Quick Navigation

Overview

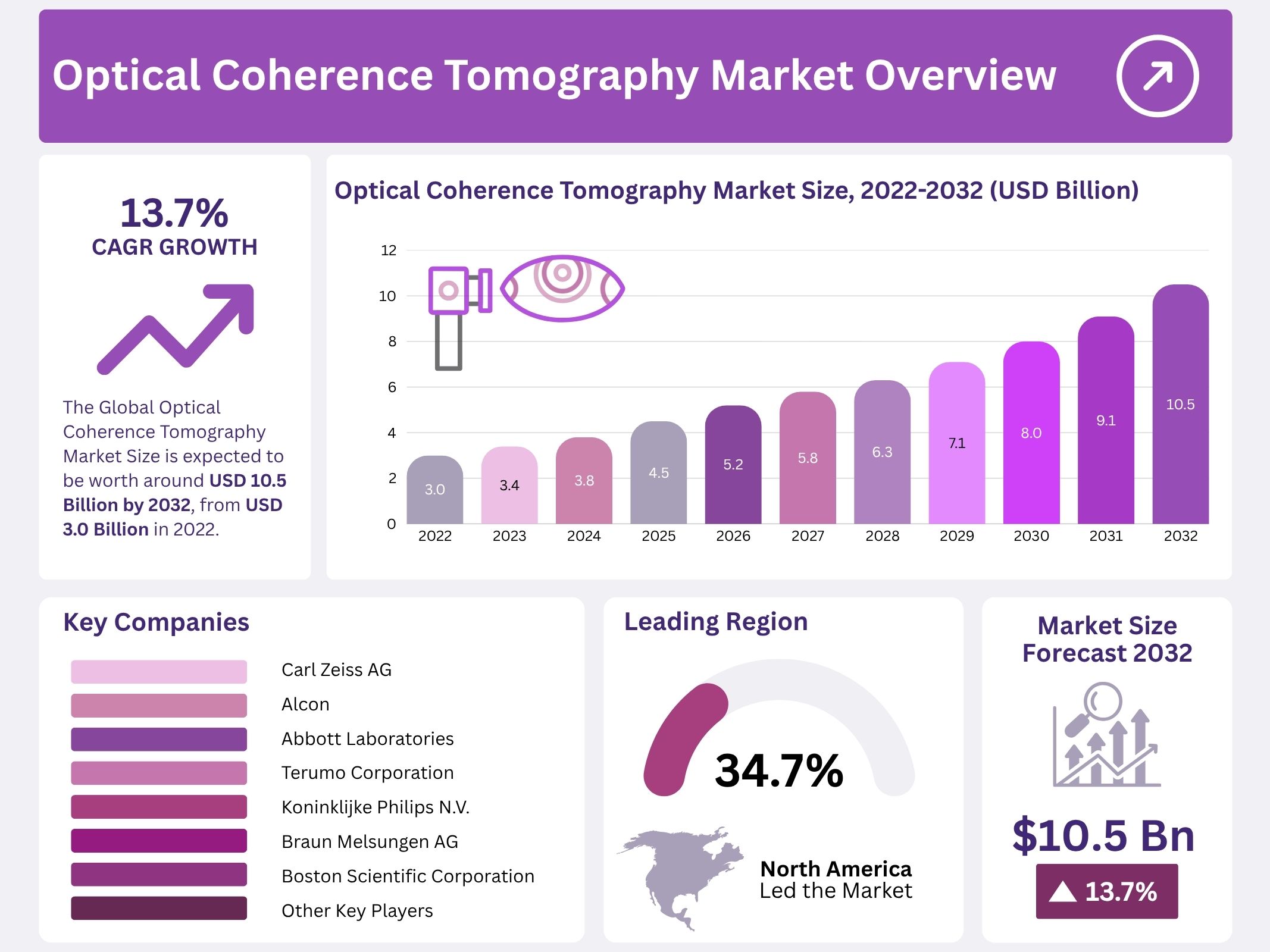

The global Optical Coherence Tomography (OCT) market was valued at USD 3.0 billion in 2022 and is projected to reach USD 10.5 billion by 2032, expanding at a CAGR of 13.7% between 2023 and 2032. Growth is being driven by the rising prevalence of ophthalmic disorders such as macular degeneration, diabetic retinopathy, and glaucoma. With more than 250 million people worldwide affected by vision impairment, the demand for reliable imaging solutions continues to increase. OCT is now widely adopted as a frontline diagnostic tool due to its precision and efficiency.

The demographic shift toward an aging population is also a major factor supporting market expansion. Older individuals are more vulnerable to ocular diseases that require frequent imaging and monitoring. This trend is creating sustained demand in hospitals, eye clinics, and specialty centers. At the same time, rising healthcare expenditure and government-backed awareness programs are improving access to diagnostic technologies, particularly in developing regions. Early detection initiatives are encouraging patient inflow and strengthening market growth prospects.

Technological innovation is reshaping the OCT landscape. Advanced modalities such as spectral-domain, swept-source, and functional OCT are enhancing imaging speed, resolution, and penetration depth. These improvements are enabling broader clinical use beyond ophthalmology, particularly in cardiology, dermatology, and oncology. The ability to provide high-resolution cross-sectional imaging across multiple applications is expected to significantly widen OCT’s adoption and commercial potential in the coming years.

Integration with artificial intelligence (AI) and digital platforms represents another key growth driver. AI-enabled OCT solutions are improving accuracy in disease detection, monitoring progression, and streamlining workflows. Such developments support teleophthalmology and remote diagnosis initiatives, making OCT an increasingly efficient and patient-friendly technology. Its non-invasive, real-time imaging capability further strengthens acceptance among clinicians and patients, giving it an edge over traditional imaging modalities.

Emerging economies in Asia-Pacific, Latin America, and the Middle East are witnessing rapid adoption of OCT technologies. Healthcare modernization, increased investment in diagnostic infrastructure, and supportive government initiatives for eye health are creating robust growth opportunities. With expanding applications, continuous technological advancements, and rising disease burden, OCT is expected to establish itself as a critical diagnostic and monitoring tool across multiple medical fields over the next decade.

Key Takeaways

- The global optical coherence tomography (OCT) market is projected to reach USD 10.5 billion by 2032, showcasing significant expansion opportunities across healthcare applications.

- In 2022, the OCT market size was valued at approximately USD 3 billion, indicating a strong foundation for future growth in advanced imaging technologies.

- The OCT market is anticipated to grow at a compound annual growth rate (CAGR) of 13.7% during the forecast period, 2023 to 2032.

- Handheld OCT devices captured the dominant share in 2022, reflecting increasing demand for portable and user-friendly solutions in clinical and diagnostic imaging.

- Ophthalmology remained the leading application segment in 2022, as OCT technology plays a vital role in diagnosing and managing ocular disorders globally.

- Spectral-domain OCT (SD-OCT) technology accounted for the largest share in 2022, driven by its accuracy, speed, and wide adoption in clinical diagnostics.

- North America contributed the highest revenue share of 34.67% in 2022, supported by advanced healthcare infrastructure, research activities, and rising patient adoption.

- The rising global population aged 65 years and above is boosting demand for OCT, as elderly individuals are more prone to vision-related diseases.

- Technological innovations such as ultra-high resolution OCT and swept-source OCT are enhancing diagnostic capabilities, making imaging faster, clearer, and clinically more effective.

- Increasing prevalence of chronic diseases, including diabetes and cardiovascular conditions, is driving higher demand for OCT imaging across multiple healthcare applications.

- Governments and healthcare providers worldwide are raising healthcare expenditure, which supports adoption of advanced medical imaging devices such as OCT systems.

- The OCT market is highly competitive and fragmented, with multiple companies competing across technology development, product innovation, and strategic global partnerships.

- Major players in the OCT market include Carl Zeiss AG, Alcon, and Abbott Laboratories, among others, leading technological advancements and market expansion.

Regional Analysis

The optical coherence tomography (OCT) market in North America is projected to expand steadily, with the market size expected to reach USD 1.05 billion by 2022. Growth in this region is supported by rising demand in the healthcare sector. The United States, being the largest market contributor, is driving adoption through rapid technological integration. Increasing investments in advanced diagnostic solutions, combined with favorable regulatory approvals, are shaping the overall momentum. This trajectory reflects both consumer demand and institutional readiness to adopt more advanced imaging systems.

The aging population across North America has been a major driver of OCT demand. With age-related eye diseases becoming more common, diagnostic imaging is gaining importance. Hospitals and specialty clinics are expanding their capabilities to meet growing patient needs. Government initiatives and rising healthcare expenditures are also influencing the trend. Moreover, diabetic retinopathy cases are on the rise, particularly in the United States, further boosting OCT adoption. The region’s strong focus on early detection and preventive care is enhancing market penetration.

Research and development investments have strengthened innovation in the OCT landscape. Leading companies are launching improved and multifunctional devices to address evolving clinical needs. An example is the unveiling of Topcon Canada Inc.’s 3D Maestro2, which combines OCT with ophthalmoscope functions. Such innovations are expanding the applications of OCT systems beyond ophthalmology. The introduction of hybrid systems is creating new opportunities for adoption in hospitals, clinics, and diagnostic centers. This trend is reinforcing the overall market growth trajectory in the region.

The United States continues to stand out as the key hub for OCT technology. Favorable healthcare infrastructure, higher healthcare spending, and willingness to adopt advanced solutions are key enablers. Wealthy demographics, including business professionals with strong purchasing power, also contribute to adoption rates. With hospital expansion plans underway, the need for advanced imaging systems is expected to rise further. Collectively, these drivers position North America as a critical region for sustained OCT market growth, ensuring the United States remains at the forefront of global demand.

Segmentation Analysis

The optical coherence tomography (OCT) market has been segmented based on product type into handheld, catheter-based, tabletop, and Doppler OCT devices. Among these, the handheld category dominated the market in 2022 and is projected to expand at the fastest pace from 2022 to 2032. Handheld OCT devices are gaining traction due to their portability and ease of use, enabling early detection of critical eye conditions such as macular degeneration, diabetic retinopathy, and glaucoma. This growing adoption is enhancing bedside monitoring and supporting broader clinical applications.

Handheld OCT devices leverage advanced technologies such as microelectromechanical systems (MEMS) and 3D imaging. These features allow clinicians to achieve more precise diagnostic outcomes. The integration of MEMS improves device miniaturization, while 3D imaging enables enhanced visualization of tissue structures. Such advancements support early diagnosis and patient management in ophthalmology. Moreover, the rising need for effective pharmacokinetic services in toxicological testing for IND-enabling studies is further contributing to the strong growth trajectory of handheld OCT devices.

Based on application, the OCT market has been categorized into cardiovascular, ophthalmology, dermatology, and oncology. Ophthalmology emerged as the leading segment in 2022 and is expected to maintain the highest growth rate until 2032. The prevalence of choroidal and retinal disorders is driving the adoption of OCT devices for diagnostic imaging in ophthalmology practices. Growing awareness regarding early disease detection and improved treatment outcomes has also reinforced the demand. As a result, ophthalmology is anticipated to account for the largest share of market revenue during the forecast period.

In terms of technology, the market is segmented into spectral-domain OCT (Sd-OCT) and swept-source OCT. The Sd-OCT segment accounted for approximately 65–67% of total revenue in 2022, making it the dominant technology. Sd-OCT offers high imaging speed and superior sensitivity compared to time-domain OCT, enabling efficient visualization of depth-resolved tissue structures. By analyzing the interference fringe spectrum, it delivers accurate biological imaging. These attributes have positioned Sd-OCT as a critical technology for clinical diagnostics and research applications, ensuring its continued prominence in the OCT market.

Key Players Analysis

The optical coherence tomography (OCT) market is driven by established medical technology leaders. Carl Zeiss AG, Alcon, and Abbott Laboratories are among the top players with extensive product portfolios in ophthalmology. These companies have invested significantly in advanced OCT systems for eye care and surgical procedures. Strong global distribution networks and brand reputation have strengthened their positions. Their innovations in imaging resolution, accuracy, and integration with digital platforms continue to enhance diagnostic precision and expand clinical applications across healthcare.

Heidelberg Engineering GmbH, Topcon Corporation, and Nidek Co. Ltd. are recognized for ophthalmic imaging expertise. These companies emphasize product differentiation through high-speed scanning and user-friendly platforms. Their offerings target glaucoma, macular degeneration, and diabetic retinopathy management. Strategic partnerships with hospitals and research institutions further reinforce their leadership. The increasing use of OCT in early disease detection supports strong demand. Continuous product upgrades and clinical validation strengthen their global competitiveness and ensure adoption across both developed and emerging markets.

Emerging players such as Novacam Technologies Inc., Michelson Diagnostics, and Imalux Corp. focus on specialized OCT applications beyond ophthalmology. These include cardiovascular imaging, dermatology, and cancer research. Their niche offerings aim to address growing clinical requirements in minimally invasive diagnostics. Collaborations with academic institutions and clinical researchers play a key role in enhancing adoption. Although smaller in scale compared to global leaders, these companies are carving a position by introducing innovative, compact, and cost-effective OCT devices that cater to broader diagnostic applications.

Other notable participants include Canon Medical Systems, Thorlabs Inc., Optovue Inc., and Excelitas Technologies Corp. These companies bring expertise in imaging technologies, optics, and light sources essential to OCT system performance. Their contributions support both research and clinical practice, enabling advancements in device precision. The competitive environment is further shaped by regional manufacturers such as Moptim Imaging Technique and Sonostar Technologies. Collectively, the presence of diversified players highlights a fragmented yet innovation-driven OCT market, where technology differentiation and clinical utility drive long-term growth.

Market Key Players

- Carl Zeiss AG

- Alcon

- Abbott Laboratories

- Terumo Corporation

- Koninklijke Philips N.V.

- Braun Melsungen AG

- Boston Scientific Corporation

- Topcon Corporation

- Nidek Co. Ltd

- Novacam Technologies Inc

- Agfa Healthcare

- Heidelberg Engineering Gmbh

- Imalux Corp

- Michelson Diagnostics

- Optopol Technology S.A.

- Thorlabs, Inc.

- Optovue Inc.

- Moptim Imaging Technique

- Sonostar Technologies Co. Limited

- Canon Medical Systems

- Excelitas Technologies Corp

- Other Key Players

Conclusion

The optical coherence tomography market is poised for strong and steady growth, supported by increasing cases of eye-related disorders, growing elderly populations, and technological innovations. OCT has become a vital diagnostic tool, offering precise, non-invasive, and real-time imaging across multiple medical fields. Its integration with advanced technologies such as artificial intelligence and digital platforms is enhancing accuracy and accessibility, making it a preferred choice in clinical settings. Expanding adoption in emerging regions, combined with rising healthcare investments and supportive government programs, further strengthens its prospects. With established leaders and emerging players driving innovation, OCT is expected to remain a critical component of modern diagnostics and patient care in the coming years.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Computed Tomography Market | Positron Emission Tomography Market | Single Photon Emission Computed Tomography Market | Cone Beam Computed Tomography Market