Quick Navigation

Introduction

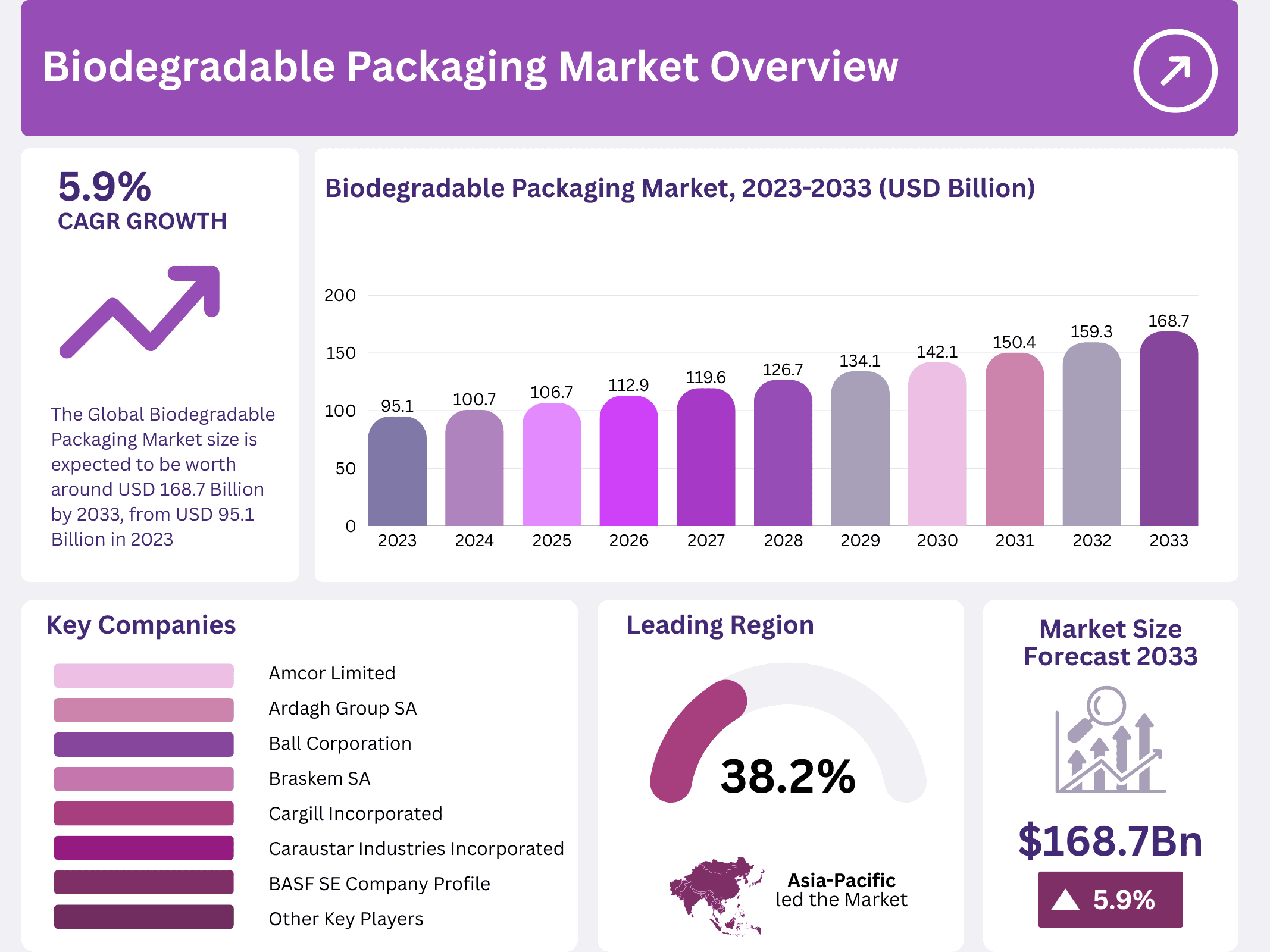

The global biodegradable packaging market is undergoing a decisive transformation. Valued at USD 95.1 billion in 2023, the market is projected to reach USD 168.7 billion by 2033, expanding at a compound annual growth rate of 5.9%. This momentum signals a fundamental shift in how industries approach packaging waste.

Consequently, businesses across food, retail, and cosmetics are rapidly adopting eco-friendly materials. From plant-based plastics to paper blends, biodegradable packaging is designed to decompose naturally, returning to the environment without long-term harm. Demand is accelerating across both developed and emerging economies.

Moreover, governments worldwide are enforcing stricter plastic regulations. The European Union’s 2021 ban on single-use plastics and India’s 2022 ban have created urgent demand for compliant alternatives. These policy shifts are compelling manufacturers to innovate faster and scale biodegradable solutions more broadly.

Furthermore, consumer behavior is shifting in tandem with regulatory action. Today’s buyers are actively choosing eco-labeled products, rewarding brands that prioritize sustainability. As a result, companies embracing biodegradable packaging are gaining measurable advantages in brand loyalty, market positioning, and long-term profitability.

In addition, technological progress is removing previous barriers. Cellulose-based packaging now decomposes in as little as 28 days, while advances in bioplastics are closing the performance gap with conventional plastics. These breakthroughs are making biodegradable options both viable and competitive across diverse applications.

Finally, global plastic waste output — exceeding 353 million tonnes annually — underscores the urgency. With over 170 countries banning single-use plastics as part of a global effort to reduce plastic use by 2030, the biodegradable packaging market stands at the center of one of the most critical sustainability transitions of this decade.

Key Takeaways

- The Biodegradable Packaging Market was valued at USD 95.1 billion in 2023 and is expected to reach USD 168.7 billion by 2033, with a CAGR of 5.9%.

- In 2023, Recycled Content Packaging led the type segment, driven by increasing consumer demand for eco-friendly solutions.

- In 2023, Plastic was the dominant material due to its flexibility and growing innovations in biodegradable plastic alternatives.

- In 2023, Food & Beverages dominated the application segment with 44%, reflecting the industry’s focus on sustainable packaging solutions.

- In 2023, Asia Pacific held 38.2% of the market, driven by increasing regulatory support for sustainable packaging practices.

Market Segmentation Overview

By type, Recycled Content Packaging leads the market. It reduces demand for virgin materials and lowers the environmental footprint of production. Additionally, Reusable Packaging is gaining ground in food service, while Degradable Packaging serves applications requiring environment-sensitive disposal methods.

By material, biodegradable plastics dominate due to their versatility. Variants such as PLA, PHA, and starch-based plastics serve a wide range of industries. Meanwhile, Paper & Paperboard — including kraft paper, corrugated fiberboard, and flexible paper — remain fundamental in reducing plastic reliance across the packaging sector.

By application, Food & Beverages holds a commanding 44% share, driven by regulations and shelf-life requirements. Consequently, sectors such as consumer products, pharmaceuticals, cosmetics, and e-commerce shipping are also adopting biodegradable packaging to meet both sustainability goals and evolving consumer expectations.

Drivers

Government regulations serve as a primary growth driver. The EU’s single-use plastic ban, India’s 2022 restrictions, and similar legislation across more than 170 countries are compelling businesses to transition away from conventional plastics. Regulatory compliance has become a baseline requirement, not a competitive differentiator.

Rising consumer preference for eco-friendly products is equally influential. As environmental awareness deepens globally, consumers are actively choosing products packaged in biodegradable materials. This behavioral shift is prompting brands to reformulate their packaging strategies, embedding sustainability into product development and corporate identity alike.

Use Cases

The food and beverage sector offers the most prominent use case. Companies like Chipotle and A&W have adopted compostable packaging for ready-to-eat meals and fresh produce. Biodegradable packaging in this context preserves product quality while aligning with mounting regulatory requirements and consumer expectations around environmental responsibility.

E-commerce logistics represent an emerging and fast-growing use case. Online retailers are replacing foam and conventional plastic fillers with biodegradable alternatives such as corrugated fiberboard and kraft paper. This shift reduces supply chain waste and appeals to sustainability-minded shoppers, reinforcing brand values across an increasingly competitive digital retail landscape.

Major Challenges

High production costs remain a persistent restraint. Biodegradable materials require more complex manufacturing processes and costlier raw inputs than conventional plastics. For small and mid-sized businesses, the price differential is a significant barrier to adoption, slowing market penetration despite growing interest in sustainable packaging solutions.

Consumer misconceptions about packaging terminology also hinder growth. Many buyers conflate biodegradable, compostable, and recyclable, leading to confusion at the point of purchase. Furthermore, inadequate composting and waste management infrastructure in many regions limits the real-world effectiveness of biodegradable packaging, reducing its environmental impact and industry credibility.

Business Opportunities

Technological innovation in bioplastics is unlocking significant opportunity. Advances in flexible, durable biodegradable materials are narrowing the performance gap with conventional plastics. Companies investing in R&D to develop stronger, longer-lasting bioplastics are well-positioned to capture market share as industries demand packaging that is both sustainable and functionally robust.

Emerging markets present another compelling avenue for expansion. Developing economies in Asia, Latin America, and Africa are experiencing rapid urbanization and growing middle-class demand for sustainable consumer goods. As environmental regulations tighten in these regions, the demand for biodegradable packaging solutions is expected to accelerate substantially over the forecast period.

Regional Analysis

Asia Pacific leads the global market with a 38.2% share, valued at USD 36.33 billion in 2023. China, India, and Japan are the primary contributors. Strict regulations, rapid urbanization, and a vast consumer base are driving strong adoption, particularly in the food and beverage sector where sustainable packaging demand is highest.

Europe follows closely, reinforced by the EU’s ambitious recycling targets of 55–80% of packaging waste. Most EU countries already met the 55% target by 2021. Meanwhile, North America benefits from consumer-driven demand and innovation in packaging technologies. Latin America and the Middle East & Africa are emerging as growth regions with increasing environmental awareness.

Recent Developments

- In October 2024, a breakthrough in bioplastic technology led to the development of 100% biodegradable material derived from barley, offering a sustainable alternative for food packaging and supporting circular economy goals.

- In August 2024, India’s Defence Research and Development Organisation (DRDO) developed PBAT-based biodegradable packaging that decomposes within 3 months, suitable for food packaging and medical waste bags.

- In June 2024, Bioelements expanded into the U.S. market with biodegradable, biobased, and compostable packaging solutions, responding to growing demand for sustainable materials from American businesses and consumers.

- In September 2024, BioPowder introduced olive stone-derived powders (branded as Olea FP) for use in biodegradable packaging applications, advancing circular economy practices through plant-derived compostable materials.

Conclusion

The biodegradable packaging market is on a clear and compelling upward trajectory. Driven by regulatory mandates, shifting consumer values, and accelerating material innovation, the industry is transforming how the world packages and protects products. From food services to e-commerce, the transition to sustainable packaging is no longer a trend — it is an imperative.

As companies navigate high production costs and infrastructure gaps, those that invest in R&D, forge strategic partnerships, and align with circular economy principles will define the next generation of packaging. With the market projected to reach USD 168.7 billion by 2033, the opportunity for forward-thinking businesses is both significant and immediate.