Quick Navigation

Overview

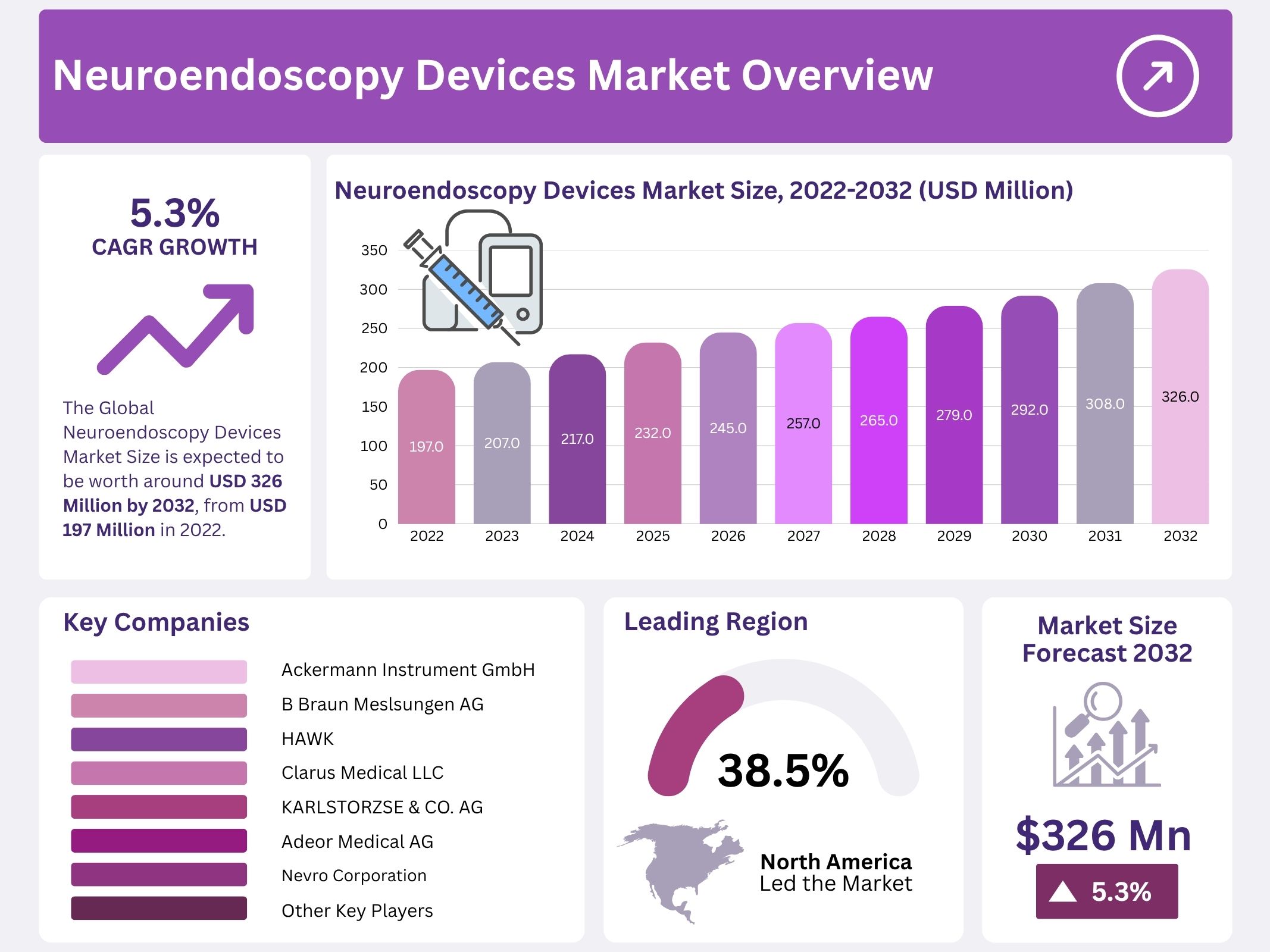

The Global Neuroendoscopy Devices Market is projected to reach US$ 326 million by 2033, rising from US$ 197 million in 2023. A compound annual growth rate of 5.3% is anticipated from 2024 to 2033. Market expansion is supported by rising adoption of minimally invasive neurosurgical techniques and the need to improve surgical precision and patient outcomes. The market landscape continues to mature as hospitals prioritize advanced devices for complex cranial procedures. Growing acceptance of minimally invasive interventions and structured neurosurgical training programs are reinforcing steady demand for neuroendoscopy systems across major medical centers worldwide.

Clinical preference for minimally invasive neurosurgery remains a significant demand driver. Neuroendoscopic procedures are associated with smaller incisions, reduced surgical trauma, and shorter hospital stays. As patient recovery times improve, a wider shift toward endoscopic interventions continues. Hospitals and neurospecialty centers are incorporating neuroendoscopy devices to expand treatment options for intracranial and ventricular disorders. Increasing procedure volumes for cyst removal, tumor excision, and intraventricular interventions are accelerating market adoption. Enhanced confidence among clinicians, supported by favourable outcomes and structured clinical guidelines, has reinforced utilization in high-volume neurosurgery units.

A rising burden of neurological diseases has contributed to procedural growth. Improved diagnostic imaging and greater clinical awareness have led to earlier detection of conditions such as hydrocephalus and brain tumors. The global geriatric population is also expanding, and neurological disorders are more prevalent in older patients. This demographic factor has increased the need for timely intervention and high-precision surgical equipment. Early diagnosis and surgeon preference for effective, minimally invasive solutions have further strengthened device adoption. Demand growth is particularly visible in regions with strong neurology and neurosurgery capabilities.

Technological innovation continues to improve neuroendoscopy performance. Advancements in imaging, optics, and navigation systems have enhanced surgical visibility and accuracy. The introduction of high-definition and 3D endoscopes, along with flexible and miniaturized instruments, has broadened clinical applications. Integration of robotics and augmented navigation is strengthening procedural capabilities and supporting complex neurosurgical operations with greater safety. Product improvements focused on visualization, precision, and instrument control are expected to create strong differentiation opportunities. Continuous development in imaging and optical technologies will remain central to competitive positioning.

Increasing healthcare spending and investments in neurosurgical infrastructure support market expansion. Developed economies benefit from favourable reimbursement policies and established neurosurgical units. Meanwhile, emerging markets are expanding neurosurgery programs and advanced operating suites. Training initiatives and partnerships with medical institutions are enhancing clinician expertise and accelerating technology adoption. Hospitals are prioritizing value-based and patient-safety-focused systems, strengthening demand for neuroendoscopy devices. Continued innovation, broader access to training, and rising adoption in developing regions are expected to maintain stable long-term growth in the global neuroendoscopy devices market.

Key Takeaways

- Market projections indicate the neuroendoscopy devices segment will grow at nearly 5.3% CAGR, rising from USD 197 million in 2022 to approximately USD 326 million by 2032.

- Clinical evaluations highlight that neuroendoscopy enables minimally invasive access to neurological regions, resulting in reduced tissue trauma, better visualization, and faster patient recovery.

- Industry reviews confirm rigid neuroendoscopes dominate product usage, supported by improved accuracy in neurosurgical procedures and consistently favorable surgical outcomes.

- Adoption studies report increasing utilization of flexible neuroendoscopes, attributed to their ability to access narrow and anatomically complex intracranial spaces effectively.

- Surgical trend analysis shows transnasal neuroendoscopy gaining momentum, particularly for brain tumor removal, due to reduced invasiveness and enhanced patient tolerance.

- Market insights reveal reusable neuroendoscopes leading demand, driven by long-term cost efficiency and suitability for high-volume healthcare environments.

- End-user assessments identify hospitals as primary adopters of neuroendoscopy solutions, supported by multispecialty capabilities and strong health reimbursement mechanisms.

- Growth drivers include escalating brain tumor prevalence, continuous advances in neuroendoscopic technology, and supportive government initiatives promoting minimally invasive neurosurgical solutions.

- Market constraints persist due to limited availability of specialized neuroendoscopy professionals and high procedural and equipment costs, hindering broad-scale adoption.

- Expansion opportunities are expected across emerging economies, supported by aging demographics, rising healthcare awareness, and increased demand for minimally invasive neurosurgical procedures.

Regional Analysis

North America is projected to lead the neuroendoscopy market, holding an estimated 38.5% revenue share during the forecast period. The expansion of healthcare technologies in the region has supported market dominance. Strong presence of major players such as B. Braun and Karl Storz has also strengthened regional growth. Rising cases of pediatric brain tumors will further support market expansion. Increased investment in neurosurgery and advanced medical systems is expected to sustain North America’s leadership and generate significant market value throughout the forecast period.

Europe is anticipated to secure a considerable market share, supported by a strong presence of skilled neurosurgeons. Countries such as the UK, Germany, and France are adopting advanced neuroendoscopy systems at a steady rate. Increasing prevalence of neurological disorders and supportive government healthcare infrastructure further drive regional demand. Continuous focus on minimally invasive neurosurgical procedures enhances adoption. As a result, Europe is expected to see positive growth and remain a major contributor to the global neuroendoscopy market landscape.

Asia Pacific is expected to record the fastest growth rate, assisted by rising healthcare expenditure and expanding access to advanced medical facilities. Increasing cases of brain tumors across India and China contribute significantly to device demand. Large aging populations in these countries increase incidences of glioblastoma, pushing market growth. Untapped market opportunities and improving hospital infrastructure will foster regional expansion. Government initiatives supporting medical modernization are expected to accelerate adoption of neuroendoscopy systems, strengthening Asia Pacific’s position in the global market.

The Middle East and Africa region is projected to witness slower growth due to limited awareness regarding minimally invasive neurosurgical techniques. Lower access to advanced healthcare technologies also influences adoption rates. However, gradual improvements in medical infrastructure and healthcare spending in select countries may support long-term progress. Growing focus on neurological care improvement could increase demand in future years. Despite current constraints, steady enhancements in healthcare capabilities are expected to gradually support market expansion throughout the region.

Segmentation Analysis

The market is segmented by product type into rigid neuro endoscopes and flexible neuro endoscopes. The rigid segment is projected to hold a major share, driven by increased neuro endoscopy procedures and advanced optical rod lenses enabling high-resolution visualization. These devices enhance access to intricate brain areas and remain widely used in surgical applications. Vendors are improving rigid systems to enhance outcomes in minimally invasive surgeries. The introduction of advanced rigid and semi-rigid systems in hospitals is boosting adoption and market expansion globally during the forecast period.

The market based on surgery type includes intraventricular, transnasal, and transcranial procedures. Intraventricular endoscopy is a key application for brain tumors. The transnasal segment is expected to dominate during the forecast period, supported by its use in CSF diversion, biopsy, and hydrocephalus treatment. Transcranial endoscopy is applied for larger tumors with suprasellar extension via supraorbital and trans-glabellar approaches. Increasing adoption of transnasal methods is driven by access to deep brain regions with minimal surgical trauma and rising brain tumor cases.

The neuroendoscopy market is also segmented by usability into reusable and disposable neuro endoscopes. Reusable devices currently dominate due to cost-effectiveness and suitability for repeated clinical use. Their high initial cost is offset by long-term affordability across multiple procedures. Disposable endoscopes are gaining traction due to lower cost per unit and reduced infection risk. These devices are preferred in developing countries and resource-limited settings. Growth in disposable models is encouraged by rising infection-prevention focus and expanding adoption in emerging healthcare markets.

By end-user, the market is divided into hospitals, ambulatory surgical centers, diagnostic centers, and others. Hospitals account for the largest revenue share due to a higher patient volume and advanced surgical infrastructure. Growth in multispecialty hospitals and favorable reimbursement policies supports adoption. Increasing healthcare investments in developing countries, including India and Mexico, further strengthen growth prospects. According to NCBI, approximately 50,000 neurosurgeons are active worldwide. The rising neurosurgeon workforce and growing demand for neurosurgical procedures reinforce hospitals as primary revenue contributors.

Key Market Segments

Based on Type

- Rigid

- Flexible

Based on Surgery

- Intraventricular

- Transnasal

- Transcranial

Based on Usability

- Reusable

- Disposable

Based on End-User

- Hospitals

- Diagnostic Centre’s

- Ambulatory Surgical Centers

- Others

Key Players Analysis

The neuro endoscopy devices market is led by established players such as Aesculap, B. Braun, and Karl Storz. These companies hold a primary share, particularly in the United States. Market share analysis shows that these leaders generate significant revenue compared to other traders. Their strong distribution networks and advanced product portfolios support this dominance. The competitive landscape is defined by product innovation, consistent technology upgrades, and wide clinical adoption. The presence of strong regulatory approvals and high product reliability further enhances their competitive positioning in the global market.

Other major participants include Ackerman Instruments GmbH, Clarus Medical LLC, Adoer Medical AG, Olympus Corporation, Machida Endoscope, Tonglu WANHE Medical Instrument, and Schindler Endoskopie Technologies GmbH. The industry remains partially consolidated but has seen new entrants in recent years. These emerging companies focus on cost-efficient and innovative solutions. Market competition has intensified due to expanding product offerings and global distribution improvements. Technology partnerships, product expansions, and strategic collaborations are observed as common growth strategies in the industry.

Market growth is driven by rising demand for minimally invasive procedures and an increasing geriatric population worldwide. The adoption rate is influenced by advantages such as reduced surgical risks and faster recovery. However, high procedure costs and limited affordability in developing regions act as barriers. Healthcare institutions often opt for conventional treatments due to cost constraints, slowing adoption in certain markets. Despite these challenges, technological advancements and growing patient preference for minimally invasive techniques support strong market potential and sustained long-term expansion.

Market Key Players

- Ackermann Instrument GmbH

- B Braun Meslsungen AG

- HAWK

- Clarus Medical LLC

- KARLSTORZSE & CO. AG

- Adeor Medical AG

- Nevro Corporation

- Tonglu WANHE Medical Instrument

- Machida Endoscope

- Schindler endoskopie Technology GmbH

- Olympus Corporation

- Boston Scientific Corporation

- Aesculap, Inc.

- KARL STORZ AE & CO

- Medical Instruments Co, Ltd.

- Evonos

- Other Key Players

Conclusion

The global market for neuroendoscopy devices is expected to grow steadily over the next decade, supported by rising use of minimally invasive brain surgeries and ongoing improvements in imaging and surgical tools. Growth is helped by greater awareness of neurological diseases, increasing access to skilled neurosurgeons, and continuous investment in hospital infrastructure. Demand is strong in developed regions, and emerging healthcare systems are also adopting these technologies at a faster pace. Although high costs and shortage of trained specialists remain challenges, ongoing innovation and wider training programs are expected to support adoption. The market outlook remains positive as hospitals focus on safer, faster, and more precise neurosurgical care.