Quick Navigation

Overview

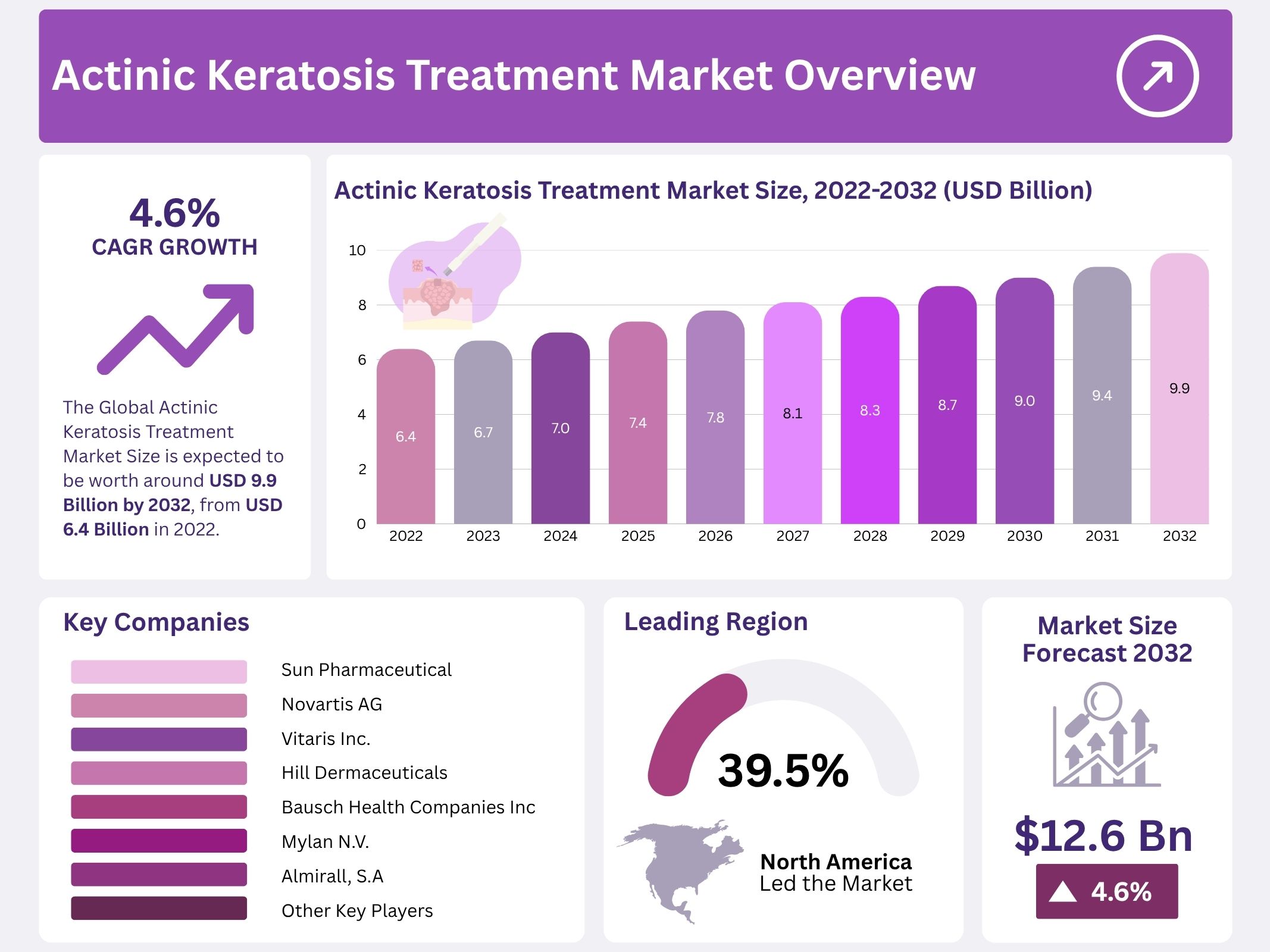

The Global Actinic Keratosis Treatment Market was valued at USD 6.4 billion in 2022 and is projected to reach approximately USD 9.9 billion by 2032, registering a compound annual growth rate (CAGR) of 4.6% from 2024 to 2033. This steady expansion is driven by the increasing prevalence of actinic keratosis (AK), advancements in treatment technologies, and rising awareness of early-stage skin cancer prevention. The growing emphasis on timely diagnosis and preventive dermatology practices is also playing a crucial role in accelerating market demand across developed and emerging regions.

The rising incidence of actinic keratosis, primarily caused by long-term ultraviolet (UV) exposure, is a key growth driver. Elderly populations and individuals in sun-exposed geographic areas represent a major patient base. Studies indicate that AK affects nearly 60% of fair-skinned adults over 60 years old, creating a significant treatment demand. Public health campaigns and dermatology awareness programs are further improving early detection rates. Patients are increasingly seeking medical attention to prevent the progression of AK into squamous cell carcinoma, leading to a rise in the adoption of both topical and procedural therapies.

Technological innovation has significantly improved treatment effectiveness. Advances such as photodynamic therapy (PDT), cryotherapy, and topical immunomodulators offer higher efficacy with fewer recurrences. The growing use of field-directed and combination therapies has enhanced patient compliance and clinical outcomes. Minimally invasive treatments are particularly gaining traction, as they provide faster recovery and better cosmetic results compared to surgical methods. This shift toward less invasive care aligns with patient preferences for comfort, safety, and improved aesthetic appearance.

Government initiatives and institutional support have further strengthened the market landscape. Healthcare authorities in regions such as North America and Europe are promoting screening and preventive programs for precancerous skin conditions. Favorable reimbursement policies and investments in cancer prevention have encouraged wider use of diagnostic and therapeutic solutions. Pharmaceutical companies are also increasing their R&D investments in innovative topical agents and targeted drug formulations. Clinical trials are exploring new molecules and treatment combinations, which are expected to expand the product pipeline in the near future.

Additionally, the growth of dermatology infrastructure in developing markets and the adoption of teledermatology platforms are improving treatment accessibility. The rising demand for cosmetic dermatology and preventive skincare has also created parallel opportunities for AK management. Increasing consumer focus on skin health and early intervention continues to boost the overall market outlook. Collectively, these factors indicate that the actinic keratosis treatment sector will maintain steady and sustainable growth over the forecast period.

Key Takeaways

- The Actinic Keratosis Treatment Market is projected to expand at a CAGR of 4.6% between 2023 and 2032, indicating steady long-term growth.

- Surgical procedures, particularly cryotherapy, dominated the market in 2022, accounting for 55.4% of total treatment revenues.

- Nucleoside metabolic inhibitors led the drug class segment with a 33% market share, highlighting their widespread clinical use and effectiveness.

- Online providers recorded the fastest growth, supported by increasing consumer preference for online drug purchases and digital healthcare platforms.

- North America captured a significant 39.5% market share in 2022, driven by advanced healthcare infrastructure and high treatment adoption.

- The Asia-Pacific region is projected to witness the highest CAGR, supported by rising diagnosis rates and expanding access to dermatological care.

- Leading companies are emphasizing product innovation to strengthen competitiveness and meet the growing demand for advanced actinic keratosis therapies.

- Research into novel treatments and the availability of cost-effective generic drugs are creating promising opportunities for market expansion.

Regional Analysis

North America held a dominant share of 39.5% in the actinic keratosis treatment market in 2022. The region’s dominance is attributed to the high prevalence of skin diseases and increasing awareness among consumers. Advancements in treatment technologies and government support also contribute to this growth. Improved healthcare infrastructure and easy access to medical care further strengthen the market. Additionally, the presence of leading market players enhances competition and innovation in the region, sustaining its strong position in the global landscape.

Favorable government initiatives and reimbursement policies are driving the market in North America. These initiatives ensure affordability and accessibility of advanced treatment options for patients. Continuous investments in healthcare infrastructure and research activities are improving treatment outcomes. Moreover, collaborations between healthcare organizations and pharmaceutical companies are fostering product innovation. The proactive approach toward early disease detection and preventive care is also boosting market demand, strengthening the region’s leadership in actinic keratosis treatment adoption and technological development.

The Asia-Pacific region is expected to record the fastest growth rate during the forecast period. This growth is driven by rising disease awareness, growing disposable incomes, and improved access to dermatological care. Countries such as Australia and New Zealand report high disease prevalence, increasing the demand for treatment solutions. Pharmaceutical companies are expanding their operations in the region through partnerships and strategic investments. Additionally, government efforts to modernize healthcare infrastructure are encouraging treatment adoption, making Asia-Pacific a key emerging market for actinic keratosis treatment.

Segmentation Analysis

The global actinic keratosis treatment market is segmented into surgery, topical, and photodynamic therapy. The surgery segment recorded the largest market share of 55.4% in 2022. This dominance is linked to the increasing adoption of cryotherapy as a preferred treatment option for actinic keratosis. The topical segment held a significant share during the historical period due to the convenience of self-administered and home-based therapies. Photodynamic therapy is projected to grow at a CAGR of 6.8%, driven by rising demand for non-invasive treatment alternatives.

Based on drug class, the actinic keratosis treatment market is segmented into nucleoside metabolic inhibitors, immune response inhibitors, NSAIDs, photo enhancers, and others. The nucleoside metabolic inhibitor segment captured the highest market share of 33% in 2022. The segment’s dominance is attributed to the strong sales performance of drugs such as Fluroplex and Efudex. In addition, growing awareness about field-directed treatments, including 5-fluorouracil, and the American Academy of Dermatology’s recommendation of 5-FU as a first-line therapy are expected to support continued segment growth.

The distribution channel segment of the market is divided into online providers, drug stores, and retail pharmacies. Among these, online providers are projected to record the fastest CAGR during the forecast period. This trend is attributed to the growing preference for online drug purchases, increasing internet penetration, and awareness of digital pharmacies. Meanwhile, drug stores and retail pharmacies continue to hold a strong position, registering a steady CAGR of 5.1% due to the accessibility and trust associated with physical pharmacy outlets.

Key Market Segments

By Therapy

- Surgery

- Topical

- Photodynamic Therapy

By Drug Class

- Nucleoside Metabolic Inhibitor

- Immune Response Modifiers

- NSAIDs

- Photo enhancer

- Other Drug Classes

By Distribution Channel

- Hospital Pharmacies

- Drug Stores & Retail Pharmacies

- Online Providers

Key Players Analysis

The actinic keratosis treatment market is characterized by intense competition and ongoing innovation. The market is driven by a mix of large pharmaceutical companies and emerging biotechnology firms focusing on effective and affordable therapies. Continuous advancements in dermatological research and improved product accessibility have accelerated growth. Companies are emphasizing expanding their portfolios and enhancing treatment effectiveness through technological developments and strong distribution channels. This has resulted in a diversified and competitive market structure where innovation and patient-focused outcomes remain key priorities.

Sun Pharmaceutical Industries Ltd. maintains a strong presence through its wide dermatological product range and established global network. The company benefits from its robust brand image and distribution strength, allowing it to reach extensive markets. Novartis AG continues to lead with its significant R&D investment and strategic partnerships. Its focus on advanced therapies and clinical research keeps it ahead in developing innovative skin disease treatments. These initiatives have helped both companies maintain a dominant market position and drive overall market growth.

Vitaris Inc. is recognized for its patient-centric approach and focus on cost-effective treatment solutions. The company integrates research-driven advancements to enhance product performance and accessibility. Hill Dermaceuticals, Inc. concentrates on the development and improvement of high-quality dermatological treatments. Its strong marketing strategies and clinical support services strengthen its market standing. Both companies contribute to expanding treatment options and ensuring affordability, which is essential for addressing the rising prevalence of actinic keratosis across global populations.

Other prominent players, including Bausch Health Companies Inc., Almirall S.A., Galderma S.A., and Mylan N.V., are focusing on innovation and market expansion. Additionally, organizations like 3M Company, Stanford Chemicals, and McKesson Corporation support the market through diversified product portfolios and strategic alliances. The presence of smaller biotechnology firms further enhances competition by introducing niche solutions and novel drug formulations. Collectively, these efforts ensure steady progress in actinic keratosis treatment development and reflect the market’s dynamic and evolving nature.

Market Key Players

- Sun Pharmaceutical Industries Ltd.

- Novartis AG

- Vitaris Inc.

- Hill Dermaceuticals, Inc.

- Bausch Health Companies Inc.

- Mylan N.V.

- Almirall, S.A.

- Galderma S.A.

- 3M Company

- Stanford Chemicals

- Mckesson Corporation

- Other Key Players

Conclusion

The global actinic keratosis treatment market is expected to grow steadily due to the increasing number of cases and growing awareness about early skin cancer prevention. Advances in treatment options, such as topical agents, cryotherapy, and photodynamic therapy, are improving patient outcomes and driving demand. Supportive government policies and continuous investment in dermatological research are further strengthening the market. In addition, rising healthcare access in developing regions and the popularity of online pharmacies are expanding treatment reach. Overall, the market outlook remains positive, supported by innovation, preventive care initiatives, and increasing patient awareness.