Quick Navigation

Overview

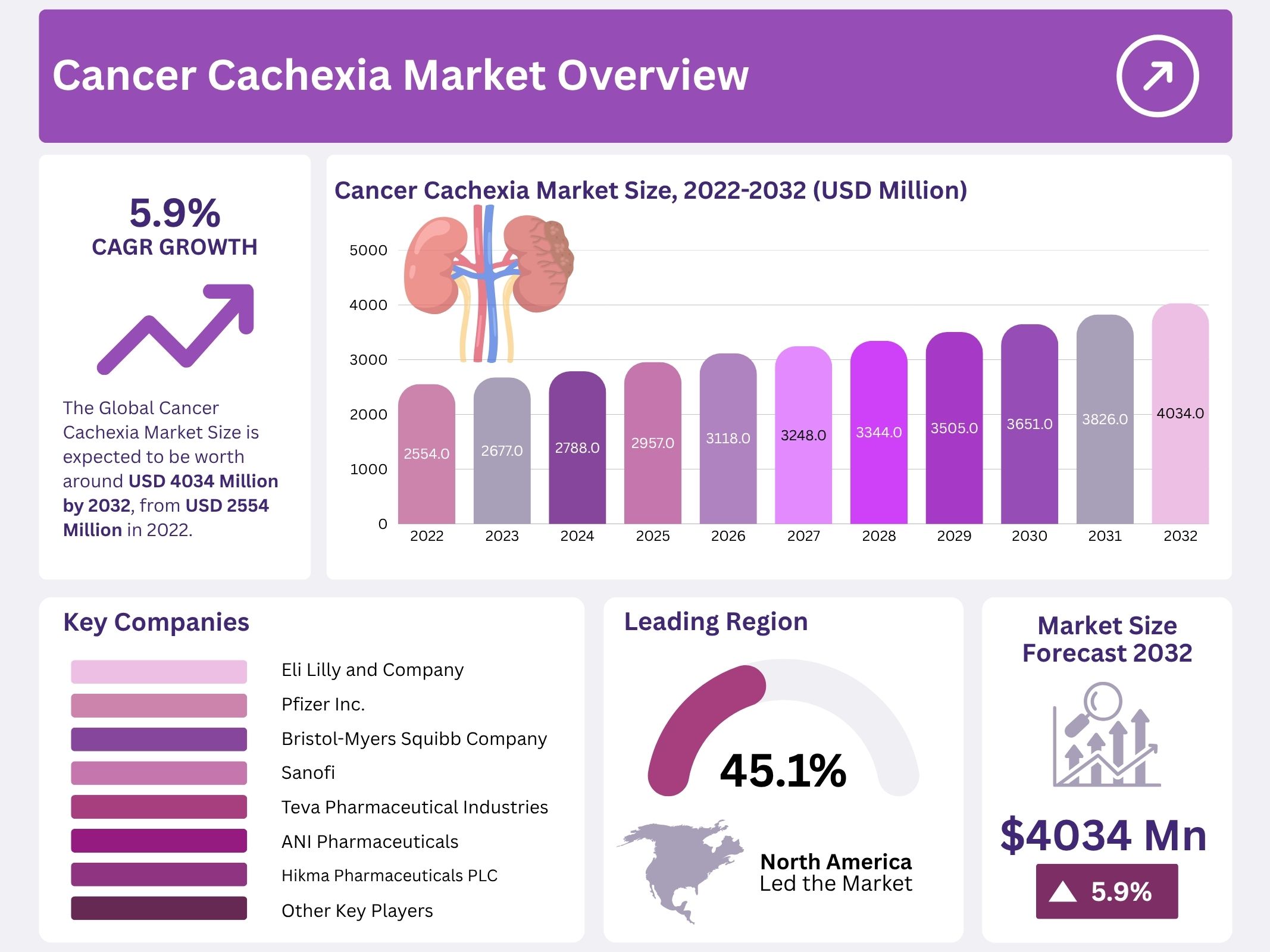

The Global Cancer Cachexia Market is projected to reach USD 4,034 million by 2032, rising from USD 2,554 million in 2022. The market is anticipated to grow at a CAGR of 4.8% during 2022–2032. Growth is supported by rising cancer incidence, increasing clinical focus on supportive oncology care, and improved awareness of cancer-related metabolic disorders. Cancer cachexia is defined as a complex metabolic syndrome marked by unintended weight loss, muscle wasting, and appetite reduction. Its recognition as a distinct clinical condition has strengthened medical and commercial interest, leading to greater emphasis on supportive care as a critical part of cancer treatment.

The rising global cancer burden has been a major driver of market expansion. Cancer cachexia affects an estimated 50% to 80% of patients with advanced malignancies. It contributes to nearly 20% of cancer-related deaths, underscoring the severity of the condition. As cancer prevalence rises, especially in aging populations, demand for cachexia intervention is expected to increase. The growing volume of oncology patients has created significant unmet clinical needs. This trend has supported broader adoption of nutritional and metabolic therapies aimed at improving treatment tolerance, functional outcomes, and patient survival.

Advancements in therapeutic research have played a vital role in market development. Pharmaceutical companies and biotechnology firms are investing in new approaches that target inflammation, cytokine pathways, anabolic metabolism, and appetite regulation. Innovations such as ghrelin receptor agonists and anti-inflammatory agents reflect expanding scientific understanding of cachexia pathophysiology. Public and private research funding has strengthened clinical pipelines, while academic-industry partnerships have accelerated development activities. These efforts are expected to generate novel treatments that offer more effective symptom management and improved patient quality of life.

Regulatory support has further encouraged innovation. Cancer cachexia has gained recognition as a separate therapeutic area across major markets. Orphan drug designations and expedited approval pathways have incentivized development by offering benefits such as market exclusivity and regulatory assistance. Government agencies and regulatory bodies have also emphasized the need for structured clinical guidelines, enabling better integration of cachexia care into oncology practice. These initiatives have supported a favorable market environment and encouraged industry participation.

Improved diagnostics and clinical awareness continue to advance treatment adoption. Standardized assessment tools, nutritional screening programs, and body composition analysis methods have promoted earlier diagnosis and intervention. Oncology professionals are increasingly trained to identify cachexia in its early stages, improving care outcomes. Rising awareness among patients and caregivers has also contributed to higher treatment uptake. Combined with demographic trends such as rapid population aging, these factors are expected to sustain long-term market growth and reinforce the importance of comprehensive supportive oncology care.

Key Takeaways

- The cancer cachexia market was projected to expand at nearly 4.8% CAGR, reaching approximately USD 4,034 million by 2032 from USD 2,554 million in 2022.

- Progesterone therapy was identified as the leading treatment segment, achieving a 5.4% CAGR and being regarded as the safest therapeutic option in 2022.

- Hospital pharmacies held the dominant distribution channel share in 2022, attributed to higher patient admissions and increased cancer-related hospitalization needs.

- Weight-loss stabilizing drugs demonstrated essential utility in managing cancer cachexia, recording a 4.2% CAGR due to their role in improving patient weight and life quality.

- Global cancer incidence continued rising, supported by WHO reporting 18.1 million new cancer cases in 2018, significantly driving cachexia treatment demand.

- Increasing disease burden strengthened research efforts, resulting in a robust therapeutic drug pipeline aimed at improving cachexia management outcomes.

- Combination therapy approaches gained strong clinical preference, as healthcare providers adopted multi-drug strategies to achieve enhanced treatment results.

- North America retained over 45.1% market share, while the Asia-Pacific region was expected to record faster growth driven by rising patient populations and healthcare advancements.

Regional Analysis

North America dominates the global cancer cachexia market. The region held a market share of more than 45.1%. This leadership is driven by a strong healthcare infrastructure and advanced cancer management practices. The growth of supportive care services for cancer patients has strengthened the market position. A high burden of cancer cases further supports demand for cachexia therapies. A focus on early diagnosis and treatment also boosts adoption rates. Investments in oncology research are significant. Favorable reimbursement systems also encourage the use of supportive therapies.

North America also benefits from the presence of several key pharmaceutical manufacturers. These companies invest in clinical research and innovation. Advanced product pipelines for cancer-related wasting syndrome are being developed. Novel technologies are emerging to improve treatment outcomes. Many ongoing trials aim to introduce safe and effective therapies. Regulatory bodies and academic centers also play a role. Their involvement enhances clinical advancement. The growing interest in targeted therapies has further strengthened the regional market outlook.

Asia-Pacific is projected to register the fastest growth during the forecast period. The rising geriatric population in countries like China and Japan increases the incidence of cachexia. Awareness about supportive cancer care is improving among healthcare professionals and patients. Access to advanced oncology services is gradually expanding. Government programs support cancer treatment facilities. Pharmaceutical companies are increasing their activities in the region. Research collaborations and clinical trial initiatives are also growing. These factors are expected to support a higher CAGR for the APAC cancer cachexia market.

Segmentation Analysis

The therapeutics segment in the cancer cachexia market is led by progesterone, which recorded the highest share in 2022. Its growth is projected at a CAGR of 5.4% from 2023 to 2032. The dominance of progesterone is attributed to its safe profile and its ability to provide pain-free treatment options. As a result, it is expected to continue driving the progestogens category. Existing therapies mainly focus on reducing discomfort and supporting palliative care. Combination therapies are also gaining traction due to their positive effects on survival and quality of life.

Across distribution channels, hospital pharmacies held the largest share in 2022. The lead position is supported by rising hospitalization rates among cancer patients and individuals with cachexia. Hospitals remain the primary point of care for advanced cancer treatment and supportive therapy, which enhances demand for prescription-based cachexia medicines. Consequently, hospital pharmacies are expected to continue maintaining a high share throughout the forecast period, supported by patient admissions and structured oncology treatment pathways.

By mode of action, weight loss stabilizers secured a significant share in 2022 and are forecast to expand at a CAGR of 4.2% through 2032. Their adoption is driven by the high burden of involuntary weight loss, inflammation, and muscle wasting in cancer patients. Around half of cancer patients develop cachexia, with cases reaching 85% during late stages. More than 45% experience weight loss above 10% during disease progression. Physicians increasingly recommend weight stabilizers to improve treatment tolerance and support patient survival outcomes.

Key Market Segments

Based on Therapeutics

- Progestogens

- Corticosteroids

- Combination Therapies

- Others

Based on Distribution Channel

- Hospital

- Retail Pharmacy

- Online Pharmacy

Based on the Mode of action

- Appetite Stimulators

- Weight Loss Stabilizers

- Others

Key Players Analysis

The cancer cachexia market is driven by limited approved treatment options. As a result, a competitive landscape is emerging where pharmaceutical companies are investing in research to address unmet clinical needs. The growth of the market can be attributed to active drug development and supportive clinical trial activities. Companies are focusing on innovative molecules targeting muscle wasting, systemic inflammation, and metabolic imbalance seen in advanced cancer patients. This approach is expected to enhance treatment outcomes and offer significant commercial potential in the coming years.

Key pharmaceutical manufacturers continue to explore multimodal therapeutic strategies. Investment in late-stage trials and expansion of supportive care solutions are increasing. Treatments targeting inflammatory pathways, appetite stimulation, and anabolic agents are under development. Cancer cachexia remains a critical area of focus due to the severe impact on patient survival and quality of life. As clinical understanding improves, companies are strengthening pipelines to secure a leading position in this high-need therapeutic space.

The competitive environment is influenced by established pharmaceutical corporations and emerging biotechnology developers. Several firms are advancing novel drug candidates such as OHR/AVR118, currently investigated in Phase 2 for cancer-related cachexia. Strong emphasis is placed on regulatory progress and strategic collaborations for research and commercialization. Industry players are adopting evidence-based strategies to accelerate approval timelines and broaden access to treatment solutions that meet oncology care requirements.

Prominent market participants include Eli Lilly and Company, Pfizer Inc., Bristol-Myers Squibb Company, Sanofi, Teva Pharmaceutical Industries Ltd., ANI Pharmaceuticals, Hikma Pharmaceuticals PLC, and SkyePharma. Other companies such as Merck & Co. Inc., Artelo Biosciences Inc., Aavogen Inc., GTx Inc., and Helsinn Healthcare SA also strengthen the market landscape. Continuous research investments and partnerships indicate positive growth prospects as firms focus on offering broad therapeutic coverage in cancer cachexia management.

Market Key Players

- Eli Lilly and Company

- Pfizer Inc.

- Bristol-Myers Squibb Company

- Sanofi

- Teva Pharmaceutical Industries Ltd.

- ANI Pharmaceuticals

- Hikma Pharmaceuticals PLC

- SkyePharma

- Other Key Players

Conclusion

The cancer cachexia market is positioned for steady expansion as global cancer cases continue to rise and supportive oncology care gains priority. Growing awareness among doctors and patients is improving early diagnosis and treatment adoption. Pharmaceutical companies are advancing new therapies that target muscle loss, appetite changes, and inflammation, which is expected to strengthen clinical outcomes. Supportive regulatory pathways and increased research funding have encouraged development of safer and more effective treatment options. With improving healthcare systems, wider access to cancer care, and sustained investment in innovation, the market is expected to benefit from long-term demand, reinforcing cancer cachexia management as an essential part of comprehensive oncology care.