Quick Navigation

Overview

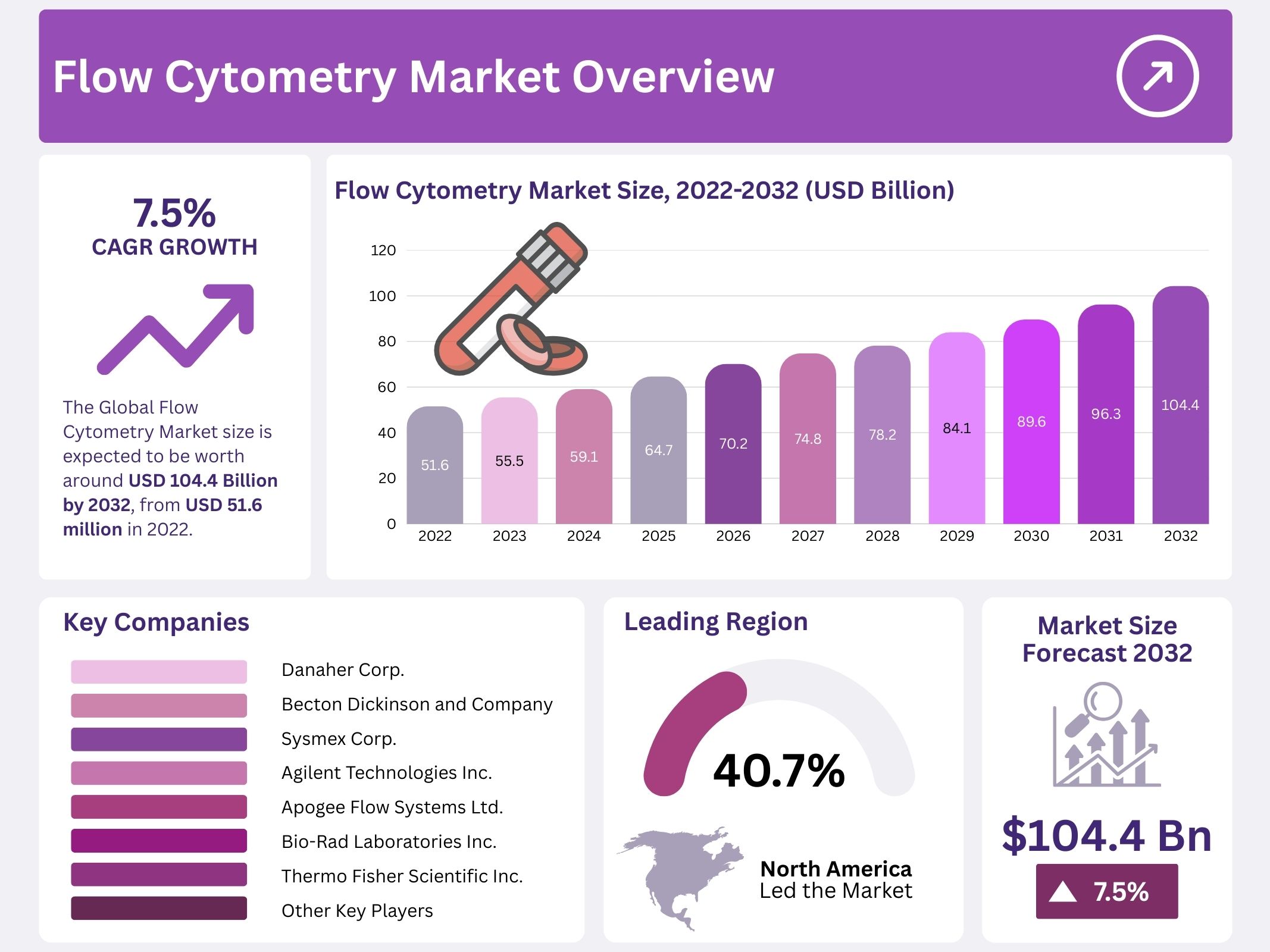

The Global Flow Cytometry Market is projected to grow from USD 51.6 billion in 2022 to USD 104.4 billion by 2032, at a CAGR of 7.5%. This growth is primarily driven by the rising prevalence of chronic and infectious diseases, including cancer and HIV. Flow cytometry is widely used in diagnostics, disease monitoring, and immunophenotyping, making it vital for early detection and improved treatment outcomes. Its role in personalized healthcare has become increasingly significant in the past decade.

The clinical utility of flow cytometry has expanded beyond traditional immunology and hematology. It is now central in detecting minimal residual disease (MRD), evaluating organ transplantation outcomes, and supporting stem cell and prenatal diagnostics. With increasing clinical applications, the demand for advanced solutions in hospitals and diagnostic centers is accelerating. Broader integration into clinical workflows has positioned flow cytometry as a cornerstone of modern diagnostics, with adoption rates expected to rise further across developed and emerging healthcare systems.

Technological advancements are further strengthening market growth. Developments such as spectral flow cytometry enable deeper analysis of cell populations. The integration of AI and machine learning into data interpretation improves accuracy and reduces human error. Miniaturized and high-throughput instruments are making processes faster and more efficient. Collectively, these innovations are increasing accessibility, improving clinical decision-making, and expanding the scope of use across research and clinical domains.

Research Growth, Emerging Markets, and Future Opportunities

The growing biopharmaceutical and biotechnology industries are contributing significantly to demand for flow cytometry. This technology supports drug discovery, immunotherapy development, and biomarker research. It is also crucial in quality control for biomanufacturing. As pharmaceutical pipelines continue to shift toward advanced therapies, flow cytometry remains one of the most relied-upon tools in laboratory and industrial applications. The sector benefits from sustained investments in personalized medicine and immuno-oncology.

Academic and research institutions represent another strong growth segment. Governments and funding bodies are prioritizing life sciences research, particularly in immunology, stem cell biology, and cancer. Flow cytometry has become a core technology in these domains, ensuring high adoption in universities, research labs, and global consortia. These developments are expanding the knowledge base and accelerating the translation of research into clinical and commercial applications.

New opportunities are also emerging in point-of-care and portable systems. Compact devices are increasingly adopted in low-resource settings for infectious disease monitoring. Favorable reimbursement policies and faster regulatory approvals are reducing adoption barriers, particularly in diagnostics. Furthermore, rising healthcare investments in Asia-Pacific, Latin America, and the Middle East are boosting uptake of advanced diagnostic tools. These regions are expected to see rapid growth as awareness and infrastructure improve, providing significant opportunities for market expansion over the forecast period.

Key Takeaways

- The global flow cytometry market is projected to attain USD 104.4 billion by 2032, reflecting strong long-term growth potential worldwide.

- Market expansion is estimated at a compound annual growth rate of 7.5%, highlighting steady demand for flow cytometry technologies and applications.

- In 2022, the instruments segment accounted for 37% of total market share, demonstrating its dominance as the leading product category.

- North America emerged as the largest regional market in 2022, capturing 40.7% of overall revenues due to advanced healthcare infrastructure.

- Europe secured 32% of the market’s revenue share in 2022, driven by rising adoption of advanced diagnostic and research technologies.

- Asia-Pacific is forecasted to exhibit the highest compound annual growth rate, supported by improving healthcare access and rising investment in research.

- A growing global geriatric population is significantly fueling demand for flow cytometry, owing to higher prevalence of age-related diseases.

- Continuous technological advancements in chronic disease treatment are providing a major boost to flow cytometry adoption across healthcare systems worldwide.

- The cost-effectiveness of flow cytometry devices is increasing their adoption across research and clinical settings, strengthening overall market demand.

- Growing involvement in stem cell research and expansion of clinical trials are further contributing to market growth for flow cytometry technologies.

- Hospitals and clinics have emerged as the dominant end-user segment, reflecting strong clinical adoption of flow cytometry for diagnostics and treatment.

- The instruments category remains the most dominant product type within the flow cytometry market, highlighting its central role in research and diagnostics.

Regional Analysis

In 2022, North America held a leading share in the flow cytometry market, accounting for more than 40.7% with a market value of US$ 38.5 billion. The United States contributed significantly to this dominance due to widespread adoption of advanced flow cytometry solutions. A strong healthcare infrastructure, high levels of healthcare spending, and technological advancements reinforced the region’s position. Furthermore, supportive government initiatives and investment in life sciences research strengthened the region’s ability to maintain its competitive advantage in the global market.

The United States has become the core driver of growth within North America. This is attributed to continuous research and development activities, focusing on innovative product launches and advanced cytometry applications. High prevalence of chronic conditions, particularly cancer, has further stimulated demand for improved diagnostic and therapeutic tools. The presence of major pharmaceutical and biotechnology companies, together with active participation of academic and research institutions, provides an ecosystem that supports market innovation, collaborations, and long-term market growth.

The Asia-Pacific region is projected to demonstrate the fastest growth in the forecast period. This expansion is driven by increasing outsourcing of research projects to contract research organizations. Rising cases of chronic diseases, such as HIV and cancer, are fueling the need for advanced healthcare technologies. Countries like China and India are making substantial investments in healthcare infrastructure, enhancing accessibility to modern diagnostic tools. The region’s growing focus on precision medicine and clinical trials is anticipated to accelerate the adoption of flow cytometry solutions across diverse applications.

Segmentation Analysis

The flow cytometry market is segmented into instruments, software and services, kits, and reagents. Instruments remain the most profitable segment, while reagents and consumables are poised to dominate due to their affordability, accuracy, and role in research and clinical trials. Their adoption is rising as they provide efficient and reliable outcomes for diagnostic and therapeutic purposes. Compact, high-throughput cytometers are also expected to gain traction, offering user-friendly and cost-effective solutions. These developments are set to expand market opportunities and enhance adoption across diverse applications.

Technological segmentation of the market is divided into cell-based and bead-based flow cytometry. Cell-based cytometry is expected to register the highest growth, supported by its application in early-stage research and enhanced technological advances in reagents, labeling, and software. Bead-based cytometry is also gaining momentum, as it allows the measurement of multiple soluble proteins simultaneously. Its capability in multiplex assays makes it highly suitable for immune-related disorder studies. Together, these technological advancements are broadening the scope of flow cytometry in research and clinical diagnostics.

In terms of end users, hospitals and clinics represent the leading segment, owing to their extensive use of flow cytometry in diagnostics and disease management. Increasing reliance on this technology in oncology, immunology, and infectious disease testing supports its growth. Clinical laboratories are projected to expand rapidly, driven by demand for accurate and timely diagnostics. Academic and research institutes, along with pharmaceutical and biotechnology companies, also play a vital role in advancing the adoption of flow cytometry. This diversified usage highlights the critical importance of the technology across healthcare and research ecosystems.

Key Players Analysis

Prominent companies in the flow cytometry market, including Sysmex Corporation, Luminex Corporation, Sartorius AG, Danaher Corporation, and Becton Dickinson and Company, are actively strengthening their global presence. Alongside these, players such as BioLegend, Inc., bioMérieux SA, Thermo Fisher Scientific Inc., Bio-Rad Laboratories Inc., and Enzo Life Sciences, Inc. are intensifying research and development. These companies are expanding their facilities and investing in innovation. Such initiatives are aimed at enhancing product offerings and capturing a larger market share in an evolving landscape.

Strategic investments, mergers, and acquisitions are being pursued to diversify product portfolios and improve technological capabilities. For instance, BD Life Sciences has reinforced its regional influence by establishing a flow cytometry center of excellence in India. This initiative, developed in collaboration with Vellore Christian Clinical School, highlights the commitment to regional market expansion. Such collaborations strengthen both research outcomes and commercial adoption, ensuring that these companies remain competitive in meeting global healthcare and diagnostic demands.

The flow cytometry market is characterized by intense competition, with both established international brands and emerging regional players. Strong distribution networks allow leading companies to maintain dominance. However, local firms are challenging market leaders by offering cost-effective solutions. To retain leadership, companies are focusing on launching innovative products and building partnerships. This environment fosters continuous advancements, driving the development of efficient and high-quality cytometry technologies. As a result, the market remains dynamic, with sustained opportunities for growth and expansion across regions.

Market Key Players

- Danaher Corp.

- Becton Dickinson and Company (BD)

- Sysmex Corp.

- Agilent Technologies Inc.

- Apogee Flow Systems Ltd.

- Bio-Rad Laboratories Inc.

- Thermo Fisher Scientific Inc.

- Stratedigm Inc.

- DiaSorin SPA

- Other Key Player

Conclusion

The flow cytometry market is set for strong and steady growth, supported by its expanding role in clinical and research applications. Its use in disease detection, personalized medicine, and advanced therapies is making it a core technology in healthcare systems worldwide. The adoption of innovative solutions, including AI-driven tools and portable devices, is enhancing efficiency and accessibility across both developed and emerging markets. With rising healthcare investments, a growing elderly population, and increasing focus on precision medicine, the demand for flow cytometry is expected to remain robust. Continued innovation and strong competition among key players will further strengthen its position in diagnostics and life sciences.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]