Quick Navigation

Overview

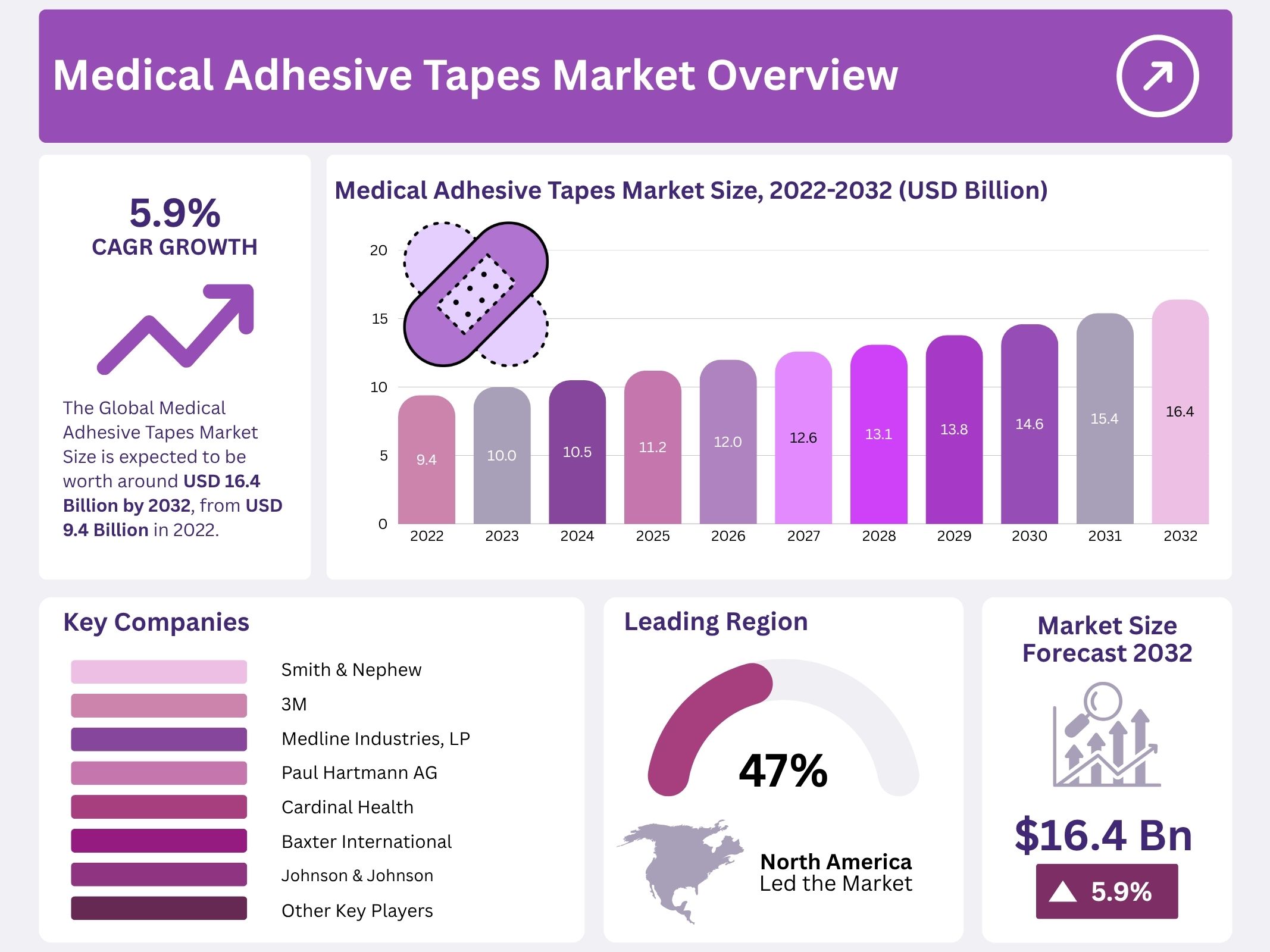

The Global Medical Adhesive Tapes Market is projected to reach USD 16.4 billion by 2032, increasing from USD 9.4 billion in 2022. A CAGR of 5.9% has been estimated for the forecast period. Market expansion is supported by increasing healthcare needs, rising patient admissions, and advanced wound management practices. The growth of minimally invasive and traditional surgeries, supported by improved healthcare access worldwide, continues to elevate product demand across hospitals and outpatient facilities.

The increasing global surgical volume remains a primary growth driver. A steady rise in chronic illnesses and trauma cases has resulted in higher counts of wound closures and device securement procedures. Growing post-operative care needs contribute to frequent use of adhesive tapes for bandages, tubing, and device stabilization. Enhanced recovery protocols in modern clinical systems and the preference for reliable fixation materials strengthen adoption in acute and chronic care settings.

Chronic wound prevalence has risen, fueled by diabetes, vascular conditions, and pressure injuries in long-term care environments. Advanced tapes designed for moisture balance, breathability, and strong adhesion support the management of ulcers and long-duration dressings. This trend aligns with greater clinical emphasis on early wound intervention and improved skin protection. Adoption is expected to rise further as demand for high-performance wound dressings increases in developed and emerging regions.

Technological advancements have accelerated product development toward improved comfort and safety. Hypoallergenic, antimicrobial, silicone-based, and breathable materials have been introduced for sensitive and fragile skin. Product innovation focuses on long-wear performance, reduced irritation, and enhanced compatibility with diagnostic and wearable devices. In parallel, home healthcare growth drives widespread use in self-care wound management, catheter securement, and remote-monitoring equipment, supported by rising geriatric populations and extended care needs outside clinical facilities.

Increasing wearable medical device adoption has reinforced demand for skin-friendly tapes used to secure sensors and continuous-monitoring systems. Emphasis on infection prevention in hospitals and outpatient centers further promotes the use of secure fixation solutions that limit contamination risks. Sustainability has also emerged as a key priority, leading to development of eco-friendly, latex-free, biodegradable, and non-toxic adhesive materials. These innovations align with environmental standards and patient-safety guidelines, supporting long-term market expansion driven by safer and greener adhesive technologies.

Key Takeaways

- The market is projected to expand at a 5.9% CAGR, increasing from USD 9.4 billion in 2022 to reach approximately USD 16.4 billion by 2032.

- Acrylic-based medical tapes currently dominate with around 41% share, while silicone tape usage is forecasted to advance steadily at a 5.9% CAGR.

- Paper remains the preferred tape material with about 42% market share, while plastic and fabric-based tapes continue gaining traction due to enhanced performance properties.

- Double-coated medical tapes account for roughly 57% share, whereas single-coated variants are expected to grow at a 5.2% CAGR driven by clinical utility.

- Surgical applications represent approximately 38% of total demand, while wound dressing requirements are anticipated to increase at a 5.4% CAGR due to rising patient needs.

- Hospitals constitute around 44% of end-use adoption, with ambulatory surgical centers projected to expand at a notable 5.3% CAGR due to outpatient care growth.

- North America leads the global market with nearly 47% share, whereas the Asia Pacific region is forecasted to grow at a 5.9% CAGR.

- Market expansion is supported by increasing chronic illness prevalence, aging demographics, advanced product innovations, and a rising volume of surgical procedures worldwide.

Regional Analysis

Regional analysis shows a strong concentration of demand in North America. The region currently holds a 47% share of the global medical adhesive tapes market. This position reflects advanced healthcare systems and consistent investment in medical facilities. Rising consumer awareness of wound care also supports growth. The region benefits from early adoption of medical technologies. Strong reimbursement frameworks further enhance product uptake. These factors establish North America as the key hub for market expansion. Its market strength is expected to remain stable through the forecast period.

North America’s dominance can be attributed to a mature healthcare infrastructure. Hospitals and clinics demonstrate high adoption of medical adhesive tapes. Increasing surgical procedures are expected to drive steady demand. Aging population trends further support product use. Chronic illness cases remain high, contributing to wound care needs. Strong presence of established manufacturers enhances market access. Public awareness of health and hygiene remains elevated. As a result, consistent market growth is expected. Regional demand continues to strengthen, backed by continuous medical advancements.

Asia Pacific is projected to register significant growth during the forecast period. The region is expected to achieve a CAGR of 5.9%. Growing population and expanding healthcare access are key drivers. Rising diabetes prevalence plays a major role in increased wound care needs. India reported 74.2 million adults with diabetes in 2021. This number is expected to reach 124.8 million by 2045. Economic development across Asian countries supports healthcare spending. Urbanization and lifestyle changes continue to influence diabetes incidence across the region.

Diabetes-driven wound issues contribute to rising demand for medical adhesive tapes in Asia Pacific. The Philippines recorded 3,993,300 diabetes cases in 2019, as noted by the International Diabetes Federation. Individuals with diabetes face a higher risk of foot ulcers. These ulcers require consistent wound dressing and secure adhesive support. Growing awareness of diabetic wound management further stimulates product usage. Governments are increasing focus on chronic disease control. As more patients seek treatment, demand for wound care materials rises steadily. This trend supports continued regional market expansion.

Overall, regional market growth is strongly connected to healthcare improvement and disease trends. Higher surgical rates in North America continue to support product adoption. Asia Pacific, driven by rising diabetes cases, presents strong future potential. Medical adhesive tapes remain essential for effective wound management and postoperative care. Healthcare development programs enhance product accessibility in developing countries. Increasing public awareness promotes higher usage in both regions. Continued focus on chronic disease treatment strengthens long-term market stability. Global demand is projected to advance through enhanced medical practices and growing patient volumes.

Segmentation Analysis

Acrylic, silicone, and rubber are key adhesive types in the medical adhesive tapes market. Acrylic dominates with a 41% share. Its strong tack, low skin sensitivity, and clean removal drive adoption. High heat and humidity resistance also support demand. Silicone tapes are forecast to grow fastest at 5.9% CAGR from 2023 to 2032. Their ability to be repositioned, reduce scarring, and prevent trauma supports higher usage. Rubber remains relevant for cost-driven applications, but advanced tapes lead demand across clinical environments.

Based on material, paper, fabric, plastic, and other substrates are used. Paper tapes hold a 42% market share and lead due to cost-effectiveness and strong patient compliance. Research published in NCBI shows paper tapes result in lower inflammation and infection rates than sutures or staples. Plastic tapes rank second with waterproof features and long-lasting adhesion. Fabric materials such as cotton, silk, and polyester are rising in demand, driven by wearable medical devices and long-term monitoring needs.

The adhesion segment includes single-coated and double-coated medical tapes. Double-coated tapes dominate with a 57% share due to superior strength, dimensional stability, and customizable backing. Their breathable, hypoallergenic, and repositionable nature boosts adoption in medical conversion processes. Single-coated tapes are projected to grow at a 5.2% CAGR. These tapes use foam, nonwoven, film, or metal substrates with one adhesive side. They are widely used in skin-contact devices and benefit from a silicone release liner for sterile handling in clinical settings.

Surgery, wound dressing, IV lines, and other uses define the application landscape. Surgical applications hold a 38% market share. Rising procedure volumes and increased use in cosmetic surgery support leadership. Global major surgeries reach approximately 310 million annually. Wound dressing is expected to record a 5.4% CAGR through 2032, driven by growing chronic wounds. Conditions such as diabetic foot ulcers and venous leg ulcers require frequent tape usage. Diabetes prevalence, including 34.2 million U.S. patients, fuels long-term demand.

Hospitals lead end-use demand with a 44% market share. High surgical volume, expanding hospital networks, and accident-related injuries support usage. Growing traffic accidents in markets like the Philippines reinforce consumption. Ambulatory surgery centers are set to expand at a 5.3% CAGR due to higher chronic disease rates and increased investment. Government programs and patient preference for cost-efficient and convenient care models also support ASC growth. These trends indicate strong future demand for reliable, skin-friendly medical adhesive tapes across care settings.

Market Segmentation

Based on Type

- Acrylic

- Silicone

- Rubber

Based on Material

- Paper Tapes

- Fabric Tapes

- Plastic Tapes

- Other Tapes

Based on Adhesion

- Single Coated

- Double Coated

Based on Application

- Surgery

- Wound Dressing

- IV Lines

- Other Application

Based on End-User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Other End-Users

Key Players Analysis

The medical adhesive tapes market remains fragmented, and competition has been observed as intense due to the presence of many established manufacturers. Market participants are focusing on innovation and performance-driven adhesive technologies, especially in long-wear and sensitive-skin applications. Rising patient demand for durable and skin-friendly tapes is encouraging companies to enhance R&D capabilities. Strategic moves like new product development are being adopted to strengthen brand preference, and the launch of extended-wear solutions is viewed as an important step toward gaining clinical acceptance and commercial advantage.

Industry expansion efforts are supported by multinational healthcare companies with wide product portfolios and distribution capabilities. Firms are expanding manufacturing footprints to improve supply reliability and meet global healthcare quality benchmarks. Mergers and acquisitions are being considered to increase product accessibility and accelerate technological integration. This strategy allows market leaders to leverage shared resources, reduce time to market, and improve clinical outreach while addressing growing needs in hospitals, surgical centers, and home-care settings across regions.

Key companies are prioritizing geographic expansion to penetrate emerging markets with rising healthcare spending. Strong sales channels, localized logistics, and targeted customer training programs are being utilized to increase adoption. Increased competition has encouraged investment in dermatologically tested adhesive systems and improved latex-free materials. Attractive growth opportunities are expected in advanced wound-care environments, promoting more partnerships with healthcare providers for clinical validation and procurement agreements. These efforts support broader adoption in both developed and developing economies and reinforce competitive positioning.

Major players in the medical adhesive tapes market include 3M, Smith & Nephew, Medline Industries, Paul Hartmann AG, Cardinal Health, Baxter International, Johnson & Johnson, Nitto Denko Corporation, Nichiban, and Lohmann GmbH & Co. KG. Their strategies center on high-performance product lines, patient comfort improvements, and enhanced wear-time capabilities. With innovations like 3M’s extended-wear tape lasting up to 21 days, the market is expected to witness continued product launches, driving quality standards and competitive differentiation among leading global manufacturers.

Market Key Players

- Smith & Nephew

- 3M

- Medline Industries, LP

- Paul Hartmann AG

- Cardinal Health

- Baxter International

- Johnson & Johnson

- Nitto Denko Corporation

- Nichiban

- Lohmann GmbH & Co. KG

- Other Key companies

Conclusion

The medical adhesive tapes market is expected to grow steadily due to rising surgical procedures, chronic wound cases, and expanding home healthcare services. Demand is supported by improved medical access, higher patient admissions, and greater focus on safe wound care. Innovation in gentle, breathable, and long-wear materials continues to shape product development. Growing use of wearable medical devices and remote monitoring also increases adoption. Sustainable, latex-free, and skin-friendly tapes are gaining attention as healthcare providers prioritize safety and comfort. With strong investments in product quality and wider distribution networks, the market outlook remains positive across hospitals, clinics, and home-care environments.