Quick Navigation

Market Outlook

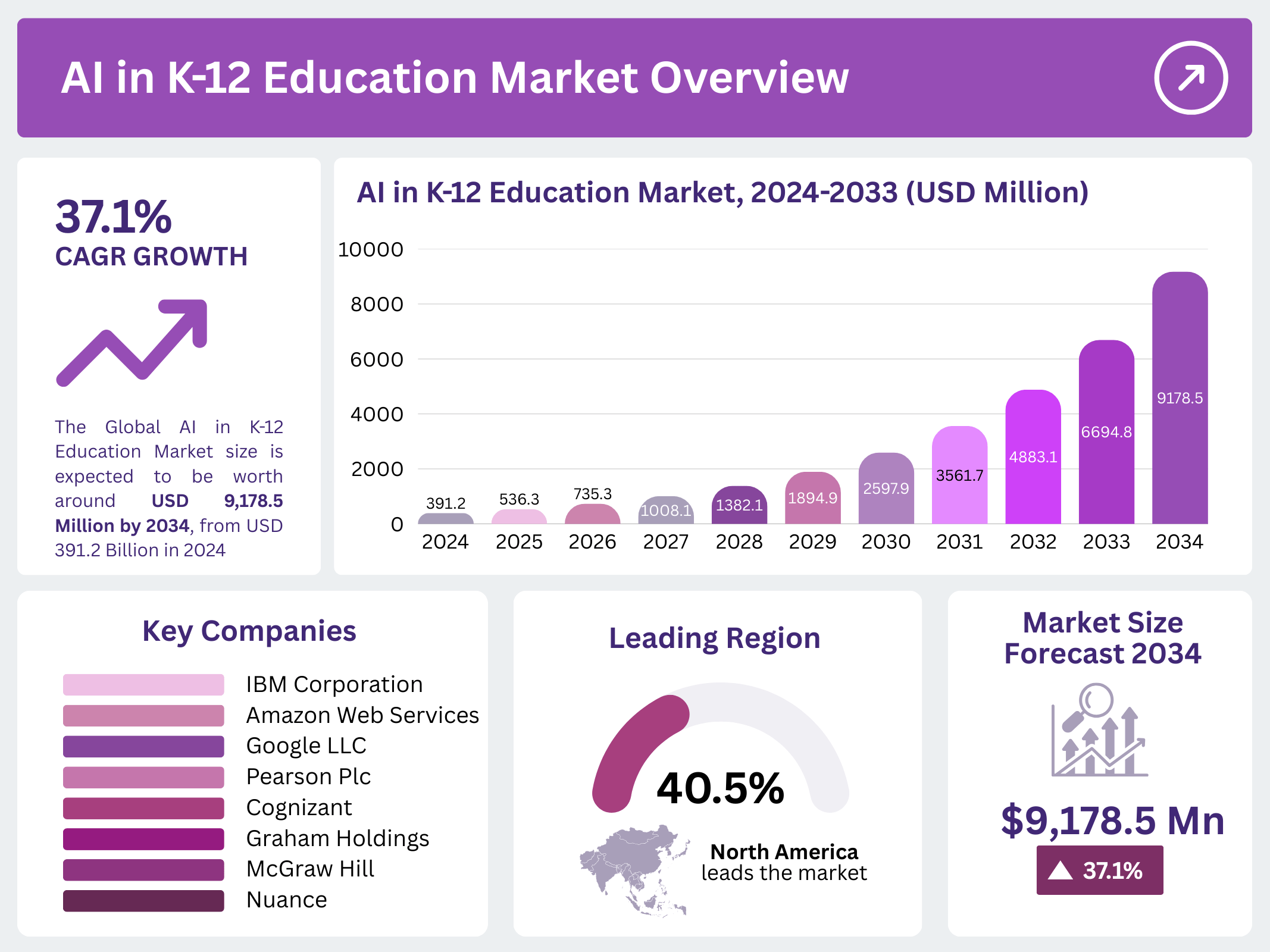

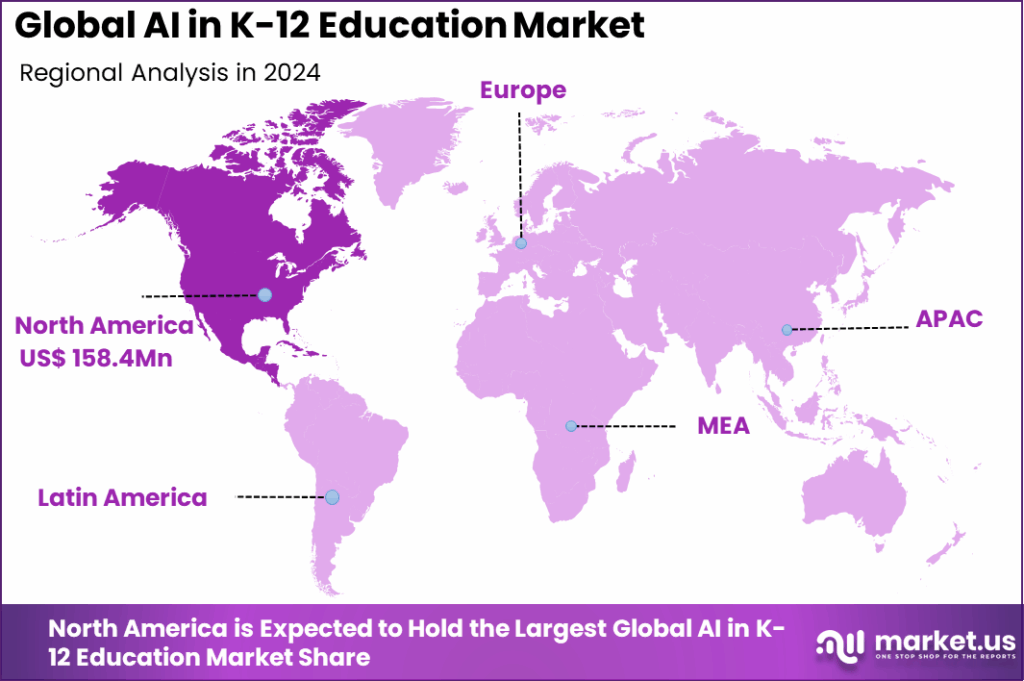

The Global AI in K-12 Education Market is on a remarkable growth path, projected to expand from USD 391.2 million in 2024 to USD 9,178.5 million by 2034. This represents a dynamic CAGR of 37.1% during 2025–2034. In 2024, North America stood as the leading region with over 40.5% share (USD 158.4 million), driven by advanced educational infrastructure and strong government support. The market’s momentum stems from rising demand for personalized learning, AI tutors, and adaptive classroom solutions, coupled with increasing investments in digital literacy programs worldwide.

Spot the next trending sample inside @ https://market.us/report/ai-in-k-12-education-market/free-sample/

Economic Ripple Effects

The acceleration of AI in education is triggering a cascading impact on the economy. Beyond school systems, this growth is generating new ecosystems in EdTech, cloud platforms, and cybersecurity. The market is contributing to efficiency in schools by automating grading and assessments, which reduces administrative costs. At a macro level, it is fueling digital skill development essential for future labor markets. As governments integrate AI curricula in schools, national productivity gains are anticipated, strengthening competitiveness in the knowledge economy.

Business Impact and Industry Shifts

Rising Costs and Supply Chain Trends

The AI education market is increasing hardware and infrastructure demand, leading to higher production costs for devices and cloud networks. Semiconductor shortages and logistics challenges also influence delivery times for AI-enabled digital tools in schools.

Sector-Specific Disruption

- Education Technology Providers: experiencing strong funding inflows and rapid scaling.

- Traditional Learning Material Companies: shifting toward AI-embedded, digital-first content.

- K-12 Institutions: transitioning to hybrid and data-driven classroom models.

- Software Innovators: prioritizing adaptive platforms and analytics dashboards.

Strategic Roadmap for Players

- Develop low-cost AI solutions for emerging markets to reduce barriers.

- Partner with regional schools and ministries of education for large-scale deployments.

- Ensure robust data security frameworks to build trust with institutions and parents.

- Create multilingual, culturally localized platforms for global expansion.

- Leverage cloud-first strategies to improve scalability and reduce infrastructure dependence.

Analyst Perspective

The present scenario reflects an expansionary phase driven by AI tutors, smart classrooms, and content automation. Moving forward, adoption will accelerate in underserved markets, bridging education gaps. Analysts expect AI to become a default enabler of personalized learning by the next decade. With supportive government initiatives, the long-term outlook is positive. In the future, AI adoption in K-12 classrooms will transition from optional innovation to mainstream necessity, empowering schools to prepare students for technology-driven economies.

Key Use Cases and Growth Drivers

| Use Cases | Growth Drivers |

|---|---|

| Virtual learning assistants | Need for round-the-clock student support |

| Automated grading | Rising teacher workload & efficiency needs |

| Dynamic content creation | Push for engaging, adaptive instructional material |

| Predictive student analytics | Focus on performance tracking & intervention |

| AI for special needs support | Global demand for inclusive education |

| Gamified AI platforms | Increased student engagement requirements |

Regional Landscape

- North America: Leads the market due to strong public and private investments in EdTech solutions.

- Europe: Follows with adoption supported by strict privacy frameworks and funding in advanced digital education initiatives.

- Asia-Pacific: Forecast as the fastest-growing region, driven by vast student populations and state-backed digital education reforms.

- Latin America & Middle East/Africa: Emerging regions where growth relies on connectivity improvements and public-private partnerships.

Emerging Business Opportunities

Businesses find potential in affordable AI-powered tools, localized apps, and subscription-based platforms for remote and hybrid learning. Offering AI-enabled STEM learning kits and language programs will cater to growing demand in both developed and developing regions. Strong opportunities exist in serving rural and underserved schools, where AI can close accessibility gaps. Firms that focus on cost-efficient, cross-platform, and curriculum-integrated AI systems are positioned to gain market leadership.

Market Segmentation Insights

The market is divided into:

- Deployment Modes: Cloud vs. On-premises AI solutions.

- Applications: Virtual tutoring, automated grading, content development, student analytics, and classroom management.

- End-users: Public schools, private schools, hybrid and online learning centers.

The cloud-based and virtual tutoring segments are showing the fastest adoption due to lower transactional costs and ease of integration.

Competitive Landscape

The industry features global tech giants, EdTech challengers, and content providers embracing AI. Competition is driven by efforts to innovate with personalized platforms, localized curricula, and scalability. Vendors are focusing on AI-driven analytics, blockchain certification, and cloud compatibility to gain an edge. Many players are pursuing strategic acquisitions and partnerships to expand reach and diversify their AI portfolios.

Recent Market Movements

- Expansion of AI tutor integration in public schools across leading economies.

- Increased funding for language learning AI platforms in the Asia-Pacific.

- Public-private initiatives in equitable AI adoption for rural education systems.

Final Word

The AI in K-12 Education Market stands as one of the fastest-growing EdTech domains globally. With exponential CAGR and transformative use cases, it promises not only to reshape classrooms but also to redefine global competitiveness through future-ready workforces.