Global 3D Printing Market By Component (Software, Hardware, Services), By Printer Type (Industrial 3D Printer, Desktop 3D Printer), By Technology (Selective Laser Sintering, Stereolithography, Fuse Deposition Modeling, Direct Metal Laser Sintering, Inkjet Printing, Polyjet Printing, Electron Beam Melting, Laminated Object Manufacturing, Digital Light Processing, Laser Metal Deposition, Others), By Application (Functional Parts, Tooling, Prototyping), By Vertical(Industrial 3D Printing [Automotive, Aerospace & Defense, Healthcare, Consumer Electronics, Industrial, Power & Energy, Others], Desktop 3D Printing [Educational Purpose, Fashion & Jewelry, Objects, Dental, Food, Others]), By Material (Metal, Polymer, Ceramic), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2024-2033

- Published date: Jan. 2024

- Report ID: 102268

- Number of Pages: 302

- Format:

- keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Component Analysis

- Printer Type Analysis

- Technology Analysis

- Application Outlook

- Vertical Insights

- Material Analysis

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenges

- Key Market Trends

- Key Market Segmentation

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

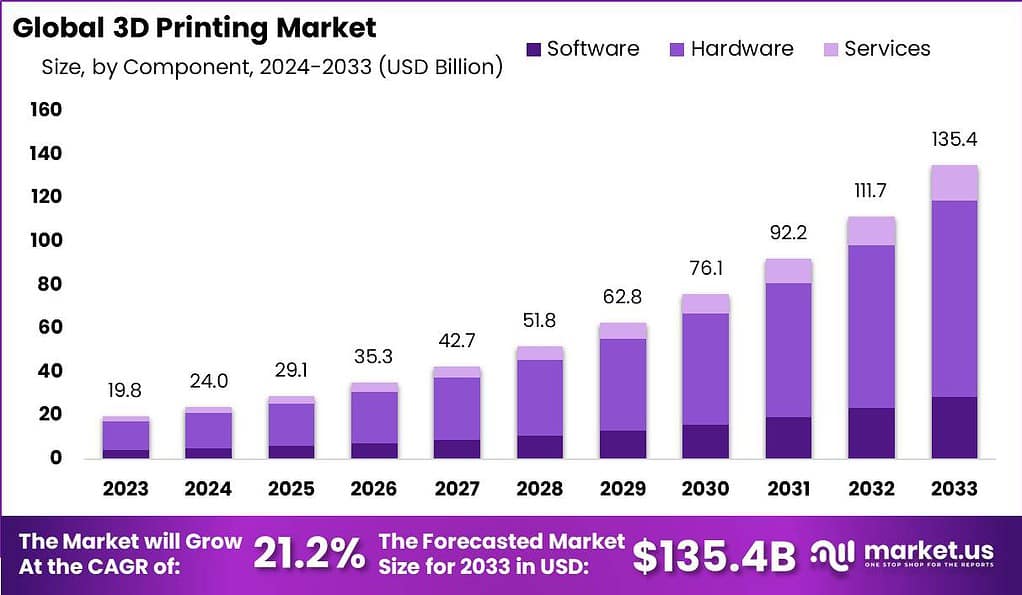

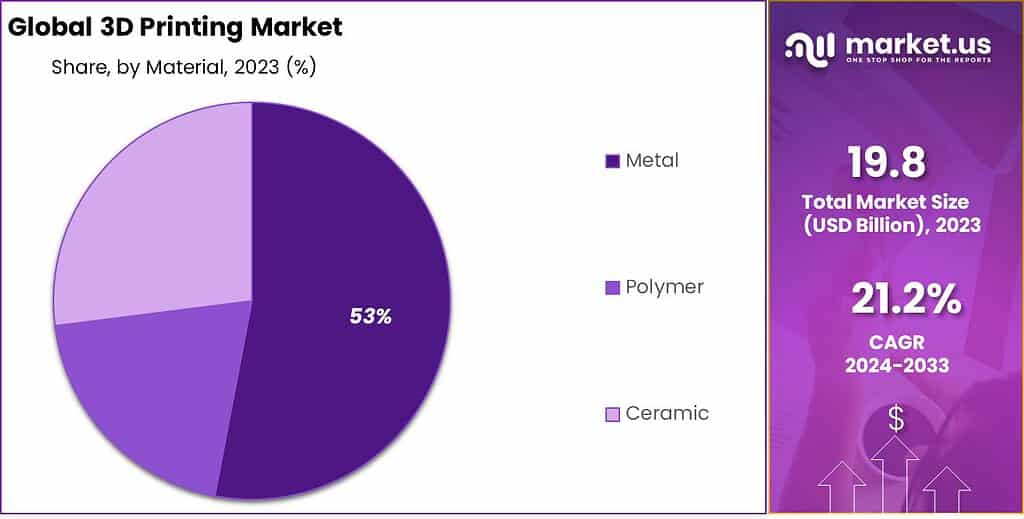

The Global 3D Printing Market is projected to be worth USD 19.8 billion in 2023. The market is likely to reach USD 135.4 billion by 2033. The market is further expected to surge at a CAGR of 21.2% during the forecast period 2024 to 2033.

3D printing, also known as additive manufacturing, is a process of making three dimensional solid objects from a digital file. It is achieved using a specialized printer which lays down successive layers of material until the entire object is created. It consists of the creation of objects by layering successive layers of materials, including metal, plastic or composite materials to ensure that the design is created.

The 3D printing market refers to the industry surrounding the development, production, and adoption of 3D printing technologies and services. It encompasses a wide range of stakeholders, including 3D printer manufacturers, material suppliers, software developers, service bureaus, and end-users from various sectors such as aerospace, automotive, healthcare, consumer goods, and education.

Note: Actual Numbers Might Vary In The Final Report

Key Takeaways

- Market Growth Projection: It is estimated that the 3D Printing Market is expected to reach USD 135.4 billion by 2033, and an average CAGR in the range of 21.2% over the forecast time.

- Key Components: The market is segmented into three key components: Software, Hardware, and Services. Hardware dominates with a market share of over 67%, followed by Software and Services.

- Printer Types: Two primary printer types are Industrial 3D Printers and Desktop 3D Printers. Industrial 3D Printers hold a dominant position with over 75% market share due to their precision and compatibility.

- Technological Landscape: Various technologies are in use, with Stereolithography, Selective Laser Sintering (SLS), and Fuse Deposition Modeling (FDM) among the prominent ones, each catering to specific industry needs.

- Applications: 3D printing finds applications in Functional Parts, Tooling, and Prototyping, with Prototyping commanding over 54% of the market share due to its role in rapid and cost-effective product development.

- Vertical Insights: The market is segmented into Industrial 3D Printing and Desktop 3D Printing, with the Automotive industry leading in the former and Educational Purpose and Fashion & Jewelry in the latter.

- Materials: Materials used include Metal, Polymer, and Ceramic. Metal printing holds a commanding market share of over 53%, driven by its precision and durability.

- Driving Factors: Market growth is driven by technological advancements, cost-efficiency, customization demands, and a focus on sustainability.

- Challenges: Challenges include limited material selection, regulatory hurdles, intellectual property concerns, and a shortage of skilled workforce.

- Growth Opportunities: Opportunities include healthcare applications, automotive innovation, aerospace manufacturing, and education and training programs related to 3D printing.

- Key Market Trends: Trends include the growth of metal 3D printing, additive manufacturing in construction, bioprinting, and distributed manufacturing.

- Regional Analysis: North America leads the market, followed by Europe and the Asia-Pacific region. Each region has its unique strengths and growth drivers.

- Key Market Players: Leading companies in the 3D printing market include Stratasys Ltd, Materialise, EnvisionTec Inc, 3D Systems Inc, and GE Additive, among others.

Component Analysis

In 2023, the 3D printing market exhibited notable segmentation across three key components: Software, Hardware, and Services. The Hardware segment emerged as the frontrunner, firmly establishing its dominance with a commanding market share of over 67%. This significant presence can be credited to the continually rising demand for state-of-the-art 3D printing equipment and devices, which have become indispensable in various industries such as aerospace, automotive, and healthcare. Hardware offerings have consistently evolved, integrating innovative features, improved precision, and greater efficiency, thereby increasing their attractiveness among businesses aiming to optimize their manufacturing processes.

The Software component, it also played a pivotal role in the market landscape. Although not as dominant as Hardware, the Software segment demonstrated steady growth, commanding a significant portion of the market share. This growth was driven by the continuous development of sophisticated 3D printing software solutions, designed to streamline design processes, enhance compatibility with diverse hardware setups, and facilitate seamless printing operations. As businesses increasingly recognized the importance of efficient software integration for achieving optimal results, this segment experienced sustained expansion.

Lastly, the Services segment, while holding a relatively smaller portion of the market share, remained a critical aspect of the 3D printing ecosystem. Companies sought specialized 3D printing services for prototyping, consulting, and customization, catering to their unique requirements. Although it did not command the same market share as Hardware or Software, the Services segment continued to grow steadily, driven by its ability to provide tailored solutions and expertise to businesses seeking to harness the full potential of 3D printing technology.

Printer Type Analysis

In 2023, the 3D printing market witnessed a compelling segmentation based on Printer Types, primarily categorized into Industrial 3D Printers and Desktop 3D Printers. The Industrial 3D Printer Segment emerged as the undisputed leader, firmly securing a dominant market position with an impressive share of over 75%.

This dominant presence can be ascribed to the extensive adoption of industrial-grade 3D printing technology across diverse sectors, including aerospace, automotive, and healthcare. Industrial 3D printers have consistently showcased their ability to provide high precision, large-scale manufacturing capabilities, and compatibility with a broad range of materials, making them the preferred choice for businesses with stringent quality and production requirements.

On the other hand, the Desktop 3D Printer Segment, while holding a smaller market share, has been steadily gaining traction. These compact and user-friendly 3D printers have found favor among smaller businesses, educational institutions, and individual enthusiasts. The segment’s growth has been fueled by continuous advancements in desktop 3D printer technology, making them more affordable and accessible. Their versatility and ease of use have opened up opportunities for rapid prototyping, personalized manufacturing, and creative experimentation.

Technology Analysis

In 2023, the 3D printing market underwent a comprehensive technological segmentation, with various methods vying for prominence. Among these, the Stereolithography segment emerged as a dominant force, commanding a significant market share of over 11%. This noteworthy position can be attributed to Stereolithography’s reputation for delivering exceptional precision and surface quality in 3D-printed objects.

Stereolithography has emerged as the preferred choice in industries like healthcare, automotive, and aerospace, where the production of intricate and highly detailed components is crucial. The capability of Stereolithography to manufacture complex parts with exceptional accuracy and resolution has solidified its position as a fundamental technology in the 3D printing landscape.

Another significant player in this technological realm is Selective Laser Sintering (SLS), which holds a considerable share of the market. The popularity of SLS technology is propelled by its versatility in working with a diverse range of materials, including plastics, metals, and ceramics. This adaptability has made it indispensable in industries requiring functional prototypes and end-use parts. Its ability to produce robust, high-strength components has positioned SLS as a key player in the 3D printing landscape.

In 2023, the Fuse Deposition Modeling (FDM) segment made substantial advancements, securing a significant market share. The attractiveness of FDM stems from its accessibility and cost-effectiveness, rendering it an appealing choice for small and medium-sized enterprises (SMEs) and hobbyists. With the ongoing advancements in FDM technology, it has continued to improve in terms of speed, precision, and material compatibility.

Direct Metal Laser Sintering (DMLS) and Electron Beam Melting (EBM) secured their foothold in industries demanding metal parts with outstanding mechanical properties. These technologies have found applications in aerospace, healthcare, and automotive sectors where the strength-to-weight ratio and material integrity are critical factors.

Inkjet Printing and Polyjet Printing, known for their ability to produce multi-material and full-color prototypes, contributed significantly to the 3D printing market’s diversification. These technologies have become essential in industries where aesthetics and intricate designs are paramount, such as consumer goods and fashion.

Laminated Object Manufacturing (LOM) gained traction as a cost-effective solution for producing large-scale parts, particularly in industries like architecture and construction. Its ability to create large, robust prototypes and models swiftly has positioned it as a valuable player in the market.

Digital Light Processing (DLP) and Laser Metal Deposition (LMD) technologies have carved out their niche in specialized applications. DLP’s speed and precision make it ideal for dental and jewelry industries, while LMD’s ability to add metal layers for repair and modification is invaluable in the maintenance and aerospace sectors.

Application Outlook

In 2023, the 3D printing market exhibited a diverse array of applications, with a notable segmentation into Functional Parts, Tooling, and Prototyping. Among these segments, the Prototyping segment stood out as the dominant force, commanding a substantial market share of over 54%. This prominent position can be attributed to the indispensable role that 3D printing technology plays in the rapid and cost-effective creation of prototypes across various industries.

From automotive to aerospace, businesses across the spectrum relied heavily on 3D printing for prototyping purposes. Its ability to swiftly translate design concepts into tangible prototypes not only accelerated product development cycles but also significantly reduced development costs, making it a preferred choice for companies seeking innovation and efficiency.

Meanwhile, the Functional Parts segment also held a significant portion of the market. As 3D printing technology continued to advance, it became increasingly viable for the production of functional components used in end-use products. Industries such as healthcare and manufacturing saw substantial benefits in the creation of custom, complex parts with tailored functionalities. This shift towards 3D printing for functional parts highlighted its potential to revolutionize traditional manufacturing processes and address specific needs in a wide range of sectors.

In the realm of Tooling, 3D printing played a crucial role in crafting specialized tools and molds. While this segment held a smaller market share compared to Prototyping and Functional Parts, its importance cannot be overstated. Tooling is vital for maintaining production efficiency and precision, and 3D printing offered a nimble and cost-effective solution for tool and mold production.

Vertical Insights

In 2023, the 3D printing market was characterized by a robust segmentation based on vertical insights, with a particular focus on two major categories: Industrial 3D Printing and Desktop 3D Printing. Within Industrial 3D Printing, the Automotive segment emerged as the dominant player, solidifying its market position with an impressive share of over 61%. This commanding presence was driven by the automotive industry’s increasing reliance on 3D printing technology to revolutionize the production of vehicle components. 3D printing not only enabled automotive manufacturers to reduce production costs but also facilitated the creation of lightweight, intricate parts that improved fuel efficiency and performance.

The Aerospace & Defense vertical also played a significant role within the Industrial 3D Printing category, harnessing the technology for the fabrication of complex, high-performance aircraft and defense equipment components. Healthcare was another pivotal sector, leveraging 3D printing to create personalized medical implants and prosthetics, thereby enhancing patient care. Consumer Electronics, Industrial machinery, and Power & Energy sectors embraced 3D printing to optimize manufacturing processes, boost product innovation, and reduce lead times.

On the other hand, within the Desktop 3D Printing category, the Educational Purpose segment made a notable impact, catering to the needs of educational institutions seeking to introduce students to the world of 3D printing technology. Fashion & Jewelry also found its niche, with designers and jewelers utilizing desktop 3D printers to craft intricate and customized pieces. Objects, Dental, and Food segments further diversified the desktop 3D printing landscape, offering solutions for creating various items, dental models, and even edible creations.

Material Analysis

In 2023, the 3D printing market experienced a significant segmentation based on the materials used, with a focus on three major categories: Metal, Polymer, and Ceramic. Among these, the Metal segment emerged as the uncontested leader, firmly establishing its dominance by capturing an impressive market share of over 53%. This commanding position was attributed to the growing demand for metal 3D printing across various industries, including aerospace, automotive, and healthcare.

Metal 3D printing offered unparalleled precision and strength, making it the material of choice for the production of critical components and parts that required exceptional durability and performance. Its ability to create intricate, high-quality metal objects with reduced waste and enhanced design flexibility made it a pivotal force in the 3D printing landscape.

Polymer materials also held a substantial portion of the market, offering versatility and cost-effectiveness. They found extensive use in applications ranging from consumer goods to prototyping. With ongoing advancements in polymer-based 3D printing, these materials continued to evolve, becoming more accessible and accommodating a wider array of production needs.

Driving Factors

- Technology Advancements: Continuous advancements in 3D printing technology, such as faster printing speeds and improved materials, are driving market growth. These innovations enhance the efficiency and capabilities of 3D printers.

- Cost-Efficiency: 3D printing offers cost-effective solutions for rapid prototyping and manufacturing. Reduced material waste and streamlined production processes contribute to its adoption across various industries.

- Customization Demands: Growing consumer and industrial demand for customized products is a significant driver. 3D printing enables the production of tailor-made items, from personalized medical implants to customized consumer goods.

- Sustainability Focus: With increasing environmental concerns, 3D printing’s eco-friendly attributes are gaining attention. It minimizes waste by using only the required materials, aligning with the sustainability goals of many businesses.

Restraining Factors

- Limited Material Selection: The availability of suitable materials for 3D printing is still somewhat limited. This constraint can hinder the production of certain complex or high-performance parts.

- Regulatory Challenges: Stringent regulations in industries like aerospace and healthcare may pose obstacles. Ensuring compliance with quality and safety standards can be complex and time-consuming.

- Intellectual Property Concerns: The ease of replicating objects through 3D printing raises intellectual property issues. Protecting designs and preventing counterfeiting can be challenging.

- Lack of Skilled Workforce: The 3D printing industry requires a skilled workforce to operate and maintain printers effectively. A shortage of qualified professionals can slow down adoption.

Growth Opportunities

- Healthcare Applications: 3D printing’s potential in creating patient-specific implants, prosthetics, and even organs opens up vast opportunities within the healthcare sector.

- Automotive Innovation: The automotive industry sector can gain from 3D printing to create lightweight and complicated parts, which can lead to fuel efficiency and less emissions.

- Aerospace Manufacturing: In the aerospace industry, 3D printing is a great way to decrease the mass of parts increasing fuel efficiency and reducing overall cost.

- Education and Training: The requirement for education and training programs in relation the printing process 3D is an expanding market, providing opportunities for training institutions and providers.

Challenges

- Quality Control: Keeping a consistent quality for 3D-printed items can be a challenge because of the variations in printing properties and material properties. processes

- Post-Processing Requirements: A large number of 3D-printed objects require post-processing for example, painting or sanding which may increase the time and cost of production.

- Scalability Issues: The process of scaling up 3D printing to large-scale production is a challenge particularly when compared to traditional manufacturing techniques.

- Market Competition: The 3D printing industry expands and competition grows, it makes it challenging it for newcomers to make a name their own brands.

Key Market Trends

- Metal 3D Printing: The use of 3D printing on metal is growing which allows the manufacture of highly-strength and intricate metal parts.

- Additive Manufacturing in Construction: 3D printing is currently being utilized to build buildings and structures and infrastructure, allowing for cost savings as well as design flexibility.

- Bioprinting: The science of bioprinting, which entails 3D printing living organs and tissues is developing, with implications for the pharmaceutical industry and healthcare.

- Distributed Manufacturing: This idea distribution manufacturing in which items are 3D printed closer than the place of usage, is growing in popularity, and can help reduce the cost of logistics and inventory.

Key Market Segmentation

Component

- Software

- Hardware

- Services

Printer Type

- Industrial 3D Printer

- Desktop 3D Printer

Technology

- Selective Laser Sintering

- Stereolithography

- Fuse Deposition Modeling

- Direct Metal Laser Sintering

- Inkjet Printing

- Polyjet Printing

- Electron Beam Melting

- Laminated Object Manufacturing

- Digital Light Processing

- Laser Metal Deposition

- Others

Application

- Functional Parts

- Tooling

- Prototyping

Vertical

- Industrial 3D Printing

- Automotive

- Aerospace & Defense

- Healthcare

- Consumer Electronics

- Industrial

- Power & Energy

- Others

- Desktop 3D Printing

- Educational Purpose

- Fashion & Jewelry

- Objects

- Dental

- Food

- Others

Material

- Metal

- Polymer

- Ceramic

Regional Analysis

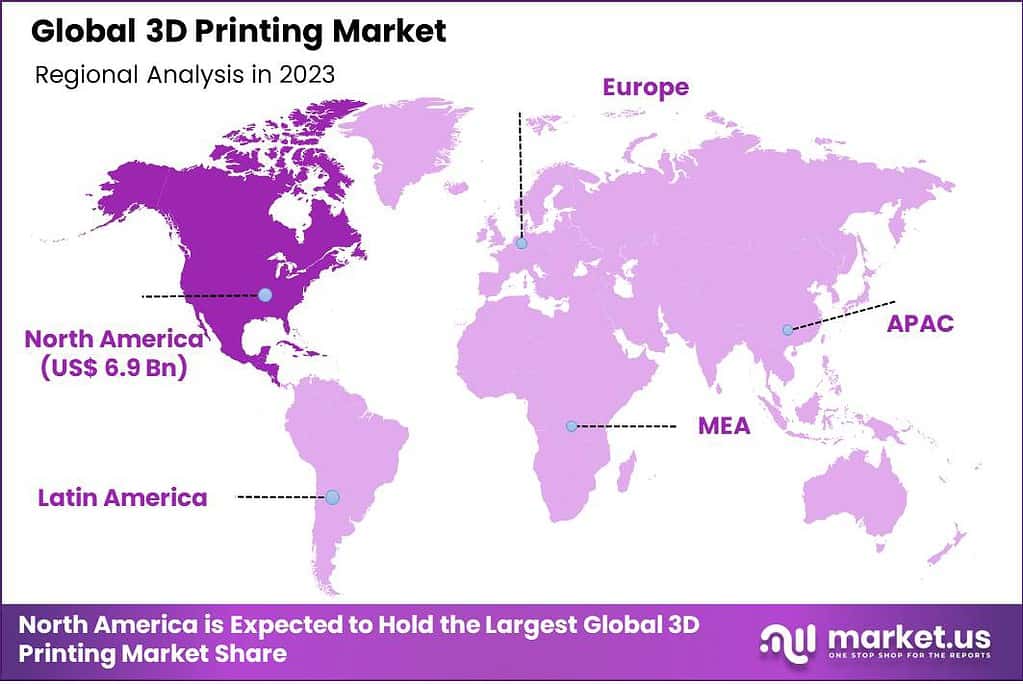

The North America held a leading position within the world of 3D printing with a staggering percentage of more than 35%. This dominance is due to the region’s initial and robust adoption of 3D printing technology across a variety of industries, including aerospace medical, automotive, and healthcare. It is the United States, in particular has a well-established 3D printing industry with a variety of companies leading the way with innovative additive manufacturing techniques. The demand for 3D Printing in North America reached USD 6.9 billion in 2023, and there are optimistic projections for significant growth in the foreseeable future.

The European market’s strength lies in its diverse industrial base, with countries like Germany, the United Kingdom, and France driving the adoption of 3D printing for advanced manufacturing applications. The region’s emphasis on sustainability and reducing carbon footprint through additive manufacturing techniques has led to significant growth. Europe’s supportive regulatory environment and collaborations between research institutions and industry players contribute to its substantial presence in the 3D printing market.

The Asia-Pacific (APAC) region has seen rapid growth, Countries such as China, Japan, and South Korea are at the leading the way in 3D printing adoption particularly in fields like healthcare, electronics and automobile. APAC’s growing manufacturing sector and increasing investment into research and development and the presence of skilled workers have fueled the region’s expansion in the market for 3D printing.

Latin America and the Middle East & Africa (MEA) regions contributed together to around some percent in market shares by 2023. Although these areas have an accelerated rate of adoption in comparison to other regions but the potential for 3D printing is clear especially in sectors like construction in which additive manufacturing is employed to build components

Note: Actual Numbers Might Vary In The Final Report

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The 3D printing market is comprised of several key players that operate in different segments of the industry, including 3D printer manufacturers, material suppliers, software developers, and service providers. Stratasys Ltd, The leading company in Making improvements in 3D printing technology to meet the growing demand for 3D printing technology from the healthcare, aerospace, defense, and automotive industries.

Top Key Players in the 3D Printing Market

- Stratasys Ltd

- Materialise

- EnvisionTec Inc

- 3D Systems Inc

- GE Additive

- Autodesk Inc

- Made In Space

- Canon Inc

- Voxeljet AG

- Other Key Players

Recent Developments

- In March 2023, Materialise joined forces with Exactech, a developer of cutting-edge instrumentation, implants, and other intelligent technologies for joint replacement surgery. The collaboration aims to offer advanced treatment alternatives for individuals facing severe shoulder defects.

- In February 2023, Stratasys entered into a partnership with Ricoh USA, Inc. to provide on-demand 3D-printed anatomic models tailored for clinical settings.

- Also in February 2023, Desktop Metal introduced Einstein Pro XL, an affordable, high-accuracy, high-throughput 3D printer designed for dental labs, orthodontists, and other manufacturers of medical devices.

Report Scope

Report Features Description Market Value (2023) US$ 19.8 Bn Forecast Revenue (2033) US$ 135.4 Bn CAGR (2024-2033) 21.2% Base Year for Estimation 2023 Historic Period 2018-2022 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component (Software, Hardware, Services), By Printer Type (Industrial 3D Printer, Desktop 3D Printer), By Technology (Selective Laser Sintering, Stereolithography, Fuse Deposition Modeling, Direct Metal Laser Sintering, Inkjet Printing, Polyjet Printing, Electron Beam Melting, Laminated Object Manufacturing, Digital Light Processing, Laser Metal Deposition, Others), By Application (Functional Parts, Tooling, Prototyping), By Vertical(Industrial 3D Printing [Automotive, Aerospace & Defense, Healthcare, Consumer Electronics, Industrial, Power & Energy, Others], Desktop 3D Printing [Educational Purpose, Fashion & Jewelry, Objects, Dental, Food, Others]), By Material (Metal, Polymer, Ceramic) Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; The Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA. Competitive Landscape Stratasys Ltd, Materialise, EnvisionTec Inc, 3D Systems Inc, GE Additive, Autodesk Inc, Made In Space, Canon Inc, Voxeljet AG, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) Frequently Asked Questions (FAQ)

What does the term “3D Printing” refer to?3D Printing, or additive manufacturing, is a process of creating three-dimensional objects layer by layer from digital models using materials such as plastic, metal, or resin.

How big is 3D Printing Market?The Global 3D Printing Market is projected to be worth USD 19.8 billion in 2023. The market is likely to reach USD 135.4 billion by 2033. The market is further expected to surge at a CAGR of 21.2% during the forecast period 2024 to 2033.

What industries benefit from 3D Printing technology?Various industries, including aerospace, healthcare, automotive, and manufacturing, benefit from 3D Printing technology due to its versatility in creating complex and customized components.

How does North America contribute to the 3D Printing Market?North America holds a dominant position in the 3D Printing Market, with a share of over 35%. The region's early adoption and robust integration of 3D printing technologies across industries contribute to its leadership.

What are some challenges in the 3D Printing Market?Challenges include maintaining consistent quality in 3D-printed products, addressing post-processing requirements, and overcoming scalability issues for mass production compared to traditional manufacturing methods.

Is 3D printing in high demand?Yes, 3D printing is in high demand, particularly for applications like rapid prototyping, custom manufacturing, and creating complex components across industries.

What is the profit margin on 3D printing?Profit margins in 3D printing can vary widely depending on factors like the type of printing services offered, target market, and cost structures. Some businesses achieve higher margins by focusing on specialized, high-value applications.

- Stratasys Ltd. Company Profile

- Materialise

- EnvisionTec Inc

- 3D Systems Inc

- GE Additive

- Autodesk Inc

- Made In Space

- Canon Inc

- Voxeljet AG

- Other Key Players

- Nestlé S.A Company Profile

- settingsSettings

Our Clients

- 102268

- Jan. 2024

| Single User $4,599 $3,499 USD / per unit save 24% | Multi User $5,999 $4,299 USD / per unit save 28% | Corporate User $7,299 $4,999 USD / per unit save 32% | |

|---|---|---|---|

| e-Access | |||

| Report Library Access | |||

| Data Set (Excel) | |||

| Company Profile Library Access | |||

| Interactive Dashboard | |||

| Free Custumization | No | up to 10 hrs work | up to 30 hrs work |

| Accessibility | 1 User | 2-5 User | Unlimited |

| Analyst Support | up to 20 hrs | up to 40 hrs | up to 50 hrs |

| Benefit | Up to 20% off on next purchase | Up to 25% off on next purchase | Up to 30% off on next purchase |

| Buy Now ($ 3,499) | Buy Now ($ 4,299) | Buy Now ($ 4,999) |