accessibility for budget-conscious consumers. In price-sensitive emerging markets, this premium gap remains a significant barrier to adoption. Manufacturers must balance technological ambition with affordability to unlock the full growth potential of these high-population regions.

Rising Injury Rates Among Runners: Despite innovations in shoe design, approximately 50% of regular runners experience injuries annually. This statistic reveals a persistent gap between product promises and real-world outcomes. It also places reputational pressure on brands, compelling continued investment in biomechanics research, fit customization, and injury-prevention technologies to sustain consumer trust and loyalty.

Business Opportunities

Expansion into Emerging Markets: Asia Pacific already commands 41.6% of global market share, yet significant headroom remains in Southeast Asia, South Asia, and Latin America. Rising disposable incomes, growing youth populations, and expanding fitness culture in countries like India, Brazil, and Indonesia create fertile ground for both established brands and nimble new entrants seeking volume growth.

Growth of Eco-Friendly Footwear: Consumer demand for sustainable products is translating directly into purchasing behavior. Brands that integrate recycled materials, biodegradable components, and transparent supply chains are gaining competitive advantage. This shift represents not only an ethical imperative but a tangible market differentiator — especially among younger, environmentally aware consumers who are becoming the dominant buyer cohort globally.

Regional Analysis

Asia Pacific Leads Global Growth: APAC holds the dominant position with a 41.6% market share and a value of USD 1.87 billion in 2024. A surging middle class, intensifying health awareness, and rising participation in fitness activities are fueling this lead. China, India, Japan, and South Korea are the primary growth engines, collectively representing both massive production capacity and rapidly expanding consumer demand.

North America and Europe Sustain Strong Momentum: North America benefits from a mature e-commerce infrastructure and an established culture of running events, enabling high-quality shoes to reach broad audiences efficiently. Europe, meanwhile, is propelled by strong sporting traditions and premiumization trends in the UK, Germany, and France. Both regions continue to innovate around performance and sustainability, setting global standards for product development and consumer marketing.

Recent Developments

- In 2024, Mytheresa and Richemont finalized an agreement for Mytheresa to acquire 100% of YNAP, establishing a global digital luxury platform curating top-tier brands for high-end consumers worldwide.

- In 2024, Deichmann expanded its portfolio by acquiring the Esprit shoe trademark for Europe and the U.S., following Esprit’s insolvency restructuring, while Theia Brands secured rights to Esprit’s apparel.

- In 2025, HOKA® introduced the Bondi 9, the latest addition to its renowned road-running shoe line, featuring enhanced plush cushioning and a smoother ride experience.

- In May 2024, Allbirds announced its first-quarter financial results, highlighting transformation strategy progress, with CEO Joe Vernachio crediting operational discipline for meeting key performance targets.

- In June 2023, ASICS launched the GEL-KAYANO™ 30, featuring new adaptive technology that enhances stability and comfort, reinforcing the brand’s commitment to biomechanics-driven innovation.

Conclusion

The global running shoes market stands at an inflection point. Driven by health-conscious consumers, occupational demand, and relentless technological advancement, the industry is on a clear trajectory from USD 4.5 billion in 2024 to USD 8.7 billion by 2034. A 6.8% CAGR underscores the durability of this growth across economic cycles and geographies. For manufacturers, investors, and retailers, the opportunity is both significant and strategically accessible — provided they align with the twin imperatives of performance innovation and sustainable value creation.